Economic Updates

Stay up-to-date on economic conditions and outlook with our analysis and commentary.

How the New Tax Law Could Impact You

By Samantha Webster

By Samantha Webster

In December, our team compiled an overview of the various provisions found within the Tax Cuts & Jobs Act of 2017.

The new tax legislation brought about significant changes to several areas of the federal tax code, some of which could impact you and your family.

Although the tax legislation is far-reaching and nuanced, one of the key themes of the new law is increasing the standard deduction while phasing out certain itemized deductions. Single filers can now claim a $12,000 standard deduction; $24,000 for joint filers.

As such, we would like to take the opportunity to hone in on three specific itemized deductions that have been reduced – mortgage deductions, state and local tax (SALT) deductions, and medical expense deductions.

These particular changes to the tax bill could influence the approach you take when filing your 2018 tax return, as well as the financial decisions you make throughout the course of the year.

Important: Several areas of the new law were implemented on a “sunset provision” basis, meaning that the changes will revert to previous levels at the end of 2026 unless Congress reauthorizes the provisions.

Mortgage Deductions

For many Americans, becoming a homeowner is seen as an integral part of the American dream. Owning a house is not only a source of pride and stability, but your home is also a key asset that constitutes a considerable proportion of your net worth.

Owning a home also carries substantial tax benefits in the form of deducting mortgage debt interest from your individual tax return.

What Changed? – Prior to the new tax law, homeowners could deduct interest on up to $1 million in mortgage debt on their primary residence, as well as deduct interest on up to $100,000 in a home equity line of credit (HELOC).

Under the new tax law (effective December 14, 2017), homeowners may deduct interest on up to $750,000 in mortgage debt on the primary residence. The HELOC deduction has been eliminated entirely.

The changes to mortgage and HELOC deduction caps were passed as a “sunset provision” and will be reverted to their previous level in 2026 if Congress does not reauthorizes the new thresholds.

Who Is Impacted? – Anyone who took out a mortgage after December 14, 2017, will be subject to the $750,000 mortgage interest deduction cap. If you purchased your home prior to this date, the $1.1 million in deductions are still available to you.

The Bottom Line – Since the vast majority of homes in the U.S. are valued at under $750,000, the change should not directly impact most homeowners.

However, the new tax law may reduce the incentive for potential homebuyers to take out a mortgage that exceeds the $750,000 threshold. Also, homeowners who were considering whether to sell a house that is valued at more than $750,000 may opt to hold off until the deductions are reverted to previous levels in 2026.

These two factors could increase competition over an already limited supply of homes valued under $750,000 – which could cause home equity to rise for these residences, while also boosting the appeal of renting over buying for potential first-time homebuyers.

Lastly, homeowners may be more hesitant to open a home equity line of credit for a second mortgage or when refinancing their house.

State and Local Tax Deductions

Across the U.S., there is a great disparity between both states and cities in terms of the taxes you owe. Whereas Florida and Texas have no state income taxes, people living in Manhattan are faced with hefty taxes from both New York State and New York City.

The state and local tax (SALT) deduction provides some relief to residents of high-tax, high-cost areas of the country on their federal tax returns.

What Changed? – The old tax code allowed you to deduct all property taxes paid to your state and local government from your federal tax return. Income or sales taxes paid at the state or local level were also eligible to be deducted from your federal taxes.

The new law mandates that the amount of state and local taxes you may deduct from your federal taxes will be capped at $10,000 per household. This limitation applies to both individual and joint filers.

As with the changes to mortgage deduction thresholds, the new SALT deduction cap will sunset in 2026 if Congress does not reauthorize.

Who Is Impacted? – Residents of high-tax states (e.g. New York, California, Connecticut) and residents of coastal cities where property values and cost of living are high (Boston, Seattle, Washington, D.C.) will bear the brunt of the federal tax liability that results from the SALT deduction cap. This is especially true for people whose combined mortgage and SALT itemized deductions exceed the new standard deduction.

People residing in areas where taxes and cost of living are relatively low will see little (if any) impact on their federal taxes as a result of this provision.

The Bottom Line – For many residents of New York and the other high-tax states/cities listed, $10,000 may not cover the full amount of your property taxes – let alone other state and local taxes you have paid.

Although state legislatures in New York and California are brainstorming new ways to circumvent the added federal tax burden on their constituents, it appears that – for now – residents of the high-tax coastal states will be left picking up the tab.

Medical Expense Deductions

Given the skyrocketing cost of health care, it is reassuring to know that a portion of your annual out-of-pocket medical expenses may be deducted from your federal taxes.

What Changed? – For your 2017 tax return, you could claim an itemized deduction for out-of-pocket medical expenses that exceeded 10% of your adjusted gross annual income.

The new legislation allows you to deduct out-of-pocket medical expenses that exceed 7.5% of your adjusted gross annual income for the year 2018 only. By lowering the threshold, you can deduct more medical expenses from your taxes. Without Congressional reauthorization, the floor will be raised back to 10% in 2019.

Who Is Impacted? – People with substantial medical bills (relative to their income) – especially those with chronic illnesses or disorders that require continual care – will be able to deduct a larger share of their medical expenses. In particular, those who are in poor health and do not yet qualify for Medicare would receive the greatest assistance in 2018.

If your medical costs are less than 7.5% of your income, there is no added benefit.

The Bottom Line – The new tax law provides a welcome gift – albeit fleeting – to Americans who are plagued with hefty medical bills. The medical expense deduction could help to temporarily alleviate the financial strain on these families – potentially offsetting any increases in insurance premiums that might occur in 2018.

Although these tips provide you with a more detailed understanding of three particular provisions in the new tax law, you should review your unique circumstances with your advisor before making any substantial life changes (selling a home, undergoing a major medical procedure, etc.) to determine the best opportunities for tax relief.

Our CAS team is constantly monitoring any proposed legislation that could impact your financial wellness, and we will continue to keep you abreast of any pertinent topics that might affect you and your family.

Tax Reform Special Update

The GOP has delivered on its campaign promise to overhaul the federal tax code. Both the Senate and the House voted in favor of The Tax Cuts and Jobs Act of 2017, and the President signed the bill into law on Friday.

Our team has combed through all of the major provisions in the tax reform legislation and identified eight key changes that could impact you and your family.

#1 – Individual Tax Brackets and Standard Deductions

Despite the GOP’s desire to reduce the number of individual tax brackets, the final bill retains the 7-tiered individual progressive income tax brackets. The new tax brackets for individuals and families are 10 percent, 12 percent, 22 percent, 24 percent, 32 percent, 35 percent and 37 percent (see the chart below for a more detailed breakdown by income level).

As such, many Americans will see a slight reduction in their top marginal tax rate. That being said, these updated brackets were passed on a “sunset provision” basis – meaning that the updated tax rates will expire and revert to current levels at the end of 2025 unless Congress reauthorizes the lower rates.

Secondly, the standard deduction will essentially double for both individuals and families. Whereas the current standard deductions are $6,500 for individuals and $12,000 for families, the new standard deductions will be $13,000 for individuals and $24,000 for families.

For most working- and middle-class families, this piece of the tax bill represents the greatest source of tax cuts that each family will realize. In addition to an increased standard deduction, several itemized deductions will be reduced or phased out of the tax code (more details in the following sections).

The intention of increasing the standard deduction is to simplify the tax-filing process for individuals – encouraging more people to claim the standard deduction as opposed to itemizing their deductions.

Figure 1 – Marginal tax rates for individuals under the new tax legislation

#2 – State & Local Tax Deductions and Mortgage-Interest Deductions

One point of contention in the earlier stages of the tax legislation was state and local tax deductions. While the original House proposal called for the elimination of this deduction, pushback from House members in high-tax states persuaded Congress to compromise on this provision. As a result, taxpayers will be able to deduct up to $10,000 in state and local income, property and/or sales taxes from their federal tax burden.

In addition, you may deduct up to $750,000 of mortgage interest under the new tax proposal (a reduction from the current cap of $1 million). This deduction can be applied to your primary residence and one other qualified residence (which could include a vacation home, mobile home or a boat).

As with the new individual tax rates, the revisions to both of these deductions would sunset after 2025.

#3 – Medical Expenses Deduction

In 2017 and 2018, you will be able to deduct out-of-pocket medical expenses that exceed 7.5% of your gross adjusted income (but not on health care expenses that are less than 7.5%). For instance, if you earn $100,000 in a year and your out-of-pocket medical costs are $12,000, you may deduct $4,500 in medical expenses.

Effective January 2019, the threshold will return its current level, with any out-of-pocket medical expenses that exceed 10% of your gross adjusted income being tax-deductible.

#4 – Estate Tax

Due to resistance in the Senate, the GOP was unable to pass a “clean repeal” of the estate tax; and the 40% tax rate will remain unchanged. That being said, they have significantly raised the exemption threshold on taxable estates – meaning that fewer people will be subject to the estate tax.

Under the new policy, individual estates valued under $11.2 million ($22.4 million for couples) would be exempt. Once again, the estate tax provisions will expire at the end of 2025.

#5 – Alternative Minimum Tax

The alternative minimum tax – which is primarily levied on individuals and families who earn more than $200,000 annually – will remain intact. Although the assessment of this tax can vary significantly based on your personal circumstances, the exemptions and phase-outs will be slightly raised. As a result, fewer people will have to pay the tax and those who do will pay a smaller sum. These changes also sunset after 2025.

The 20% corporate alternative minimum tax has been permanently repealed.

#6 – Corporate Tax Rate

Perhaps the most drastic change to our tax code can be observed in the reduction of the corporate tax rate. Whereas the current rate is 35%, the new corporate tax rate will be 21%. Unlike many provisions in the bill, these tax cuts are permanent (i.e. the new rates do not sunset in 2025).

The substantial reduction aligns with the GOP’s promise to slash the corporate tax rate, with the goal of stimulating economic growth. However, contrary to the rhetoric on the campaign trail, none of the tax loopholes or deductions for special interests were eliminated – meaning that many larger, publicly traded corporations will pay an even lower effective tax rate.

#7 – Pass-Through Businesses

Small business owners have typically paid income taxes at their individual tax rate – particularly those who earn income via pass-through entities (limited-liability companies, S corporations, partnerships and sole proprietorships).

However, the tax legislation allows individuals to deduct 20% of their qualified business income, up to $157,500 for individuals ($315,000 for joint filers). For small business owners, this deduction will greatly reduce their tax liability. The provisions for pass-through businesses will also expire at the end of 2025.

#8 – Individual Healthcare Mandate

One of the most controversial provisions of the Affordable Care Act (colloquially known as Obamacare) is the individual mandate, where individuals must either purchase a qualifying health insurance plan or pay an annual penalty. Under the new tax code, the individual mandate penalty would be eliminated – reducing the incentive for healthy individuals to sign up for coverage.

Repealing the individual mandate is expected to lead to higher premiums for those who do not qualify for government subsidies or Medicare, and constitutes a renewed effort by the GOP to gradually do away with the Affordable Care Act.

For additional details on how the new tax legislation could affect you and your family, contact your advisor.

Tax Reform – Will They or Won’t They?

You can be forgiven if you’re skeptical that Congress will be able to completely overhaul our tax system after failing to overhaul our health care system, but our advisors are studying the newly-released nine-page proposal closely nonetheless. We only have the bare outlines of what the initial plan might look like before it goes through the Congressional sausage grinder:

We would see the current seven tax brackets for individuals reduced to three — a 12% rate for lower-income people (up from 10% currently), 25% in the middle and a top bracket of 35%. The proposal doesn’t include the income cutoffs for the three brackets, but if they end up as suggested in President Trump’s tax plan from the campaign, the 25% rate would start at $75,000 (for married couples), and joint filers would start paying 35% at $225,000 of income.

The dreaded alternative minimum tax, which was created to ensure that upper-income Americans would not be able to finesse away their tax obligations altogether, would be eliminated under the proposal. But there is a mysterious notation that Congress might impose an additional rate for the highest-income taxpayers, to ensure that wealthier Americans don’t contribute a lower share than they pay today.

The initial proposal would nearly double the standard deduction to $12,000 for individuals and $24,000 for married couples, and increase the child tax credit, now set at $1,000 per child under age 17. (No actual figure was given.)

The chief architects of the GOP tax reform proposal – economic advisor Gary Cohn and Treasury Secretary Steven Mnuchin – unveiled their plan with the President at Trump Tower.

At the same time, the new tax plan promises to eliminate many itemized deductions, without telling us which ones other than a promise to keep deductions for home mortgage interest and charitable contributions. The plan mentions tax benefits that would encourage work, higher education and retirement savings, but gives no details of what might change in these areas.

The most interesting part of the proposal is a full repeal of the estate tax and generation-skipping estate tax, which affects only a small percentage of the population but results in an enormous amount of planning and calculations for those who ARE affected.

The plan would also limit the maximum tax rate for pass-through business entities like partnerships and LLCs to 25%, which might allow high-income business owners to take their gains through the entity rather than as income and avoid the highest personal brackets.

Finally, the tax plan would lower America’s maximum corporate (C-Corp) tax rate from the current 35% to 20%. To encourage companies to repatriate profits held overseas, the proposal would introduce a 100% exemption for dividends from foreign subsidiaries in which the U.S. parent owns at least a 10% stake, and imposes a one-time “low” (not specified) tax rate on wealth already accumulated overseas.

What are the implications?

The most obvious, and most remarked-upon, is the drop that many high-income taxpayers would experience, from the current 39.6% top tax rate to 35%. That, plus the elimination of the estate tax, plus the lowering of the corporate tax (leading to higher dividends) has been described as a huge relief for upper-income American investors, which could fuel the notion that the entire exercise is a big giveaway to large donors. But the mysterious “surcharge” on wealthier taxpayers might take away what the rest of the plan giveth.

But many Americans with S corporations, LLCs or partnership entities would potentially receive a much greater windfall, if they could choose to pay taxes on their corporate earnings at 25% rather than nearly 40%. (Note: The Trump organization is a pass-through entity.)

A huge unknown is which deductions would be eliminated in return for the higher standard deduction. Would the plan eliminate the deduction for state and local taxes, which is especially valuable to people in high-tax states such as New York, New Jersey and California, and in general to higher-income taxpayers who pay state taxes at the highest rate?

Currently, about one-third of the 145 million households filing a tax return — or roughly 48 million filers — claim this deduction. Among households with income of $100,000 or more, the average deduction for state and local taxes is around $12,300. Some economists have speculated that people earning between $100,000 and around $300,000 might wind up paying more in taxes under the proposal than they do now. Taxpayers with incomes above $730,000 would hypothetically see their after-tax income increase an average of 8.5%.

Big picture, economists are in the early stages of debating how much the plan might add to America’s soaring $20 trillion national debt. One back-of-the-envelope estimate by a Washington budget watchdog estimated that the tax cuts might add $5.8 trillion to the debt load over the next 10 years.

According to the Committee for a Responsible Federal Budget analysis, Republican economists have identified about $3.6 trillion in offsetting revenues (mostly an assumption of increased economic growth), so by the most conservative calculation, the tax plan would cost the federal deficit somewhere in the $2.2 trillion range over the next decade.

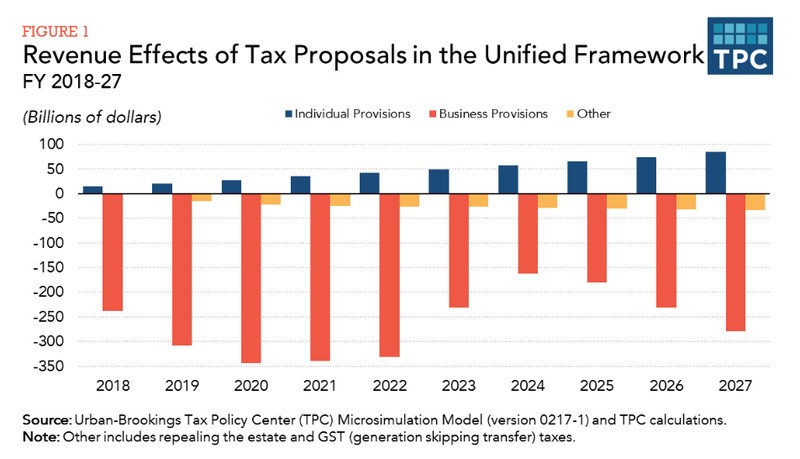

Others, notably the Brookings Tax Policy Center (see graph) see the new proposals actually raising tax revenues for individuals (blue bars), while mostly reducing the flow to Uncle Sam from corporations.

These cost estimates have huge political implications for whether a tax bill will ever be passed. Under a prior agreement, the Senate can pass tax cuts with a simple majority of 51 votes — avoiding a filibuster that might sink the effort — only if the bill adds no more than $1.5 trillion to the national debt during the next decade.

That means compromise. To get the impact on the national debt below $1.5 trillion, Congressional Republicans might decide on a smaller cut to the corporate rate, to something closer to 25-28%, while giving typical families a smaller 1-percentage point tax cut. Under that scenario, multi-national corporations might be able to bring back $1 trillion or more in profit at unusually low tax rates, and most families might see a modest tax cut that will put a few hundred extra bucks in their pockets.

Alternatively, Congress could pass tax cuts of more than $1.5 trillion if the Republicans could flip enough Democratic Senators to get to 60 votes. The Democrats would almost certainly demand large tax cuts for lower and middle earners, potentially lower taxes on corporations and higher taxes on the wealthy. Would you bet on that sort of compromise?

Special thanks to Bob Veres for his commentary.

The Future of Brick-and-Mortar Retail

The rise of e-commerce has been a disruptive force in the retail sector. In fact, 5,300 store closings were announced in the first half of 2017 — about three times as many as during the same period in 2016. At this pace, the 2017 total should easily exceed the 6,163 store closings in 2008, the worst year on record. Retail bankruptcies have also been on the rise, with 345 companies filing by mid-year.1

A painful recession was to blame for thousands of retail store casualties in 2008, but for the most part, the U.S. economy has been humming along in 2017. The unemployment rate dropped to 4.3% in June, and gross domestic product grew at a 2.6% annual rate in the second quarter, driven by a 2.8% increase in consumer spending.2 So why is 2017 turning out to be such a tough year for retailers?

Structural Shakeout

Brick-and-mortar retailers are losing market share to e-commerce sites such as Amazon. Average monthly sales at department stores were $7.3 billion less in 2016 than they were in 2000, while non-store retail sales increased by $35 billion.3 The Internet also makes it easier for shoppers to research products and compare prices, reducing foot traffic in stores and limiting pricing power. Here are several more trends that have created challenges for the nation’s retailers.

Profit pressure. Even though many traditional retail chains have invested in e-commerce channels, online sales require higher technology, customer acquisition, and marketing costs than in-store sales, which reduces their profit margins. E-commerce sales increased to 15.5% of total sales in 2016, up from 10.5% in 2012, while retail margins fell from 10.5% to 9%, on average.4

Mall bubble. The shift to e-commerce was preceded by several decades of overbuilding. Between 1970 and 2015, the number of U.S. malls grew twice as fast as the population, leaving the United States with five times more shopping space per person than the United Kingdom, and 10 times more than Germany.5

Debt burden. Some companies are also struggling under heavy debt loads, making it more difficult to turn a profit and fund investments needed to compete in the e-commerce arena. Overall, the amount of retail debt rated by Moody’s has surged 65% since 2007.6

Reluctant shoppers. Many Americans (and especially young consumers) now prefer to spend their money on special experiences with friends and family (such as travel and restaurant meals) rather than material goods such as clothing and jewelry. For example, spending in restaurants and bars has grown twice as fast as all other retail spending since 2005. And 2016 was the first year ever that U.S. consumers spent more money eating out than they spent on groceries.7

Coping Strategies

Retailers that specialize in goods that are difficult to buy online (such as home improvement supplies) and stores that appeal to “bargain hunters” may fare better than pricier department stores and mall chains that mostly sell apparel and accessories, an e-commerce category that is growing quickly.8 Inside or outside of bankruptcy, many retailers are working to improve their future prospects by renegotiating more affordable leases and reducing their real estate “footprint,” which often involves closing underperforming stores and/or moving into smaller spaces.

Other common strategies include elevating the in-store shopping experience, focusing on exclusive brands, and using loyalty programs to reward and retain customers.9 Retailers are also working to integrate online and in-store sales channels, which makes it easier for customers to locate the items they want and finalize their purchases. To help generate online and in-store sales, many companies are using technology that tracks customer behavior and uses the data to create targeted marketing strategies and promotions.

Even so, as many as one-fourth of the nation’s 1,200 malls could close by 2022, primarily aging properties in less prosperous communities. A number of malls with advantageous locations are being redeveloped into lifestyle destinations with activities and entertainment (such as athletic facilities and concert venues) designed to attract foot traffic to the remaining stores and restaurants. Mall tenants are likely to become more diverse, with a wider range of service providers and fewer clothing stores.10

Economic Effects

Nearly 16 million people work in retail, many as cashiers or salespeople. From January to June, the U.S. economy shed about 71,000 retail jobs, and job losses could continue as long as the sector continues to struggle.11 E-commerce employment is expanding considerably, but most of these new jobs are in or near metropolitan areas. If large-scale dislocation of retail jobs continues, the economic effects could be worse for rural areas than for larger cities.12

The growth in e-commerce may also be holding down inflation. According to the PCE price index, inflation increased just 1.4% in June over the previous year.13 Consumers have largely benefited from lower prices resulting from intense competition among retailers, some of which now offer to match online prices. More household names could cease to exist in the coming months, and some of their competitors might even benefit from industry consolidation. In the end, a retail company’s long-term survival may depend on its ability to adapt quickly to an ever-changing market environment.

Sources

1) CNNMoney, June 23, 2017

2, 13) The Wall Street Journal, August 1, 2017

3) The Wall Street Journal, May 11, 2017

4, 8) The Wall Street Journal, April 21, 2017

5, 7) The Atlantic, April 10, 2017

6) The Wall Street Journal, July 17, 2017

9) The Wall Street Journal, February 28, 2017

10) The Los Angeles Times, June 1, 2017

11) The Wall Street Journal, July 19, 2017

12) The New York Times, June 25, 2017

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Where Do Your Tax Dollars Go?

As you look back on your tax payments for calendar year 2016, you’re undoubtedly wondering where those dollars are being spent.

The Wall Street Journal recently published a report that breaks down government spending for every $100 of tax receipts. The report concluded that the U.S. government is, in reality, a large insurance company that also happens to have an army.

For every $100 you pay in taxes, $23.61 goes to Social Security payments and administration – basically insurance for retirees. Another $15.26 goes to Medicare, the government health insurance program. Medicaid, the health insurance program for the poor, accounts for another $9.55 of that $100 tax bill – bringing the total costs for various civilian insurance programs to 48% of the total budget.

And that army? It costs $15.24 of every $100 the government collects in taxes, not counting veterans benefits.

In all, the 2016 federal budget fell $15.24 short out of every $100 of revenues equaling expenses. So where would you cut?

Things like federal expenditures and grants for education ($2.08), food stamps ($1.89), affordable housing ($1.27) and foreign aid ($1.14) actually make up a very small part of the budget, smaller than interest payments on the national debt ($6.25).

There has been talk about helping reduce the budget by lowering expenditures on the National Endowments for the Arts and Humanities, which together represent eight-tenths of one cent of that $100 tax bill. This would be comparable to someone trying to pay off his mortgage by looking for coins under the sofa cushions!

Source:

Special thanks to Bob Veres for his commentary

https://www.wsj.com/articles/how-100-of-your-taxes-are-spent-8-cents-on-national-parks-and-15-on-medicare-1492175921

Brexit is Beginning

If you have a good long memory, you may recall that last summer, the U.K. panicked the investment markets by voting, in a nation-wide referendum, to exit the European Union. There were, of course, dire predictions about the impact on the U.K. economy, which never materialized, in large part because the U.K. had not yet formally opted out of its Eurozone agreements.

At the end of March, the U.K. finally pulled the trigger and made the departure from the European Union official. The Queen of England delivered her royal assent, and the U.K.’s envoy to the European Union hand-delivered a letter to the office of the European Council president in Brussels invoking Article 50 of the EU treaty. This delivered formal notification of the Brexit decision, the first time this has happened in the EU’s history.

So that means those dire predictions will finally come true. Right?

As it happens, Article 50 was intended to prevent any rash or immediate consequences of an exit from EU membership, and it seems to have accomplished that goal. Under the bylaws, the divorce will be negotiated, item by item, over the next two years, meaning that any change in economic circumstances will be gradual and perhaps accommodated as they happen. How gradual? Over the next several weeks, the EU’s remaining 27 members will discuss their priorities in advance of the negotiations, and then hold a summit on April 29. Only then will the European Commission have a mandate to negotiate with representatives from London.

What will the negotiations cover? First up will be Britain’s obligations to the EU for its participation thus far—a bill that could total up to roughly $65 billion. Also: what will be the rights of 3 million EU citizens living in the U.K., and the rights of more than 1 million Britons living and working in the Eurozone?

After that, it is speculated that the British government will seek to negotiate a broad free-trade agreement which will effectively replicate the provisions of its former membership in the European Union, as a way to protect its commercial ties with the Continent. This is where negotiations will get sticky, since France and Germany will almost certainly oppose a no-consequences exit, and they will want to protect their own economies’ free-trade access to Eurozone markets. On the EU side, a simple majority of countries will decide what proposals are accepted and which are sent back to the negotiating table—with one notable exception: any free trade agreement between the two sides much win unanimous approval.

This latter issue is problematic for the U.K., because it exposes each country to yet another referendum on the conditions of EU membership; the citizens of France, Germany, Luxembourg, Ireland, Holland and, well, all the other nations would want to be involved in the final decision, which would give them yet another opportunity to voice displeasure with the EU and stir up nationalistic parties and sentiments.

Also still to be determined are budgetary considerations. The U.K.’s contribution to the governing infrastructure of the EU will have to be made up by the remaining members, whose citizens are not eager to contribute more to the increasingly unpopular entity. The British government, meanwhile, will have to create an expensive governance infrastructure to replace the EU bureaucracy in Brussels, and Parliament will have to formally repeal the European Communities Act of 1972, making EU law U.K. law. Then, parallel with the EU negotiations, Parliament will debate every aspect of the EU law and decide which to keep long-term and which to drop. That, too, will take years.

The bottom line is that nothing dramatic is likely to happen, economically and in the investment markets, for years. Throughout the two years of negotiations, the U.K. will remain a full EU member, albeit without a chance to participate in EU decision-making. Some are predicting that the discussions will last for several additional years, with extensions on the status quo until issues can be ironed out. Unpicking 43 years of treaties and agreements covering thousands of different subjects will not be an easy task.

Those investors who overreacted to the initial (and shocking) Brexit vote sold their stocks into a market rally, and there is no reason to think that those who might panic now that the trigger is finally pulled will fare any differently. Both sides in this negotiation have a stake in not having anything dramatic—particularly dramatically damaging—from happening, and they will probably succeed in making Brexit a boring exercise in bureaucratic handover.

Sources:

Special thanks to Bob Veres for his commentary.

https://www.stratfor.com/geopolitical-diary/brexit-has-begun-now-what?utm_source=Twitter&utm_medium=social&utm_campaign=article

https://www.theatlantic.com/news/archive/2017/03/brexit-faq/521175/?utm_source=atltw

Fed Announces Rate Hike

As the U.S. economy and the stock market continue to see sustained growth, the Federal Reserve has elected to increase the interest rates once again. Just as in December, the latest Fed rate hike is quite conservative: an increase of 0.25%, to a range of 0.75% to 1%. As indicated in the chart, the rates remain historically low.

While the Fed’s decision to move forward with another modest rate hike was not surprising, the more consequential aspect of this story is their intention to gradually increase the rates over the next several years.

The below dot plot illustrates the interest rates that have been projected by each of the 17 Federal Reserve policy board members.

The majority of policy board members said they believe the interest rates should be increased to a range of 1.25-1.5% by the end of 2017 – indicating that we could see two or three more rate hikes before the end of the year. By the end of 2019, the Fed policy board anticipates an interest rate of about 3% – a considerable increase from the current rates, but a fairly moderate rate when compared to historical levels.

The latest interest rate projections are consistent with the Fed’s December projections, reflecting the Fed’s overarching goal of tying future rate increases to U.S. economic progress.

How Does the Rate Hike Affect You?

The rise in rates is good news for those who believe that the Fed has intruded on normal market forces by suppressing interest rates much longer than could be considered prudent, and even better news for people who are bullish about the U.S. economy.

However, bond investors might be less enthusiastic, as higher bond rates mean that existing bonds lose value. The recent rise in bond rates suggests that the bull market in fixed-rate securities may finally be waning.

The impact on stock investors is more complex. Bonds and other interest-bearing securities compete with stocks, in the sense that they offer stable returns on your investment. As interest rates rise, some stock investors could be inclined to move a portion of their investments into the bond market – reducing demand for stocks and potentially lowering future returns.

As the Fed contemplates more rate hikes in 2017 and 2018, our family team of advisors will continue to closely monitor the market and offer recommendations that reflect your current situation and future objectives.

Sources:

https://www.ft.com/content/76cffb46-6661-3424-ba07-0e11e3a58cbe

https://www.washingtonpost.com/news/wonk/wp/2017/03/15/fed-hikes-interest-rate-hits-brakes-on-growing-economy/?utm_term=.55ca0ba430c6

Graphs:

Federal Reserve/Washington Post

Federal Open Market Committee/Financial Times

START – A Guide to the U.S. Economy

By Logan Curti, Lynn A. Ferraina and Jasen Gilbert, CFP®

Based on the January 29 presentation by Garrett D’Alessandro, CEO of City National Rochdale

In the midst of a major transition within our government – the inauguration of President Trump and initiation of a Republican-controlled Congress – many people have expressed uncertainty about the economic conditions that face our nation.

START is an acronym that serves as a useful tool for predicting U.S. economic performance as it relates to our government. Stimulus, Taxes, Attitude, Regulation and Trade are directly impacted by congressional legislation and executive action.

By understanding the interplay between public policy and economic factors, we are able to make informed predictions about the outcomes for investors. We have compiled this article to guide you through the economic landscape over the upcoming years.

Stimulus

Perhaps the most effective way to stimulate the U.S. economy is through increased spending by the government, consumers and corporations.

In terms of public-sector spending, defense and infrastructure spending serve as the foundation for stimulus efforts. As part of our nation’s $18 trillion annual GDP in 2016, about $450 billion was spent on infrastructure projects, whereas more than $600 billion was spent on national defense1.

Infrastructure spending creates well-paying middle-class jobs, and our country has a pressing need for modernization. However, infrastructure projects have a gradual effect on our economy; building a new bridge or upgrading a water system can take several years, and we do not feel the full impact of the stimulus until the project is completed. On the other hand, increased defense spending serves as a means for immediately stimulating the U.S. economy.

The U.S. economy is currently entering its 92nd consecutive month of economic expansion – the longest streak of growth since the 1990s. During the past eight years of expansion, we have experienced a modest but steady rate of GDP growth (between 2-2.25% in annually)2.

Based on the campaign platform of President Trump and the GOP, the U.S. may increase defense and infrastructure spending. This suggests that there may be a low likelihood of recession during the next 18 months.

While the government plays a less direct role in determining consumer spending, about 65-75% of our economy is driven by consumers3 – buying groceries, automobiles, clothing, housing, etc. Healthy consumer fundamentals will help to boost economic growth. Given that the U.S. has a low unemployment rate (4.8%)4 and the lowest level of consumer debt since the early 1980s5, consumer spending may also be on the rise during 2017.

Another critical component of our economy is corporate spending. As a result of business-friendly reforms on taxes and regulations (discussed in the following section), corporations may have more buying power under President Trump.

Taxes

When Congress and the President discuss tax reform, there are two distinct areas of conversation: the tax rates and the tax code. The two parties have different priorities in regards to tax reform, with Trump emphasizing tax cuts more heavily and Congress more focused on simplifying the tax code.

Given that our tax code is more than 10,000 pages long and is full of pork for corporate interests, reform will be a slow, arduous process. Regardless of Congress’ intentions, we likely won’t see any materials changes to the tax code during the next year, or even during the tenure of President Trump.

However, City National Rochdale feels that corporations, wealthy individuals and upper-middle class people may receive substantial tax relief in the form of lower marginal tax rates. Corporations will likely experience the greatest amount of tax reduction. The top federal marginal corporate tax rate is currently 35%; the GOP is proposing a top marginal rate of 20%, and Trump is supporting a 15% top marginal rate6.

For individuals, President Trump is proposing a top marginal tax rate of 33%, while congressional Republicans typically favor a top rate of 35% (the current rate is 39.6%)7. In regards to the capital gains tax and the estate tax, both Trump and the Republicans have advocated for the absolute repeal of these measures. Upper- and upper-middle class individuals will find these tax cuts to be advantageous to their bottom line.

With significantly lower tax rates, the national deficit could rise substantially over the next several years. However, if these tax breaks serve as a catalyst for companies and individuals to start spending more, the economy could boom – which could result in a long-term reduction in the deficit.

Attitude

The attitudes of consumers also play a vital role in shaping the economy. When consumers feel confident about their financial situation, they are inclined to spend more and invest more.

Today, consumer attitudes are positive as a result of various factors. First, the U.S. is the wealthiest country in the world, and we have never held as much wealth as we do today. American households have an estimated $91 trillion of wealth, up from the previous high of $81 trillion in 20078.

Secondly, wages and median household income are on the rise for the first time since 20079. Higher wages for lower- and middle-class consumers help to stimulate the economy. As businesses receive lower tax rates and have more money to spend, we could see this trend continue.

Thirdly, as mentioned earlier, low levels of unemployment and consumer debt also play an important role in shaping positive attitudes about economic performance.

Lastly, when consumers are anticipating lower tax rates, they will be apt to put their tax savings to work – either by spending or investing the surplus. Increased spending and investment both serve to stimulate the economy.

On the other hand, uncertainty about complex situations can reduce consumer confidence. Because of the uncertainty involved with a major governmental transition – particularly given Trump’s reputation of being unpredictable – some emotion-based investors will react too aggressively. This attitude of uncertainty may bring more volatility to the market, but may not affect the long-term trend of steady economic growth.

When taken as a whole, the current public opinion regarding the U.S. economy could spur increased spending from consumers. The increase in our collective purchasing power may stimulate economic growth in 2017.

Regulation

Regulations on the private sector are a balancing act. While too few regulations can lead to volatility, overbearing regulations can hinder investment in our economy. Congressional Republicans want to loosen regulations, whereas President Trump has voiced support for eliminating most regulations. Despite this fundamental difference in opinion, the end goal is consistent: reducing regulations on business owners and corporations.

In particular, banking regulations have created a bottleneck in our nation’s financial system since the recession of 2008. In fact, there is more than $3 trillion in corporate and personal assets that are “frozen” in money market funds under the current system10. By loosening regulations, consumers and companies alike may begin to spend and invest this frozen money.

Under the regulatory and tax environment that have existed since 2008, corporate earnings have increased by 4-5% annually11. The new administration’s proposals to deregulate private enterprise and reduce corporate taxes may have a drastically positive impact on corporate earnings.

Trade

On trade issues, President Trump breaks from the mainline Republicans in Congress. While most Republicans have supported free trade agreements and globalist policies, President Trump has been outspoken in supporting domestic manufacturing and economic protectionism.

Trump’s call for tariffs – or “border adjustment fees” – could lead to an increase in prices for consumers. Levying a 20% tax on all imports from Mexico and China may incentivize consumers to buy more American-made goods; however, the actual burden of the tariff falls on consumers, who would have to pay 20% more for some of the goods they need.

Also, other countries could retaliate if we begin to levy tariffs against their products – sparking a trade war. In the case of China, retaliation of tariffs could be dangerous for the U.S. economy. China owns a significant portion of our national debt and produces a substantial amount of our consumer goods. The risks associated with tariffs against China and Mexico far outweigh the potential benefits for U.S. manufacturing.

When considering trade, the 80/20 rule (otherwise known as the Pareto rule) can be instructive. While the 20% of Americans who are involved in manufacturing benefit from protectionist policies and a weak U.S. dollar, about 80% of our population benefits from free trade and a strong U.S. dollar. In short, free and fair trade policies that embrace globalization lead to a positive impact on our economy.

Conclusion

The first four factors of START – stimulus, taxes, attitude and regulation – are positive indicators for economic growth under the Trump administration. On the other hand, protectionist trade policies could be a wild card that lead to volatility in the market.

Overall, 2017 should be an interesting year for investors.

References

1) Congressional Budget Office 2016 Year-End Report

2) Word Bank Annual GDP Growth Rate by Country, 1961-2015

3) Bureau of Labor Statistics Consumer Spending Report, Year-End 2014

4) Bureau of Labor Statistics Jobs Report, Q4 2016

5) Federal Reserve Consumer Debt Report, Q3 2016

6-7) Congressional Budget Office & Tax Policy Institute, 2016

8) US Department of the Treasury: Financial Crisis Response Report, 2015

9) Bureau of Labor Statistics Jobs Report, Q4 2016

10) A Financial History of the United States: From the Enron-Era Scandals to the Great Recession (Markham, J.W.), 2015

11) U.S. Bureau of Economic Analysis: U.S. Corporate Profits, 1951-2016

This newsletter is an independently created publication which is meant for the general illustration and/or informational purposes only. Although this information has been gathered from sources believed to be reliable, it cannot be guaranteed. The views expressed are not necessarily the opinion of FSC Securities Corporation and should not be construed directly or indirectly, as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets, opinions are subject to change without notice. All Investing involves risk including the potential loss of principal. No investment strategy including buy and hold and diversification can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary and therefore information presented here should only be relied upon when coordinated with professional advice. This information is not to be taken as investment advice or a guarantee of future results.

2016 in Review – An Economic Update

You know you’re deep into a longstanding bull market when you see things like average pedestrians keeping one eye on the market tickers outside of brokerage houses to see when the Dow Jones Industrial Average has finally breached the 20,000 mark. Who would have imagined record market highs at this point last year, when the indices ended the year in negative territory? Or when 2016 got off to such a rocky start, tumbling 10% in the first two weeks—the worst start to a year since 1930?

The markets eventually bottomed in mid-February and began a long, slow recovery, turning positive by the end of March, suffering a setback when the U.K. decided to leave the Eurozone and endured another hard bump right after the elections. In the end, we were disappointed; the Dow finished at 19,762.60 for the year—by the bull market has continued for another year.

This was the second year in a row that the final quarter provided investors with solid gains. The Wilshire 5000–the broadest measure of U.S. stocks—was up 4.54% in the fourth quarter of 2016, ending the year up 13.37%. The comparable Russell 3000 index gained 4.21% in the final quarter, to finish up 12.74% for the year.

This was the second year in a row that the final quarter provided investors with solid gains. The Wilshire 5000–the broadest measure of U.S. stocks—was up 4.54% in the fourth quarter of 2016, ending the year up 13.37%. The comparable Russell 3000 index gained 4.21% in the final quarter, to finish up 12.74% for the year.

Large cap stocks were up as well. The Wilshire U.S. Large Cap index gained 4.14% in the fourth quarter, and finished the year up 12.49%. The Russell 1000 large-cap index closed with a 3.83% fourth quarter performance, and finished the year up 12.05%, while the widely-quoted S&P 500 index of large company stocks was up 3.25% in the fourth quarter, finishing up 9.54% for calendar 2016.

The Wilshire U.S. Mid-Cap index gained 5.31% in the final quarter, finishing the year with a gain of 17.22%. The Russell Midcap Index gained 3.21% in the fourth quarter, and was up 13.80% in calendar 2016.

This was a year to remember for investors in small company stocks. As measured by the Wilshire U.S. Small-Cap index, investors posted an 8.30% gain over the last three months of the year, for a total return of 22.41% over the entire 12 months. The comparable Russell 2000 Small-Cap Index finished the year up 21.31%, while the technology-heavy Nasdaq Composite Index rose 1.34% in the fourth quarter, to finish the year up 7.50%.

International investments contributed a slight decline to overall portfolio returns. The broad-based EAFE index of companies in developed foreign economies lost 1.04% in the fourth quarter of the year, finishing the year down 1.88% in dollar terms. In aggregate, European stocks lost 3.39% for the year, while EAFE’s Far East Index gained just 0.14%. Emerging markets stocks of less developed countries, as represented by the EAFE EM index, gained 8.58% for the year.

Looking over the other investment categories, real estate investments, as measured by the Wilshire U.S. REIT index, lost 2.28% during the year’s final quarter, but managed to finish up 7.24% for calendar 2016.

Last year, investors were wondering why they owned commodities in their portfolios, when their statements showed that the index delivered a whopping 32.86% loss. This year, they may be wondering why they weren’t more committed to the asset class, as the S&P GSCI index gained 27.77%, fueled in part by a 45.03% rise in the S&P crude oil index. Gold prices shot up 8.63% for the year and silver gained 15.84%.

In the bond markets, it’s possible that the decades-long bull market—which basically means declining interest rates—has ended, and the fixed-income world is experiencing rate rises. But despite the nudge by the Federal Reserve Board, the moves have not exactly been dramatic. Over the past year, rates on 10-year Treasury bonds have risen from 2.25% to 2.44%, while 30-year government bond yields have risen from 3.00% to 3.07%. According to Barclay’s Bank indices, U.S. liquid corporate bonds with a 1-5 year maturity have seen yields rise incrementally from 2.4% to 2.8% on average.

As always, there were many unpredictable anomalies in the investment world. In the international markets, anyone lucky enough to have speculated on the Brazilian Bovespa index—comparable to the U.S. S&P 500—would have reaped a gain of 68.9% this year, despite all the headline drama around the Zika virus and political uncertainties that were reported on during the Olympic games. Russian stocks were up 51% for the year, despite the recent sanctions from the U.S. government and the lingering international sanctions related to the invasion of the Crimean peninsula.

What’s going to happen in 2017? Short-term market traders seem to be expecting a robust economic stimulus combined with lower taxes and deregulatory policies that would boost the short-term profits of American corporations. But it is helpful to remember that we are entering the ninth year of economic expansion, making this the fourth longest since 1900. In addition, growth has not exactly been robust; the U.S. GDP has averaged just 2.1% yearly increases since the Great Recession, making this the most sluggish of all post-World War II expansions.

Slow but steady has not been a terrible formula for workers or stock investors. The unemployment rate has slowly ticked down from a post-recession peak of 10% to less than 5% currently. U.S. stock indices are posting record highs with double-digit gains, and that Dow 20,000 level, while essentially meaningless, is still catching a lot of attention.

It’s clear that the new President-elect wants to accelerate America’s economic growth, but the policy prescription has not always been clear. Will we rip up longstanding trade agreements, cut back on immigration quotas and deport millions of workers who crossed the border without a visa? Will there be a wall built between the U.S. and Mexico? Will the government pay for huge infrastructure projects, at the same time reducing taxes and thus raising the national debt? Will Congress raise the debt ceiling without protest if that happens? Will the Fed raise rates more aggressively in the coming year, or cooperate with the President-elect in his efforts to drive the economy into a faster lane?

At the same time, there are many unknowns around the globe. China’s economic growth has stalled for the second consecutive year, and you will soon be reading about a banking crisis in Italy that could force the country to leave the Eurozone—potentially a much bigger blow to European economic unity than Brexit or a still-possible Greek exit. Russian hackers may have ushered in an era of unfettered global intrusions into our Internet infrastructure, and there will surely be a continuation of ISIS-sponsored terrorism in Europe and elsewhere.

Every year of this longstanding bull market, we have to look over our shoulders and wonder when and how it will end. With the January downturn and so much uncertainty at this time last year, nobody could have predicted double-digit returns on U.S. stocks at year-end. Next year could bring more of the same, or it could fulfill the dire predictions many have made during the election cycle, including both Democrats and Republicans who believe the country is in worse shape than the numbers would indicate.

What we have learned over the past few years is that the markets have a way of surprising us, and that trying to time the market, and get out in anticipation of a downturn, is a loser’s game. At the county fair, when we get on the roller coaster, we don’t bail out and jump over the side at some scary point on the track; we hang on for the ride. The history of the markets has been a general upward trend that benefits long-term investors, and looking out over the long-term, that—and a few hard bumps along the way–is probably the best outcome to expect.

Sources:

Wilshire index data: http://www.wilshire.com/Indexes/calculator/

Russell index data: http://www.russell.com/indexes/data/daily_total_returns_us.asp

S&P index data: http://www.standardandpoors.com/indices/sp-500/en/us/?indexId=spusa-500-usduf–p-us-l–

Nasdaq index data:

http://quotes.morningstar.com/indexquote/quote.html?t=COMP

http://www.nasdaq.com/markets/indices/nasdaq-total-returns.aspx

International indices: https://www.msci.com/end-of-day-data-search

Commodities index data: http://us.spindices.com/index-family/commodities/sp-gsci

Treasury market rates: http://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

Aggregate corporate bond rates:

https://index.barcap.com/Benchmark_Indices/Aggregate/Bond_Indices

Aggregate corporate bond rates: http://www.bloomberg.com/markets/rates-bonds/corporate-bonds/

Muni rates: https://indices.barcap.com/show?url=Benchmark_Indices/Aggregate/Bond_Indices

http://www.wsj.com/articles/chinas-stock-market-still-a-draw-after-tumultuous-year-1451303164

http://www.theworldin.com/article/10632/unsettling-year-markets

Federal Reserve Interest Rate Hike

![]() Was anybody surprised that the Federal Reserve Board decided to raise its benchmark interest rate last week?

Was anybody surprised that the Federal Reserve Board decided to raise its benchmark interest rate last week?

The U.S. economy is humming along, the stock market is booming and the unemployment rate has fallen faster than anybody expected. The incoming administration has promised lower taxes and a stimulatory $550 billion infrastructure investment. The question on the minds of most observers is: what were they waiting for?

The rate rise is extremely conservative: up 0.25%, to a range from 0.50% to 0.75% – which, as you can see from the chart, is just a blip compared to where the Fed had its rates ten years ago.

The bigger news is the announced intention to raise rates three times next year and to move rates to a “normal” 3% by the end of 2019—which is faster than some anticipated, although still somewhat conservative. Whether any of that will happen is unknown; after all, in December 2015, the Fed was telegraphing two and possibly three rate adjustments in 2016, before backing off until now.

The rise in rates is good news for those who believe that the Fed has intruded on normal market forces by suppressing interest rates much longer than could be considered prudent, and even better news for people who are bullish about the U.S. economy.

The Fed may have been the last remaining skeptic that the U.S. was out of the danger zone of falling back into recession; indeed, its announcement acknowledged the sustainable growth in economic activity and low unemployment as positive signs for the future.

However, bond investors might be less pleased, as higher bond rates mean that existing bonds lose value. The recent rise in bond rates at least hints that the long bull market in fixed-rate securities—that is, declining yields on bonds—may finally be over.

For stocks, the impact is more nuanced. Bonds and other interest-bearing securities compete with stocks in the sense that they offer stable—if historically lower—returns on your investment. As interest rates rise, the see-saw between whether you prefer stability or future growth tips a bit, and some stock investors move some of their investments into bonds, reducing demand for stocks and potentially lowering future returns.

None of that, alas, can be predicted in advance, and the fact that the Fed has finally admitted that the economy is capable of surviving higher rates should be good news for people who are investing in the companies that make up the economy.

The Bottom Line

There is no reason to change your investment plan as a result of a 0.25% change in a rate that the Fed charges banks when they borrow funds overnight. There is always too much uncertainty about the future to make accurate predictions, and today, with the incoming administration, the tax proposals, the fiscal stimulation, and the real and proposed shifts in interest rates, the uncertainty level may be higher than usual.