CAS News

Open House & Ribbon Cutting

On February 26, we held our open house and ribbon cutting ceremony to celebrate the opening of our new office, which combined the teams from our former Bonita and Naples offices.

The Greater Naples Chamber of Commerce, along with nearly 30 Chamber Ambassadors joined our Partners for the office ribbon cutting. An open house and reception followed with over 225 guests in attendance. All enjoyed wine, appetizers and desserts catered by Cappelli’s, music by local youth and great networking opportunities.

Preparing a Strategic Plan

by Anthony J. Curatolo

by Anthony J. Curatolo

Two years ago I began working with noted psychologist Dr. Bill Beckwith who specializes in memory management for individuals affected with mild memory loss and dementia. During the course of our collaboration, I became aware of how a decline in memory such as mild cognitive impairment or Alzheimer disease affects not only the forgetful person but also the family as a whole.

Try to imagine the impact on family members when, what took a few minutes and little thought, such as reconciling your checking account, now takes hours and can possibly be riddled with numerous errors. If the decline becomes severe, think of what stress it would be if your parent, husband, wife or sibling did not recognize you. If would be a truly sad and empty experience.

Memory loss may come on suddenly, as in the case of a head injury, stroke, medication side effects, etc., or it may come on gradually and progressively as in the case of Alzheimer’s disease. The good news about slow onset memory loss changes is that you can be proactive in maintaining your quality of life. Just as in managing finances, managing memory loss early may improve outcome.

Through Dr. Beckwith, I learned that dementia can be misdiagnosed or made worse by loss of hearing, severe depression, medication side effects, or sleep apnea. The key is to identify a baseline and monitor short term memory just as you do blood pressure or blood sugars. To date, there are no medical or vitamin cures to prevent dementia, but one can slow the process with exercise, a healthy diet and social activities. In fact, Medicare covers memory evaluation through approved providers.

It is important to distinguish the difference between natural aging and progressive memory loss. For example, it’s normal to forget your keys or where you park your car, but it’s not normal to forget that you own a car.

How does the caretaker cope with a loved one‘s progressive memory loss? How does one better cope with a progressive chronic disease? Dr. Beckwith recommends the solution to managing your memory is to know how your memory works and then create a strategic plan for your future, rather than waiting until the memory loss is serious and detrimental. Realize that your daily calendar is your best tool. It allows you to control not only what you have to do but also what you love to do. Remember the one minute rule “anything given less than one minute of thought will fade from your memory” to quote Dr. Beckwith.

How does this relate to financial planning? It’s advised to develop a documented plan for a good life, no matter what circumstances may present themselves along the way. We suggest a Plan for a Lifetime report to assist you and your loved ones in helping you maintain a good life. This report should include:

- Account numbers of all investments and their values, along with company phone numbers and possible online credentials

- List of how assets are titled and taxed

- List of all insurance contracts inforce, along with company phone numbers

- Identify who the beneficiaries are

- Identify who will manage the assets if you are unable

- Identify who will be the executor and do they know the responsibilities that come with the position

- Identify who will be your care provider, if necessary

- List of trusted advisors (accountant, attorney, etc.) and their contact information

- Funeral and legacy arrangements

- Best friend or spiritual advisor

This report should also include a flow chart mapping how money is to be distributed to loved ones and a budget for your surviving spouse so there is continuity in their lifestyle.

A methodical and thoroughly thought out plan ensures your money is passed to family members as you desire. This flow chart is particularly important when divorce, step-children and or ex-spouses are involved.

Money has a habit of evaporating with poor communications, especially when health issues or second marriage families play into the scenario. The wall we must overcome is the “Code of Secrecy” which is more common than not. Unfortunately, many families do not share money behavior patterns among members, which can lead to chaos and confusion during a period of crisis. What is critically important is working with a trusted financial advisory team to develop a transparent and strategic document so that those who survive you are well aware of the financial and legacy plan you have worked to put in place. Engaging a loved one in your financial management responsibilities and on the building of this life-long plan is an important aspect of the process.

Don’t ignore this process. Involve members of your family; most importantly your spouse. Talk with your advisor and review all documents and plans. Have your accountant and attorney engaged in the process and have all trusted advisors on the same page in regards to major decision making issues.

Dementia /Alzheimer’s are more feared than death. Losing your memory does not mean that you must lose your best friends and family members. Communication and transparency are paramount to reducing anxiety, family disappointments and legal fees in the face of an uncertain future.

It is a good idea to constantly build and communicate to all trusted parties. You may even consider making a short video of your life to include your best lessons to pass along to the next generation and in which you can share your philosophy of financial and wealth management.

Begin preparing your Strategic Plan for a Lifetime today, while you have the capability. Should there ever be a period of crisis and you do not have the ability to perform or make the decisions you do today, you may find that this plan will be of great value to you and your loved ones.

A Community Event for Women on Aging Gracefully

![]()

[aio_button align=”none” animation=”none” color=”orange” size=”small” icon=”none” text=”Click here to RSVP” relationship=”dofollow” url=”http://ciccarelliadvisory.com/newswp/health-wealth-event-sign/” target=”_blank”]

Please note, our event is currently full, but you are still encouraged to RSVP and be placed on our waiting list. Should a seat become available, we will contact you.

3 Keys to Living Longer and Maintaining Optimum Health & Wealth

A Community Event Especially for Women on Aging Gracefully

Featuring Expert Speakers:

Dee Harris, RD, LDN, CDE of D-Signed Nutrition, LLC

Gaynell Anderson, PT, CSCS of Absolute Physical Therapy of Southwest Florida

Jill Ciccarelli Rapps, CFP® of Ciccarelli Advisory Services, Inc.

Our daily food choices have a lot to do with keeping our brain

healthy. This program will teach you about foods and meal

plans that specifically enhance the memory center and help

reduce inflammation in our precious organ. We have the power

to think more clearly and keep our brain young!

– Dee Harris

Movement has become a leisure activity instead of a way of

life. Most of our health related problems can be prevented

and often resolved with one “miracle drug” known as motion!

Become empowered to gain optimal health and enjoy a healthy,

happy, pain-free and active life.

– Gaynell Anderson

Managing the cost of healthcare is one of the most complex

issues facing society today. Most retirees have no idea what

their real out of pocket expenses may be. This program will

help you to uncover various strategies to feel more secure

about your short and long term healthcare planning.

– Jill Ciccarelli Rapps

For more information about our speakers, Click here.

Join us for resources, education, discovery, inspiration, giveaways, & fun

Thursday, May 8, 2014 from 9:00-11:30 AM

9:00-9:30 AM Continental breakfast & discover local resources for living better

9:30-11:00 AM Featured presentation

11:00-11:30 AM Panel Questions & Answers

St. John the Evangelist Ballroom, 625 111th Avenue North, Naples, FL | For directions, click here.

To reserve your seat, click the button above or telephone 239-262-6577.

(Dee Harris and Gaynell Anderson are not affiliated with FSC Securities Corporation.)

Three-part workshop featuring McKenney Home Care

[aio_button align=”none” animation=”none” color=”orange” size=”small” icon=”none” text=”Click here to RSVP” relationship=”dofollow” url=”http://ciccarelliadvisory.com/newswp/mckenney-home-care-sign/”]

[aio_button align=”none” animation=”none” color=”orange” size=”small” icon=”none” text=”Click here to RSVP” relationship=”dofollow” url=”http://ciccarelliadvisory.com/newswp/mckenney-home-care-sign/”]

McKenney Home Care co-founders, Patrice Magrath and Michele McKenney, will be the special guest speakers at a series of workshops presented this winter in our Florida Office (Ciccarelli Advisory Services, 9601 Tamiami Trail North, Naples, FL 34108 – Click here for a map to our office).

The three-part series, Better Care for Better Living, will feature the following topics on the following dates:

- Part 1: Initiating Conversations about Care – Wednesday, January 22, 2014, 9:00-10:15 AM

- Part 2: Exploring the Continuum of Care Options – Tuesday, February 18, 2014, 9:00-10:15 AM or 2:00-3:15 PM

- Part 3: Implementing Care Decisions – Thursday, March 20, 2014, 9:00-10:15 AM or 2:00-3:15 PM

Please note: An additional afternoon session has been added to the February and March dates

The workshops will provide useful information and resources for starting dialogue with loved ones regarding responsibility and family dynamics. All sessions are free, but space is limited. To reserve your seat, please fill out the form at the bottom of this page.

“While 70% of us will need long-term care after the age of 65, few of us openly discuss care needs and wishes.” – Michele McKenney

McKenney Home Care was created by sisters, Patrice Magrath and Michele McKenney, who relocated to Naples after successful international careers in healthcare, law and business. Their own personal experience of caring for an aging mother inspired them to create a professional private pay agency designed to bring best practices in home health care to Southwest Florida. For more information about McKenney Home Care (ACHA License # 299994144), please visit www.mckenneyhomecare.com.

Our guest speakers:

Michele McKenney graduated from Boston College, received a master’s degree in Public Health from the University of Pittsburgh and a law degree from Duquesne University. She worked at the University of Pittsburgh Medical Center, starting as a graduate student at Eye and Ear Hospital and ending as President of two of the systems major divisions, Diversified Services and the International Division. As President of these Divisions, she had overall responsibility for the UPMC Home Health Agency, Senior Living Facilities, as well as, 21 other health related businesses. She was also responsible for the development and implementation of ISMETT, a specialty transplant hospital in Palermo, Italy.

Patrice Magrath graduated from Boston College then received a law degree from Catholic University, Columbus School of Law in Washington, DC. She practiced commercial law in DC with Swidler and Berlin (now Bingham McCutchen) then joined her sister in Palermo, Italy to oversee the development and opening of a respite facility for patients and families going to Palermo for medical treatment. She later returned to DC to work for SmithBucklin Corporation, a consulting firm managing not-for-profit organizations. Magrath was then recruited to Nyon, Switzerland to serve as the CEO of the International Osteoporosis Foundation where she was responsible for their global re-organization from 2009 to 2012.

McKenney Home Care is not affiliated with FSC Securities Corporation.

Come and celebrate our new office!

[aio_button align=”none” animation=”none” color=”orange” size=”small” icon=”none” text=”Click here to RSVP” relationship=”dofollow” url=”http://ciccarelliadvisory.com/newswp/open-house-sign/”]

Join us for a VIP event with Audrey H. Kaplan

[aio_button align=”none” animation=”none” color=”orange” size=”small” icon=”none” text=”Click here to RSVP” relationship=”dofollow” url=”http://ciccarelliadvisory.com/newswp/?p=772/” target=”_blank”]

Live in Naples

Audrey H. Kaplan

Senior Vice President, Senior Portfolio Manager, Head of Global Equity Management Team

Federated

Ms. Kaplan will be presenting a timely and very lively discussion on what economies around the world provide the greatest opportunity for growth and why. Please join us for… Where in the World are the Opportunities?

Wednesday, April 9, 2014 | 9:30 AM

Vi at Bentley Village in Naples | Click here for directions

Complimentary Valet Parking & Continental Breakfast

RSVP by April 4, 2014

Audrey Kaplan is responsible for portfolio management and research in the global equity area. She is a senior portfolio manager of Federated InterContinental Fund and Federated Global Equity Fund.

Kaplan managed the Rochdale Atlas Portfolio at Rochdale Investment Management, LLC in New York until it was acquired by Federated in 2007. She also was a hedge fund strategy consultant for Blue Crest Capital Management in London; worked in European quantitative strategy for Merrill Lynch in London; researched global emerging markets at Robert Fleming in London; and completed equity, fixed income and derivative analysis with Salomon Brothers in Tokyo and New York. She has 23 years of investment experience.

Kaplan earned a bachelor of science degree from Rensselaer Polytechnic Institute and a master in finance from London Business School. She is a member of the Society of Quantitative Analysts, Stamford Society of Investment Analysts, 100 Women in Hedge Funds, and the Quantitative Work Alliance for Applied Finance, Education and Wisdom.

Vi at Bentley Village, Audrey Kaplan and Federated are not associated with FSC Securities Corporation.

Maintaining Optimum Health & Wealth Online Webinar

Featuring:

Jill Ciccarelli Rapps

Financial Advisor, Vice President of Ciccarelli Advisory Services, Inc.

- Discover tips to help manage healthcare costs

- Uncover strategies for short & long-term healthcare planning

Dee Harris

Registered, Licensed and Certified Dietitian, Founder of D-Signed Nutrition, LLC

- Learn about foods and meal plans that enhance the memory center

- Develop ways to reduce inflammation and keep your brain young

Gaynell Anderson

Licensed Physical Therapist, Founder of Absolute Physical Therapy of Southwest Florida

- Become empowered to gain optimal health

- Discover how health related problems can be prevented through motion

Join us for the webinar Thursday, April 10, 2014 | 4:30-5:15 PM

Space is limited.

Reserve your Webinar seat now at: https://www3.gotomeeting.com/register/220487110

After registering you will receive a confirmation email containing information about joining the webinar.

System Requirements

PC-based attendees

Required: Windows® 8, 7, Vista, XP or 2003 Server

Mac®-based attendees

Required: Mac OS® X 10.6 or newer

Mobile attendees

Required: iPhone®, iPad®, Android™ phone or Android tablet

Dee Harris and Gaynell Anderson are not affiliated with FSC Securities Corporation.

Economic Update – Fourth Quarter 2013

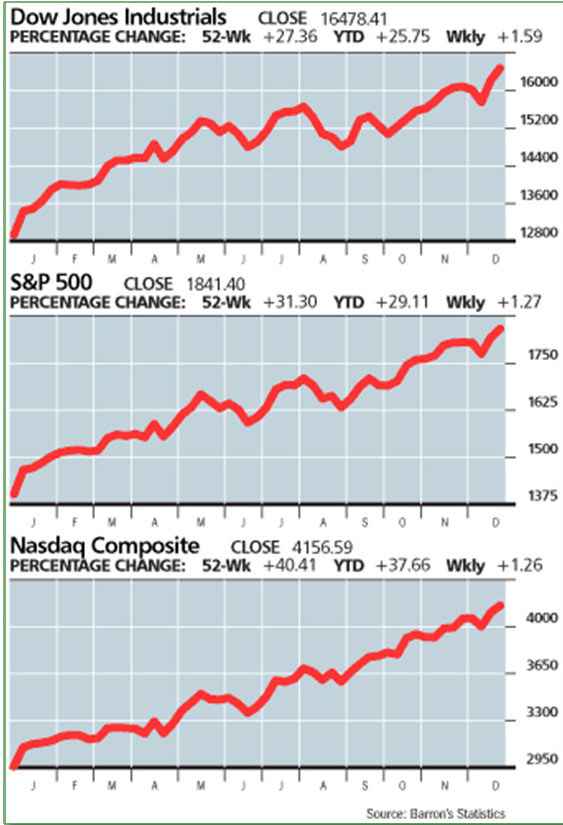

Wow – what a year! Federal Reserve chairman Ben Bernanke provided us with cheap credit for the 5th straight year, encouraging consumers to purchase big-ticket items, which kept the U.S. factories humming. These low interest rates pushed passbook savers and investors seeking conservative returns into the unpredictable securities market, which increased demand and in turn assisted in the increase of the markets. (Source: Barron’s, December 23, 2013)

The Dow Jones Industrials climbed 27% during 2013, logging its best annual performance since 1995. In fact, the Dow Jones achieved a record high 52 times last year. The S&P 500 and the NASDAQ Composite also experienced significant gains last year, with total returns of 30% and 32%, respectively. (Source: WSJ, Jan. 2, 2014)

The Dow Jones Industrials climbed 27% during 2013, logging its best annual performance since 1995. In fact, the Dow Jones achieved a record high 52 times last year. The S&P 500 and the NASDAQ Composite also experienced significant gains last year, with total returns of 30% and 32%, respectively. (Source: WSJ, Jan. 2, 2014)

2013 was certainly a year to remember. Let’s review some notable highlights:

- January 1st – Democrats and the GOP announced the budget deal that averted the fiscal cliff

- March 15th – the Cyprus banking crisis marked a turning point for Europe, with a new tax on many bank depositors

- March 28th – the Dow Jones Industrials and the S&P 500 finally surpassed their October 2007 highs

- May 22nd – Ben Bernanke notified Congress the central bank might taper the size of its bond-buying program, which had kept interest rates low and lent support to the economy and the stock market

- September 18th – the Fed decided not to taper and the markets reacted favorably

- October 1st & October 16th – Congress failed to strike a budget deal, and nonessential government services shut down

- November 22nd – the S&P 500 topped 1800 for the first time, a day after the Dow hit a new high above 16,000. (Source: Barron’s, Dec.16, 2013)

When you consider all of the problems that the economy encountered last year, including the prospect of reduced federal stimulus and the Federal Government shutdown, you might ask how we arrived at these above-average returns. The contributing factors included:

- Continued earnings and profit growth, even though it was at a very slow pace.

- Investors were willing to pay more for earnings in recent years, especially in 2013.

- Investors’ worst fears were not realized—the U.S. did not default on its debt, China didn’t experience a hard economic landing, interest rates remained low, and Europe’s debt crisis abated.

- U.S. consumers felt more upbeat about the economy in December than during the prior two months, recovering from pessimism about the October government shutdown (according to the Conference Board’s index of consumer confidence).

- Consumers are stepping up their spending, which is vital since it represents 70% of the economy.

- Steady economic growth gave investors more confidence that companies rated investment grade (the equivalent of triple-B-minus or higher) wouldn’t have problems paying back bondholders.

- A booming U.S. energy sector and rising overseas demand brightened the economic picture in the last quarter, sharply increasing estimates for economic growth and hope for a stronger expansion.

- A scarcity of attractive investments outside of equities brought numerous investors to the stock market, and the increase in money and demand helped boost returns.

- Buybacks have increased per-share profits and signaled management’s confidence. In the biggest of these buybacks, the Federal Reserve spent more than $1 trillion last year to purchase U.S. Treasury and agency paper on the open market to foster economic growth.

- Companies are returning cash to shareholders via dividends. Payouts by the S&P 500 have increased by nearly 15% in the past year, nearly triple the historical average. (Source: The Complete Investor, December 30, 2013)

Looking Ahead to 2014

Tapering, which is the easing of the U.S. Federal Reserve’s $85 billion-a-month bond purchases, could affect the economy in 2014. Tapering is a vote of confidence in the improvement in the U.S. economy. To be successful, the Federal Reserve must get the timing of any move right, and must make clear the distinction between tapering and an actual rate hike.

The Fed has not always communicated its intentions well, and this tapering could become a major cause for a rocky stock market. In 2013, mere mention of tapering sent jitters through the markets, with stocks dropping as much as 6% last spring after Bernanke, on May 22, 2013, broached the idea of stimulus removal.

When the Fed announced in December to “taper” or scale back its stimulus starting in January 2014, many investors simply shrugged off the announcement. Investors now worry that the Fed could make missteps under its new boss, Janet Yellen, who will replace Chairman Ben Bernanke on February 1, 2014. Until the market has time to become comfortable with Yellen, there is greater potential for error or misinterpretation.

Another concern is an increased probability of a market correction. The current bull market began in March 2009 and the S&P 500 has rallied 162% since then. “Typically, bull markets that last more than four years eventually are knocked off course because of a recession,” states Thomas Lee, investment officer at JPMorgan Chase. Despite this, many economists predict stocks rising about 10% on the basis of corporate fundamentals. Lower gains might seem boring, but boring could be just what we need to renew investor confidence. (Source: Barron’s, Dec. 16, 2013)

Many strategists will be keeping an eye on Washington to see if Congress can reach an agreement in the spring on raising the Federal debt ceiling. A bipartisan budget deal was finalized in December and that offers some hope that politics won’t derail the bull market.

Bond Market

The bond market experienced a negative year with the return for the Barclays U.S. Aggregate Bond Index down 2%, its first decline since 1999. Many economists are concerned that one of the biggest risks for the bond market is that the economic upturn could end up accelerating even more, causing a continuing bearish environment for bonds. Bond yields remain low by historical standards and returns could suffer if interest rates rise, weighing on bond prices.

Highly rated companies sold a record $1.111 trillion of bonds in the U.S. in 2013, even as the debt offered the worst returns in five years. (Source: WSJ, January 2, 2014)

Yields on 10-year Treasury notes, the bond market’s main benchmark, jumped from 1.6% last May to just over 3% in December. For the year, the yield rose 1.27%, its largest annual climb since 2009 as investors positioned for the Fed’s tapering to begin. (Source: WSJ, January 2, 2014)

Even with an improving economy, given what they’ve experienced in recent years, many companies are likely to remain reluctant to increase capital spending or make acquisitions. Yet they have a mounting pile of cash at their disposal. The companies that comprise the S&P 500 (excluding the financials) held cash and marketable securities of $1.36 trillion at the end of the third quarter – an 18% increase from the same period a year ago. (Source: The Complete Investor, December 30, 2013)

International Countries

Many market indexes throughout the world had double-digit percentage gains as easy-money policies washed over concerns about growth. Japan’s Nikkei Stock Average surged 57% for its biggest gain since 1972. Germany’s DAX gained 25%, France’s CAC-40 rose 18% and Spain’s IBEX 35 climbed 21%. (Source: WSJ, January 2, 2014) European equities could add 15% in 2014, according to the Barron’s survey of 12 market strategists. Most analysts see the good times continuing for at least a couple years beyond 2014. (Source: Barron’s, Dec. 30, 2013)

Inflation

Inflation measures were well below the Fed’s 2% target. Core inflation, which excludes food and energy, has been around the 1.1% level, year after year. Many believe that the lingering threat of inflation could result in monetary policy being looser than expected, fueling continued rallies in stocks and keeping bond yields relatively low. (Source: Bob LeClair’s, Dec. 28, 2013)

Gold

Many economists had predicted 2013 would be lucky for gold. It appeared that all the pieces that inspired rallies in 2011 and 2012 were still in place, and gold had a seemingly unstoppable 12-year bull run behind it. Instead, gold fell and ended the year with a 28% loss. Investors, seeing little need for safety as stocks rose and inflation barely budged, sent gold to its first annual loss since 2000.

Unemployment

The government reported the U.S. economy has added jobs for 35 straight months, unemployment has fallen to a 4½ year low, and employers are laying off fewer workers. As Mark Twain said, “there are three types of lies: lies, damned lies, and statistics.” On August 2013, the official unemployment rate fell to 7.3%, the lowest level since December 2008. The harsh reality, however, is that more than 4 million Americans have been unemployed for more than 6 months. Since 1994, the government only counts people as unemployed if they are receiving jobless benefits. Once the benefits run out, they are no longer considered by the government to be unemployed.

Some people are going back to work for minimum wage. Some Baby Boomers have decided just to retire at a very young age. Some have decided to go back to school. Many more have simply been beaten down by constant rejection. On average, there are now three unemployed workers for every job opening. Some have gone on disability or other welfare, or are no longer productive.

Even Ben Bernanke says that long-term unemployment had become a “national crisis.” John Williams, editor of Shadow Government Statistics, calculates the actual unemployment rate at more than 23%. “The unemployment rates have not dropped from peak levels due to a surge of hiring; instead, they generally have dropped because of discouraged workers being eliminated from headline labor-force accounting.”

What do you do with this bad news? Simply be cautious. Even while the overall outlook remains positive, it is always best to be aware of potential problems and understand that various risks remain.

Conclusion

Yes, there are risks, but let’s review a few of the reasons as to why the bull market might continue: consumers are optimistic, manufacturing continues strong, construction spending improves and auto sales are up. In fact, many economists believe that the risks that lay ahead are more likely to be political and international rather than economic. Sure, we would like faster growth and even more jobs, but at least we are moving in the right direction. (Source: Bob LeClair’s, January 4, 2014)

This year could be very confusing for investors. We are constantly monitoring the economic environment and our goal is to keep you aware as things change. If you have any immediate concerns about your specific investments or portfolio prior to your next review, please contact our office.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Indexes cannot be invested in directly, are unmanaged and do not incur management fees, costs or expenses. No investment strategy, such as asset allocation and rebalancing, can guarantee a profit or protect against loss in periods of declining values. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. The investor should note that investments in lower-rated debt securities (commonly referred to as junk bonds) involve additional risks because of the lower credit quality of the securities in the portfolio. The investor should be aware of the possible higher level of volatility, and increased risk of default.

The payment of dividends is not guaranteed. Companies may reduce or eliminate the payment of dividends at any given time.

International investing involves special risks including greater economic and political instability, as well as currency fluctuation risks, which may be even greater in emerging markets.

The price of commodities is subject to substantial price fluctuations of short periods of time and may be affected by unpredictable international monetary and political policies. The market for commodities is widely unregulated and concentrated investing may lead to higher price volatility.

Sources: Wall Street Journal (1/2/14), Barron’s (12/16/13, 12/23/13), Bob LeClair’s Finance (12/28/13, 1/4/14), Bob Livingston Letter (November 2013), The Complete Investor (12/30/13), American Spectator (November 2013)

Contents Provided by MDP, Inc. Copyright 2014 MDP Inc.

Gaining Knowledge from the Experienced Generation

Kim Ciccarelli Kantor | Naples Daily News | January 23, 2014

Kim Ciccarelli Kantor | Naples Daily News | January 23, 2014

Dealing with the financial histories of clients over the past 30 years has been a very valuable asset; a priceless treasure of experience and knowledge shared. If only these experiences and knowledge of our senior citizens, “the grandparents and parents” of our country, could be bottled and then digested by young adults, children, and grandchildren, it could be a very important step in the right direction.

This valuable source of information could alone help us make better decisions. No matter your age, the future starts right now, and the learning process never stops.

What advantages do our parents and grandparents offer us? They have gone past the idiosyncrasies that sometimes blind those of us in the trenches. When information is passed along to us from them, it is genuine. They are not motivated by an ulterior purpose.

I have noticed in my career that our senior citizens are not afraid to admit mistakes. They are honest and tell the truth inherent to affluence, to gaining knowledge, and to balancing our lives. Seniors are usually anxious to share, yet too few families benefit from this. Experienced investors and “survivors” have seen plenty of get-rich-quick schemes turn into quicksand. Today, in their later years, they understand the patience necessary to accomplish the goals they have defined for themselves. A wonderful attribute in sharing the retirement stage of my clients’ lives is that they know the difference between excuses and reasons; something the younger generation seems to have lost sight of. Our attitudes, as the younger generation, have to be re-cultivated and focused so that our perceptions are open to accept what life gives us, and to make the very best of it. Our attitude is most important.

Our parents and grandparents understand the necessity of sensible risk-taking. They lived through “the guarantees” of a proper retirement earning “good money” if they went to work at the local factory for X dollars an hour. They know they were taught wrong, only because of the lack of knowledge their parents had who did not understand taxes and inflation as the older generation does today.

Over the years, I have asked my older clients why they have not shared more of their experiences with their children and grandchildren. The answers were more common than unusual: “They have no interest” or “They haven’t asked.” In the process of estate planning, particularly open communications are vital. Sharing financial experiences can encourage

brighter more capable children.

I have asked younger family members why they did not “ask” or “have an interest.” I was surprised that in most cases they did not know how to ask and they do have an interest and a desire to learn.

Some suggestions for questions to open the door to meaningful communication with your senior mentors might be: What would you have done differently in your life if you had the choice? What were your goals when you were my age and how did you define them? Who were your mentors? What were the greatest tragedies in your life? What were your happiest

moments?

Balancing your attitude and financial decisions properly can be a difficult challenge; let’s seek all the experienced help we can and use it wisely. If only there could be a course on this.

I encourage you to seek experience and wisdom. Telephone your mom or dad, or grandparent today and schedule a breakfast. Ask questions that can lead to important research or homework necessary to make good decisions in our life experiences. You may find their primary purpose is for your happiness.

Economic Outlook & Stock Market Strategy featuring City National Rochdale

Featured speaker: Garrett D’Alessandro, Chief Executive Officer of City National Rochdale

Thursday, February 13, 2014 | 4:30 – 6:00 PM

Ciccarelli Advisory Services, Inc.

9601 Tamiami Trail North

Naples, FL 34108

(239) 262-6577

For directions to our office, click here.

Space is limited. To reserve your seat, please fill out the form at the bottom of this page.

About our speaker:

Mr. D’Alessandro joined the former Rochdale Investment Management (predecessor to City National Rochdale) in 1986 and is the Chief Executive Officer. In addition to setting the strategic direction of the firm, he plays a key role in the firm’s portfolio management and investment research functions. In this capacity he assists in determining the macroeconomic outlook and strategic asset allocations for the firm’s strategies. Prior to joining the firm, Mr. D’Alessandro was a Certified Public Accountant and an Audit Manager with KPMG Peat Marwick.

Mr. D’Alessandro received his MBA in Finance from the Stern School of Business at New York University. He holds the Chartered Financial Analyst designation, the Chartered Alternative Investments Analyst designation, and is a member of the New York Society of Security Analysts and the CFA Institute. He also is an Accredited Investment Fiduciary. Mr. D’Alessandro makes presentations on current investment issues to financial professionals throughout the country and has been featured in various media outlets including CNBC, The Financial Network, Practical Accountant, CPA Wealth Provider, and New Jersey CPA. Mr. D’Alessandro is an Ironman tri-athlete and has been selected multiple times to compete in the world championship in Kona, Hawaii. He is also a supporter of numerous charitable and civic organizations.