CAS News

Tax Breaks for Continuing-Care Retirement Communities

Paul F. Ciccarelli, CFP®, ChFC®, CLU®

For affluent seniors, a continuing-care retirement community (CCRC) can be an attractive alternative. These centers offer a full range of services, from independent living to skilled nursing. If you strolled through some of these CCRC campuses, you might think you were at a country club.

For those who could conceivably afford to live in a continuing-care retirement community, here’s a bit of good news: A little-known tax break could significantly lower your costs. Proper investment and tax planning can provide tremendous opportunities to enhance your future cash flow and financial positioning for the remainder of your lifetime.

The tax-saving idea here is that you may be able to deduct part of the CCRC’s one-time entrance fee and ongoing monthly fees as medical expenses. This is the case even if you currently live independently at the CCRC and require little to no care. In other words, you are allowed to claim a deduction for prepaid medical expenses, regardless of your current health status. Since the CCRC fees can be quite steep, significant write-offs may be allowed despite the 7.5% of adjusted gross income floor for deductible medical expenses.

The concept of prepaid medical deductions might sound too good to be true, but it is legitimate. For skeptical readers, consider the 2004 Tax Court decision, D.L. Baker v. Comm’r [122 TC 143, Dec. 55, 548 (2004)]. The Bakers decided to take their case to the Tax Court, which turned out to be a wise move – because they won big.

The Tax Court’s 2004 decision is good news for seniors because it confirms that you can treat a significant percentage of the one-time entry fees and recurring monthly charges as prepaid medical expenses. Even better, the amount that can be treated as medical expenses doesn’t in any way depend on the level of healthcare services you actually received during the year in question. They depend only on the CCRC’s aggregate medical expenditures in relation to overall expenses or revenue from fees paid by the residents. Any CCRC worth considering should have estimates of these percentages available for you to evaluate.

Because of the significant planning opportunities available to individuals moving into a CCRC, I strongly recommend that you seek advice from a qualified financial planner, a CPA or an attorney before making your final decision. Keep in mind that the deduction for the initial entrance fee and the ongoing monthly fees is a “use it or lose it” deduction. In other words, you will need to plan out your taxable income to ensure maximum benefit from these significant tax deductions.

Tax Reform – Will They or Won’t They?

You can be forgiven if you’re skeptical that Congress will be able to completely overhaul our tax system after failing to overhaul our health care system, but our advisors are studying the newly-released nine-page proposal closely nonetheless. We only have the bare outlines of what the initial plan might look like before it goes through the Congressional sausage grinder:

We would see the current seven tax brackets for individuals reduced to three — a 12% rate for lower-income people (up from 10% currently), 25% in the middle and a top bracket of 35%. The proposal doesn’t include the income cutoffs for the three brackets, but if they end up as suggested in President Trump’s tax plan from the campaign, the 25% rate would start at $75,000 (for married couples), and joint filers would start paying 35% at $225,000 of income.

The dreaded alternative minimum tax, which was created to ensure that upper-income Americans would not be able to finesse away their tax obligations altogether, would be eliminated under the proposal. But there is a mysterious notation that Congress might impose an additional rate for the highest-income taxpayers, to ensure that wealthier Americans don’t contribute a lower share than they pay today.

The initial proposal would nearly double the standard deduction to $12,000 for individuals and $24,000 for married couples, and increase the child tax credit, now set at $1,000 per child under age 17. (No actual figure was given.)

The chief architects of the GOP tax reform proposal – economic advisor Gary Cohn and Treasury Secretary Steven Mnuchin – unveiled their plan with the President at Trump Tower.

At the same time, the new tax plan promises to eliminate many itemized deductions, without telling us which ones other than a promise to keep deductions for home mortgage interest and charitable contributions. The plan mentions tax benefits that would encourage work, higher education and retirement savings, but gives no details of what might change in these areas.

The most interesting part of the proposal is a full repeal of the estate tax and generation-skipping estate tax, which affects only a small percentage of the population but results in an enormous amount of planning and calculations for those who ARE affected.

The plan would also limit the maximum tax rate for pass-through business entities like partnerships and LLCs to 25%, which might allow high-income business owners to take their gains through the entity rather than as income and avoid the highest personal brackets.

Finally, the tax plan would lower America’s maximum corporate (C-Corp) tax rate from the current 35% to 20%. To encourage companies to repatriate profits held overseas, the proposal would introduce a 100% exemption for dividends from foreign subsidiaries in which the U.S. parent owns at least a 10% stake, and imposes a one-time “low” (not specified) tax rate on wealth already accumulated overseas.

What are the implications?

The most obvious, and most remarked-upon, is the drop that many high-income taxpayers would experience, from the current 39.6% top tax rate to 35%. That, plus the elimination of the estate tax, plus the lowering of the corporate tax (leading to higher dividends) has been described as a huge relief for upper-income American investors, which could fuel the notion that the entire exercise is a big giveaway to large donors. But the mysterious “surcharge” on wealthier taxpayers might take away what the rest of the plan giveth.

But many Americans with S corporations, LLCs or partnership entities would potentially receive a much greater windfall, if they could choose to pay taxes on their corporate earnings at 25% rather than nearly 40%. (Note: The Trump organization is a pass-through entity.)

A huge unknown is which deductions would be eliminated in return for the higher standard deduction. Would the plan eliminate the deduction for state and local taxes, which is especially valuable to people in high-tax states such as New York, New Jersey and California, and in general to higher-income taxpayers who pay state taxes at the highest rate?

Currently, about one-third of the 145 million households filing a tax return — or roughly 48 million filers — claim this deduction. Among households with income of $100,000 or more, the average deduction for state and local taxes is around $12,300. Some economists have speculated that people earning between $100,000 and around $300,000 might wind up paying more in taxes under the proposal than they do now. Taxpayers with incomes above $730,000 would hypothetically see their after-tax income increase an average of 8.5%.

Big picture, economists are in the early stages of debating how much the plan might add to America’s soaring $20 trillion national debt. One back-of-the-envelope estimate by a Washington budget watchdog estimated that the tax cuts might add $5.8 trillion to the debt load over the next 10 years.

According to the Committee for a Responsible Federal Budget analysis, Republican economists have identified about $3.6 trillion in offsetting revenues (mostly an assumption of increased economic growth), so by the most conservative calculation, the tax plan would cost the federal deficit somewhere in the $2.2 trillion range over the next decade.

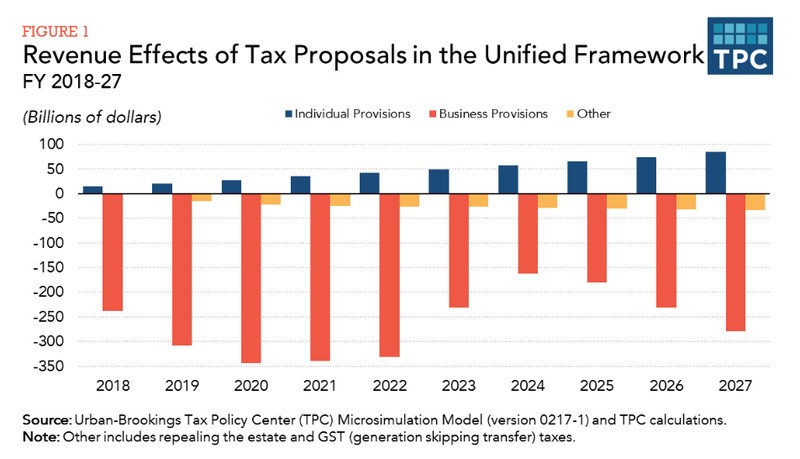

Others, notably the Brookings Tax Policy Center (see graph) see the new proposals actually raising tax revenues for individuals (blue bars), while mostly reducing the flow to Uncle Sam from corporations.

These cost estimates have huge political implications for whether a tax bill will ever be passed. Under a prior agreement, the Senate can pass tax cuts with a simple majority of 51 votes — avoiding a filibuster that might sink the effort — only if the bill adds no more than $1.5 trillion to the national debt during the next decade.

That means compromise. To get the impact on the national debt below $1.5 trillion, Congressional Republicans might decide on a smaller cut to the corporate rate, to something closer to 25-28%, while giving typical families a smaller 1-percentage point tax cut. Under that scenario, multi-national corporations might be able to bring back $1 trillion or more in profit at unusually low tax rates, and most families might see a modest tax cut that will put a few hundred extra bucks in their pockets.

Alternatively, Congress could pass tax cuts of more than $1.5 trillion if the Republicans could flip enough Democratic Senators to get to 60 votes. The Democrats would almost certainly demand large tax cuts for lower and middle earners, potentially lower taxes on corporations and higher taxes on the wealthy. Would you bet on that sort of compromise?

Special thanks to Bob Veres for his commentary.

How Secure Is Social Security?

If you’re retired or close to retiring, then you’ve probably got nothing to worry about – your Social Security benefits will likely be paid to you in the amount you’ve planned on (at least that’s what most of the politicians say). But what about the rest of us?

Media Onslaught

Watching the news, listening to the radio, or reading the newspaper, you’ve probably come across story after story on the health of Social Security. And, depending on the actuarial assumptions used and the political slant, Social Security has been described as everything from a program in need of some adjustments to one in crisis requiring immediate, drastic reform.

Obviously, the underlying assumptions used can affect one’s perception of the solvency of Social Security, but it’s clear some action needs to be taken. However, even experts disagree on the best remedy. So let’s take a look at what we do know.

Just the Facts

According to the Social Security Administration (SSA), over 60 million Americans currently collect some sort of Social Security retirement, disability or death benefit. Social Security is a pay-as-you-go system, with today’s workers paying the benefits for today’s retirees. (Source: Fast Facts & Figures about Social Security, 2016)

How much do today’s workers pay? Well, the first $127,200 (in 2017) of an individual’s annual wages is subject to a Social Security payroll tax, with half being paid by the employee and half by the employer (self-employed individuals pay all of it). Payroll taxes collected are put into the Social Security trust funds and invested in securities guaranteed by the federal government. The funds are then used to pay out current benefits.

The amount of your retirement benefit is based on your average earnings over your working career. Higher lifetime earnings result in higher benefits, so if you have some years of no earnings or low earnings, your benefit amount may be lower than if you had worked steadily.

Your age at the time you start receiving benefits also affects your benefit amount. Currently, the full retirement age is in the process of rising to 67 in two-month increments, as shown in the chart:

You can begin receiving Social Security benefits before your full retirement age, as early as age 62. However, if you retire early, your Social Security benefit will be less than if you had waited until your full retirement age to begin receiving benefits.

Specifically, your retirement benefit will be reduced by 5/9ths of 1 percent for every month between your retirement date and your full retirement age, up to 36 months, then by 5/12ths of 1 percent thereafter.

Example: If your full retirement age is 67, you’ll receive about 30 percent less if you retire at age 62 than if you wait until age 67 to retire. This reduction is permanent – you won’t be eligible for a benefit increase once you reach full retirement age.

Demographic Trends

Even those on opposite sides of the political spectrum can agree that demographic factors are exacerbating Social Security’s problems–namely, life expectancy is increasing and the birth rate is decreasing. This means that over time, fewer workers will have to support more retirees.

According to the SSA, Social Security is already paying out more money than it takes in. However, by drawing on the Social Security trust fund (OASI), the SSA estimates that Social Security should be able to pay 100% of scheduled benefits until fund reserves are depleted in 2035. Once the trust fund reserves are depleted, payroll tax revenue alone should still be sufficient to pay about 75% of scheduled benefits.

This means that in 2035, if no changes are made, beneficiaries may receive a benefit that is about 25% less than expected. (Source: 2017 OASDI Trustees Report)

Possible Fixes

While no one can say for sure what will happen (and the political process is sure to be contentious), here are some solutions that have been proposed to help keep Social Security solvent for many years to come:

♦ Allow individuals to invest their current Social Security taxes in “personal retirement accounts”

♦ Raise the current payroll tax

♦ Raise the current ceiling on wages currently subject to the payroll tax

♦ Raise the retirement age beyond age 67

♦ Reduce future benefits

♦ Change the benefit formula that is used to calculate benefits

♦ Change how the annual cost-of-living adjustment for benefits is calculated

Uncertain Outcome

Members of Congress and the President still support efforts to reform Social Security, but progress on the issue has been slow. However, the SSA continues to urge all parties to address the issue sooner rather than later, to allow for a gradual phasing in of any necessary changes.

Although debate will continue on this polarizing topic, there are no easy answers, and the final outcome for this decades-old program is still uncertain.

What Can You Do?

The financial outlook for Social Security depends on a number of demographic and economic assumptions that can change over time, so any action that might be taken and who might be affected are still unclear.

But no matter what the future holds for Social Security, your financial future is still in your hands. Focus on saving as much for retirement as possible, and consider various income scenarios when planning for retirement.

It’s also important to understand your benefits, and what you can expect to receive from Social Security based on current law. You can find this information on your Social Security Statement, which you can access online at the Social Security website, www.socialsecurity.gov by signing up for a my Social Security account. Your statement contains a detailed record of your earnings, as well as estimates of retirement, survivor, and disability benefits. If you’re not registered for an online account and are not yet receiving benefits, you’ll receive a statement in the mail every year, starting at age 60.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

A Tour of Italy!

Kim, Ray, Susie and Jan Kantor recently returned from their tour of Italy. They traversed several areas throughout “The Boot”, including Sperlonga, Pompeii, Rome and several destinations in Tuscany (see the map below).

Check out the following slideshows for some incredible photos showcasing Italian art, architecture and the Ciccarelli family!

Black – Sperlonga; Purple – Pompeii; Blue – Rome; Maroon – Terrasole Winery;

Orange – Assisi & Solomeo

Photos from Sperlonga

The ancestral homeland of the Ciccarelli family.

Photos from Sperlonga #2 – Wedding

Congratulations to newlyweds Rachel and Cory!

(Rachel is the niece of Kim, Ray, Paul and Jill; she is Gaynell’s daughter.)

Photos from Pompeii & Rome

Two ancient Italian cities, rich with history and stunning architecture.

Photos from Terrasole Winery & Brunello Cucinelli Factory

Fine wine and fashion…the pinnacle of Italian culture!

The Future of Brick-and-Mortar Retail

The rise of e-commerce has been a disruptive force in the retail sector. In fact, 5,300 store closings were announced in the first half of 2017 — about three times as many as during the same period in 2016. At this pace, the 2017 total should easily exceed the 6,163 store closings in 2008, the worst year on record. Retail bankruptcies have also been on the rise, with 345 companies filing by mid-year.1

A painful recession was to blame for thousands of retail store casualties in 2008, but for the most part, the U.S. economy has been humming along in 2017. The unemployment rate dropped to 4.3% in June, and gross domestic product grew at a 2.6% annual rate in the second quarter, driven by a 2.8% increase in consumer spending.2 So why is 2017 turning out to be such a tough year for retailers?

Structural Shakeout

Brick-and-mortar retailers are losing market share to e-commerce sites such as Amazon. Average monthly sales at department stores were $7.3 billion less in 2016 than they were in 2000, while non-store retail sales increased by $35 billion.3 The Internet also makes it easier for shoppers to research products and compare prices, reducing foot traffic in stores and limiting pricing power. Here are several more trends that have created challenges for the nation’s retailers.

Profit pressure. Even though many traditional retail chains have invested in e-commerce channels, online sales require higher technology, customer acquisition, and marketing costs than in-store sales, which reduces their profit margins. E-commerce sales increased to 15.5% of total sales in 2016, up from 10.5% in 2012, while retail margins fell from 10.5% to 9%, on average.4

Mall bubble. The shift to e-commerce was preceded by several decades of overbuilding. Between 1970 and 2015, the number of U.S. malls grew twice as fast as the population, leaving the United States with five times more shopping space per person than the United Kingdom, and 10 times more than Germany.5

Debt burden. Some companies are also struggling under heavy debt loads, making it more difficult to turn a profit and fund investments needed to compete in the e-commerce arena. Overall, the amount of retail debt rated by Moody’s has surged 65% since 2007.6

Reluctant shoppers. Many Americans (and especially young consumers) now prefer to spend their money on special experiences with friends and family (such as travel and restaurant meals) rather than material goods such as clothing and jewelry. For example, spending in restaurants and bars has grown twice as fast as all other retail spending since 2005. And 2016 was the first year ever that U.S. consumers spent more money eating out than they spent on groceries.7

Coping Strategies

Retailers that specialize in goods that are difficult to buy online (such as home improvement supplies) and stores that appeal to “bargain hunters” may fare better than pricier department stores and mall chains that mostly sell apparel and accessories, an e-commerce category that is growing quickly.8 Inside or outside of bankruptcy, many retailers are working to improve their future prospects by renegotiating more affordable leases and reducing their real estate “footprint,” which often involves closing underperforming stores and/or moving into smaller spaces.

Other common strategies include elevating the in-store shopping experience, focusing on exclusive brands, and using loyalty programs to reward and retain customers.9 Retailers are also working to integrate online and in-store sales channels, which makes it easier for customers to locate the items they want and finalize their purchases. To help generate online and in-store sales, many companies are using technology that tracks customer behavior and uses the data to create targeted marketing strategies and promotions.

Even so, as many as one-fourth of the nation’s 1,200 malls could close by 2022, primarily aging properties in less prosperous communities. A number of malls with advantageous locations are being redeveloped into lifestyle destinations with activities and entertainment (such as athletic facilities and concert venues) designed to attract foot traffic to the remaining stores and restaurants. Mall tenants are likely to become more diverse, with a wider range of service providers and fewer clothing stores.10

Economic Effects

Nearly 16 million people work in retail, many as cashiers or salespeople. From January to June, the U.S. economy shed about 71,000 retail jobs, and job losses could continue as long as the sector continues to struggle.11 E-commerce employment is expanding considerably, but most of these new jobs are in or near metropolitan areas. If large-scale dislocation of retail jobs continues, the economic effects could be worse for rural areas than for larger cities.12

The growth in e-commerce may also be holding down inflation. According to the PCE price index, inflation increased just 1.4% in June over the previous year.13 Consumers have largely benefited from lower prices resulting from intense competition among retailers, some of which now offer to match online prices. More household names could cease to exist in the coming months, and some of their competitors might even benefit from industry consolidation. In the end, a retail company’s long-term survival may depend on its ability to adapt quickly to an ever-changing market environment.

Sources

1) CNNMoney, June 23, 2017

2, 13) The Wall Street Journal, August 1, 2017

3) The Wall Street Journal, May 11, 2017

4, 8) The Wall Street Journal, April 21, 2017

5, 7) The Atlantic, April 10, 2017

6) The Wall Street Journal, July 17, 2017

9) The Wall Street Journal, February 28, 2017

10) The Los Angeles Times, June 1, 2017

11) The Wall Street Journal, July 19, 2017

12) The New York Times, June 25, 2017

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Passing the Torch to the Next Generation

Jill Ciccarelli Rapps | èBella Magazine | Aug • Sep 2017

As soon as your children or grandchildren are old enough to count, you should initiate the “money talk”. By fostering financial values within your family members at an early age, you can lay the groundwork for their continued financial growth and success throughout their lifetime.

Introduce your children or grandchildren to the concept of finance by discussing spending and saving in simple terms. As they get older, you can begin introducing them to more complex strategies: how to make their money work for them most effectively; priority spending; tips and tools for investing; and the pitfalls of misusing credit.

The resources outlined below will serve as indispensable guidelines that can benefit your children and grandchildren for years to come.

Five Secrets to Building Financial Independence

By nature of the relationship you share with your family, children and grandchildren depend on you to fulfill their financial needs. However, as they age, you should begin to instill a sense of independence. In other words, provide them with the values, tools and support they need to adequately meet their own needs.

Here are the five secrets to building financial independence:

1) Start at birth: Purchase a piggy bank for each child or grandchild shortly after they are born. As soon as you begin to educate them about money, provide them with an earnable allowance – and use the piggy bank as a tool to encourage regular savings. Have them save $0.50 or more out of each dollar they earn.

To make the savings process more fun and relatable, divide the piggy bank into various sections: retirement, education, charity, health care, etc. In doing so, younger family members will be more likely to see the value of saving consistently over time.

2) Talk about money regularly: Although discussions about money are often considered taboo in our society, financial conversations are one of the most critical topics you can discuss with your children or grandchildren.

Openly discuss financial topics around the dinner table with the whole family – with a particular focus on engaging children or grandchildren. Encourage all of your immediate family to play a role in conversations about developing budgets, prioritizing spending and selecting investments.

3) Impart smart values: Focus on positive messaging that helps them develop strong spending and saving habits. Help them foster a healthy attitude about money and guide them every step of the way. In doing so, they will start to make smart decisions on their own.

4) Lead by example: If you tell your children or grandchildren one thing while doing the exact opposite, they are not going to take your advice seriously. By exemplifying your advice in your personal financial life, younger generations are much more likely to follow your lead.

5) Do not misuse money in the relationship: Let your children or grandchildren earn their allowance from you. As a result, you will help to support their needs without creating a sense of entitlement. Also, never withhold money to make a point or as a punishment for bad behavior. Using money in this capacity will create a negative attitude towards finance that can lead them to make poor decisions down the road.

The Ten Commandments of Personal Finance

Once your children or grandchildren have grasped the basics of personal finance, introduce them to the Ten Commandments of Personal Finance. These principles provide the necessary framework that prepares your family for their financial future:

- Thou shall not put out more money than taken in.

- Thou shall spend money thinking of your future as well as your present.

- Thou shall remember that compound interest is never retroactive.

- Thou shall not collect credit cards or use them carelessly.

- Thou shall honor always thy debts and obligations.

- Thou shall develop a spending plan, “pay yourself first” by saving money, and start to invest systematically at an early age.

- Thou shall always search for reasonable returns on assets.

- Thou shall take advantage of 401(k) plans or other retirement savings options.

- Thou shall practice dollar-cost averaging in your investing.

- Thou shall obtain a financial education so as to be no one’s fool.

Knowledge + Values + Practice + Guidance = Success

As you continue to educate your children or grandchildren about money, the resources presented in this article will assist you in providing the knowledge and values that contribute to financial success. These principles are by no means a comprehensive guide; rather, you should supplement this information with your own knowledge of money and your deeply held values.

The next two steps to success are incumbent upon you: encouraging younger family members to incorporate this knowledge into their value system through continuous practice; while also offering the guidance and support they need to develop healthy financial habits.

A financial advisor may offer family meetings, educational summits, and other tools to assist you with these steps – ensuring that your insight and values are being effectively conveyed to the next generation.

When taken together, the combination of financial knowledge, time-tested values, consistent practice, and steady guidance will empower your children and grandchildren in their pursuit of lifelong financial success.

CAS Community Service Initiative 2017

Shy Wolf Sanctuary

Group #1 – Danni, Steve, Kristie, Jill, Andrew

Group #2 – Jasen, Theresa, Jess, Logan

Shy Wolf Sanctuary is a not-for-profit refuge for dozens of exotic, stray and injured animals – including wolves, wolf-dogs, cougars, coyotes and other animals.

In conjunction with United Way of Collier County, our CAS family sent two teams of volunteers to the sanctuary. We assisted with the landscaping on their beautiful 2.5-acre property, with an emphasis on removing plants that are toxic or dangerous to the sheltered animals.

We also managed to get some truly breathtaking photos of our experience! Thank you to our human and furry friends for the opportunity to serve.

Collier Child Care Resources

Andrea, Lynn, Kim, Susie, Jan, Kay

Collier Child Care Resources operates several early childhood care and education centers that serve families throughout Collier County. Driven by volunteers and donations, CCCR embraces a unique educational method that provides low-income children with the knowledge, skills and resources they need to succeed.

CAS sent a team of six volunteers to create a “documentation board” project that showcases the children’s artistic and academic work, while also assisting with sanitizing their toys and play space.

As both volunteers and sponsors of their “Business 100” program, we’re proud to support our friends at CCCR. The smiling faces of the children make it all worthwhile!

Rochester Family Fun Night 2017

Thank you to all of our client families who joined us at the Red Wings game on Friday!

We appreciate your continued trust and confidence.

Stepping Stones to Financial Independence

Jill Ciccarelli Rapps | Life in Naples Magazine | Aug • Sep • Oct 2017

For most Americans, financial independence is an important goal that motivates us throughout our entire lives. Even though our personal ambitions and goals may differ, we all share a common aspiration: generating enough money to live comfortably.

While many people think of work as a means to achieve financial independence – earning a salary to pay your bills and provide a high standard of living for your family – the term takes on a whole new meaning as you approach retirement. As a retiree, financial independence means that you are earning enough money from your investments and other assets to live your desired lifestyle.

Becoming financially independent requires a long-term commitment and a cohesive plan that can lead you towards your goals. Consider these “stepping stones” as you continue your journey to and through retirement!

Be patient. During your life, you will encounter many “get-rich-quick” schemes that promise wealth and success with little to no effort. However, as you probably have learned, very few people become wealthy overnight. Instead, the most effective way to achieve financial independence is to plan for the long term, stay committed to your goals, and make smart, stable investments.

Spend less than you earn. Each month, set aside a little money for savings before you pay your expenses; in other words, pay yourself first! The amount you save will vary based on your income and circumstances, but typically a 10-25% savings rate is a good goal to set (your financial advisor can provide you with more clarity). Over time, your regular savings habit will help you to develop resources for purchasing investments; then, your money can begin to compound and grow exponentially as you reinvest your returns.

Stay informed. Given all of the stocks and securities available on the market, it is important to consider the various factors that can impact your success as an investor. Understanding the current tax environment, inflation and interest rates will be critical in order to create an effective investment plan. In doing so, you will position yourself to build a portfolio that is stable and resilient, even amid the fluctuations of our economic climate.

Be proactive, not reactive. Neither the bear market nor the bull market will ever stay permanent; rather, the market is in a constant state of flux. When the market takes a turn for the worse, it can be difficult to focus on the long-term view – and many people end up making impulsive decisions that are not in their best interest. For this reason, you should be wary of reacting to the natural ebb and flow of the market. Instead, build a solid, proactive investment strategy and stay the course.

Of course, that is not to say that changing your investments is off-limits; but adjustments to your investment plan should reflect careful planning and analysis, not a spur-the-moment reaction to an emotional situation. By remaining calm, focused and logical when assessing your financial situation, you will be able to make smarter decisions that guide you towards financial independence.

Diversify. As the old saying goes: “Don’t put all your eggs in one basket.” A diversified approach to investing will strengthen your staying power (the ability for your portfolio to withstand fluctuations in the long run). As a result of this staying power, you will likely experience steady growth over time – cushioning your assets from volatile market conditions and mitigating your losses.

Seek professional advice. A professional financial planner provides the perspective and experience you need to identify and capitalize on opportunities to strengthen your portfolio. While many “DIY” investors are well-versed in market conditions and investment strategies, they often overlook these opportunities or make unforced errors along their journey to financial independence. Even if you consider yourself an expert on investing, seeking professional advice can greatly enhance your financial plan.

As a financial planner, I have witnessed the efficacy of these strategies in guiding my clients towards financial independence. While there are a plethora of factors to consider when creating a successful financial plan, the underlying theme is simple: save money early and consistently; invest proactively, not reactively; and seek guidance from the experts.

With these stepping stones to success, financial independence is easily within your reach.

Hale & Hearty: The Aging Dilemma

Should a 70-year-old American be considered “old”? Statistically, your average 70-year-old has just a 2% chance of passing away within a year. The estimated upper limit of today’s average life expectancy is 97 years old, and a rapidly growing number of 70-year-olds will live past age 100.

Perhaps more importantly, many 70-year-olds today are in much better shape than their grandparents were at the same age. So how do you define the term “old” in today’s environment of increasing longevity? In most developed countries, healthy life expectancy after age 50 is growing faster than life expectancy itself, suggesting that the “old age” period of diminished vigor and ill health is often deferred until a person has reached their early to mid-80s.

A recent series of articles in The Economist suggests that we need to devise a new term for people between the ages 65 to 80, who are generally “hale and hearty”; a group of individuals who are capable of performing knowledge-based work on an equal footing with 25-year-olds, but are increasingly being shunted out of the workforce by their younger counterparts. The article suggests that if this 65-to-80 cohort does not start participating in the workplace at a higher rate, the impact on our economy and society could be catastrophic.

Globally, a combination of falling birth rates and increasing lifespans threatens to increase the old-age dependency ratio – the ratio of retired people to active workers – from 13% in 2015 to 38% by 2100. This lopsided ratio could lead to major fiscal strains on our pension and Social Security systems, because fewer workers will be paying into the retirement benefits for an ever-increasing pool of retirees.

How can this dilemma be addressed? The articles note that whenever a new stage of life is defined and popularized, a wave of profound societal and economic changes have followed.

For instance, the conception of childhood in the mid-19th century paved the way for child labor and protection laws, compulsory schooling and the emergence of new businesses that focus on children (from toy making to children’s books). Another example: when teenagers were first identified as a distinct demographic in the 1940s, the value of the U.S. economy increased substantially as a result of their willingness to work part-time and to freely spend their income on new goods and services.

Instead of classifying people between the ages of 65-80 as “old” or “retired”, we should consider defining a new stage of life that recognizes the contributions of senior citizens and encourages capable people to continue participating in the workforce.

Fortunately, an increasingly large constituency of people ages 65-80 has transitioned into the “gig economy”, taking on part-time roles that emphasize knowledge and relationships. They are often content to work part-time, are not actively looking for career progression, and are better able to deal with the precariousness of such jobs. Businesses that seek on-demand lawyers, accountants, teachers, personal assistants and drivers are finding plenty of recruits among older people.

Still others are preparing for life beyond retirement by becoming entrepreneurs. In America, people between ages 55 and 65 are 65% more likely to start a new business than people who are 20-34 years old. In Britain, 40% of new business founders are over age 50, and 60% of employed people over age 70 are self-employed.

One of the largest economic contributions made by older people is often overlooked: volunteerism and child care support. More than 40% of Americans ages 65+ regularly volunteer their time and talent to serve their communities. In Italy and Portugal, about 20% of grandmothers provide daily care for a grandchild. That frees the parents to work longer hours and save a huge bundle on child care services.

All of these changes are indicative of a reality that is not well-publicized: that the traditional retirement age increasingly makes no sense in terms of our senior citizens’ health, longevity and ability to contribute to our society. The sooner we find an appropriate classification for healthy people between the ages of 65-80, the faster we can begin to fully appreciate their potential to contribute.