CAS News

Economic Update – Third Quarter 2013

Update! As of October 16, 2013, President Obama signed a bill to end the partial shutdown of the government and extend the debt ceiling until February 7, 2014. The information in this Quarterly Economic Update was based on the quarter ending September 30, 2013.

Review and Outlook

Wow! Talk about drama! Before we even get to the numbers, let’s look at the standoff between the Republicans and the White House that has resulted in the first government shutdown in 17 years. On October 1, 2013 congressional Republicans forced the shutdown with their demands to “defund” or delay the Affordable Care Act (ACA), otherwise known as “Obamacare”. At the time of this writing, Congress is still deadlocked.

Until some agreement can be reached, the shutdown has suspended all non-essential government functions. This means approximately 800,000 federal workers are at home with no pay. Another 1.3 million are still working but they will not be paid on time. The outcome is uncertain for a large number of government contractors. To give you a better idea of how this works, NASA is closed but the people supporting the astronauts currently on the International Space Station are still working. Lion-loving members of the public are currently shut out of the National Zoo, but zoo employees will continue to feed the lions!

If history is any guide, the duration of the government shutdown matters, according to Richard Salsman, chief market strategist at InnerMarket Forecasting. Shorter government shutdowns are usually not disruptive, but longer ones are bearish, he says. There have been 17 previous shutdowns since 1976, ranging from 1 day to 26, with an average of 6 days. The S&P 500 has fallen by a mean 0.8% in past shutdowns, but for those lasting 10 days or more, a decline happened 80% of the time and averaged 2.6%. One month after the longer shutdowns ended, stocks were still down slightly, compared with the 1.7% average rise after the shorter shutdowns ended. Remember that past performance is no guarantee of future results. (Source: Barron’s, October 8, 2013, Stocks Track Washington’s Ups and Downs)

If history is any guide, the duration of the government shutdown matters, according to Richard Salsman, chief market strategist at InnerMarket Forecasting. Shorter government shutdowns are usually not disruptive, but longer ones are bearish, he says. There have been 17 previous shutdowns since 1976, ranging from 1 day to 26, with an average of 6 days. The S&P 500 has fallen by a mean 0.8% in past shutdowns, but for those lasting 10 days or more, a decline happened 80% of the time and averaged 2.6%. One month after the longer shutdowns ended, stocks were still down slightly, compared with the 1.7% average rise after the shorter shutdowns ended. Remember that past performance is no guarantee of future results. (Source: Barron’s, October 8, 2013, Stocks Track Washington’s Ups and Downs)

Investors are trying to gauge what is going to happen next as the government remains shut. During the first week of the fourth quarter, the broad stock market fell and rebounded daily, if not hourly, as a result of conflicting comments from senior political leaders. “It was a manic-depressive market,” says Paul Nolte, a portfolio manager with Dearborn Partners. (Source: Barron’s, October 8, 2013, Stocks Track Washington’s Ups and Downs) The shutdown “doesn’t seem to be phasing the markets all that much,” said Brian Jacobson, chief portfolio strategist for Wells Fargo Funds Management LLC, because “we’ve seen this coming from a mile away.” (Source: WSJ, October 5, 2013)

Many investors have likely become desensitized by a series of last-minute budget deals in recent years, most of which were followed by stock gains. Still, there is significant uncertainty over the extent to which the shutdown could affect economic growth and market volatility.

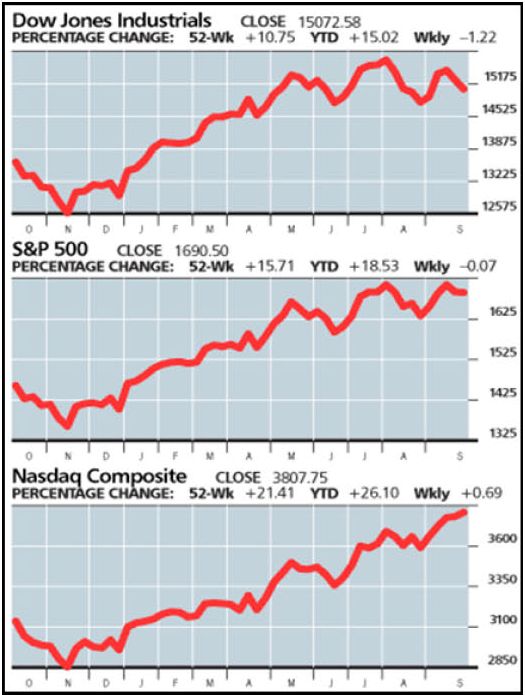

Even with all these concerns, major stock-market indexes continued their move into record territory in the third quarter. The S&P 500 gained 4.7% and headed into the fourth quarter up 18% for the year. The Dow Jones Industrial Average advanced 1.7% during the third quarter even as economic growth remained uneven. The Dow is up 14.9% for the first 9 months of 2013. The NASDAQ ended up 24.9% for the first 9 months and posted a 10.8% gain for the third quarter.

Debt Ceiling

As of October 17, 2013, the Treasury Secretary announced that the government will run out of cash and will be unable to pay its debts unless Congress first votes to raise the federal debt ceiling, which is the limit of how much money the federal government may legally borrow.

GOP leaders have stated they will agree to an increase of the debt ceiling only in exchange for a package of major budget changes, including; a delay of the health-care law, lower income tax rates, and adjustments to Medicare and Medicaid. While the White House has stated repeatedly it won’t negotiate any such agreement, many Republicans believe that this is their last chance to stop “Obamacare”, which includes big subsidies in entitlements. History suggests that such entitlements, once granted, are politically impossible to take away.

Rather than negotiate an end to the shutdown and a resolution to the debt ceiling issue, neither side has budged. The debt ceiling has been raised 74 times before. Raising it again should be routine—but what if no one backs down?

There have been warnings that a default by the U.S. government would be “catastrophic”—the government would soon begin falling behind on its bills, and this could potentially spark a financial crisis, including a stock market crash and a jump in interest rates.

America has never before found itself unable to meet its obligations. If the debt ceiling is breached, the government would have to rely solely on tax revenues, which currently cover only 84% of its expenditures. There is no question that the government would have to reduce some expenses, whether it is pensions or even interest on the National debt. However, since no politician wants to explain to grandma why her Social Security check stopped, odds are that none of this will happen—then again, looking at the mood in Congress, it’s hard to be optimistic. (Source: The Economist, October 5, 2013)

America’s government debt is considered a safe haven, which is why Uncle Sam can borrow so much so cheaply. America will not lose these advantages overnight, but an American default would cause unpredictable global repercussions. It is not just that America would have to pay more to borrow—it would threaten financial markets. Because American treasuries are very liquid and less risky, they are widely used as collateral. They make up more than 30% of the collateral that financial institutions such as investment banks use to borrow in the $2 trillion “tri-party repo” market, a source of overnight funding. A default could trigger demands by lenders for more or different collateral, which in turn could trigger a “financial heart attack” like the one caused by the Lehman Brothers collapse in 2008. (Source: The Economist, October 5, 2013)

World financial markets have already slipped on the frightening possibility that the U.S. could, in merely a few weeks, default on its debts in the absence of some agreement between the political parties. The Times of London called the “whole exercise irresponsible brinkmanship… when the world economy badly needs American leadership.” Far more worrying than these temporary effects, though, are the world’s broader doubts about American credibility and reliability. If our government can’t agree on a plan to keep the WashingtonMonument open, how can foreign powers count on the U.S. government to unite various efforts to accomplish much harder tasks internationally? Let’s face it: a superpower that can’t fund its government or pay its bills is not in a position to police problems worldwide.

The Congressional deadlock comes as our economy tries to gain traction more than four years after end of the Great Recession. Many consumers are slowly improving their personal finances. Some businesses are boosting hiring at a modest pace. The housing market is regaining lost ground and many stock indexes aren’t far off from their record highs. Many investors are more concerned with near-term decisions about the Federal Reserve’s bond-buying program than about news from Capitol Hill. In fact, confidence among U.S. consumers fell to a 5-month low this month according to a study by the University of Michigan released on Friday, September 27, 2013.

Sure, what’s happening in Washington is scary. With the government closed, the debt ceiling approaching, and an end to the standoff nowhere in sight, it’s hard to ignore the sense that a major collision is about to occur. However, as long as the default doesn’t occur, most problems will probably be short-lived.

In the meantime, the U.S. economy continues to move ahead, but at an extremely slow pace. After a recession there is supposed to be a recovery, but instead America has experienced its worst four consecutive growth years since the Bureau of Economic Analysis started compiling data in the 1930s. Recovery from the 2007-2009 Great Recession remains the slowest since World War II. Over the last three years we’ve averaged less than 2% annual growth, and in the first two quarters of 2013, the U.S. economy rose just 1.1% and 2.5%, respectively. The current GDP growth is estimated to continue at this mediocre 2.5% rate, with perhaps a slight increase in growth by mid-2014. (Source: Kiplinger’s Economic Outlook, October 2013)

Quantitative Easing

Quantitative Easing (QE) is the policy that Federal Reserve Chairman Ben Bernanke is using to promote economic recovery. Quantitative Easing has been implemented by the Fed’s $85 billion monthly bond buying (paid for with money the Fed creates out of thin air), which has kept interest rates artificially low and allowed the stock market to rally over the last 2 years. That’s an annualized rate of more than a trillion dollars. This is a breathtaking sum when you consider that the Great Recession, with its financial crisis, ended well over 4 years ago.

In May, Mr. Bernanke said that the Fed might change policies in the coming months by paring back or “tapering” its monthly bond purchases. Interest rates rose in response to his comment, which in turn caused the stock and bond markets to decrease significantly. Bernanke responded by stating that the economy is still weak, so federal policies will still be needed for a while and no changes will take place for the time being. This helped cap rising interest rates and helped halt the flight of capital from emerging markets.

Currently, the Fed does not have a fixed schedule for withdrawing QE or raising interest rates. It’s not likely the Fed will pull its support for the market before the current problems in Washington are resolved. (Source: Kiplinger’s Economic Outlook, October 10, 2013)

Inflation

Inflation is low by virtually every measure and has dropped below the Fed’s target of 2.0%. (Source: Bob Le’Clair’s Finance & Markets Letter, September 28, 2013) Although inflation appears to be tame at this time, this number does not include energy, food or healthcare costs.

Also keep in mind that although inflation hasn’t been much of a worry in recent years, even a modest amount will nibble away at your portfolio over time. Stocks don’t always beat inflation over short periods, especially when it’s caused by sudden spikes in oil or other commodity prices. But over the long haul, stocks are a powerful defense. Based on data going back to 1926, Morningstar’s Ibbotson unit reports that long-term bonds have historically returned only 2.6% annualized after inflation, compared to large-company stocks which have delivered close to 7%. (Source: Kiplinger’s Personal Finance, April 2013)

Unemployment

Thanks to the government shutdown, doors were closed doors at the Department of Labor, so the vital September employment report was not issued. However, the information we have through August shows that progress rebuilding labor markets is extremely slow and disappointing. (Source: Department of Labor)

The monthly job creation is averaging just 180,250, below the pace set in 2012 and well under the steady 200,000 a month that would signal a healthy economy. A total of about 2.1 million jobs will be created by year-end, which is little change from 2012. Prospects for next year don’t look much better, with an estimated net gain of about 2.25 million jobs over the course of the year and the unemployment rate of about 7.2% by year-end 2014. There are still about 2 million fewer jobs now than when the recession began in 2007. Including part-time workers looking for full-time work and people who have received the maximum unemployment benefit and dropped off, the records brings the unemployment numbers up to between 15-22%.

Price/Earnings Ratio

Price/Earnings Ratio

Stocks moved further into record territory in the third quarter before giving up some of their gains. The Fed’s pledge to keep current interest rates low indefinitely caused money to keep flowing out of low-yielding less risky investments such as government bonds and bank accounts and into alternatives such as the stock market. However, the bull market’s momentum has slowed lately, as rising valuations have prompted more investors to start selling some of their portfolio and rebalancing their current holdings.

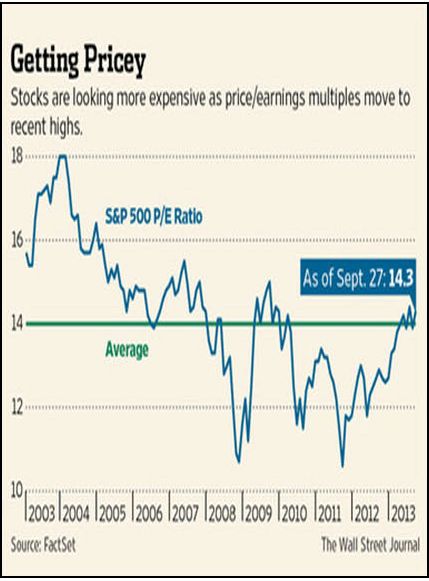

Stocks have gotten pricier in recent months. The S&P 500 is trading at a price/earnings ratio of 14.3 times the next 12 months’ worth of earnings, which is above the average of 12.9 for the past 5 years and 14.0 for the past 10 years, according to FactSet. Many economists say the slow pace of corporate earnings growth has been inflated by stock buybacks, which has the effect of lifting earnings-per-share readings even when underlying sales growth remains soft. While some economists see stocks moving into dangerous territory, others predict we are still part of a bull market that still has legs.

According to many economists, with the uncertainty surrounding interest rates, bonds are now riskier than stocks. The values in stocks are currently better. As bond yields rise, bond prices fall. For example, consider that a 1-percentage point rise in interest rates will cause a 30-year Treasury bond to fall by 17%. For now, bond holders can expect to earn whatever they collect in interest, with little or no price appreciation—which means returns in the low single digits. That compares with a likelihood of high single digits (and possibly more) from stocks. For income investors, dividend-paying stocks are an enticing alternative to bonds—the 2.2% average yield on the S&P 500 stocks is about the same as the current yield on 10-year Treasuries. Many high quality companies are offering dividend yields well above the yields of their own bonds. In addition, although there are no guarantees, the appreciation potential on stocks is still greater over the long run if it is a good quality company.

Bonds are still a vital part of a diversified portfolio. During a period of rising interest rates, instead of avoiding bonds entirely, a more thoughtful strategy would be to adjust your exposure to bonds based upon their actual duration.

International Markets

Global trade and investment push more than $50 trillion annually to the world’s financial markets—a figure that more than triples the size of the U.S. economy. This figure exceeds even the annual trading volume in U.S. government securities, the largest and most active market in the world. The stalemate in Washington has caused global stock markets to slide, although many traders stress that conditions across financial markets remain calm. The third quarter was actually a good one for European stock markets, with the STOXX Europe gaining 8.9% compared to only 4.7% for the S&P 500. Despite investors’ general skepticism about Europe, Bob Baur, Chief global economist at Principal Global Investors, says he has been taking advantage of the market’s recent weakness to buy stocks that should perform well in the strengthening economy. (Source: Forbes, October 7, 2013)

Unfortunately, there was a major upset in the global markets that began with China’s decision to promote its exports by keeping the value of its currency, the Yuan, cheap to the dollar. When Chinese goods are cheap in global markets, foreigners buy them and create a huge demand for the Yuan. Despite the financial debt crisis in Europe and the turmoil in U.S. markets over the past few years, China’s economy has continued to register strong growth, with an annual growth rate of 10%. It is now the second largest economy in the world and China is the world’s largest exporter and second-largest importer. These transactions have averaged a staggering $800 billion per year during the last 10 years and increased China’s official U.S. dollar holdings at an annual rate of 31%. Beijing currently has amassed a reserve of more than $3 trillion. (Source: World Economic Database. International Monetary Fund website, reference 2011)

Other export-oriented emerging countries have also followed variations of this policy by keeping their currencies cheap against the dollar and amassing large reserves. Changes within these countries regarding their financial decisions are often the cause of the global economic upset, which we experience on a regular basis. The problem is that these excess savings have interfered with the normal flow of the boom-bust cycles, and therefore fostered above-average global volatility due to the size and independent nature of the liquidity flows.

Many economies, especially the emerging markets, are concerned about the U.S. Federal Reserve. If the Fed scales back stimulus efforts, it could be harder for these countries to obtain the dollars they need. However, if current trends continue, these emerging economies could rival the U.S., and China may soon overtake us. The International Monetary Fund (IMF) projects that in 3 years America’s share of world GDP could fall to 17.7%, less than China’s share. (Source: The Misrule of Law in America)

“Obamacare”

“Obamacare” is the most ambitious shake-up of America’s health care system since the 1960s. There are an estimated 55 million, or 1 in 7, people in the United States without health insurance. Starting January 1, 2014, these people will be required to buy insurance or pay a fine. Those who cannot afford it will receive subsidies; part of a big expansion of coverage to the sick and the poor.

The success or failure of this program in the coming months will be influenced by people signing up for health care exchanges, the types of plans they select, and their actual health experience. Democrats believe “Obamacare” can move the country toward universal coverage while keeping costs down. However, Republicans argue that you cannot extend health insurance coverage to 55 million additional people while simultaneously improving the quality of care and lowering costs. They view it as unaffordable, socialized medicine.

One of the biggest problems with America’s system is that insurers have long charged extremely high rates to the sick, or refused to cover them at all in many circumstances. Starting in January, this practice will be banned. Since insurers would soon go bankrupt if they sold only cheap plans to sick patients needing expensive treatment, “Obamacare” pushes the young and fit to buy insurance, too. This will give insurers revenue from cheap, healthy patients to offset the cost of insuring sick ones.

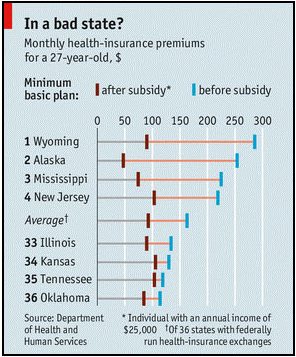

The cost of insurance will vary significantly and requires insurers to cover a minimum set of services. In most states, the simplest plans will become more comprehensive. Because there are many variables, “Obamacare” will have dramatically different effects from place to place and person to person. The law will raise health costs for some and lower them for others. For example, a 27 year old will pay $130 a month for a basic plan in Kansas, compared with $286 in Wyoming (see chart.) (Source: The Economist, October 5, 2013)

The cost of insurance will vary significantly and requires insurers to cover a minimum set of services. In most states, the simplest plans will become more comprehensive. Because there are many variables, “Obamacare” will have dramatically different effects from place to place and person to person. The law will raise health costs for some and lower them for others. For example, a 27 year old will pay $130 a month for a basic plan in Kansas, compared with $286 in Wyoming (see chart.) (Source: The Economist, October 5, 2013)

Overhauling America’s $2.7 trillion health sector is no easy task. America spends 18% of GDP on healthcare. The people of Britain, Norway, and Sweden, to name a few, spend half as much but actually live longer. Health spending is growing faster than wages, and is set to hit 20% of GDP by 2022, according to the Congressional Budget Office (CBO). The CBO states health costs remain the biggest long-term threat to America’s finances.

Public support is fragile—only 39% of Americans support “Obamacare”, while 51% disapprove, according to a recent poll by the New York Times and CBS. However, 56% would rather try to make the law work than stop it by stripping it of cash. Whether we eventually judge “Obamacare” a success or a catastrophe, only time will tell.

Conclusion

The 5 words going through every investor’s mind at this point: “What should I do now?”

The daily economic headlines are depressing and there is widespread fear that the combination of an aging population and pressures to embrace fiscal growth will weigh heavily on the economy. However, these fears tend to overshadow how much progress households are making in restoring their balance sheets. For example, balances on credit cards in the second quarter of 2012 were 22.4% below their peak in the fourth quarter of 2008, according to the Federal Reserve Bank of New York. That means Americans are saving again. The personal savings rate is now 4.2%, well above the low of 1% reached in April 2005.

Widespread fear of the consequences of the shutdown and the debt-ceiling debate may drive many investors to dump stocks and other risky assets, as they did during the last debt ceiling standoff in August 2011. You may want to buckle your seatbelt. However, now is not the time to completely overhaul your strategy, “It’s folly to try and Washington-proof your portfolio,” said Doug Cote, chief investment strategist at ING U.S. Investment Management. “This kind of thing can turn on a dime and the market can go up a lot faster than it goes down. So if you sell now, you’re just locking in losses.”(Source: Investment News, October 7, 2013)

As an investor, you can stay up all night worrying about what could happen, or you can simply focus on managing your portfolio for the long term. Make sure you have a well-diversified portfolio that can weather the corrective periods of the stock market cycle. Long term, stocks will usually reward investors for putting up with the short-term worries.

Remember the old rule of thumb, “Never waste a crisis!” Your investing behavior and choices can actually have a greater effect on your overall rate of return than the performance of your investments. History shows us that investors lose far more money as a result of their actions than markets lose for them.

P.S. Look in the mirror. History shows us that investors lose far more money as a result of their own actions than markets lose for them.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

Indexes cannot be invested in directly, are unmanaged and do not incur management fees, costs or expenses. No investment strategy, such as asset allocation and rebalancing, can guarantee a profit or protect against loss in periods of declining values.

In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. The investor should note that investments in lower-rated debt securities (commonly referred to as junk bonds) involve additional risks because of the lower credit quality of the securities in the portfolio. The investor should be aware of the possible higher level of volatility, and increased risk of default.

The payment of dividends is not guaranteed. Companies may reduce or eliminate the payment of dividends at any given time.

International investing involves special risks including greater economic and political instability, as well as currency fluctuation risks, which may be even greater in emerging markets.

The price of commodities is subject to substantial price fluctuations of short periods of time and may be affected by unpredictable international monetary and political policies. The market for commodities is widely unregulated and concentrated investing may lead to higher price volatility.

Sources: Wall Street Journal (9/30/13, 10/5/13, 10/9/13), Barron’s (10/8/13), Kiplinger’s Economic Outlook (10/10/13), Bob LeClair’s Finance (9/28/13), The Economist (10/5/13), Investment News (10/7/13)

Contents Provided by MDP, Inc. Copyright 2013 MDP Inc.

Community Event: “Aging in Place – Naples Style” Program for the Public

The NCH Healthcare System’s Brookdale Center for Healthy Aging & Rehabilitation, Collier Building Industry Association, University of South Florida – College of Engineering, as well as individual experts are hosting a free community education program called “Aging in Place – Naples Style” on Tuesday, November 5, 2013, 3:00 pm – 5:00 pm, in the Telford Auditorium, NCH Downtown Naples Hospital.

“Aging in Place” refers to continuing to live in one’s preferred home and using existing expertise, services and technologies to enjoy life to the fullest extent possible through all stages of life. This event will include a presentation on “Aging in Place” concepts followed by an “Ask the Experts” panel discussion. Helpful materials will be available for all attendees. For more information and to register for this free event, please call the Brookdale Center at 239-552-7575.

“People facing a debilitating health condition often retreat from their favorite activities because of the stigmas associated with these conditions and a change in their sense of self,” says Heather Baker, administrative director of The Brookdale Center for Healthy Aging & Rehabilitation. “Aging In Place – Naples Style” is an example of community collaboration at its best. Our goal is to promote awareness in our community to help individuals avoid these unnecessary compromises in lifestyle,” Baker adds.

The inspiration for “Aging in Place – Naples Style” comes from a local resident who faced challenges as she brought her husband home from the hospital. The family had recently renovated their home without the benefit of expert advice that could have made their home more accessible in light of the new physical challenges they face in the years ahead.

Here on the Paradise Coast, when some think of planning ahead it conjures up thoughts of meeting with financial planners, watching the hurricane forecasts, and making health care choices. Individuals form a generalized plan for the “what ifs” they may face. However, there’s a difference between surviving life’s challenges and taking steps toward sustaining a fully engaged lifestyle. This program is designed to support a satisfying, active lifestyle.

For more information, click on the flyer below…

Listed entities are not affiliated with FSC Securities Corporation.

Patience is the key to sane and successful investing

Kim Ciccarelli Kantor | Naples Daily News | October 10, 2013

Markets all over the world are interrelated and the striking resemblance of good times and bad times has in recent times become more apparent.

Confidence in investing, when markets have turned sour, is often a challenging task. Keeping a straight head and having staying power is even more difficult. Patience is a promising word in an uncertain time for investors. “Patience” is something we must learn.

Consider your reaction to fluctuating and declining stock prices.

Are you a committed long-term equity investor? If not, and you are invested in equities, then it’s time to learn just how to become committed.

If you cannot accomplish this goal, then your reactions to temporary market declines will precipitate in insane actions. You may inadvertently lock in your losses forever.

Stock market corrections are in inevitable part of investing. This, of course, does not make them any more pleasant an experience.

When any crisis or tragedy hits, you must keep a straight head.

This same advice applies to the market. Adhere to the most obvious advice from experts. Don’t run too briskly in any direction during pronounced volatility.

If you feel panicky, take a deep breath, take a walk, listen to music, pray or talk with your financial advisor.

Do not let short-term volatility deter you from staying on course with your long-term objectives.

Develop staying power. This is especially important for retirees who take cash flow from their portfolios. Review your income needs and expenditures.

Are you withdrawing too much from your portfolios, and if so, what adjustments would make sense? Study options for alternate sources of cash flow. Plan ahead 9 – 12 months and be sure you are either holding some liquid cash reserves or have immediate access to obtain them.

Review tax-planning techniques. Perhaps there are tax advantages that can reward you and help leverage the value of your portfolio.

If you are living on dividends, your income stream may not be immediately affected; however, if you depend on the sale of equity shares, be careful.

Provided you hold your share count constant, you have the ability to earn back your principal. Should you start liquidating stock shares at an advanced rate in a declining market, your income may be affected dramatically over the long term.

The patience of investors has been repeatedly tested over the last year in most global markets. To live with varying markets decline, several rules must be followed:

1. Keep a straight head.

2. Develop staying power.

3. Smart money remains invested.

4. Focus on long-term goals.

5. Maintain a diversified portfolio.

6. Invest regularly in both bear and bull markets.

7. Consider tax opportunities.

8. Talk with your financial advisor.

What a wonderful world we live in and what a great opportunity we have to be shareholders of some of the best companies in the world.

The long-term fundamentals of a good business will ultimately reward its investors. Think sanely and make sound decisions, especially in difficult times for markets or you personally. Remember, these too shall pass.

Kim Ciccarelli Kantor, CFP® CAP™ is president and founder of Ciccarelli Advisory Services Inc., a Family Focused Wealth Management Firm in Florida and New York.

Interest Rates Are Trending Up. So What?

If you haven’t already, you will soon be hearing alarming reports of the “dramatic rise of Treasury bond rates,” and the breathless implication in the articles and on the financial cable programs will be that this will have a disastrous effect on bond owners and the economy in general. Higher interest rates! More inflation! Lower economic growth! More interest on the ballooning federal debt! More competition for the stock market, and therefore lower stock prices!

Chart 1: Detail from a one-year tracking of 10-year Treasury Bond rates, showing what some have called an unprecedented rate rise.

If you look at the recent rise in 10-year Treasury rates in isolation, as several commentators have done (see Chart 1), it does indeed look remarkable: a rise of more than 70% from a May 2nd low of 1.63% to somewhere in the neighborhood of 2.90% as you read this. If the Dow were to jump that far, that fast, it would have risen from 14,500 to more than 25,500. Yikes! Maybe the headlines are justified after all!

But if you put the recent rate rise into a longer-term perspective (see Chart 2), the recent “dramatic rise” looks awfully puny compared with some of the long-term swings in market history, and the current rate still looks quite reasonable. The high percentage shift is more a reflection of how low rates had gotten than a rise to dramatic heights.

So what’s really going on here? You probably know why bond investors are asking for an extra 1.3% a year out of their longer-term fixed income investments these days: nobody knows when the Federal Reserve Board is going to stop buying Treasuries, or what, exactly, will happen when the elephant jumps off of the see-saw. The Fed’s most recent meeting minutes suggest that it will be cautious about winding down its QE bond buying program. And you can bet that Fed economists will be watching the market for signs of impending damage, and curtail their curtailment if they seem to be causing a ruckus. But that still leaves a bit of uncertainty about where rates will go.

Chart 2: The bigger picture: 10-year Treasury yields since the later 1800s. Note that the “unprecedented rise” is the little upward squiggle on the right-hand side.

All professional investors know for sure is that when a big buyer walks away from the marketplace, gradually or not, there will be less demand for whatever they were buying than there was before. Therefore bond issuers–including the U.S.–will have to pay more (i.e., higher yields) to lure in the fewer remaining buyers.

How much more? In other words, how much higher will bond rates go? How much will the bonds you own today lose value during the messy pullback from QE stimuli? We can make this second question easier to answer by simply pulling money back away from longer-term bonds until the dust settles, leaving it to the experts and institutional buyers to make educated guesses and read the tea leaves.

But you have to answer the first question in order to know the answer to the obvious third one: what other consequences will rising bond rates have on your other investments?

When market forces get back in control of the bond markets, they will be responding to three things: how scary are the alternative investments (and therefore how much do I want to put in bonds)? What is the current and expected inflation rate? And finally: where do I want to be on the yield curve? (Are the longer-term rates attractive enough to lure you away from the relative safety of shorter-duration bonds?)

Right now, inflation is pretty low, in part because the high joblessness rate is making it harder for workers to ask for huge raises, in part because the banks have a lot of money to lend and not a lot of people asking to borrow it. A recent report notes that an astonishing 82% of the U.S. money supply is currently on deposit at the Fed, mostly in accounts held by large banks. (To put that in perspective, the average percentage from January 1959 through the end of 2007 was 6.18%.) By the laws of supply and demand, banks don’t have a lot of leverage to demand high rates of interest.

If you believe that the unemployment markets are going to tighten up dramatically in the fairly near future, and that somehow millions of people will want to borrow most of the global supply of dollars, then you can project a high inflation rate. If not, then you should probably not worry about an explosion in the inflation rate for the foreseeable future.

When you’re talking about alternatives to bond investments, you’re mostly talking about stocks. If we see another Fall of 2008 scenario, people are going to flock to government bonds and drive rates higher. But the only thing we know about the Fed’s decision-making process, from its notes and internal policy debates, is that it is only going to start exiting its QE program when it thinks the economy is healthy. If the stock market starts to look edgy, or the U.S. starts sliding back into recession, you can bet that the Fed will want to keep interest rates low and be a tad more gradual about ending its QE activity.

As to the yield curve, at the moment, short-term rates on Treasuries and most other fixed-income vehicles are about as close to zero as you will ever see them again. The Fed has announced that its policy rate is 0%, and until the economy gets fully back on its feet and unemployment comes down dramatically, this is likely to continue to be its policy rate. The spread between 3-month T-bills and 10-year Treasuries is currently about 2.8%, which is nearly twice as high as the 1.5% historical average. Can it go higher? Yes. On two occasions since January of 1970, the spread has reached as high as 4%.

If you add up all these clues, you come out with something very different from the disaster scenarios you’ll be hearing in the news. The Fed is planning to stop buying Treasuries at some point in the future, and let market forces take over–but only when it feels like the economy is healthy, and only so long as it can do this without harming economic growth or hammering the stock market. The market forces themselves are unknown, but it’s hard to see how the ten-year Treasury bond will rise above 4%–or, to put that number in perspective, to the point where it is yielding about twice the dividend yield in the overall S&P 500 index. That still looks like pretty weak competition for stocks.

So what we’re seeing in the bond market appears, if you can get away from the breathless headlines, to be nothing catastrophic. Bond investors are demanding an extra 1.3% a year to compensate for all the uncertainty they face as they commit their money for the next ten years. They may well ask for a bit more in the future. Can you blame them?

Sources:

http://seekingalpha.com/article/1657072-how-high-are-yields-likely-to-rise?source=google_news

http://bigcharts.marketwatch.com/quickchart/quickchart.asp?symb=10_YEAR&insttype=Bond

http://www.minyanville.com/trading-and-investing/fixed-income/articles/What-if-the-10-Year-Treasury/8/26/2013/id/51458

In general, the bond market is volatile as prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Past performance is no guarantee of future results.

Six Steps for Successful Investing

Kim Ciccarelli Kantor | Naples Daily News | September 18, 2013

Investing is not only about money. It is mostly about a frame of mind that gives you the focus you need to be a successful investor.

A task often mistaken for success is the selection of a particular stock, rather than the fact that you choose to buy stocks. Successful investing requires a disciplined approach to decision making. It’s about proper planning and sticking to that plan.

The right mindset, combined with the appropriate knowledge, can help enable you to become a successful investor. Follow these six basic steps to help you on your road.

First, define your objectives. Your primary financial goal will lend a hand in shaping your portfolio.

Second, design your asset allocation, with the first task in portfolio construction to determine your risk tolerance levels. Asset classes such as stocks, bonds, cash, real estate and foreign investments are not equal in volatility and performance.

Third, evaluate your need to diversify. Be diversified in your portfolio selections in accordance with your tolerance for risk and volatility. Over-weighting in any one area can add more volatility to your portfolio and may not reward you accordingly. A diversified portfolio should, at the very least, carry weightings in large cap growth and value stocks, small/mid cap growth and value stocks, fixed equivalents and foreign investments.

Fourth, take time for review. Success in reaching your objectives may depend on how much time you spend in honest evaluation. Answer questions that describe your objectives. Are you seeking preservation of principal and a moderate amount of current income? Do you need income, or do you want growth?

Five years from now, what do you expect your standard of living to be – the same, somewhat better, or substantially better than now? Do you envision your investment portfolio to be worth the same or a little more than it is today, moderately greater than it is today, or substantially better? Be honest with your answers. This self-reflection is really important.

Fifth, decide what to do with the income generated by your investments. The choices might include receiving all the income, receiving some and reinvesting some, or reinvesting it all because a need for current income does not exist. How do you feel about the long-term prospects for the economy? Are you pessimistic, unsure, somewhat optimistic or very optimistic? Certainly, your view impacts the direction you set for future investing.

Sixth, be realistic when setting a time frame for achieving your goals. Do you need your portfolio within 5 years, 10 years, 15 years, or beyond? A common failing is not matching investment selections with the proper time horizon. For example, placing assets needed within three years into stocks could backfire if the economy is not robust during that time.

Do you have the right mindset for investing? If your portfolio value suddenly declined by 15% (or by 50%) would you: Be very concerned because you cannot accept a fluctuating portfolio? Be unconcerned if income you were receiving was unaffected? Be wary, but know that you are invested for the long term? Or, would you be unconcerned because it’s part of long-term investing?

A proper mindset, combined with a disciplined approach in portfolio design, will greatly enhance your opportunities for becoming and remaining a successful investor.

How to Avoid Identity Theft and Other Scams

By Lauren Tara LaCapra, Copyright © 2013 Horsesmouth, LLC.

Identity fraud and other scams are not quite as common and usually not as damaging as purveyors of scam-prevention software and services make them out to be. However, they still exist and have the potential to seriously hurt a consumer’s finances and credit score.

About 30.2 million adults—or 13.5% of the adult population—report falling victim to fraud each year, according to the most recent Federal Trade Commission data.

Scammers have a few key tactics and targets. They often prey on the elderly, vulnerable, and naive. They can present themselves as “official” bank or government representatives in a convincing way. They pull at heart strings with pleas for aid to help victims of natural disasters or war. They guarantee profits from a too-good-to-be-true money-making scheme.

“Con artists are the only criminals that we call artists,” says Steve Weisman, a lawyer and author. “They can appeal to our impulses and psychological make-ups.”

Smart, skeptical consumers can largely isolate themselves from fraud and identity theft by watching out for certain signals and ignoring the fake pitches for help or money-making schemes. Here are some common schemes that victims are falling prey to today:

WEIGHT-LOSS SCAMS

Don’t buy bogus weight-loss products that promise to burn fat without effort.

Americans spend about $30 billion each year on weight-loss products and services, according to the Food and Drug Administration. Many fall victim to claims that a miracle pill or potion can help them “melt off 10 pounds in seven days” or “shed the fat without the diet!”

Those products are a huge waste of money and won’t work as advertised. More people—about 4.8 million—were victims of fraudulent weight-loss products than any of the other frauds covered by the FTC survey.

“Any claims that you can lose weight effortlessly are false,” states the FDA’s website. “The only proven way to lose weight is either to reduce the number of calories you eat or to increase the number of calories you burn off through exercise.”

FOREIGN LOTTERIES

Another prevalent scam involves e-mail messages advising consumers that they have won a foreign lottery and requesting account information to deposit the reward.

“It’s hard enough to win a lottery when you do enter it, much less one you never entered,” says Weisman.

Fraudulent foreign lottery offers tied with buyers’ club memberships are at second place for the top scams in the FTC survey, with about 3.2 million people getting duped by each type of scheme.

Never give your personal information to anyone claiming that you have won a prize. If you’re afraid of losing out on the reward, tell them to send you a check.

“OFFICIAL” EMAILS FROM BANKS OR THE GOVERNMENT

Weisman notes that crooks have also gotten better at making e-mails look “official” when they pose as representatives from the government, banks, or other institutions.

For instance, after tax day, lots of messages are sent out by impostors who request personal information, claiming to be from the Internal Revenue Service. The e-mails can appear to have official letterheads, emblems, and signatures, but they are simply fraudulent mock-ups. Thieves also target older victims by pretending to be representatives from the Social Security Administration.

Any e-mail, phone message, or mailing that requests account information should be independently verified by calling the bank or agency directly. Be sure to scout out the outlet’s contact information separately—don’t just call a phone number presented by the potential thief.

CURRENT EVENTS

Scammers will look for any opportunity to take advantage of “whatever the event of the moment is,” says Weisman. That includes scamming disaster victims by pretending to be FEMA workers, insurance adjusters, or contractors, or scamming generous donors by posing as charity representatives.

Others present themselves as Red Cross workers to military families and say a relative has been injured in Iraq and is being airlifted to Germany for treatment. The con artist then asks for additional information about the relative serving in the military—like their date of birth or Social Security number—as well as a donation to the Red Cross to help cover the cost of the airlift and medical care.

There are still others who claim to have technology to improve gasoline efficiency. They peddle the fake products to consumers struggling with high gas prices and convince others to invest in their company—and then take off with the cash.

Those suffering from mortgage woes must also be wary, since many scammers are taking advantage of the subprime crisis by claiming to have a quick fix or cheap solution. Instead, the thief charges processing fees without helping the borrower or convinces the borrower to sign over a home or open a home-equity loan, Weisman says.

“When someone is behind on their mortgage and is going to lose their house, and someone comes up to them and says, ‘I can help you out with your troubles,’ they want to believe,” he adds. “It’s the old ‘desperate times call for desperate measures.'”

Be wary of those claiming to be representatives of charities or who offer a quick fix for a complicated situation. Donate directly through a trusted method instead of someone who contacts you via phone or e-mail. If a product— like the gasoline device or mortgage solution—seems too good to be true, it probably is.

————————————————–

Copyright © 2013 Horsesmouth, LLC. All Rights Reserved.

For the exclusive use of Horsesmouth Member: Carol Girvin

IMPORTANT NOTICE This material is provided exclusively for use by Horsesmouth members and is subject to Horsesmouth Terms & Conditions and applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties express or implied are hereby excluded.

Protect Yourself and Your Family From Online Hackers

Here are some steps and precautions you can take to protect yourself and your family from online hackers:

- Change your passwords from time to time. Don’t post anything on a social network you may use as a password: your birth date, pet’s name, mother’s maiden name or your school. Identity thieves can use the information you post to guess your password.

- Do not email your credit card number to anyone. There are many phishing scams using Sony’s name now, but Sony, or any other company, will not contact you and ask for your Social Security number, credit card number or other personal information. Be cautious about opening any attachment or downloading any files from email you get, regardless of what company sent them. You can forward phishing emails to spam@uce.gov.

- Monitor debt and credit cards for suspicious purchases at least weekly. If you feel your card information was stolen, consider canceling your linked card. Be persistent with watching your accounts; it may be months or even a year before thieves actually use your card.

- Check your credit reports. You can get one free credit report every year from each of the three credit bureaus online or by calling (877) 322-8228. Stagger these reviews throughout the year in order to catch anything that isn’t correct in your account.

- Protect your wireless router. If you use a wireless router, password protect it and enable the encryption to scramble the data you send online.

- Use your credit card instead of debit card. Credit cards offer stronger fraud and identity theft protections.

- Send out the word if you are worried. If you feel your information has been compromised, place a fraud alert at the three major credit bureaus. Call Experian at 888-397-3742; Equifax at 800-525-6285; and TransUnion at 800-680-7289. Put a security freeze on your files.

- Don’t assume you’re as safe as you can be. Ask your bank if it has free software to protect your bank account. Some offer special protections for their online banking customers.

- Contact the FTC. If your information has been stolen, file a complaint with the Federal Trade Commission. The information is used to create a picture of wrongdoing. Unfortunately, the FTC won’t get your money back.

Child Identity Fraud – Ways to Stay Safe

Child identity fraud can be particularly prevalent during back-to-school season, but there are ways to stay safe.

Child identity theft is a growing problem in the U.S., with one in 40 households with kids under the age of 18 having been victimized, according to the Identity Theft Assistance Center. The fraudsters use a child’s personal data to get a new identity so they can get a job, government benefits, medical care, auto loans, and mortgages, the center says.

Child identity fraud can be particularly prevalent during back-to-school season, given the rise of sign-up forms, school registration, and dorm move-ins.

How can parents fight back?

The I.D. theft fraud prevention firm IdentityTheft911 offers the following tips for parents:

Don’t give up Social Security data unless you have to. IDTheft911 says some schools, especially day care centers and preschools, will ask for your child’s Social Security number. Don’t give it up so easily. Offer a birth date but explain you’re reluctant to share the Social Security numbers. Chances are they’ll go along.

Be careful at sporting events. Most parents have signed their kids up for soccer or baseball without really knowing who’s seeing that information. As IdentityTheft 911 says, some local athletic organizations are great at protecting that data—others are not. If in doubt, simply write in “contact me at [phone number] for information” before you release data, especially Social Security numbers and medical identity numbers. Once an organizer contacts you directly, ask them how they protect data from I.D. thieves, and give only what you have to. And never give out Social Security or medical I.D. numbers.

Watch for college-student scams. IdentityTheft911 says college students are a particularly attractive target to fraud artists. College kids are out in the real world, often without a healthy fear of real-world threats such as identity fraud. Make sure your college-aged son or daughter knows not to share sensitive data, and equip their computers, tablets, and smartphones with I.D. theft protection software to guard their personal identities.

Know what’s at risk—and protect it. The Identity Theft Assistance Center advises keeping all documents that show a child’s personal information under lock and key. At the very least, that information includes a child’s date of birth, Social Security number, and birth certificate.

Be aware that August and September are prime times for child identity theft. A lot of money and information is changing hands right now in preparation for the classroom, so keeping close tabs on both is the surest way to protect your family.

————————————————————

Copyright@213 Horsesmouth,LLC All rights reserved

For the exclusive use of Horsesmouth Member, Carol Girvin

This material is provided exclusively for use by Horsesmouth members and is subject to Horsesmouth Terms & Conditions and applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties express or implied are hereby excluded.

Factors to Consider When Updating Insurance Coverage

By Amy E. Buttell and Elaine Floyd, CFP®, Copyright © 2013 Horsesmouth, LLC.

With health care reform implementation getting closer and the memory of super storms still fresh, now is a good time to review insurance policies coverage, insurance needs, and emergency plans.

Insurance coverage tends to be the stepchild of family financial planning. All too often, insurance is obtained and then put on autopilot, only to be found inadequate when a disaster or problem strikes. That’s why it makes sense to take time every year to review insurance coverage, consider situations when new coverage may be required, and look at the implication of disaster planning on insurance coverage. Here are the types of coverage and issues to consider in any review of personal insurance policies:

HEALTH INSURANCE

Health care reform is changing the landscape of health insurance, removing previous barriers to gaining coverage, extending coverage to children up to the age of 26, and closing the doughnut hole for senior citizen prescription drug spending. With that in mind, here are some points for individual and family health insurance coverage that should be reviewed:

Medical deductibles and limits. For employees and senior citizens, open enrollment season provides an opportunity to review current policies and potentially change providers. When reviewing coverage or deciding whether to change to a new plan, take a look at deductibles, co-pays, and overall out-of-pocket expenses.

More employers are switching to high-deductible health insurance plans, where deductibles start at $1,250. Once the deductible is met, there are usually co-pays for doctor’s appointments, prescriptions, and other medical treatment. The overall out-of-pocket expense limit reveals the most you’ll have to spend in overall out-of-pocket costs. Also consider out-of-network costs in case you or a family member are traveling and require care out of town or a specialist needs to be consulted who is out of network.

What type of policy to choose depends on many factors, such as the overall health of family members, how often doctor’s visits and medications are needed, and the family budget.

Prescription coverage. Most plans provide for cheaper options that can save money, such as generic drugs, discounts, or prescription-by-mail availability.

HOMEOWNERS’ INSURANCE

Hurricanes and super storms are important reminders that home insurance coverage should be regularly reviewed and coverage increased in certain situations.

Homeowners’ inventory. It’s all too easy to buy jewelry, home office equipment, collectibles, and even upgrade a home through a renovation project without considering upgrading a homeowners’ insurance policy. Make a list of any significant renovations, new jewelry, home office equipment, collectibles, or other assets and review them with your insurance agent. Take up-to-date photographs or videos of all major belongings in the home and keep those pictures or videos in a safe place. Archive those photos or videos remotely via online storage.

Home replacement coverage. With home values down versus mortgages in many parts of the country, obtaining competitively priced “guaranteed replacement” or “replacement” coverage is critical. Call several insurers or insurance agents to obtain estimates on this type of coverage, and incorporate whatever change makes sense into your current or new coverage as soon as possible.

Flood and earthquake insurance options. Review the need for this coverage, because it’s not a part of standard homeowners’ policies.

Hurricane and windstorm coverage. This coverage varies by state and sometimes by county. Some states offer windstorm coverage pools for people who can’t get private insurance. Most states have high-risk pools or participate in federal programs that offer this type of coverage in coastal areas, so check with an insurance agent or state insurance department to make sure you have the latest coverage options and information.

Disaster planning. This isn’t a specific insurance issue, but it’s vital just the same. Create a document in a binder, folder, or online that includes all the information that loved ones would need in case of your death–keep a physical form of this information close to the items to grab in a crisis. It is vital that in case of a catastrophic event like a sudden death that loved ones have a single go-to guide with insurance, home, and estate information. It also makes sense to make a second copy for relatives.

UMBRELLA LIABILITY

Because it can be impossible to predict how much risk or liability certain situations may create – a bad car crash that a member of your family was responsible for or a fall on your property – many insurance agents recommend buying an umbrella liability policy.

Supplement to home and auto coverage. This type of policy provides coverage over and above a homeowners’ or car insurance policy in the event of a lawsuit. That way, if an unexpected event does occur that results in a lawsuit, legal and any settlement costs will be mostly covered by insurance.

DISABILITY INSURANCE

Many employers provide disability insurance, but that coverage may not be sufficient to truly cover earnings lost if a disability strikes.

Coverage specifics. Check any employer policy for specific coverage items like when it goes into effect, what kind of disabilities are covered, how much income replacement is offered, and how long it lasts. Many policies only replace 50% to 60% of income; a supplemental individual policy may be the way to increase that. Consider long-term and short-term coverage.

CAR INSURANCE

In a similar fashion to homeowners’ insurance, it is easy to set and forget car insurance deductibles and coverage. Reviewing and updating coverage can insure coverage when an accident or disaster occurs or save money if coverage previously required is no longer needed.

Specific issues. Higher deductibles can save money on the premium, but require higher out-of-pocket costs in the event of an accident or disaster, so weigh those variables out. If a disaster strikes, most comprehensive auto coverage will cover wind, flood, or earthquake damage. In the case of an older car that is paid for, skipping on collision insurance can be a real saver in terms of monthly premiums, but will mean no insurance payment if the car is in a collision.

SMALL BUSINESS INSURANCE

Small businesses face many risks, so if you’re a small-business owner, it makes sense to review and update your coverage frequently.

Specific issues. Coverage your business may need could include general and professional liability insurance, commercial property insurance and home-based business insurance. Business interruption insurance is another type of coverage that could help pay the bills if a disaster, disability, or other crisis intrudes on the ability of a business to continue operating for a period of time.

LIFE INSURANCE

There are two aspects to life insurance — the first is coverage of a family member’s life and the second is insurance on a third party’s life. There are a variety of reasons to have coverage in both of these situations.

Family coverage. Life insurance coverage should pay enough to ensure the preservation of the lifestyle of a surviving spouse and children, as well as the children’s educational goals. That includes money for ongoing expenses, debt payments, and tuition. Working spouses should also consider similar coverage. As painful as it might seem, it is also necessary to consider burial coverage for children.

Insurance on another person’s life. There are some cases when it makes sense to buy insurance on another person’s life due to the potential financial loss that could occur if that person died. In order to buy such coverage, the insured and the beneficiary must know one another and have an emotional or financial connection such that the insured wants the beneficiary to receive a benefit in the event of death. Circumstances in which you may want to consider purchasing such a policy include divorce, to protect an inheritance, for a business partner to keep a business going, or to collect on a loan.

In a divorce, the spouse who is making alimony or child support payments should be covered so the spouse receiving those payments still has a source of income support if the former spouse dies. It can also be a good idea for the former spouse who is taking care of the children to be covered by a policy so that if he or she dies, the working spouse can cover childcare expenses.

In the case of protecting an inheritance, insurance coverage can help ensure adequate cash to cover taxes and other post-death costs outside of probate. For the owner of a small business, the death of a partner can throw the whole future of the business into question, so an insurance policy and agreement can provide for the surviving partner to have the cash and agreement in place to buy the deceased partner’s share of the business. In the case of a personal loan to a family member or friend, an insurance policy can ensure that the loan is repaid if the borrower dies unexpectedly.

A FINAL WORD

It’s a good idea to regularly set a date to review insurance coverage and check with an insurance agent to make sure you have all the types of coverage you need at the appropriate levels.

Because insurance is such an important component of overall risk management and financial planning, be sure to discuss your needs with your advisor during your annual review or at least once during each year.

——————————————————-

As Director of Retirement and Life Planning for Horsesmouth, Elaine Floyd helps advisors better serve their clients by understanding the practical and technical aspects of retirement income planning. A former wirehouse broker, she earned her CFP® designation in 1986.

Amy Buttell earned an accounting certificate from Mercyhurst University in 2009 and has written about insurance, financial planning and risk management for 14 years.

Copyright © 2013 by Horsesmouth, LLC. All Rights Reserved.

License #: 4259979-353740 Reprint Licensee: Ciccarelli Advisory Services, Inc

IMPORTANT NOTICE This reprint is provided exclusively for use by the licensee, including for client education, and is subject to applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties expressed or implied are hereby excluded.

Priority Spending

Kim Ciccarelli Kantor | Naples Daily News | August 29, 2013

Priority spending is more of a buzz word around our house than the word “budgeting.”

Somehow, the thought of a budget brings negative connotations. A more positive experience is to choose how you wish to spend your discretionary cash flow. A mentor once told me money was meant to be relatively unimportant.

However, to keep it this way, one had to be in a position of financial security and confident that money need not become an issue.

Financial security does not have the same measurement for everyone. How much in financial assets you need is your choice. The key to success is finding that balance in your life which allows you to devote your time to those things that are most important to you.

For some, this may be family, faith, business or health matters.

The workplace today and the investment arena provide unlimited rewards not only monetarily, but personally. Young adults have the capability to plan out the lifestyle they seek. Putting money to work today with the multitude of investment choices is easy. Growing financial assets can be a reality for everyone.

Today, more individuals participate in the stock and bond markets than ever before. With the right investment philosophy, when $1 becomes $2 and $2 can become $4, money no longer needs to be an issue. Managing financial security properly does not stop with investment management.

It continues with the discipline of how you choose to spend your free cash flow.

Every day you make decisions on how to spend your money. Will you travel? Go to dinner? Purchase real estate? Buy furniture? Perhaps buy a car? Or invest in the market? Will you do your homework when purchasing and determine if you want the extra sports car today or a family cottage on the lake tomorrow?

What are your priorities? If it is to have a vacation house you can take your family to, and then structure your investments now to provide the capital you will need in the future.

Spending your available cash flow now on a car can negate the possibilities of a cottage purchase several years from today.

Those individuals who have found financial security have done so because they rationally think through the financial decision they make every day.

A form of measurement is applied when a dollar is spent versus invested. Spending a $1 today does not only cost that $1, but it costs the lost opportunity of what that $1 could do in your portfolio. If you can view your spending as a “priority spending” decision, you will perhaps become more disciplined in how you spend, save and invest.

Write down your short term and long term goals, work toward them and measure your progress for a confident financial journey.