Economic Updates

Stay up-to-date on economic conditions and outlook with our analysis and commentary.

Happy New Year – Wishing you and yours the very best for 2015!

Throughout 2014 we were reminded that: markets are volatile; employment trends are ever-changing; food prices seem to continue to rise; diminishing energy prices can bolster the economy; the debt crisis in Europe appears to be on the mend; and returns are unpredictable.

Throughout 2014 we were reminded that: markets are volatile; employment trends are ever-changing; food prices seem to continue to rise; diminishing energy prices can bolster the economy; the debt crisis in Europe appears to be on the mend; and returns are unpredictable.

Through all the hints of corrections, we were there with you; guiding and advising you. While we can’t know what the future holds, here’s a glimpse of what 2015 might bring on the financial front:

Market volatility will be ever-present and a consistent element of the new “normal,” given geopolitical tensions, varying reform agendas, and divided monetary policies across the globe. Within the first couple weeks of the year, the precipitous drop in the price of oil has caused major swings.

On the home front, the dollar has strengthened, and interest rates remain low setting the stage for the U.S. to continue to be a leader in 2015. Coupled with development in new technologies: mobility, cloud computing, and additive manufacturing, the country’s future looks bright!

We expect the Fed to have its first rate hike in 2015. While many of us have benefited from low interest rates, it is time for the central bank to tighten its belt. Janet Yellen and her team will be providing strict oversight to the gradual rollout.

We are excited for what 2015 has in store for us. We will continue to work hard for you and your family and to keep you abreast of the ever-changing world and investment arena.

As we welcome another New Year, we’re hopeful this one will be a great one for you; allowing you to continue to pursue your interests and live your dreams! We wish you the very best in health and happiness and look forward to seeing you at our upcoming client events throughout the year. From our family to yours, Happy 2015!

Economic Update – Fourth Quarter 2014

While market participants and forecasters had their share of surprises and disappointments in 2014, many investors were rewarded as U.S. stocks had a solid year overall. That was not the case for most bellwether international and emerging-market indexes.

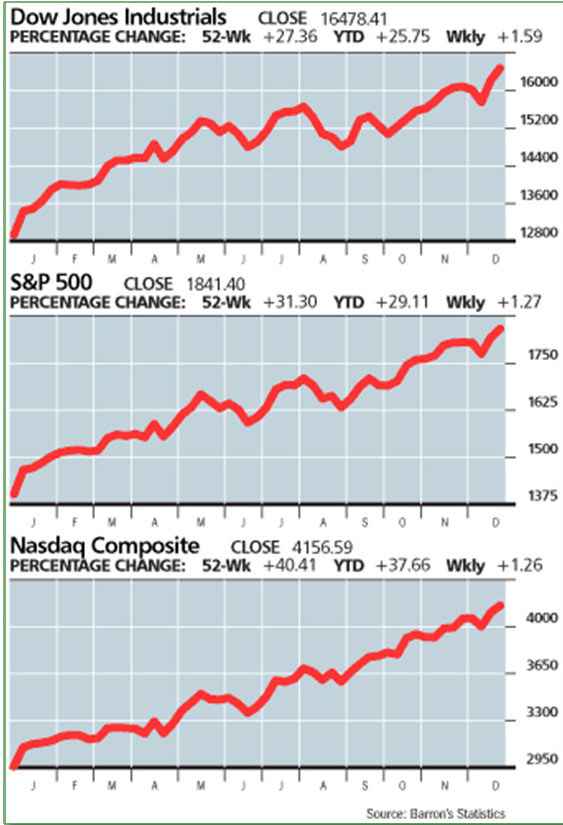

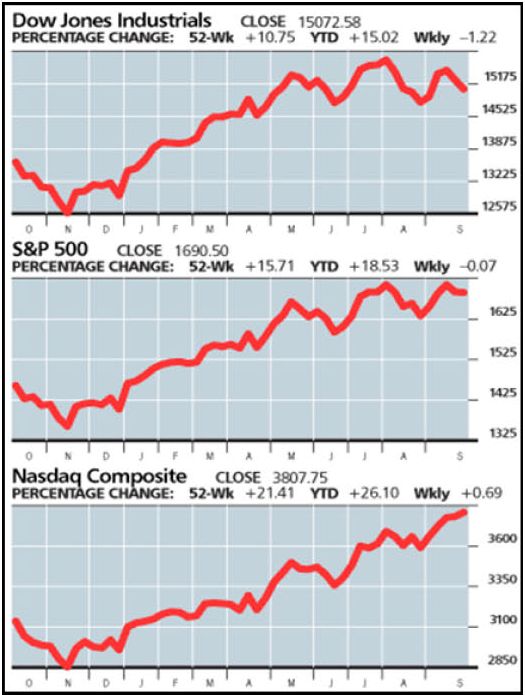

The Dow Jones Industrial Average was up 7.5% in 2014 while the S&P 500 experienced its third straight annual increase of over 10%. These two major indexes outperformed the broader market—the NYSE Composite Index rose a little more than 4% for the year.

Perhaps one of the more telling signs for 2015 was that the bull rested on the last two days of the trading year. In fact, U.S. stocks took most of the last week of 2014 off, finishing more than 1% lower. This prompted many market analysts to predict that 2015 could bring a return to more volatility than investors experienced in 2014. The late drop was attributed to an absence of buyers, not a plethora of sellers. Dan Greenhaus, Chief Strategist at BTIG Research, said, “With volumes so low, you can’t read much into the action. The market’s inertia is up until something comes along to change it.”

Bond investors also fared well in 2014. Most Wall Street professionals were off target as they predicted the government bond market to extend its selloff from 2013 and lead to higher interest rates. Thanks to slowing economic growth and declining inflation—especially in Europe—bond prices rose and yields fell.

2014 MARKET RETURNS (Source: yahoofinance.com)

Bonds were also helped when the Federal Reserve signaled that even though they ended their stimulus efforts, they were in no hurry to raise short-term interest rates. This added to the year’s bullish rally for income investors whose holdings were in government or investment grade bonds. Those who invested in sub-investment grade bonds did not fare as well. Russel Kinnel, director of manager research at Morningstar, said many non-traditional bond funds used wide mandates to bet on interest rates rising, “and that was not a great recipe for a year like 2014.” While income investors fared well in 2014, 2015 may look less attractive.

2014 was certainly a year to remember. Let’s review some notable highlights:

- January 31st – The New Year begins badly, as aftershocks from a sell-off in emerging markets hit the U.S.

- February 3rd – Leadership of the Federal Reserve passes to Janet Yellen, but Ben Bernake’s policies still rule.

- February 28th – Russian leader Vladimir Putin invades Crimea, sowing regional turmoil as the West shudders.

- July 3rd – First day the Dow Jones Industrial Average closes above 17,000.

- July 23rd – Oil prices peak at over $100 a barrel before sliding more than 40% in the second half to under $55.

- September 26th – Bond titan Bill Gross leaves Pimco for Janus, sparking huge redemptions at his old firm.

- October 31st – Bank of Japan’s Haruhiko Kuroda grabs the baton from the Fed and doubles down on monetary stimulus.

- November 4th – Republicans gain control of both the House and the Senate after midterm elections as a rebuke to President Obama.

- December 23rd – First day the Dow Jones Industrial Average closes above 18,000.

(Source: Barron’s, 12/2014)

As we look back at 2014, analysts are citing that the U.S. economy is looking better. Financial experts are pointing to the fact that we are experiencing falling unemployment, rising stock prices and an uptick in housing starts. Although at first many predictions for 2014 were met with skepticism, it would be difficult to argue with the average strategists’ 2013 prediction for a 10% rally in 2014.

As we look back at 2014, analysts are citing that the U.S. economy is looking better. Financial experts are pointing to the fact that we are experiencing falling unemployment, rising stock prices and an uptick in housing starts. Although at first many predictions for 2014 were met with skepticism, it would be difficult to argue with the average strategists’ 2013 prediction for a 10% rally in 2014.

Looking Ahead to 2015

Although there are still some strong contrarians out there, the consensus for 2015 appears to be bullish. Many analysts are suggesting that the market will continue to rise based on many factors, including:

- The U.S. economy will continue to move forward in a reasonable manner

- Unemployment figures will continue to go lower

- The European economy will get better

- Japan’s recession will ease

- The Federal Reserve will raise the federal funds rates

- Stocks will remain attractive compared to U.S. Treasuries

Bob Doll, Senior Portfolio Manager and Chief Equity Strategist of Nuveen Asset Management, believes 2015 will be the year of “increasing belief.” In other words, 2015 could be the year that we feel better about the U.S. economy than we do about the stock market. Doll said, “I think the dichotomy between a mediocre U.S. economy and a really good, if not great, U.S. stock market has been the reason people have not gotten enthusiastic.” Doll predicts it will be a good economic year, with low inflation, consumer spending picking up, an improving job market, and a solid year of earnings growth. The biggest risk, however, is the risk of deflation outside the U.S., led by a decline in oil prices. (Source: WealthManagement.com, 1/2015)

While it’s easy for investors to want U.S. stocks to have another strong year in 2015, we still need to remember that the current bull market started in 2009. In fact, some analysts conclude that stocks are no longer cheap—and under certain financial metrics valuations, are high. According to Bloomberg, after gaining 10% in 2014, consensus earnings-per-share growth for U.S. corporations is expected at 8% in 2015.

While no one can predict the future, there seems to be agreement on which factors will most influence investment outcomes. Adam Parker, Chief U.S. equity strategist at Morgan Stanley, says that “everyone is talking about rates, the dollar and oil.”

Interest Rates

(Source: Wall street Journal 12/2014)

Interest rates will play a role for investors again in 2015. The Federal Reserve has already signaled that it plans to raise interest rates and phase out the easy money policies that were designed to stimulate the faltering economy from the 2008 financial crisis. Having said that, their timeline for doing so still remains uncertain and financial experts are split on whether interest rates will actually go up in 2015.

Jurrien Timmer, Director of Global Macro in Fidelity’s Global Asset Allocation Division, says that “Federal Reserve uncertainty could mean more volatility for investors. This is particularly true at the beginning of a rate cycle, when the market is trying to gauge the speed and magnitude of the Fed’s plans. Indeed, big questions remain as to whether the Fed will follow a carefully choreographed rate-normalization script in 2015 or whether it will be forced to speed things up or slow them down.”

Most analysts started 2014 with what they considered a can’t-miss notion that interest rates would rise. They fell. Again in 2015, many feel rates could rise. The Fed’s short-term policy affects other rates, but longer-dated bonds depend more on a variety of market-based factors. 2014 results proved those factors can overpower even talks of Fed policy changes. While a growing U.S. economy and a deteriorating European outlook should exert pressure on 30-year Treasury bond yields, inflation needs to pick up meaningfully before that yield can rise significantly. (Source: Barron’s, Dec.15, 2014)

Remember—in many cases, bonds are supposed to provide portfolios with stability and hopefully help against stock market swings. Conservative investors should not try to chase speculative returns in bonds.

In their 2015 Investment Outlook, Delaware Investments wrote, “We believe returns will be lower than they have been in recent years.” They say that bond investing “will be transitioning into a new reality, one in which return expectations ought to be tempered.”

Jeffrrey Gundlach, who oversees $64 billion dollars at DoubleLine and is often referred to as the King of Bonds, agrees with others that the Federal Reserve will begin to raise the federal funds rates this year. However, he also predicts that the result will be the opposite of conventional wisdom, with longer-term yields declining in 2015 and investors facing a flattening yield curve.

As financial professionals, we intend to be very watchful of both the Federal Reserve’s movements and interest rates this year. We would be glad to recheck your personal situation during your next review or at any other time.

U.S. Employment

U.S. Employment

One of the barometers that the Federal Reserve looks to for direction is U.S. employment statistics. The unemployment rate, obtained from a separate survey of U.S. households, was 5.6% in December, down two-tenths of a percentage from November and its lowest level since June 2008. In December of 2014, U.S. employers added to payroll at a brisk rate. While economists surveyed by The Wall Street Journal had predicted that payrolls would rise by 240,000 in December, the actual number of non-farm payrolls rose to a seasonally adjusted 252,000 according to the Labor Department. This brought unemployment down to 5.6%.

Altogether, employers added 2.95 million jobs in 2014, the biggest calendar increase since 1999. Of course, the U.S. population has grown significantly in that time, to a population of more than 318 million in 2014, from 279 million in 1999. (Source: Wall Street Journal, 1/2015)

Oil Prices

Energy stocks have been among the year’s worst performers, as oil prices declined almost 50% from their mid-year peak of over $100 a barrel.

Many investors are questioning if there are bargains in beaten-down energy shares. Some analysts see value, while others fear that oil prices still have to stabilize. Lower oil prices help consumers at the pump, but they can wreak real havoc on unemployment, capital spending, loan collateral values, energy-company balance sheets and the junk-bond market.

Jeffrey Gundlach alerts investors that “the boost to U.S. consumers from lower pump prices is the first shoe to drop, but the negative secondary effects from the crude-oil price lapse take longer to surface.” He also reminds investors that “when you have a market that showed extraordinary stability for five years—trading consistently at $90 a barrel or above—undergo a catastrophic crash like this one, prices usually go down a lot harder and stay down a lot longer than people think is possible.” (Source: Barron’s, 1/2015)

“It’s not clear that anyone can answer how low [oil prices] will go,” said Ed Morse, global head of commodities research for Citigroup Inc. He adds, “It’s always hard to call a bottom.” Oil prices and their fluctuations can create market disruption and uncertainty. Oil prices will be on the list of items that we will monitor in 2015. (Source: Bloomberg.com, 1/2015)

International Concerns

For many market strategists, the bullish case for equities includes a stronger European economy and the end of the current recession in Japan.  Like the U.S., Europe and Japan will benefit from lower oil costs. Their exports are currently cheaper because they have depreciating currencies andtheir borrowing costs are low. Most analysts feel that the European Central Bank will follow the Federal Reserve’s example and provide Quantitative Easing and an asset buying program. These measures allow the European Central Bank to bolster their countries’ money markets by making funds available for banks to borrow on more favorable terms. (Source: Barron’s, 12/2014)

Like the U.S., Europe and Japan will benefit from lower oil costs. Their exports are currently cheaper because they have depreciating currencies andtheir borrowing costs are low. Most analysts feel that the European Central Bank will follow the Federal Reserve’s example and provide Quantitative Easing and an asset buying program. These measures allow the European Central Bank to bolster their countries’ money markets by making funds available for banks to borrow on more favorable terms. (Source: Barron’s, 12/2014)

Russia and China also present concerns for investors. Russia “is in bad shape, due to lower oil prices, but it wants to remain relevant on the world stage,” according to John Praveen of Prudential International Investment Advisors. He and others also caution that China will be another concern for forecasting markets in 2015. Investors will need to see if the Chinese central bank can provide sufficient stimulus to help their economy continue its expansion in 2015. (Source: Barron’s, 12/2014)

U.S. Politics

U.S. Politics

As we head into 2015, the political landscape in the U.S. has changed dramatically. Following six years of gridlock and brinksmanship, 2015 could prove to be a very interesting one.

With Republicans taking control of both the House and the Senate, analysts are predicting an active year in Washington. Jason Furman, Chairman of President Obama’s Council of Economic Advisors, said, “There’s no reason why we can’t continue to have a strong economy in 2015” after coming off a year of solid economic performance marked by improvements in hiring, wages, and corporate investment. President Obama only has 24 months remaining—a short period of time for him to cement his legacy. Analysts feel that comprehensive tax reform, especially closing some loopholes and revamping corporate taxes, could prove to be a big win for investors. The U.S. political scene is another area investors need to pay attention to this year. (Source: Barron’s, 1/2015)

Conclusion: What Should an Investor Do?

Although the U.S. stock market isn’t filled with bargains, most analysts see the potential for U.S. stock market gains in 2015. Jurrien Timmer, Director of Global Macro in Fidelity’s Global Asset Allocation Division, encourages investors to “continue to view the U.S. market as the best house on the street. As we all know, the best house is usually the most expensive, and for good reason.” While many analysts are predicting growth for U.S. stocks, that growth might not come easily. In the last three years the S&P 500 has risen from a humble 11.7 times next-four-quarter earnings estimates to an ambitious 16.5 times. Investors might be best served structuring their portfolios to weather stock market turbulence. (Source: Barron’s, 12/2014)

Some analysts expect that the Fed might raise the short-term federal funds rate at mid-year, but not enough to destroy any good times for investors. Columbia Management’s Barry Knight reminds investors that “the case for higher interest rates is a little stronger than last year’” and he feels that getting the Fed’s moves right is the single most important factor in making an accurate market prediction for 2015.

Some analysts expect that the Fed might raise the short-term federal funds rate at mid-year, but not enough to destroy any good times for investors. Columbia Management’s Barry Knight reminds investors that “the case for higher interest rates is a little stronger than last year’” and he feels that getting the Fed’s moves right is the single most important factor in making an accurate market prediction for 2015.

So what can investors do?

Continue to be watchful. Perhaps some of the optimism can be attributed to holiday cheer; however, even the most optimistic need to be aware of some of the warning signs.

Long term investors should try to not change their outlooks based on short-term market forecasts. It might be in your best interest to prepare your portfolio for turbulence and focus on risk. Two of the questions investors need to ask themselves are:

- How much risk do I pose to my portfolio?

- How much risk do I need to take?

These are great starting places for investors for 2015. Generic and non-specific advice might not be best during volatile and confusing times.

Focus on your own personal objectives. During confusing times it is always wise to revisit your personal timelines. It is typically in your best interest to create realistic time horizons and return expectations for your own personal situation and to adjust your investments accordingly. For example, it’s important to consider your time horizon when looking at an investment. If you will need more cash flow from your investments over the next one to five years, you might consider different choices than someone with a ten-to-fifteen-year time horizon.

Understanding your personal commitments and categorizing your investments into near-term, short-term and longer-term can be helpful. We are skilled at this and are happy to help you.

Be cautious with income investments. While some income investors did well in 2014, this year the menu is less attractive. With the Federal Reserve and interest rates in the spotlight, this is a good time to understand your true income and cash flow needs. Again, this is one of our strengths and we are happy to provide you with help. To review your situation, either call our office or wait for your next review.

Don’t try to predict the market. Investment decisions driven by emotion can cause problems for investors. Vanguard Investments reminds us that in the face of market turmoil, some investors may find themselves making impulsive decisions or, conversely, becoming paralyzed, unable to implement an investment strategy or to rebalance a portfolio as needed. (Source: Vanguard.com, 2014)

Discipline and perspective can help investors remain committed to their long-term investment programs through periods of market uncertainty.

Discuss any concerns with us.

Our advice is not one-size-fits-all. We will always consider your feelings about risk and the markets and review your unique financial situation when making recommendations.

We strongly believe it is prudent for investors to work with an advisor who offers constant communication and frequent discussions, as well as one who is continually reviewing economic, tax and investment issues and drawing on that knowledge when offering direction and strategies to their clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy. Through changes in the aggregate market value of 500 stocks representing all major indices. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Sources: yahoo.com; Wall Street Journal, Barron’s; WealthManagement.com; Bloomberg.com; mic.com; forbes.com; businessinsider.com; thefiscal.times.com

© Academy of Preferred Financial Advisors, Inc.

Volatility Is Up. So What?

Professional investors know something that most people find impossible to believe: that the threat of scary ups and downs in the markets is by far the best friend of the long-term investor. Why? Because over the long term, stocks have provided returns far higher than bonds or cash. If it weren’t for the occasional dizzying gyrations, any rational investor would put his or her money where the highest returns have been. Right?

This appears to be one of those times–a time when non-professional investors are reminded of the reasons why they have this lingering fear of the stock market. Since the end of September, the S&P 500 index has done something regularly that it normally does infrequently: moved more than a full percent up or down in a single day. Consider the recent pattern this month:

- Oct. 1 -1.3%

- Oct. 4 +0.05%

- Oct. 5 +1.1%

- Oct. 6 -0.2%

- Oct. 7 -1.5%

- Oct. 8 +1.8%

- Oct. 9 -2.1%

- Oct. 10 -1.1%

- Oct. 13 -1.65%

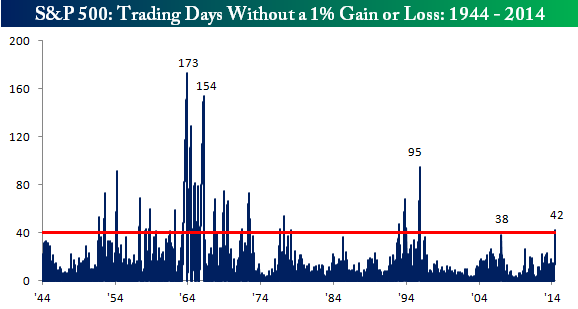

Contrast this to the calm before the storm: earlier this year, the markets experienced 42 consecutive days without a single 1% price move, and the accompanying chart shows that this is far from the record.

The question we should be asking ourselves is: why are we paying such close attention to daily market movements? Why are we allowing ourselves to fall for the trap of getting anxious over short-term swings in stock prices?

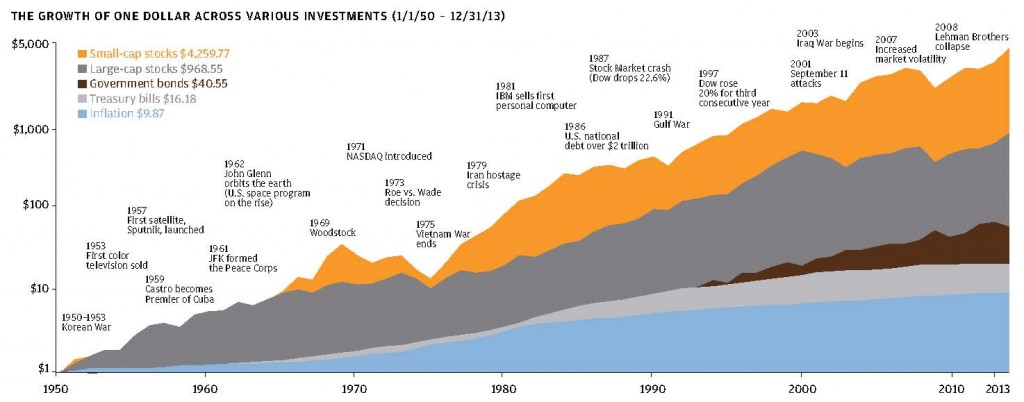

The second chart shows the growth of a dollar invested in the S&P 500 at the beginning of 1950, with dividends reinvested, compared with a variety of alternative investments which have not provided the same returns. (Note that small cap stocks, which are more volatile, have done even better.) The chart also shows all the scary headlines that the markets managed to sail through on the way to their current levels–all of which are scarier than the things we’re reading about today.

This is not to say that the markets won’t go lower in the coming days, weeks or months; in fact, we are still awaiting that correction of at least 10% which the markets delivery with some regularity on their way to new highs, which has been long-delayed in this current bull market. The thing to remember is that the daily price of your stock holdings are determined by mood swings of skittish investors whose fears are stoked by pundits and commentators in the press, who know that the best way to get and hold your attention is to scare the heck out of you. What they don’t say, because it’s boring, is that the value of your stock holdings are determined by the effectiveness of millions of workers who go to work every day in offices and factories, farms, warehouses, power plants and research facilities, who slowly, incrementally, with their daily labor, build up the value of the businesses they work for.

The last time we checked, that incremental progress hasn’t stopped. The economy is still growing. You won’t get a daily report on the value of the stocks you own; only the daily, changing opinions of skittish investors. But if you take a second look at the growth of an investment in stocks over the long-term, you get a better idea of how that value is built over time, no matter what the markets will do tomorrow.

Sources: http://www.bespokeinvest.com/thinkbig/2014/6/17/1-moves.html

Economic Update – Third Quarter 2014

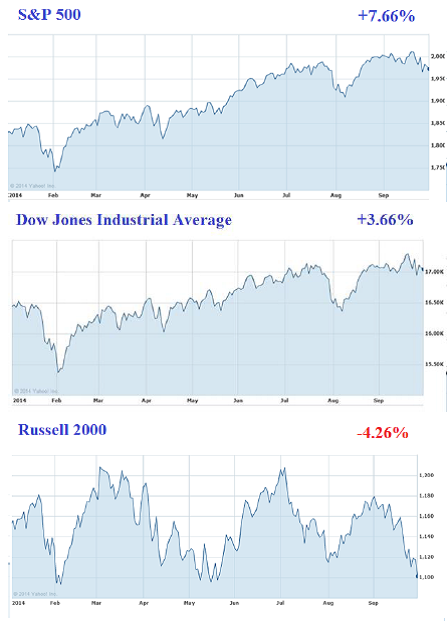

The third quarter of 2014 was very interesting. The overall results for many investors were positive, but while several diverse pockets of the market enjoyed gains, other stocks struggled. The S&P 500 and the DJIA (both of which track larger established companies) continued to outperform small stocks and foreign shares. Through Sept 30, 2014 the S&P 500 was up 7.66% and the DJIA was up 3.66%. By comparison, the Russell 2000 Index (which tracks small stocks) is down 4.26% for 2014. (Source: Wall Street Journal)

pockets of the market enjoyed gains, other stocks struggled. The S&P 500 and the DJIA (both of which track larger established companies) continued to outperform small stocks and foreign shares. Through Sept 30, 2014 the S&P 500 was up 7.66% and the DJIA was up 3.66%. By comparison, the Russell 2000 Index (which tracks small stocks) is down 4.26% for 2014. (Source: Wall Street Journal)

Many analysts feel that several U.S. big stocks are still more attractively priced than smaller stocks and that this trend could continue. “Small stocks are victims of their own success,” according to Jack Ablin, Chief Investment officer of BMO Private Bank. “They made a huge move last year and entered into this year overvalued. While there are great small company stocks, small caps in general need to take a back seat to their larger competitors until valuations come back into alignment.” In fact, some portfolio managers are fearful that the small cap underperformance has just begun. (Source: Wall Street Journal 9/29/2014)

Although caution still remains the top priority for most investors, many analysts feel that the bull could stay in charge for the rest of this year and possibly longer. Barron’s surveyed 10 top analysts in September and surprisingly, all of them felt that the upward trend would continue. While several analysts toned down their optimism because of the market’s gains, they still feel that we have not reached the market’s ultimate peak. They feel that rising corporate profits will continue to lead to increases in large cap stock prices. Having said this, they still caution investors about political tensions and interest rates. (Source: Barron’s 9/8/2014)

In a recent Interview, Dirk Hofschire, Senior Vice President of Asset Allocation Research at Fidelity Investments, said, “We continue to have a favorable global backdrop for asset prices. It’s been a Goldilocks environment where things are not too fast, not too slow, not too warm, not too cold. The U.S. economy has still been making progress, jobs are being created, unemployment is coming down and many leading indicators still point up.” (Source: Fidelity.com)

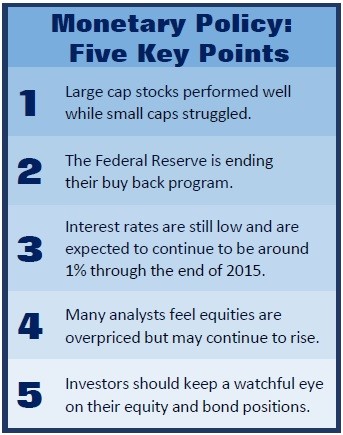

Investors are still keeping a watchful eye on the Fed—its bond buying program is set to end in October and many investors expect the Fed to raise interest rates sometime next year.

Recently, volatility has returned to the market and investors are noticing a “see-saw” effect between the bears (who are convinced stock prices will fall) and the bulls (who rush in during market swings to selectively add to their equity positions). Who is right? Only time will tell!

MONETARY POLICY

Many investors are watching the Federal Reserve very closely and with good reason. The Fed’s September bond purchases were only $15 Billion and in October they are moving towards their pledge to end the Quantitative Easing program of buying bonds. This is leaving many analysts concerned about the upward movement of interest rates. The Fed’s key interest rate target has been pinned at virtually zero since December 2008 (the depth of the financial crisis).

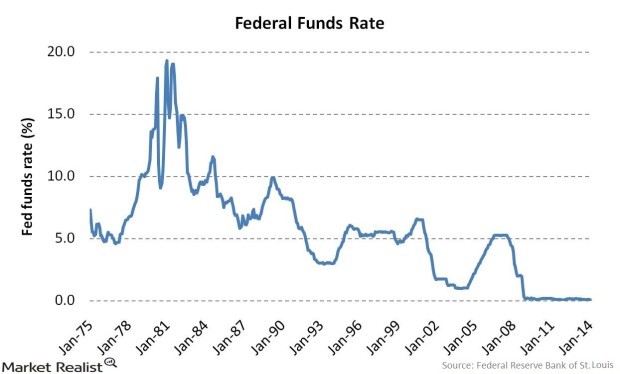

This is not the first time that the Federal Reserve has taken a “whatever it takes” approach to supporting monetary policy. Thirty-five years ago on October 6, 1979,  the Federal Reserve, led by Paul Volker, made a revolutionary change in how it handled monetary policy. Faced with double-digit inflation rates, the central bank responded by raising interest rates to 20%. Although this caused other aftershocks, this extreme policy would go on to tame inflation rates. (Source: Barrons 10/6/2014)

the Federal Reserve, led by Paul Volker, made a revolutionary change in how it handled monetary policy. Faced with double-digit inflation rates, the central bank responded by raising interest rates to 20%. Although this caused other aftershocks, this extreme policy would go on to tame inflation rates. (Source: Barrons 10/6/2014)

Monetary policy has had a key impact on the world’s major economies. Investors are rightly concerned about how effective monetary policy can be given the fact that central bankers have cut rates just about as much as they can.

According to Matthew Coffina at Morningstar research, “interest rates have been one of the biggest surprises of the year. Going into 2014, most pundits expected a steady rise in interest rates as the Federal Reserve winds down its purchases of long-term bonds and moves closer to raising short-term rates. Instead, the yield on the 10-year Treasury fell from 3% at the start of the year to a low of 2.34% in mid-August. The 10-year Treasury yield has since recovered to around 2.6%, but it remains below where many market observers had expected.”

Today, as the Fed prepares to wind down its extraordinary Quantitative Easing policy, interest rates are still close to zero. The consensus among analysts is that we are still about a year or so away from the Fed’s first interest rate hike, or tightening of the cycle. The Federal Reserve faces a delicate few months ahead amid internal debates over when to start raising interest rates and how to adjust its public guidance about its likely actions. The Fed and its current leader, Janet Yellen, have been clear in communicating that even when they get to that first tightening, they will probably go pretty slow in raising interest rates.

Many investors are still searching for safe, short-term debt. This demand intensified at the end of the quarter, pushing up bond prices and forcing down yields. The yield on the US Treasury bill on September 2nd reached a negative .01%. (Source: Wall Street Journal 9/24/2014)

During periods of market anxiety, Treasury Bonds can provide a safe harbor for many investors. So what should Bond investors do? Should they sit back and watch the data and refrain from taking any long term positions?

The entire bond market suffered when interest rates rose last year. If the Fed changes rates it could affect shorter dated bonds. Russ Koesterich, Chief Investment Strategist at Blackrock, warns to be careful with even two to five year Treasury bonds. (Source: Barron’s 9/1/2014)

While bonds are an important part of many financial plans, this is a good time to be very watchful of all income-oriented investments. Interest rates have remained at historically low levels for quite some time. Global rates continue to remain exceptionally low and that typically reduces the risk of a swift upward movement in U.S. interest rates.

Recent employment reports painted a brighter picture of the U.S. economy, but they also showed stagnant workers’ wages. Without rising incomes, the Fed seems to be less worried about inflation. That means that even though the jobless rate has hit a level at which the Fed might otherwise consider raising interest rates, it is no longer under the inflation gun when it comes to timing. (Source: Barron’s 10/6/2014)

It is anyone’s guess when the Fed will raise interest rates and by how much. On a positive note, Federal Reserve Chairperson Janet Yellen stated that she sees interest rates continuing around 1% until the end of 2015.

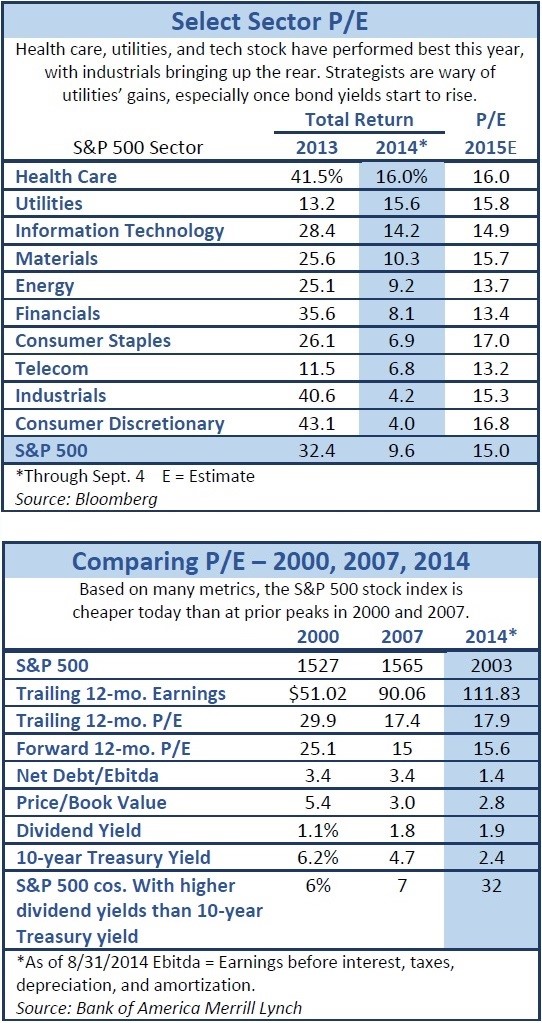

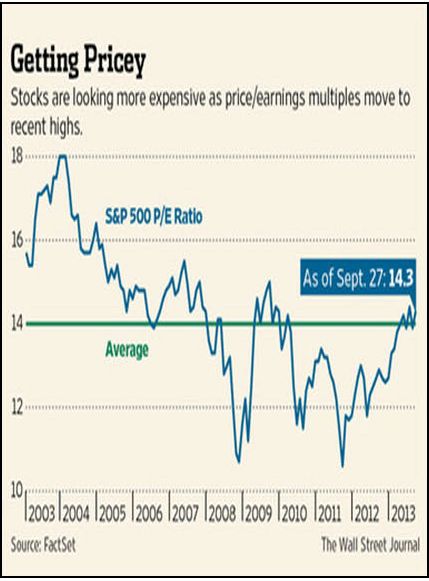

PRICE–TO–EARNINGS RATIO

Price-to-earnings (P/E) ratios are still a key factor in the valuation of equities for many analysts. P/E is a valuation ratio of a company’s current share price (market value) compared to its per-share earnings. For example, if a company is currently trading at $40/share and earnings over the last 12 months were $2/share, the P/E ratio for the stock would be 20 ($40/$2). Generally a high P/E ratio means that investors are anticipating higher growth in the future.

According to a Barron’s survey in September, P/E ratios were one of the main criteria used by 10 top analysts to measure equity valuations. They felt that with macroeconomic data improving and profitability broadening out, a case could be made that the market’s P/E ratios were extended but not outrageous. They viewed U.S. stocks as neither cheap nor expensive, considering the low level of interest rates. “Stocks offer less compelling value than a few years ago,” says Savita Subramanian, head of U.S. Equity and Quantitative Strategy at Bank of America Merrill Lynch. “But if anything, there’s an upside risk to my view.” (Source: Barron’s 9/1/2014)

Steven Auth, Chief Investment Officer of Federated Investors, is more bullish. “The U.S. economy is accelerating and so are earnings,” he said, adding that his market views have been right on for the past two years. (Source: Barron’s 9/1/2014)

However, John Campbell, a Harvard economist who collaborates with Robert Shiller (a Nobel laureate in economics who is also a noted P/E watcher) feels that based on today’s P/E measurements, stocks are overpriced. (Source: New York Times)

While the P/E ratio can be informative, you can see that not even the experts always agree on what it means. It is therefore important not to base a decision on this measure alone. When the denominator in this equation (earnings per share) shrinks, the actual numbers can change significantly.

STOCK BUYBACKS

Once again in the third quarter, corporate managements preferred to put their cash to work by purchasing their own stock. Reducing the number of outstanding shares raises the earnings per share. To the extent that corporate executives are compensated with stock, this can enhance their stakes. Many analysts presume that the decision to buy back stock is fueled by analyses that suggest that stock buybacks yield a better return than investments in expanding the businesses.

THE ECONOMY

Positive economic news during this quarter included the following:

- The U.S. labor market is improving at a faster rate, though gains remain slow enough to avoid provoking broad-based, late-cycle wage inflation. Year to date, the economy has added 1.6 million jobs—the 1.9% year-over-year increase in July was the fastest pace of growth since 2006.

(Source: Bureau of Labor Statistics)

- Core consumer inflation has slowed to 1.9% year over year. (Source: Fidelity.com)

- Personal consumption is still growing at a relatively modest 4% (nominal) year-over-year pace. (Source: Bureau of Economic Analysis, Haver Analytics)

In addition to this good news, of course, there were still some concerning factors. The main one was the housing sector, which remains in a soft patch, even though leading indicators are showing signs of slow improvement. Sales activity remains at historically weak levels and prices have flattened over the past three months. Construction starts and permit issuance remain at low levels, though they rose in July and remain in an upward trend. (Source: Core-Logic, Haver Analytics)

Although mortgage credit remains relatively tight during this quarter, banks reported the broadest rise in more than 20 years in their willingness to make residential loans during the second quarter.

GLOBAL OUTLOOK

Although differences vary wildly across the globe, overall economic developments outside the U.S. appear to be moving slowly and carefully.

Eurozone growth has idled due to GDP reductions in their two largest economies—Germany and France. However, analysts believe this might be a mid-cycle slowdown instead of the start of a new recession. Bank lending standards have eased up across the board and the European Central Bank has indicated a desire to help beyond the monetary stimulus plans already announced. The rate of growth is likely to remain low, with about 60% of the region’s economies experiencing expansion in their leading economic indicators during the past six months, down from 90% at the start of 2014.

Japan’s outlook remains ambiguous. Due to April’s tax hike, they recently underwent a worse-than-anticipated 19% annualized contraction in second quarter consumer spending. With the tax hike over, consumption should stay stable. Economic indicators have improved, but they still remain below the levels seen before the tax increase.

China, on the other hand, continues to benefit from their second quarter stimulus. However, leading indicators are exposing the diminishing returns that these policy decisions can provide and any return to expansive growth remains questionable. China’s property sector has been persistently plagued by falling housing prices and rising inventories and continues to be the largest near-term risk for economic and financial stability.

Across other developed markets, conditions vary drastically. Countries such as Indonesia and India seem to have benefited from the global stabilization after the interest rate shudder in 2013. Elections of perceived reformers have also seemed to add optimism back into their respective economies. Other emerging markets, such as Brazil, have been hindered by recessionary conditions. The weak global situation and diminishing commodity prices continue to challenge many developing countries. However, this significant variation among the world’s economies is still pushing the global business cycle into a slow upward trend.

INFLATION

The rate of inflation is something that is always monitored by the Fed and investment professionals. As mentioned earlier, inflation appears to be under control. However, it is important to remember that this number (which excludes food and energy) rose at its fastest pace in 15 months. (Source: Barron’s 6/23/2014)

Currently inflation isn’t high enough to cause much damage to the stock market, says Ned Davis of Ned Davis Research. He notes that since 1925, the S&P 500 has dropped 5% a year on average, when the inflation rate has exceeded the S&P500’s yield by more than 2.1 percentage points. While May’s 2.1% inflation rate was higher than the S&P 500’s 1.9% dividend yield, it’s in a range where shares have historically produced positive returns. (Source: Barron’s 6/23/2014)

Many investors are also concerned that inflation might start to decrease dramatically and actually cause a very unusual dilemma: deflation. This has already taken hold in many different European countries. The European Central Bank cut interest rates significantly and stimulated bank lending—moves that were specifically aimed at reversing this trend before other countries might encounter this problem. (Source: Wall Street Journal 6/6/2014)

CONCLUSION

Volatility seems to have returned to the equity markets and past 4th Quarters have seen their share of market swings. Analysts are focused on earnings, the Fed, the economy and stock valuations. However, individual investors still have to look at their own situations first. It is important to be cautious, but it is just as important to determine your own personal risk or “worry” level. That’s where we can help.

Now is good time to ask yourself:

- Has my risk tolerance changed?

- What are my investment cash flow needs for the next few years?

- What is a realistic return expectation for my portfolio?

Your answers to these questions will govern how we recommend investment vehicles for you to consider. We can help you determine which investments to avoid and how long to hold each of your investment categories before making major adjustments. For example, if your cash flow needs have changed for the next few years, you might consider different investments than someone who has limited to no cash flow needs.

We continually review economic, tax and investment issues and draw on that knowledge to offer direction and strategies to our clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings and

- continuing education for our team on the issues that affect our clients.

A good financial advisor team can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting, or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

P.S. Under normal conditions, Fed tightening wouldn’t be too much of a worry. Since 1983, the Standard & Poor’s 500 Index has averaged a 4.4% gain during the 6 months before a hike and another 7.7% during the six months following it, according to Strategic Research Partners. The only problem: These aren’t normal times!

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. The P/E ratio (price to earnings ratio is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher P/E ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower P/E ratio. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Sources: Barron’s; New York Times; Core-Logic-Haver Analytics; Bureau of Economic Analysis-Haver Analytics; Fidelity; Bureau of Labor Statistics; Wall Street Journal; HSH.com; Contents © 2014 Academy of Preferred Financial Advisors

Economic Update – Second Quarter 2014

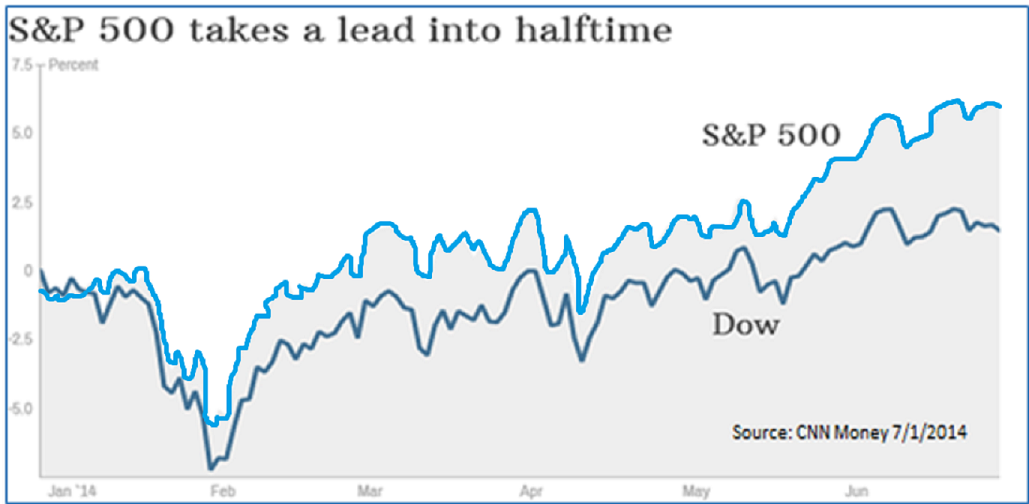

The year’s first half for equities can be summed up in simple terms: confusing and unpredictable markets produced gains. As of June 30, the S&P 500 had already logged 22 record highs this year alone, ending the first half up 6% while the Dow Jones Industrial Average (DJIA) increased by 1.5%. Both of these indexes hit new highs in the 2nd quarter while the NASDAQ Composite index rose by 5.5%, reaching a 14-year highpoint. Interestingly, 2014 has produced the biggest halftime lead by the S&P 500 over the DJIA since 2009 and the seventh-biggest since 1929, according to Bespoke Investment Group.

Bespoke also shared that in eight of the 10 years with the most underperformance, the DJIA has gone on to outperform the S&P 500 during the second half of the year. If this pattern holds, then the Dow might make up some of that lost ground. (Source: Barron’s, June, 2014)

Investors started 2014 with several serious concerns that were enough to make them nervous. How would the S&P 500 Index follow up 2013’s 30%+ gain (including dividends)? Would the market correct because the bull was getting tired, or would there be profit-taking? Would the slow improvement in the U.S. economy send bond prices lower, or would we see the Federal Reserve shift to higher interest rates? All of these fears made investors nervous.

Would the market correct because the bull was getting tired, or would there be profit-taking? Would the slow improvement in the U.S. economy send bond prices lower, or would we see the Federal Reserve shift to higher interest rates? All of these fears made investors nervous.

So far in 2014, the bond market has also fared well—in fact, better than most had expected. The yield on the U.S. Treasury ten-year note, which moves inversely to its price, fell to 2.51% from 2.76% at the end of the first quarter.

Unfortunately, many investors are having a hard time enjoying these increases, as concerns about lofty prices make it difficult to decide whether to keep funds in cash or stay invested. The forces driving the stock market to new highs and helping parts of the bond market to remain near record low yields don’t show immediate signs of changing.

What are the forces driving the rallies in both stocks and bonds? Many economists credit the aggressive efforts by the world’s major central banks to flood financial markets with new money in an effort to keep sluggish economies continually moving forward.

U.S. stocks have been supported by expectations that the U.S. economy, while still sluggish, will grow fast enough to keep corporate profits expanding. However, many investors no longer feel comfortable with that outlook, and have begun focusing more on what can go wrong with their portfolios than on where they can make money.

The current stock market rally has outlasted the historical average of other Bull Markets with higher returns. In contrast, the preceding Bear Market was much steeper and longer than average, and the gains from the period—from the beginning of the Bear Market to the end of this Bull Market—are currently near the median and below the average. This confusion can be why many investors are proceeding with great caution. (Source: Fidelity)

There is “still a bit of a fear-factor” among investors, said Thomas Huber, Manager of the T. Rowe Price Dividend Growth Fund. “Everyone is looking for what’s going to be the big crack in the markets.” (Source: Wall Street Journal, July 1, 2014)

While many investors are concerned about how markets will respond when the Fed raises interest rates in the future, there are also concerns building in the opposite direction regarding the estimate in the growth of our economy. The Commerce Department’s third and final estimate of the Gross Domestic Product (GDP) for the first quarter of 2014 continued the downward spiral of the first two estimates—from +0.1% to -1.0%, and now down to -2.9%. This was the largest drop recorded since the end of World War II that wasn’t part of a recession.

Many economists believe that the extent of the first quarter decline is so substantial that it makes it unlikely that we will reach a 2% increase, even if the next three quarters are significant. (Source: Bob LeClair’s Finance, June 28, 2014)

Early in the year, stocks ran into problems and investors blamed the harsh winter weather in large parts of the country. Several early indicators led to speculation that the economy was weakening, but in the 2nd quarter the market rebounded, sparked by thoughts that better growth was leading winter into spring. So far, those thoughts have proved to be accurate: the U.S. economy has improved, although there are still concerns over how strong the rebound will be.

A recent GDP report offered some positive data, including:

- Existing-home sales climbed 4.9%, the strongest gain in three years.

- New-home sales jumped 18.6% in May (the largest gain in more than 20 years) to an annual rate of 540,000 units, a six-year high. The median price for a new home also increased almost 7% from last year.

- The Conference Board’s confidence index improved to 85.2 in June. That was its highest reading since 2008, as many consumers were more optimistic about jobs and future conditions. (Source: Bob LeClair’s Finance, June 2014)

Will we be able to hold onto these gains and add enough through the end of the year to at least have a positive GDP for 2014? Let’s hope so. Slow growth could reduce corporate profits, which would be bad news for stocks and could lead to higher-than-expected default rates on junk bonds.

PRICE–TO–EARNINGS RATIO

Price-to-earnings (P/E) ratios have risen over the last two years, as improving investor confidence helped drive market gains. Some are focused on the current valuations which are slightly above the long-term average, 17.1 versus 15.1. The higher the P/E, the more likely the stock market is overpriced. Although most stock indices are at an all-time high, the market valuation is nowhere near its 2001 peak. (Source: Fidelity.com)

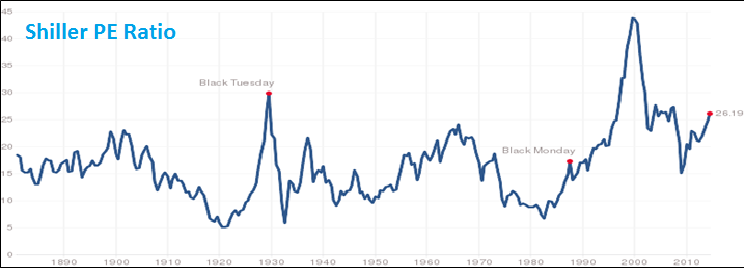

Even with a gain in the first half of 2014, bears exist. Nobel Prize-winning professor Robert Shiller notes that currently the market looked more expensive on a cyclically adjusted price/earnings basis only three other times in the past 130 years—1929, 2000 and 2007. The Shiller P/E ratio for the S&P 500 is based on average inflation-adjusted earnings from the previous 10 years. Despite this statistic in today’s low interest rate environment, Shiller is not telling investors to sell all of their holdings and to retreat to a bunker. He just thinks it might be time to be cautious and lighten up.

STOCK BUYBACKS

Many investors do not realize that one of the stock market’s biggest drivers today is stock buybacks. Companies buying back their own shares represent the single biggest category of stock buyers today, according to a study by Jeffery Kleintop, Chief Market Strategist at LPL Financial. (Source: Wall Street Journal, June 30, 2014)

Stock buybacks are also a source of controversy. Some economists say they allow companies to provide artificial support for stock prices by increasing demand for shares. Also, if a company reduces its number of shares, simple math shows that the earnings per share will rise even if the total earnings go nowhere. Most professional money managers look primarily at earnings per share, so buybacks can improve a company’s apparent earnings performance, even if overall earnings aren’t rising at all. Executives may use buybacks to manipulate share prices, helping them hit earnings targets, receive bonuses, and other benefits.

According to Mr. Kleintop, half of the first quarter’s S&P 500 per-share earnings gains came from declining share count, not from increases in actual earnings. (Source: Wall Street Journal, June 30th)

That doesn’t mean all buybacks are misguided, he added. In some cases, buybacks are better than dividends as a way to return money to shareholders because investors pay taxes on dividends and don’t pay taxes on buybacks unless they sell their shares.

GLOBAL

Financial markets worldwide are getting a boost from recent upbeat economic data out of China that is improving the outlook for global growth. China has increased its manufacturing activity and many economists believe that its appetite for raw materials will continue.

Many markets were rattled earlier this year by worries that China’s slowing growth would lead to a hard landing. However, the Chinese government has taken various measures to build investor confidence, including credit easing, more spending on highways, and business tax breaks.

After a massive credit boom in recent years, China continued to struggle to balance the competing objectives of tapering down its excessive credit expansion, preventing financial instability, and maintaining a fast pace of growth. Foreign capital inflows have risen and become more short-term in nature, increasing China’s vulnerability to shifts in global capital flows. (Source: Fidelity)

The U.K. and Germany remain the primary drivers of the European Economic Expansion, but there have now been indicators that other European economies have improved significantly, suggesting that Europe’s cyclical upturn continues to become more broad-based.

INTEREST RATES

Central bankers around the world debate whether very low interest rates, adopted in many economies since the 2008 financial crisis to spur stronger recoveries, are actually feeding market bubbles that could burst and potentially cause new financial turmoil. In June, Mario Draghi, President of the European Central Bank (ECB), made a bold move by cutting the main lending rate from 0.25% to a record low 0.15%. This pushed the deposit rate from zero to a minus 0.1%, effectively charging banks to park funds at the central bank. Following that move, Mr. Draghi said, “Are we finished? The answer is no. If need be, within our mandate, we aren’t finished here.” (Source: Barrons, June 2014)

The Fed has held short-term interest rates near zero since late 2008 and is winding down its bond-buying program. Recently, Janet Yellen, Chairperson of The Federal Reserve, assured investors and the public that the Fed won’t raise interest rates abruptly simply because some markets may look a bit volatile. The Fed has taken pains to reassure investors that interest rates will remain low even as the economic recovery picks up. (Source: Wall Street Journal, July 3, 2014)

Most Fed officials have indicated they expect to start raising interest rates in 2015, but the final decision will depend on whether the economy continues to strengthen as they forecast. The Fed has also stated that when it actually does increase rates, it will do so gradually and short‑term interest rates are unlikely to rise as high as they have in previous recoveries.

Many investors think that the rise in interest rates could happen sooner than the Fed’s estimate and the pace of increases could be more rapid than currently expected.

Historically, low interest rates and strong profitability have allowed U.S. corporations to reduce interest expense, improve their balance sheets, and accumulate liquid assets. Companies have used high cash balances to return capital to shareholders as both dividends and share buybacks, maintaining relatively high yield even though equity prices have continued to rise.

INFLATION

Inflation finally nudged above the 2% level that the Fed says is its long-term target. Compared with a year ago, the Consumer Price Index (CPI) is up 2.1% (not including food or energy). Although that might make the Fed happy, it sent a tremor of worry through analysts, investors, and economists.

Ongoing weak wage growth has continued to eliminate inflationary pressures in many developed economies. Weaker economic outlooks may help bring down inflation in some emerging markets’ economies over time. However, the rapid rise in agricultural prices could create inflationary pressures in many emerging economies, where food represents a higher proportion of consumer expenses. (Source: Fidelity)

UNEMPLOYMENT

On Wednesday, July 2, a report on the U.S. labor market was better than expected in that 281,000 private-sector jobs were created in June compared with an estimated increase of 210,000.

Although this is certainly good news, many investors say that stocks will need continued evidence of an improving economy to sustain the move higher. (Source: Wall Street Journal, July 3, 2014)

CONCLUSION

Equities have provided a nice return for the first half of 2014, so now what should an investor do? Your answer could depend upon your “worry level.” Some believe that stocks will benefit from robust earnings and low interest rates, while many other financial professionals are spending sleepless nights focusing on downward equity outlooks. The Federal Reserve has been a key factor in why equity markets have done well since 2009, but they have already started paring back their bond purchase programs and they will need to raise interest rates eventually.

Several money managers are suggesting that the five-year-plus bull market may be getting long in the tooth, but few are selling the bulk of their portfolios and leaving the room. Those money managers who sided with caution so far in 2014 have underperformed the indexes; however, even the great Confucius once said “the cautious seldom err.” Money managers that sometimes hold large cash positions don’t always move in sync with peers or benchmark indexes. Approaching market tops, they may become increasingly cautious, while peers remain fully invested. Thus, it is common for such money managers to trail peers when stocks are moving higher like they did in the first half of this year.

Several money managers are referring to the current period as the “new neutral.” Although U.S. stock indexes are pushing through fresh records and valuations have passed pre-financial crisis levels, some analysts believe markets aren’t overvalued yet.

“Sure, the S&P 500’s valuations look high on historical standards, but it’s really about ultra-low yields,” Bill Gross, chief investment officer at Pimco, told CNBC recently, citing Pimco’s “new neutral” mantra that the neutral federal funds rate will be lower for longer. “Based upon our assumption that this new neutral stays low, they’re not as bubbly as some would suggest,” Gross said.

“If fed funds going forward stops at 2% instead of 4%, which is historical, then [the Dow Jones Industrial Average, or DJIA] at 17,000 and high yield spreads at 350 basis points over Treasurys are attractive and are less bubbly than some would imagine,” he said.

In a blog post on July 2, Gross said that the “new neutral” means “all financial assets might logically be repriced relative to historical experience.”

Gross also noted that while the S&P 500’s 10-year cyclically adjusted P/E ratio, or cost adjusted P/E (CAPE), typically has predictive value of whether shares are overvalued, the “new neutral” indicates the CAPE’s historical median valuation of 17 times earnings may need to be adjusted to around 20-22 times. “That would mean the S&P 500’s current CAPE of 25 times isn’t terribly bubbly.”(Source: CNBC.com, July, 2014)

With the stock market setting new highs, investors face unusually tough choices. An examination of historical valuations points to proceeding with caution in the stock market. Normally during these times bonds would provide a safe harbor. Sadly, with interest rates still near historic lows, bonds might not provide the same portfolio protection as in years past and, potentially even worse, bond prices will decline when interest rates rise.

Fed Chairperson Janet Yellen warned investors on July 2 that, “Falling corporate bond spreads and volatility indicators are signs that investors may not fully appreciate the risk of future losses.” She continued her prepared remarks for a speech at the International Monetary Fund by also sharing, “that said, I do see pockets of increased risk-taking across the financial system.”

It’s not easy to structure a portfolio in the face of these risks, but investors still have to make some decisions. Perhaps the best advice is to continue to focus on your personal situation and timelines. Consider these three important questions:

- What is a realistic time horizon for my personal situation?

- What is a realistic return expectation for my portfolio?

- What is my risk tolerance?

Your answers to these questions will help us recommend what type of investment vehicles you should consider, which investments to avoid and how long to hold each of your investment categories before making major adjustments. For example, if you will need more cash flow from your investments over the next few years, you might consider different choices relative to someone who has a ten- to fifteen-year time horizon.

We are continually reviewing economic, tax and investment issues and drawing on that knowledge to offer direction and strategies to our clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

On a final note, remember, one of the major causes of a stock market decline may not be investment performance—sometimes it’s investor behavior.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the “emotions” out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

P.S. During this year’s big Treasury rally, the question has been, “Who’s buying all those bonds?” The answer is the Federal Reserve. During the six months ended in May, the Fed bought 73% of all new Treasurys, notes Strategas Research Partners’ Daniel Clifton. That’s the largest percentage since the start of quantitative easing.

The reason isn’t greater demand, but reduced supply. With the budget deficit falling, the amount of bonds issued has declined faster than the Fed’s taper, or reduction in bond buying. That leaves a limited supply of bonds for others to buy, according to Clifton. Perhaps that’s why bonds have held up in the first half of 2014.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. The investor should note that investments in lower-rated debt securities (commonly referred to as junk bonds) involve additional risks because of the lower credit quality of the securities in the portfolio. The investor should be aware of the possible higher level of volatility, and increased risk of default.

The payment of dividends is not guaranteed. Companies may reduce or eliminate the payment of dividends at any given time.

Sources: CNN Money; Shiller PE Ratio; Barron’s, June 2014; Bob LeClair’s Finance, June 2014; Fidelity; Bob LeClair’s Finance, June 28, 2014; Wall Street Journal; CNBC.com 7/2014 Contents © 2014 Academy of Preferred Financial Advisors, Inc.

Economic Update – First Quarter 2014

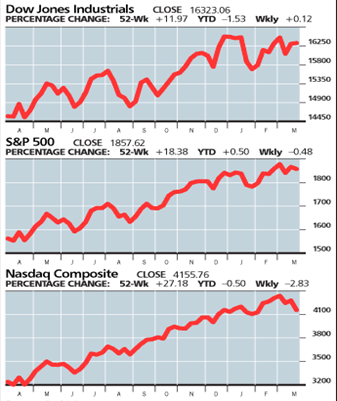

The first quarter of 2014 has proved to be very interesting with results that were significantly different than 2013. For example, the total return of the S&P 500 for the first quarter of 2014 was 1.8%. This is a far cry from the almost 10% rise in the same quarter of 2013. As of March 31, 2014, the Dow fell 0.7%—its first quarterly decline in a year. The NASDAQ ended the quarter up with a gain of 0.5%.

The first quarter of 2014 has proved to be very interesting with results that were significantly different than 2013. For example, the total return of the S&P 500 for the first quarter of 2014 was 1.8%. This is a far cry from the almost 10% rise in the same quarter of 2013. As of March 31, 2014, the Dow fell 0.7%—its first quarterly decline in a year. The NASDAQ ended the quarter up with a gain of 0.5%.

Contributing to the fall were concerns about many stocks’ rich valuations and lawmakers’ questions about high drug prices. During the quarter many stocks struggled to maintain the upward momentum of 2013, though they remained near record highs a majority of the past three months.

Fortunately for investors, stocks staged a broad rally on the last day of the quarter and kicked off the second quarter with major gains, propelling the S&P 500 to its seventh record close of the year. Although the Dow closed at the highest level of 2014, it was still 0.3% short of its December 31st record finish. (WSJ – April 2, 2014)

The Economy

The U.S. economy expanded at a 2.6% annual rate in the fourth quarter of 2013, up from 2.4% due to a revised calculation. Many economists expect economic growth to rebound in the second quarter as the weather improves. (WSJ – April 4, 2014)

One major problem in the first quarter was that U.S. exports fell in February due to weak demand overseas. This also caused the largest trade deficit since December of last year. (WSJ – April 4, 2014)

Another area of disappointment came from new-home sales, which dropped by 3.3% in February. Higher mortgage interest rates and poor weather conditions seemed to contribute to the decline.

But let’s look on the bright side. Most economic data has been positive recently and growth seems to be gaining traction, though at a pace less than we would like to see:

- Real GDP rose higher than its earlier estimate, chiefly due to consumer and business spending.

- The Conference Board’s Index of Consumer Sentiment climbed to 82.3 in March, its highest level in six years.

- Orders for durable goods also increased, along with personal income and spending.

The bottom line is that things are continuing to improve gradually. According to sources at Economy.com, “The economy’s fundamentals are strong. Businesses are profitable and competitive. Household debt loads are low and credit conditions are strengthening. Banks are well capitalized and liquid. The fiscal health of government at all levels is much improved.” (Bob Leclair’s Finance & Markets Newsletter- Mar. 29, 2014)

Possible Stock Market Correction

The U.S. equity markets provided strong gains in 2013. Despite worries about Fed tapering and higher interest rates, Washington’s dysfunctional behavior and a modest economic recovery, the S&P 500 rose almost 30% for the year. However, many investors started speculating about when the next correction would arrive and what could cause it.

The U.S. economy surged in the last quarter of 2013 and appears set to maintain that momentum. Even with this positive outlook, it shouldn’t surprise any investor if a market correction comes along and produces a decline of 10-12% and lasts up to eight weeks or longer.

One of the most obvious triggers for a correction could be a stalling U.S. economy. The economic data seem to show the economy continuing to recover at a modest pace, but there are still significant pockets of weakness and things could potentially change rapidly.

Another potential risk is high expectations for corporate earnings in 2014 and beyond. Many economists are skeptical that earnings growth can meet projections. If the market comes to the conclusion that the economy is not going to see that kind of earnings growth, this could be the catalyst that might cause a major correction. Also, an increase in the costs of raw materials, labor or interest expense could pose a threat to profit margins. If profit margins slip, current stock evaluations might prove unsustainable.

Outside factors are the most likely threats to the U.S. economy. Europe is a long way from resolving its problems or even being on a long-term path to recovery, and it could spin out of control at any time. China is changing its policies and those changes will affect the global economy. There are several significant emerging economies that could have debt payment or economic problems. A wide range of global political issues may also result in a crisis or war that could unsettle markets.

Of course, there may not be a correction at all. A major argument supporting that possibility is the fact that U.S. businesses are sitting on cash at a level not seen since WWII. According to Liz Ann Sonders, Chief Investment Strategist at Charles Schwab and Company, Inc., “We know the capital is there, but we haven’t had the animal spirits to put it back to work yet. But this is the year we’ll probably see increase in [capital expenditure] spending.” (Investment News–Feb. 2014)

Potential problems will always cause concern for the equity markets, but this does not necessarily mean you should constantly alter your portfolio. A prudent approach is to invest in a manner that will not cause you to be up all night worrying about your investments.

Interest Rate Changes

Long-term treasury interest rates moved a little lower at the end of the quarter. Many investors did not expect this when the Fed began to cut back on its bond-buying program. Although treasury rates have dropped, mortgage interest rates moved higher. This movement might have put a chill into new-home sales. Many investors are concerned that housing might not prove to be the investment that it has been in the past.

During this quarter, Federal Reserve Chairwoman Janet Yellen offered new assurances that the Fed plans to keep short-term interest rates near zero as long as unemployment stays relatively high and inflation low. This is what Ben Bernanke said throughout his term as Fed chief. On March 31st, in her first public remarks outside Washington since she took the Fed’s helm in February, Ms. Yellen said, “While there has been steady progress, there is also no doubt that the economy, and the job markets, are not back to normal health.” She also used unusually personal terms to describe why the economy needs these policies to support a weak job market, saying, “The Recovery still feels like a recession to many Americans, and it also looks that way in some economic statistics.” (WSJ, April 1, 2014)

The Fed announced on December 18th that it would start to reduce its bond‑buying program. It decreased its buying from $85 billion down to $75 billion in January of this year, $65 billion in February and March, and now $55 billion starting in April. What is left unsaid is how the tapering process will unfold from here. If left unchanged through the end of 2014, the Fed’s balance sheet will add $635 billion by December 31, 2014, taking the Fed’s total assets to $4.4 trillion. The Fed held only about $480 billion (i.e. $0.480 trillion) of securities in early September 2008. (Federal Reserve– March 19, 2014)

Bond Market Risks

The bond market continues to confuse many investors. Since the Fed announced the tapering, there has been an expectation that interest rates would rise. However, bond prices are actually higher and interest rates are lower.

The bond market continues to confuse many investors. Since the Fed announced the tapering, there has been an expectation that interest rates would rise. However, bond prices are actually higher and interest rates are lower.

The long end of the treasury yield curve has flattened a bit, which suggests that many bond investors don’t see much in the way of U.S. economic growth. That is one of the reasons that many investors have put their money to work overseas. (Barrons – March 31, 2014)

Investors might still put their money into long-term bonds for safety. In fact on several occasions, bonds delivered strong returns. Currently, though, with market interest rates at such a low level, it’s difficult to even think that bonds will be able to offer most investors that kind of return at this time.

In the past, bond yields might have been high enough to compensate for their drop in value even if interest rates increased. But today, with interest rates remaining low, the math just doesn’t work. Conservative and moderate investors still need to consider bonds, but they should proceed with caution. We will be monitoring the bond market carefully over the next year or two. (Money Magazine – Jan. 2014)

Quantitative Easing

We are currently experiencing QE3, which started in September 2012 at $40 billion dollars of monthly bond purchases, increased to $85 billion/month in December 2012, and is now $55 billion/month. Five years ago, on President Obama’s inauguration day, the U.S. had a total debt of $10.6 trillion. By January 15, 2014, that number was up to $17.3 trillion. The increase of $6.7 trillion over this five‑year period equals an average daily deficit of $3.6 billion! (Treasury Department, January 20, 2014)

However, there is also some good news – reports in the first quarter of 2014 showed that December 2013 produced a surplus of $53 billion for the U.S. government. This was the first time that December has had “receipts in excess of outlays” since December 2007. (Treasury Department, January 2014)

What Should an Investor Do?

Be watchful. On March 9, 2014, the S&P 500® Index reached the fifth year of the bull market, which is quite an accomplishment. Since the global financial crisis hit bottom on March 9, 2009, the S&P has risen a cumulative 178%. This is quite an accomplishment: of the 13 bull markets since 1928, only four have made it to their fifth anniversary, and only two went on beyond a sixth. This worries some investors who fear the market might be nearing its peak. (Fidelity, March 2014)

Put the current bull market into context. Today’s bull market has been strong, but it follows the third-worst bear market (a drop of 57% compared to the average of 37%). The current bull market also took much longer to return to its previous peak (4+ years vs. the 2-year average). While no one can predict the future, prior bull markets that survived beyond their five-year anniversaries went on to post much higher returns. (Fidelity, Mar. 2014, Bloomberg Finance, L.P.)