CAS News

The Longer Road Ahead? Women Baby Boomers Prepare for Retirement

Lynn A. Ferraina | Life in Naples Magazine | May, June, July 2015

Women are healthier, engage in more active lifestyles and are living much longer. Their retirement period could be as much as 20 years longer which creates both opportunities and challenges. Many women will spend as much time in retirement as they did in the workforce.

Some women were not in the workforce as long as their male counterparts which affects their savings for retirement. Companies that provide a monthly pension are no longer the norm. Many retirees will need to rely on their 401K, IRA, and personal assets accumulated during their working years. Whether you have 5 or 25 years until retirement if your company offers a 401k take advantage of it. Many companies offer a match or contribute a portion to your 401k on your behalf. If you qualify for an IRA strive to deposit the maximum each year.

If you have additional discretionary income to target toward retirement, consider making deposits to a non-retirement account. This creates an emergency fund which could be used before retirement if needed.

Eliminating debt before you reach retirement will help you have more discretionary income to live on. Make it a priority to pay off your credit cards in full each month, make additional payments on your mortgage and avoid home equity loans unless it’s an emergency.

More baby boomers are working part time in retirement either out of need or boredom. Many find they miss the day-to-day feeling of accomplishment that working can bring. Others found the cost of retirement was more than anticipated and need a part time job to make ends meet. Regardless of the reason, a part time job may offer an opportunity to try something different from your prior career – something new, interesting and rewarding.

Research early how to best apply for social security, typically three months before the time comes. Those born before 1937 can collect full benefits at age 65. Full benefits gradually increase to age 66 for those born between 1943 and 1954. After that, an older retirement age is phased in. To receive the maximum benefit, waiting to age 70 might be advisable. If you are a widow or can collect on a spouse’s social security, you need to know the rules. A beneficial tool to use is the Retirement Estimator. Visit www.SSA.gov/estimator for more information.

A few other tips ….In every woman’s life there comes a time to downsize. Get rid of the clutter and simplify your life. Invest in your health by exercising. When you eat out, order healthy choices, learn to cook Mediterranean diet meals. Not only will you feel better, you can potentially cut down on your medical expenses.

Have your affairs in order by documenting. Know where your investments are and how they are managed and diversified. Keep a log of all you own and are responsible for. Have your legal documents up-to-date, for example, your will, trust, healthcare surrogate and power of attorney. Give much thought to who you choose to make these important legal decisions for you. Document your insurance policies and when your premiums are due including life insurance, auto, health, home, long term care, disability, etc. Review your beneficiary designations periodically for changes.

Know how much you save and how much you spend each year and what you pay in taxes. Document your passwords, where your safe deposit box is and other important information to share with the person you trust if you become ill or incapacitated.

The knowledge, experience and support of a financial professional can help you put your affairs in order and to monitor the process annually. If their credentials are similar, choose the professional you feel you can communicate openly with. Ongoing communication is what makes any relationship work.

By taking time to empower yourself now, you will feel more self-assured and optimistic about your future.

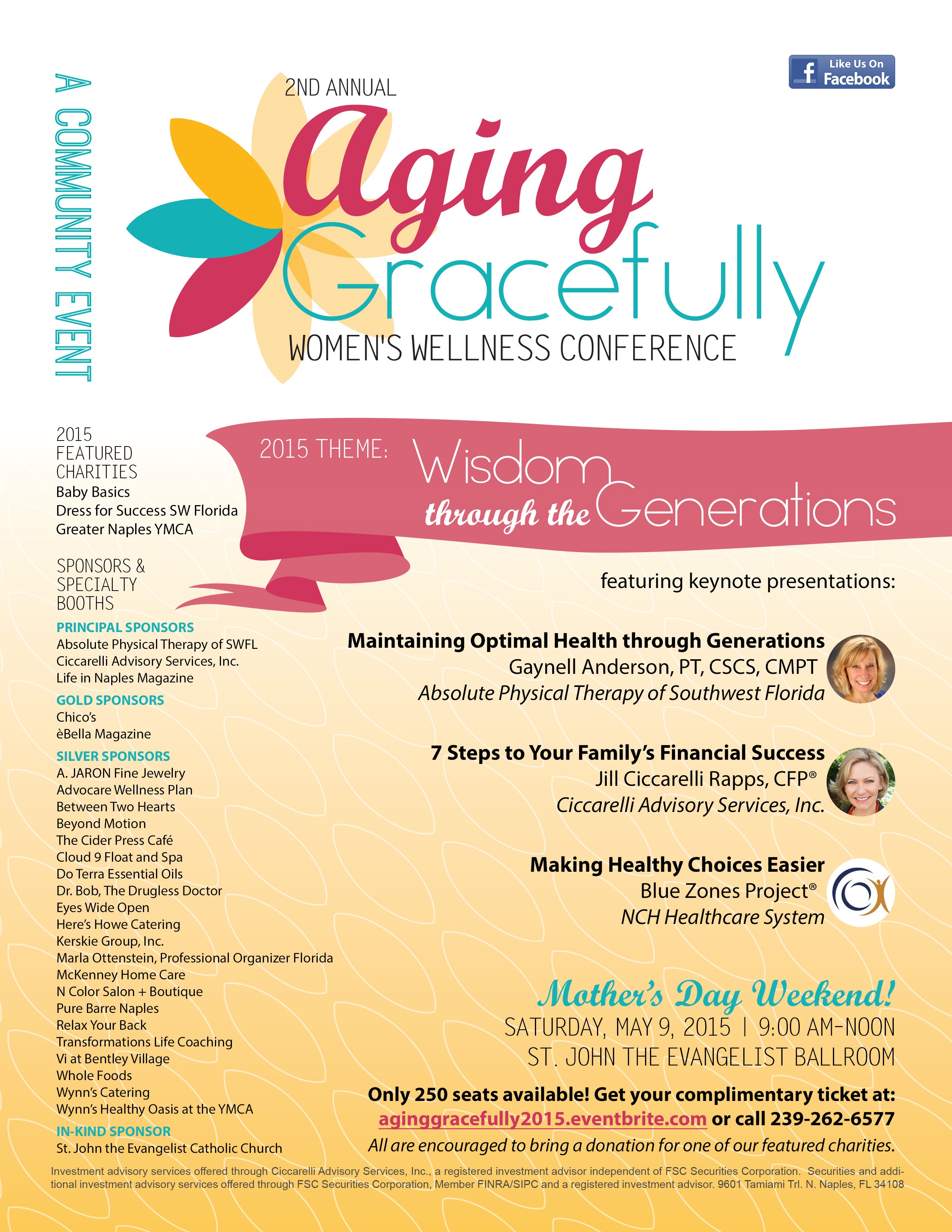

Aging Gracefully Conference draws hundreds of women of all ages

Over 250 women were in attendance for the second annual Aging Gracefully: Women’s Wellness Conference which was held on May 9th in Naples, FL. The conference, presented by Absolute Physical Therapy, Ciccarelli Advisory Services, Inc. and Life in Naples Magazine, gave women a chance to network with other women, visit sponsor booths to see what our community has to offer in the area of wellness and hear three inspiring keynote presentations.

Jill Ciccarelli Rapps, CFP® of Ciccarelli Advisory Services, Inc., kicked off the presentation portion of the conference by presenting ‘7 Steps to Your Family’s Financial Success.’ It was not a usual “how to invest and save for the future talk,” but more focused on setting goals, planning, enjoying life and sharing with others. The seven tips gave an overall sense of security, happiness and well-being.

Gaynell Anderson, PT, CSCS of Absolute Physical Therapy of Southwest Florida spoke on ‘Maintaining Optimal Health Through Generations.’ Attendees learned simple tips for exercising, stretching and building body strength, as well as the importance good posture has on entire body health.

The last presentation was delivered by Deb Millsap, executive director of the SWFL Blue Zones Project®. She showcased how the Blue Zones Project®, spearheaded by NCH Healthcare System, will help with ‘Making Healthy Choices Easier’ in Collier County. Millsap encouraged attendees to get involved in making their world a safer, healthier place to live.

The conference, along with speakers and sponsor displays, gave women of all ages a chance to examine their own lives and answer questions that could lead them to a healthier and happier life. Event co-organizer, Jill Ciccarelli Rapps said that this year’s theme, ‘Wisdom through the Generations,’ really represented those powerful lessons that mothers pass to their daughters and granddaughters.

There were a number of sponsors helping to make the event possible. Each one was on-hand with information and/or samples of their products or services. They were: Chico’s and é Bella Magazine, along with A.JARON Fine Jewelry, Advocare Wellness Plan, Between Two Hearts, Beyond Motion, The Cider Press Café, Cloud 9 Float and Spa, Dō Terra Essential Oils, Dr. Bob – The Drugless Doctor, Eyes Wide Open, Here’s Howe Catering, Kerskie Group Inc., Marla Ottenstein – Professional Organizer Florida, McKenney Home Care, N Color Salon + Boutique, Pure Barre Naples, Vi at Bentley Village, Whole Foods, Wynn’s Catering, Wynn’s Healthy Oasis at the YMCA, and St. John the Evangelist Catholic Church.

Sponsorship dollars from the conference will be donated to this year’s three featured charities: Baby Basics, Dress for Success SW Florida, and the Greater Naples YMCA. For more information on the speakers please visit absoluteptswfl.com, CASMoneyMatters.com, and southwestflorida.bluezonesproject.com. To inquire about next year’s conference or for volunteering or sponsoring opportunities, please call Ciccarelli Advisory Services, Inc. at 239-262-6577 or email Ciccarelli@CAS-NaplesFL.com.

Gaynell Anderson and Deb Millsap are not affiliated with FSC Securities Corporation.

Video: Economic Rebound

Three Steps to Develop Your Best Long-term Health Plan

Jill Ciccarelli Rapps | Life in Naples Magazine | April 2015

Walt and Doris are a charming couple in the early sixties who came in to assess whether they were ready for Walt to retire. They wanted to pay off the house, travel a little and spoil their grandchildren. Not a bad plan overall.

It wasn’t long before they found a serious shortfall in their financial plan: long-term healthcare. Both Walt and Doris are in excellent health, but Walt’s parents died of heart disease in their 70s, and while Doris’ parents are in their late eighties, they have spent many years in assisted living facilities. Now, Walt and Doris might both live long lives with limited health expenses covered totally by Medicare, but they need to be prepared that one or both of them could have significant healthcare costs over the next twenty years.

While nobody likes to think about these scenarios, your retirement plan is not complete without some accommodation for long-term healthcare. The difficult part is guessing what kinds of care you could possibly need several years out that would not be covered by your insurance or Medicare. We have had clients in their sixties who needed long-term care, older clients whose health took a turn suddenly, and others who lived vibrant lives into their nineties. For a couple like Walt and Doris, their costs could range anywhere from $202,415 to $947,188 apiece when they may need long term care.

To be truly prepared for retirement, you need to develop your personal healthcare strategy. Part of it is staying fit and active, but the other part is ensuring that you have adequate assets in place to cover whatever unforeseen costs may arise. It’s never too early to put a strategy in place to ensure that you and your spouse receive the best care you can when you need it.

People who don’t take three essential simple steps may be setting themselves up for a very bumpy road through retirement.

Step 1 – Be Aware. Healthcare will likely be your largest expense in retirement, second only to your home, so it’s critical that you have a plan. It is no longer safe to assume a large insurer – or the federal government – will cover most of the cost going forward. We need to be prepared to shoulder a larger financial responsibility for our own care. The average premium for a couple in their fifties – not including proactive care – can exceed $15,000 a year, not counting deductibles and out-of-pocket expenses.

Step 2 – Educate. It’s important to understand what Medicare covers at age 65. Part A – “hospital insurance” – is involuntary and covers inpatient hospitalization, skilled nursing facilities, home health care, and hospice. Part B – “medical insurance” – covers doctors and providers, preventive benefits, durable medical equipment and outpatient services. Part B is voluntary and premiums are based on your modified adjusted income. Typically, you will also have a deductible and a 20% coinsurance on some services. “Medigap” and prescription supplemental insurance cover most gaps that Medicare A and B will not cover. Walt’s brother Bruce is 65 and he and his wife pay $7,581 per year for their premiums and supplements.

Step 3 – Assess. We use current cost of care, projected lifespan, and inflation to estimate an average annual cost over the rest of your and your spouse’s lifetime for out-of-pocket expenses and the projected cost of what long term care may cost on top of this. In Walt and Doris’ case, their average out-of-pocket cost of care may be $21,062 a year. They needed to adjust their investment portfolio to prepare for that extra cost. Now, our assessment did not include things that Medicare doesn’t cover completely, like pro-active physical therapy, chiropractic care, personal trainer services, and alternative care options, but these may be things you would want to consider as well. Most importantly the above figure does not include long term health care which Medicare does not cover.

The Official U.S. government Medicare Handbook, Medicare & You, 2013. Medicare Part D premiums are on average about $400 per year (varies by State) and are subject to the plan a person selects. Medigap Insurance can vary by carrier and state. The average plan in 2011 was $178 per person per month for an annual cost of about $2,136. Fidelity Consulting Services, 2010. Based on a hypothetical couple retiring in 2010, 65 years or older with average (82 male, 85 female) and longer (92 male, 94 female) life expectancies. Estimates are calculated for “average” retirees, but may be more or less depending on actual health status, area, and longevity.

CAS Rochester – Spring Clean Up Shredding Party

Join us Saturday, June 13, 2015 at our Rochester office, 110 Linden Oaks from 10:00 AM until Noon for our “SPRING CLEAN UP SHREDDING PARTY”. Confidential documents placed at the curb for disposal or recycling offer identity thieves an opportunity to strike. Since all documents will be shredded and recycled, this collection offers our clients the chance to protect their personal information while doing something positive for the environment.

Join us Saturday, June 13, 2015 at our Rochester office, 110 Linden Oaks from 10:00 AM until Noon for our “SPRING CLEAN UP SHREDDING PARTY”. Confidential documents placed at the curb for disposal or recycling offer identity thieves an opportunity to strike. Since all documents will be shredded and recycled, this collection offers our clients the chance to protect their personal information while doing something positive for the environment.

We will shred your documents while you WATCH! You do not have to remove staples, but no plastic please. Think about destroying your old life insurance and annuity policies, tax returns, old cancelled checks, or whatever you have been saving! Please let us know if you are planning on coming by calling 585-383-0180. This event will go on rain or shine. Coffee and donuts will be provided.

2nd Annual Aging Gracefully

DATE: Saturday, May 9th

TIME: 9:00 AM – Noon

WHERE: St. John the Evangelist Catholic Church Ballroom, 625 111th Ave N, Naples

TICKETS AVAILABLE AT: aginggracefully2015.eventbrite.com or call 239-262-6577

Economic Update – First Quarter 2015

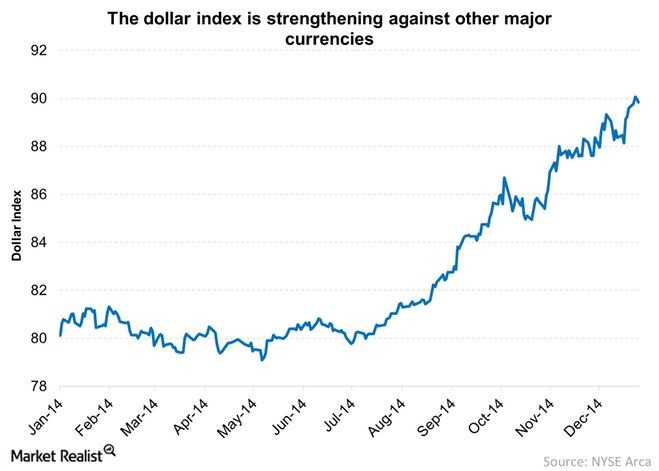

Many market strategists predicted that volatility would return to the equity markets in 2015, and the first quarter proved them right as stocks plunged, soared and then plunged again. During the first 3 months of 2015, the dollar strengthened, oil weakened, and monetary policy became a little less certain.

Many market strategists predicted that volatility would return to the equity markets in 2015, and the first quarter proved them right as stocks plunged, soared and then plunged again. During the first 3 months of 2015, the dollar strengthened, oil weakened, and monetary policy became a little less certain.

By the end of the quarter, the S&P 500 index finished about where it started. However, some of the movements in individual stocks and sectors were extreme. The S&P 500 rose approximately 0.4% for the first three months of 2015, but that benchmark moved at least 1% on nearly a third of the quarter’s trading days, says SunTrust strategist Keith Lerner. This statistic compares with just 15% of all trading days for 2014.

Lerner attributes these turbulent moves to the combination of factors that have become repetitive themes including the rising dollar, falling oil prices and the uncertainty surrounding Federal Reserve monetary policy. “The market can handle one or two things at one time,” he says. “We’ll get a tug of war till there is clarity.” (Source: Barron’s, 3/2015)

The fact that the market has been oscillating by macro forces does not mean that investors cannot succeed. Awareness of how these moves within currencies, commodities and interest rates could affect stocks and sectors can help investors with their decisions. The combination of all forces that took place in this first quarter actually balanced out the S&P 500 return, which is why it finished close to where it started. Still, certain industry sectors were affected more this quarter than others. Some connections are easier to see than others. For example, the energy sector has tracked the price of oil, while utilities, with their large dividends, could be more affected by a rise in interest rates. The fact that investors are concerned that the Fed will raise interest rates at some point in 2015 can help explain why utilities dropped 6% during the first three months of 2015. Similarly, the 10.6% decline in oil prices during the first quarter can be closely connected to the energy sector’s drop of 3.6%. Some sectors were less affected by some of the recent macro risks. Goldman Sachs strategist David Kostin noted that while utilities and energy sectors had high levels of macro risk, consumer discretionary and tech were less susceptible this quarter. The bottom line is still that investors should always be aware and cautious. (Source: Barron’s, 3/2015)

Interest Rates

Interest rates and Fed watching continues to play a role for investors in 2015. Ever since the Fed ended its bond buying program last October, investors have been wondering when the Fed will finally raise interest rates. There has been no clear answer and investors still need to be patient. The good news is that the uncertainty that comes before the first rate hike might cause more volatility than the rate hike itself.

The short term interest rate has been 0% since late 2008. In a speech given on Friday, March 27, Federal Reserve Chair Janet Yellen offered conditions for the central bank’s interest rate policy. She said that the initial increase from the 0% – 0.25% target range that was set for the federal-fund rate in December of 2008 should come later this year. She added that the upward trajectory of future rate hikes would be moderate and will depend on incoming economic data.

Yellen felt that equity markets were more pessimistic than the Fed and added that we should not expect a mechanical elevation in rates. She also said that if the data dictates it, the central

bank is prepared to hike rates. (Source: Barron’s 3/2015)

Many economists speculate that an interest rate hike is inevitable in the near future as the job market is doing well, the dollar is strong and home sale values have ticked up. “God forbid something happens in the world and the Fed needs some policy tools to try to aggressively stimulate economic growth here or abroad,” says Phil Orlando, chief equity strategist at Federated Investors. “With the funds rate at zero, they’ve got no bullets to employ. So what they want to do is reload the gun, if you will, and get back to some neutral level of the funds rate over the next couple years.”

Many economists speculate that an interest rate hike is inevitable in the near future as the job market is doing well, the dollar is strong and home sale values have ticked up. “God forbid something happens in the world and the Fed needs some policy tools to try to aggressively stimulate economic growth here or abroad,” says Phil Orlando, chief equity strategist at Federated Investors. “With the funds rate at zero, they’ve got no bullets to employ. So what they want to do is reload the gun, if you will, and get back to some neutral level of the funds rate over the next couple years.”

What’s important to keep in mind is that an interest rate hike is likely still a few months off. Some say the earliest reasonable target date for a rate hike could fall in June, while others speculate the announcement will come closer to the end of this year or even sometime in 2016.

Orlando says the announcement likely will coincide with a meeting and press conference. Federal Reserve Chair Janet Yellen and the Federal Open Market Committee don’t speak with the press after each one of their meetings, so Orlando speculates that an announcement is likely to come out of their June meeting or the session scheduled for September.

If the U.S. Central Bank were to raise rates they would be going against the tide of rate cuts and other monetary-easing measures currently being taken by their counterparts abroad. Specifically, the European Central Bank announced in March the terms of its quantitative easing program. They are instituting this in the face of a negative interest rate environment.

The People’s Bank of China, housed in the world’s second largest economy, became the latest of 20-odd central banks this year to cut rates after a reduction in their growth target to “around 7%.” (Source: Barron’s 3/2015)

The changing of interest rates or even comments suggesting movements continue to create noise and news for investors. As financial professionals, we intend to be very watchful of both the Federal Reserve’s actions and interest rates this year. It seems as if everything is filtered through the lens of monetary policy. For example, when investors learned that the U.S. had added nearly 300,000 jobs in February, the S&P 500 tumbled because it signaled to some that the Fed might be forced to raise rates sooner to curb an overheating economy. Then a lackluster consumer spending report in March caused stocks to surge, because it signaled that the Fed could now afford to wait. “Everyone is playing economist, not trader,” says Michael Block, strategist at Rhino Trading Partners. (Source: Barrons, 3/2015)

Should you have any concerns about your holdings we would be glad to recheck your personal situation during your next review or at any other time.

Oil Prices

Oil Prices

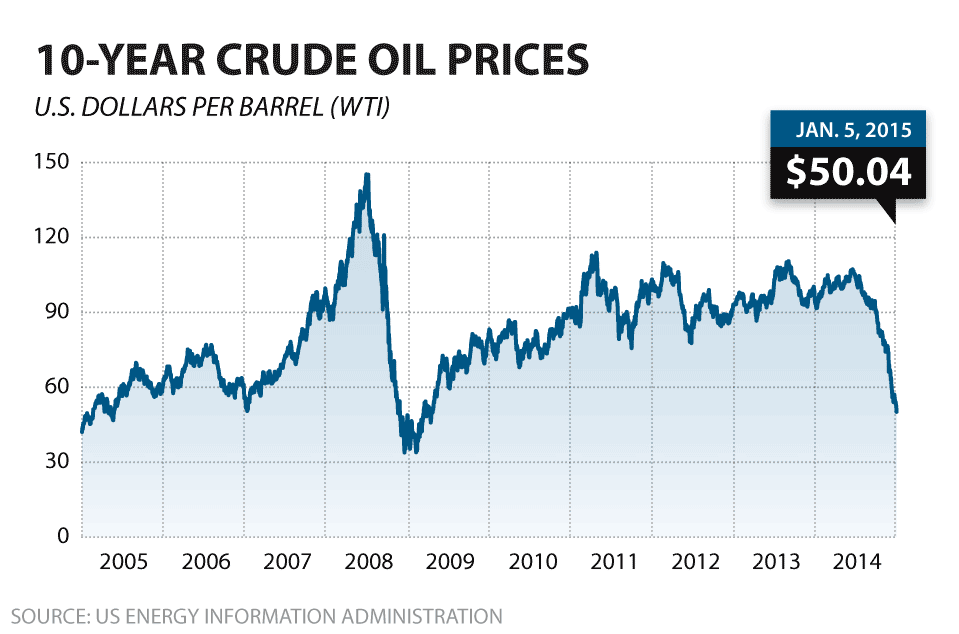

Along with interest rate movements, oil prices continue to be another area that investors should pay attention to. The price of oil, down over 50% in the last seven months, is creating issues beyond even the energy markets.

Moody’s Investors Service analysts link oil’s falling prices to sectors that might benefit from increased consumer purchasing power. With oil prices down and people spending less at the pump, they should have more money in their pockets. “The average U.S. household will spend about $550 less on gas in 2015 than in 2014,” the Moody’s analysts said, citing data from the U.S. Energy Information Administration. They go on to conclude that, “oil price declines act like a tax cut enabling consumers to spend a greater percentage of their incomes on non-energy goods and services.” (Source: Barron’s, 3/2015)

Falling oil prices can hurt those extracting oil and oil service companies. They are expecting lower profits and this could affect jobs. Plummeting oil prices also add challenges for alternative energy sources like solar and wind power suppliers. Lower oil prices have resulted in a decline of many stocks dependent on energy. On the positive side, lower oil prices keep energy costs down for manufacturing companies and transportation companies.

“It’s a net positive for the U.S. economy,” says Don O’Neal, a portfolio manager at American Funds with 33 years of investment experience. He adds that, “It’s really good for the consumer and for a whole range of consumer products. But there is an offset – not all sides are benefiting from low oil prices.” (Source: American Funds, 3/2015)

The fluctuations of oil prices can continue to yield uncertainty for investors. As 2015 continues, this is another area that we will be watchful of.

Earnings and Currency Concerns

Earnings and Currency Concerns

Several market strategists are predicting a rocky earnings season for companies in the first quarter of 2015. The two biggest culprits behind the projected declines are the price of oil and the strength of the U.S. dollar.

The price of WTI (West Texas Intermediate) crude averaged $48.21 for the first three months of 2015 compared to $100.50 in the first three months of 2014, a more than 50% decline. This plunge in price means that energy sector companies have slashed their earnings guidance by 60% according to Dan Greenhaus of BTIG. He adds that overall earnings would rise 2% if you were to exclude the energy sector from the overall results. Meanwhile, the U.S. dollar index averaged $96.14 during the first quarter of the year compared to $80.33 for the same period in 2014 — a 20% year-over-year jump. While this is a great thing for Americans looking to travel or a U.S. company with little to no foreign sales, it’s bad news for a large portion of the S&P.

“The S&P 500 derives about 40% of sales from overseas, therefore relying heavily on global strength,” Christine Short, an analyst at Estimize, explained in a research note. “These companies hail from a variety of sectors — materials, industrials, information technology, consumer staples, and consumer discretionary — proving that the impact will be broad based as almost all sectors will feel forex fluctuations to some degree, with the exception of telecommunications and utilities which are mostly domestically focused,” Short explained.

S&P Capital IQ analyst Sam Stovall wrote in a recent note, “Even though the forecast for S&P 500 EPS (earnings per share) in Q1 is expected to decline 3%, history shows that actual results have been two to four percentage points higher than initial estimates.” He goes on to add that, “As a result, there is still a possibility that EPS will rise, thereby delaying the start of an EPS recession.” (Source: Forbes, 3/2015)

Global Markets

The start of 2015 has suggested that many monetary authorities were becoming responsive to weak growth outlooks and upwards pressure on their currencies. More than 20 countries eased their monetary policy already in 2015, with several countries like Sweden and Denmark even implementing negative interest rates to protect their currencies. (Source: Fidelity, 3/2015)

At the beginning of 2015, the consensus amongst most analysts was that U.S. equities were the place to be. The U.S. economy seemed to be expanding and Europe and the rest of the world did not have the same strength. A recent survey from Bank of America Merrill Lynch infers that a net 19% of global asset allocators are currently underweight U.S. stocks by the largest margins since 2008. This is a dramatic shift from their net overweight positions reported in February. (Source: Barrons, 3/2015)

The current peaking of growth in certain countries has created cause for concern. Inflationary pressures still seem to be absent and corporate profits are still looking solid. On a positive note, the European Central Bank’s quantitative easing program has surpassed market expectations. With the Eurozone emerging from a mid-cycle slowdown, economic sentiment has moved higher in recent months. With the manufacturing sector expanding, a cheaper currency, lower oil prices and banks easing lending standards, Fidelity analysts conclude that though still slow, Europe is showing clear signs of an improving mid-cycle expansion.

The current peaking of growth in certain countries has created cause for concern. Inflationary pressures still seem to be absent and corporate profits are still looking solid. On a positive note, the European Central Bank’s quantitative easing program has surpassed market expectations. With the Eurozone emerging from a mid-cycle slowdown, economic sentiment has moved higher in recent months. With the manufacturing sector expanding, a cheaper currency, lower oil prices and banks easing lending standards, Fidelity analysts conclude that though still slow, Europe is showing clear signs of an improving mid-cycle expansion.

After a multi-year property and credit boom, China seems to be approaching a cyclical downturn. Fidelity’s global market analysis summed up China’s economy by saying, “China continues on a decelerating trend with an elevated risk of a growth recession.”

Japan, on the other hand, seems to be in a mild recession. In April of 2014, the Japanese government implemented a consumption-tax hike that caused a downturn in demand. Although they are in a mild recession, lower oil prices and a weaker yen may have Japan’s economic woes bottoming out.

The weakness in oil has had an effect on many countries worldwide. Those countries that are leading oil exporters are obviously the ones that are being affected the most. The U.S. economy continues to be strong and although analysts are predicting a slowing effect, global growth is still on the positive side. The global backdrop coupled with the weakening of certain countries’ currencies could create further volatility for investors in 2015. While a strong dollar can benefit some sectors, it will adversely affect others. Investors should continue to be watchful of business cycle conditions in both the U.S. and overseas.

Conclusion: What Should an Investor Do?

Ultimately, predictions are just that: predictions. While investors need to be watchful of oil prices, the dollar, and even bad weather, the actual results could end up looking much different than the projections look now. So what can investors do?

Continue to be watchful. Even the most optimistic investors need to be watchful of the warning signs.

Focus on your own personal objectives. During confusing times it is always wise to create realistic time horizons and return expectations for your own personal situation and to adjust your investments accordingly. Understanding your personal commitments and categorizing your investments into near-term, short-term and longer-term can be helpful.

Revisit your risk tolerance. Investopedia defines risk tolerance as an individual having a realistic understanding of his or her ability and willingness to stomach large swings in the value of his or her investments. With the return of more frequent volatility, we would be glad to talk about any changes to your risk tolerance during your next review or at any other time.

Discuss any concerns with us.

Our advice is not one-size-fits-all. We will always consider your feelings about risk and the markets and review your unique financial situation when making recommendations.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

A knowledgeable and informed financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. The P/E ratio (price to earnings ratio is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher P/E ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower P/E ratio. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Tips to Reducing the Risk of Identity Theft

By Carrie Kerskie

By Carrie Kerskie

Every three seconds someone becomes a victim of identity theft. Florida is number one in the country for identity theft complaints. Naples is number three in the country nationwide for identity theft complaints. No one is immune from identity theft. In fact, there is nothing you can do or a service you can buy that will prevent it from happening to you. However, there are steps you can take to reduce your risk of becoming a victim.

MySSA

The Social Security Administration (SSA) has launched My Social Security Account (MySSA) which permits you to manage your benefits online. To create your account visit www.SSA.gov and click in the box where it says “my Social Security”. You will be required to enter your name, address, date of birth and social security number. Note: the site uses the latest security measures to protect your information. Next you will be asked a series of questions based on your Experian credit report. Questions such as: how much is your mortgage payment, what is the address of the property where you have the mortgage, or how much is your car loan payment. After answering the questions you will be able to view your benefits. You can also change your deposit account or you can file for benefits if you are not yet receiving them. Unfortunately thieves have been using this system to steal your benefits. To prevent this from happening to you have two options:

- Create your MySSA account online, as mentioned above

- Block electronic access to your information online or by calling the SSA at 1-800-772-1213

The act of either setting up your account or requesting to block electronic access will prevent someone else from creating an account using your information. If, when you are attempting to create or block your account, you are notified you already have an account you may already be a victim. You will need to contact Social Security to notify them of the potential fraud and inquire about the procedures to correct the problem.

Credit Reports

Per federal regulation you are entitled to receive one free credit report from each credit bureau (Experian, Equifax and TransUnion) every twelve months. To order and review your credit reports online visit www.annualcreditreport.com. You will be required to enter your sensitive information. You will also be asked a series of questions to verify your identity. Because of this I recommend you do this where you have access to your financial records (mortgage, loan and other information). The process could take an hour or more.

Junk Mail Opt-Out

There are two ways to stop the junk mail you receive such as pre-approved credit card offers, magazine subscriptions, offers for services, etc.

- DMAchoice.org was created by the Direct Marketing Association to block unwanted solicitations. Visit their website, enter your information (name, street address and email address) and then list your opting-out preference(s). You can choose to opt-out of specific categories of direct mail or all categories of direct mail. This service is free of charge. If you prefer to register by mail you can download the registration form from www.DMAchoice.org. The fee to register by mail is $1.00.

- OptOutPrescreen.com allows you to opt-out from receiving pre-approved credit card offers. This program reports directly to the credit bureaus Experian, Equifax, TransUnion and Innovus. You can register online or by calling 888-567-8688. Once registered will receive a confirmation letter. You have the option to sign the confirmation letter and return it to OptOutPrescreen. Doing so will make your registration permanent. If you choose to not return the confirmation page your registration will be valid for five years.

These are just a few of the tips to reduce your risk of becoming a victim of identity theft. If you would like additional information you can visit my website CarrieKerskie.com. There you can read articles and register for my free electronic newsletter. You only need to enter your name and email address. I promise that I will not sell, rent, lease, or share your information. I am here to help. If you have a question or need assistance give me a call or send me an email.

Contact Information:

Carrie Kerskie

(239) 435-9111

Email: ck@kerskie.com

Website: www.Kerskie.com

Blog: www.CarrieKerskie.com

Twitter: @carriekerskie

Carrie Kerskie and the views expressed in this article are not necessarily the opinion of, nor is she, affiliated with Ciccarelli Advisory Services, Inc. or FSC Securities Corporation.

Aging Gracefully: Women’s Wellness Conference

DATE: Saturday, May 9th

TIME: 9:00 AM – Noon

WHERE: St. John the Evangelist Catholic Church Ballroom, 625 111th Ave N, Naples

TICKETS AVAILABLE AT: aginggracefully2015.eventbrite.com or call 239-262-6577

![]()

For a printer friendly version of the flyer below, CLICK HERE

Domicile is a Matter of the Heart

By Jill Ciccarelli Rapps & Kim Ciccarelli Kantor | Naples Daily News: Estate Planning Special Edition 2015

By Jill Ciccarelli Rapps & Kim Ciccarelli Kantor | Naples Daily News: Estate Planning Special Edition 2015

The sunshine, soft ocean breezes and lower taxes makes Florida a popular place to live. Generally speaking Florida domicile brings with it tax advantages over domicile in other states with respect to income taxes, state estate taxes, and homestead.

A person may have several residences at the same time, but in theory may be domiciled in only one place at any given time. The term domicile means the place where the taxpayer has his or her true, fixed permanent home, for legal purposes. Domicile is a matter of intent and requires a serious commitment that may entail a change in lifestyle and the ability to break ties with his /her old state. Many auditors consider five primary factors when considering place of domicile: home, active business involvement, time, items near & dear, and family connections.

A consideration may be to the size of home maintained in the old state vs. the domicile state. As far as business is concerned, a consideration to control and supervision, the taxpayer’s role in the business, pattern of activity, and whether it is a passive or active investment. Of course time is important, the number of days spent in your previous state vs. domiciled state. Your timing and duration of visits also play a role in determining intent. Items that are near and dear to you should be kept in your domiciled state; receipts and documents showing the transport of these items could be important to keep. Also anything that has strong sentimental value including family picture albums should be kept in your domiciled residence. Other factors, like changing address forms, shifting banking and investment relationships, various registrations, church affiliations should all be maintained in your domiciled state. Be careful even the smallest affiliation as a fishing license from your old state could wreak havoc.

The other benefit to establishing domicile in Florida is the Florida homestead exemption. This exemption can protect your home from creditors (with four exceptions), give you a credit against your homes assessment for tax purposes, and cap your property taxes to the lesser of 3% or the rate of inflation (“Save Our Homes”). Because of the “portability” provision, a homesteaded owner may now move up to $500,000 of the “Save Our Homes” benefit from one Florida home to the next. Florida homestead may also protect spouses for inheritance purposes with a life estate or a 50% interest in lieu of a life estate unless the spouse waives these rights in writing.

Exemptions are only available on an individual’s primary home. To qualify you must be a permanent resident of Florida as of January 1st of the year in which you apply for the exemption and file with the local county property appraisers office. If you moved into your residence in 2014 you have until March 1st to file for your 2015 homestead exemption, and have your assessed value capped for 2016.

If you are considering a change of domicile to Florida, it is important to discuss the advantages and disadvantages with your financial advisor, your CPA and your attorney. Domicile should be looked at not only with a tax perspective but also with an estate perspective regarding rights of spouse and children at your death. An advisor versed in the steps for new domicile can provide a more complete package of instructions and discuss planning opportunities to help assist you in your decision to domicile.