CAS News

CAS Selected as a Finalist for “Florida Companies to Watch”

We are proud to announce that Ciccarelli Advisory Services, Inc. was selected as one of four companies in Collier County as a finalist for the “Florida Companies to Watch” awards program.

This awards program is presented by GrowFL- the Florida Economic Gardening Institute (in association with Edward Lowe Foundation)- state economic development program at the University of Central Florida. It seeks to identify, serve, and celebrate these Florida companies that have the best potential to contribute to Florida’s economy- those companies with solid increasing revenue growth and new job creation potential.

2014 marks the fourth anniversary of “Florida Companies to Watch” awards program. The distinctive awards program is specifically designed to seek out second-stage businesses from a wide range of industries throughout Florida. GrowFL’s definition of “Second-Stage” companies are those identified as a company somewhere between a start-up and a large firm- with a common ground of being poised for growth. These companies have 10-99 employees and $1 million to $50 million in revenue. Companies selected for the award have been determined to strengthen the economy of the region and support the spirit of the entrepreneurs who live among us.

Family Meeting: The Power of Conversation

Kim Ciccarelli Kantor | Life in Naples Magazine | August 2014

Kim Ciccarelli Kantor | Life in Naples Magazine | August 2014

All families desire a common thread, and though difficult to identify where the need is greatest, families whose assets range between $5,000,000 and $20,000,000 + have a significant need. This is where the family can benefit from an approach to financial areas that can provide an enhancement to how they each address their own concerns in planning. The difference between a cohesive or non-aligned plan can be significant.

By textbook definition, ultra high net worth families oftentimes have the money run for them by family offices or an assigned company or party, with each family member benefiting from an aligned plan for their inheritance or legacy. This is not true however for most families, who are not considered “ultra-wealthy” by financial terms, but have been successful in achieving wealth. They generally have respectfully developed assets and a financial security, but do so by seeking their own separate guidance. Historically bridging the many tools available under an aligned interest has not been top of mind. Planning benefits can be collectively designed to enhance each family member’s planning in a confidential, individualistic way as a member of the family group.

The family meeting has helped families bridge an otherwise unmet need for education, trust planning, healthy money discussions and knowledge transfer. Serving multiple family members can help bring harmony in an otherwise difficult situation. There is a need for parents to have conversations about money, family values and the future. A family meeting offers an opportunity to discuss critical issues that can impact today and future generations. When families are empowered to discuss more than money, there is an opportunity to build stronger family cohesiveness, especially prior to a crisis or critical life change such as health issues or death. Family history can be shared and many can be enlightened about how family members evolve their values and plans. This leaves a meaningful mark. Family meetings are to a family, what a strategic planning meeting is to a company. And as our family facilitator stresses, preparation is the key to a successful outcome. Individual interviews can be accomplished by an outside facilitator so that all have input and can identify with the goal of bringing the family together.

Objectives can be to work on keeping the family together, providing a common interest platform for otherwise geographically diverse families such as a philanthropic family fund, sustaining the innate value of the family legacy, sharing the areas you wish to pass on to younger generations regarding your insight or experiences that shaped your thinking, and with all this in mind, setting the expectations and responsibilities for the family members. All inheritances or gifts are important, regardless of size. Don’t let your family be a part of the normal statistics where over 70% of an asset transfer is lost by the second generation and more than 90% by the third¹….forming the old saying “Shirtsleeves to shirtsleeves in three generations.” Most people are simply inexperienced to handle a large sum directed to them in a disciplined way unless they have been prepared properly and have a “vision” of their wealth responsibility. Best of planning to you, most of all, seek advice as your family and your planning is the bridge that allows you to cross the gorge.

¹Source: http://online.wsj.com/

The 2014 Social Security Trustees Report: What Does the Future Hold?

On July 28, The Boards of Trustees for Medicare also issued their 2014 annual report on the current and future financial health of the Medicare program. The financial projections in their report indicate that even though the trust fund that finances Medicare’s hospital insurance coverage will remain solvent until 2030 (four years beyond last year’s projection), steps need to be taken to address Medicare’s financial challenges. To read this report, visit www.cms.gov.

Every year, the Trustees of the Social Security Trust Funds release a report to Congress on the current financial condition and projected financial outlook of the program. This year’s report, released on July 28, contains valuable information about the health of Social Security that may help you understand how your Social Security benefits might be affected.

What are the Social Security Trust Funds?

The Social Security program consists of two parts. Retired workers, their families, and survivors of workers receive monthly benefits under the Old-Age and Survivors Insurance (OASI) program; disabled workers and their families receive monthly benefits under the Disability Insurance (DI) program. The combined programs are referred to as OASDI. Each program has a financial account (a trust fund) that holds the Social Security payroll taxes that are collected to pay Social Security benefits. Other income (reimbursements from the General Fund of the Treasury and income tax revenue from benefit taxation) is also deposited in these accounts. Money that is not needed in the current year to pay benefits and administrative costs is invested (by law) in special Treasury bonds that are guaranteed by the U.S. government and earn interest. As a result, the Social Security Trust Funds have built up reserves that can be used to cover benefit obligations if payroll tax income is insufficient to pay full benefits.

What are some highlights from this year’s report?

This year’s Trustees report projects that the OASI Trust Fund and the DI Trust Fund will have sufficient reserves to pay full benefits on a timely basis until 2034 and 2016, respectively. The combined trust fund reserves (OASDI) are still increasing and will continue to do so through 2019. Beginning in 2020, annual costs will exceed total income, and the U.S. Treasury will need to redeem trust fund asset reserves. The combined trust fund reserves will be depleted in 2033 if Congress does not act before then. This is the same year projected in last year’s report.

Once the combined trust fund reserves are depleted, payroll tax revenue alone should still be sufficient to pay about 77% of scheduled benefits. This means that 20 years from now, if no changes are made, beneficiaries may receive a benefit that is about 23% less than expected.

However, because the DI Trust Fund reserve is projected to be depleted in two years, legislative action is needed as soon as possible. Once the reserve is depleted, income to the fund will be sufficient to pay only 81% of DI benefits.

You can view the 2014 OASDI Trustees Report at www.ssa.gov.

Why is Social Security facing financial challenges?

Fewer workers are paying into the system, so payroll tax income is decreasing. When there are fewer payroll taxes coming into the system each year than benefits paid out, trust fund reserve assets have to be spent to make up the difference. The strain on the trust funds is worsening as large numbers of baby boomers reach retirement age and Americans live longer.

What is being done to address the financial challenges Social Security faces?

For years, the Trustees have been urging Congress to address the financial challenges in the near future, so that solutions will be less drastic and may be implemented gradually, lessening the impact on the public. As the conclusion to this year’s report states, “The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust to them. Implementing changes soon would allow more generations to share in the needed revenue increases or reductions in scheduled benefits. Social Security will play a critical role in the lives of 59 million beneficiaries and 165 million covered workers and their families in 2014. With informed discussion, creative thinking, and timely legislative action, Social Security can continue to protect future generations.”

Action needs to be taken very soon to address the DI program’s reserve depletion. According to this year’s report, in the short term, lawmakers may reallocate the payroll tax rate between OASI and DI (as they did in 1994). However, this may only serve to delay DI and OASI reforms. Members of Congress and the President support longer-term efforts to reform Social Security, but progress on the issue has been slow.

Some long-term reform proposals on the table are:

- Raising the current Social Security payroll tax rate (according to this year’s report, an immediate and permanent payroll tax increase of 2.83 percentage points would be necessary to address the revenue shortfall)

- Raising the ceiling on wages currently subject to Social Security payroll taxes ($117,000 in 2014)

- Raising the full retirement age beyond the currently scheduled age of 67 (for anyone born in 1960 or later)

- Reducing future benefits, especially for wealthier beneficiaries

- Changing the benefit formula that is used to calculate benefits

- Changing how the annual cost-of-living adjustment for benefits is calculated

What can you do in the meantime?

The financial outlook for Social Security depends on a number of demographic and economic assumptions that can change over time, so any action that might be taken and who might be affected are still unclear. But no matter what the future holds for Social Security, your financial future is still in your hands.

- Follow the news to learn about new developments or proposed legislation to reform Social Security

- Understand your own benefits, and what you’ll receive from Social Security based on current law

- Consider various income scenarios when planning for retirement

- Focus on saving as much for retirement as possible

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014

A View of Healthcare from Around the World

The United States health-care system has been impacted by the Affordable Care Act (ACA). But how does delivery of health care in the United States compare to that of other nations? And where does the United States rank with respect to the cost of health care per capita and as a percentage of gross domestic product?

The United States health-care system has been impacted by the Affordable Care Act (ACA). But how does delivery of health care in the United States compare to that of other nations? And where does the United States rank with respect to the cost of health care per capita and as a percentage of gross domestic product?

Types of health-care systems

While each country has its own system of health care, most health-care systems generally fall within the parameters of one of four models, with the health-care system of the United States consisting of aspects of each of these models.

The Beveridge Model.Countries such as the United Kingdom, Finland, Denmark, Spain, and Sweden generally follow this model, named after social reformer William Beveridge. Health care is deemed to be a right for each citizen and is provided by the government and financed primarily through taxes. Hospitals and clinics may be government owned, and medical staff, including doctors, may be government employees. Medical providers are paid by the government, which generally dictates treatments provided and the cost for services.

The Bismarck Model.The Bismarck Model requires that all citizens have health insurance. Health care is provided by private doctors and hospitals whose fees and charges are paid for by insurance. The insurance programs are nonprofit entities and must accept all applicants, including those with pre-existing medical conditions. Insurance is funded through employer and employee payroll taxes. Countries that use a form of the Bismarck Model include Germany, France, Belgium, the Netherlands, Japan, and Switzerland.

The National Health Insurance (NHI). Combining aspects of both the Beveridge and Bismarck Models, the NHI Model is used in several countries, with the most prominent being Canada. Health care is provided through private providers who are paid by government-run insurance. Citizens pay into the government insurance program primarily through taxes. As the sole payor, the government directly influences the cost of medical care and the services covered.

The Out-of-Pocket Model. Used by the majority of countries, including China, this model provides little or no government health care. Instead, those who can afford care get it and those who cannot pay for care generally do not receive care.

The United States Model.The United States incorporates all of these systems to varying degrees. Medicare is akin to the NHI Model; servicemembers and veterans receive health care similar to the Beveridge Model; and the ACA can be described as a type of Bismarck plan, although health insurers are typically for-profit entities.

Comparing the cost of health care*

The following information compares health-care expenditures of several countries as a percentage of gross domestic product as well as per capita.

*Information derived from The World Bank Health, Nutrition, and Population Data and Statistics (www.datatopics.worldbank.org)

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

The Healthcare Dilemma

Jill Ciccarelli Rapps | Life in Naples Magazine | August 2014

Jill Ciccarelli Rapps | Life in Naples Magazine | August 2014

One of the most important issues for all of us is managing our affairs for longevity. Many elderly today did not plan to live so long; they did not consider if their assets would last well into their 90’s, or what their needs would be. Today the baby boomer generation may live past age 100 and our children and grandchildren as well. Living longer has wonderful benefits, but the challenges of managing our health care can be devastating for you and your family if a plan is not in place. Even though health care in our lifetimes will most likely be our largest expense, second to our home, very few of us spend the time planning for it until something urgent happens. If you have not had a serious conversation about how the cost of your health care may affect your quality of life, maybe today is the time to do so!

For those under 65 (not on Medicare), you will experience the greatest shift in cost to cover you and your family for healthcare. Companies will start to shift more and more costs to their employees, and with current government deficits, you may not be able to rely on our Medicare program like we know it today. In fact for people who are 65, Medicare is only covering about 51% of their health care costs[1]. The other myth about Medicare is that it covers long-term care costs. Medicare may pay a portion of up to 150 days of hospital insurance (inpatient, skilled nursing, home health, hospice); after that you are on your own!

Your financial advisor may help you complete a health care assessment to estimate future health care costs including long term care costs. A plan should be designed and integrated with your financial plan. The key is to have your own personal strategy in place so you are not surprised by what the future may bring, and worse yet, lose the quality of your life.

There are many health care strategies that one may utilize, including; 1) developing your own “bucket” of assets for health care needs, just like you would do for retirement, travel, education etc., 2) purchase or convert your old life insurance contracts to a long term care insurance “hybrid” policy, 3) consider purchasing long term care insurance, or 4) do your homework on a continuing care community, where your lifetime care may be provided to you as your needs arise. Each option takes time to understand and to decide which is best for your situation, and because everyone is so unique, each and every plan should be personalized. Your financial advisor can educate you on the opportunities available, how each plan may affect your financial affairs, and help guide you to create a health care strategy that you are comfortable with. Like almost everything in life, planning ahead can make a huge impact on the quality of your health and your lifestyle! The bottom line, if you have not already, make a point to focus on your health care and develop a plan no matter what age you are!

[1](Fonstin, Paul. “Savings Needed to Fund Health Insurance and Health Care Expenses in Retirement. Findings from a Simulation Model\ EBRI”. Employee Benefit Research Institute\EBRI. May 2008. The official U.S. government Medicare Handbook. The official U.S. government Medicare Handbook, Medicare & You, 2013.

Family Night at Frontier Field, Rochester, NY

Come join us to watch the Rochester Red Wings play the Syracuse Chiefs and enjoy a picnic dinner and fireworks after the game!

Come join us to watch the Rochester Red Wings play the Syracuse Chiefs and enjoy a picnic dinner and fireworks after the game!

You, your children, and grandchildren are invited to join us for a picnic and a night of baseball at Frontier Field in Rochester, NY on Friday, August 15, 2014 at 6:00 PM. This event grows larger every year, so reservations are limited to a maximum of 8 tickets per family. To reserve your tickets please email cgurnow@cas-rocny.com or call 585-383-0180. Please provide an accurate count of adults and children, and be sure to include the children’s ages. Kindly RSVP by August 8, 2014. Seats are limited.

Tickets can be picked up on the day of the game at our table outside the main gate at 6:00 PM. The Nest will begin serving food at 6:00 PM. Game starts at 7:00 PM.

Please note: THIS EVENT WILL BE RAIN OR SHINE

In the event of rain, we will still enjoy a picnic together, as that area is covered. Your game tickets will be issued a makeup game.

We look forward to seeing you there!

Economic Update – Second Quarter 2014

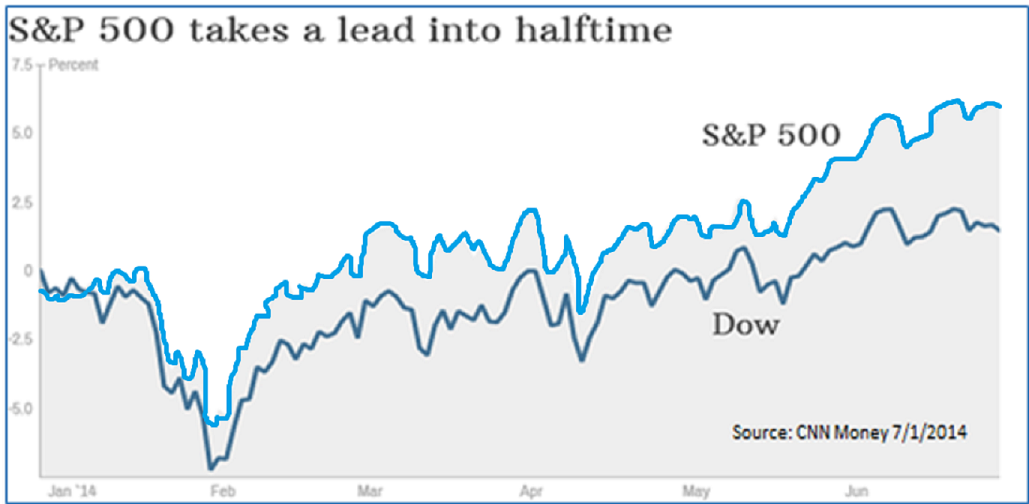

The year’s first half for equities can be summed up in simple terms: confusing and unpredictable markets produced gains. As of June 30, the S&P 500 had already logged 22 record highs this year alone, ending the first half up 6% while the Dow Jones Industrial Average (DJIA) increased by 1.5%. Both of these indexes hit new highs in the 2nd quarter while the NASDAQ Composite index rose by 5.5%, reaching a 14-year highpoint. Interestingly, 2014 has produced the biggest halftime lead by the S&P 500 over the DJIA since 2009 and the seventh-biggest since 1929, according to Bespoke Investment Group.

Bespoke also shared that in eight of the 10 years with the most underperformance, the DJIA has gone on to outperform the S&P 500 during the second half of the year. If this pattern holds, then the Dow might make up some of that lost ground. (Source: Barron’s, June, 2014)

Investors started 2014 with several serious concerns that were enough to make them nervous. How would the S&P 500 Index follow up 2013’s 30%+ gain (including dividends)? Would the market correct because the bull was getting tired, or would there be profit-taking? Would the slow improvement in the U.S. economy send bond prices lower, or would we see the Federal Reserve shift to higher interest rates? All of these fears made investors nervous.

Would the market correct because the bull was getting tired, or would there be profit-taking? Would the slow improvement in the U.S. economy send bond prices lower, or would we see the Federal Reserve shift to higher interest rates? All of these fears made investors nervous.

So far in 2014, the bond market has also fared well—in fact, better than most had expected. The yield on the U.S. Treasury ten-year note, which moves inversely to its price, fell to 2.51% from 2.76% at the end of the first quarter.

Unfortunately, many investors are having a hard time enjoying these increases, as concerns about lofty prices make it difficult to decide whether to keep funds in cash or stay invested. The forces driving the stock market to new highs and helping parts of the bond market to remain near record low yields don’t show immediate signs of changing.

What are the forces driving the rallies in both stocks and bonds? Many economists credit the aggressive efforts by the world’s major central banks to flood financial markets with new money in an effort to keep sluggish economies continually moving forward.

U.S. stocks have been supported by expectations that the U.S. economy, while still sluggish, will grow fast enough to keep corporate profits expanding. However, many investors no longer feel comfortable with that outlook, and have begun focusing more on what can go wrong with their portfolios than on where they can make money.

The current stock market rally has outlasted the historical average of other Bull Markets with higher returns. In contrast, the preceding Bear Market was much steeper and longer than average, and the gains from the period—from the beginning of the Bear Market to the end of this Bull Market—are currently near the median and below the average. This confusion can be why many investors are proceeding with great caution. (Source: Fidelity)

There is “still a bit of a fear-factor” among investors, said Thomas Huber, Manager of the T. Rowe Price Dividend Growth Fund. “Everyone is looking for what’s going to be the big crack in the markets.” (Source: Wall Street Journal, July 1, 2014)

While many investors are concerned about how markets will respond when the Fed raises interest rates in the future, there are also concerns building in the opposite direction regarding the estimate in the growth of our economy. The Commerce Department’s third and final estimate of the Gross Domestic Product (GDP) for the first quarter of 2014 continued the downward spiral of the first two estimates—from +0.1% to -1.0%, and now down to -2.9%. This was the largest drop recorded since the end of World War II that wasn’t part of a recession.

Many economists believe that the extent of the first quarter decline is so substantial that it makes it unlikely that we will reach a 2% increase, even if the next three quarters are significant. (Source: Bob LeClair’s Finance, June 28, 2014)

Early in the year, stocks ran into problems and investors blamed the harsh winter weather in large parts of the country. Several early indicators led to speculation that the economy was weakening, but in the 2nd quarter the market rebounded, sparked by thoughts that better growth was leading winter into spring. So far, those thoughts have proved to be accurate: the U.S. economy has improved, although there are still concerns over how strong the rebound will be.

A recent GDP report offered some positive data, including:

- Existing-home sales climbed 4.9%, the strongest gain in three years.

- New-home sales jumped 18.6% in May (the largest gain in more than 20 years) to an annual rate of 540,000 units, a six-year high. The median price for a new home also increased almost 7% from last year.

- The Conference Board’s confidence index improved to 85.2 in June. That was its highest reading since 2008, as many consumers were more optimistic about jobs and future conditions. (Source: Bob LeClair’s Finance, June 2014)

Will we be able to hold onto these gains and add enough through the end of the year to at least have a positive GDP for 2014? Let’s hope so. Slow growth could reduce corporate profits, which would be bad news for stocks and could lead to higher-than-expected default rates on junk bonds.

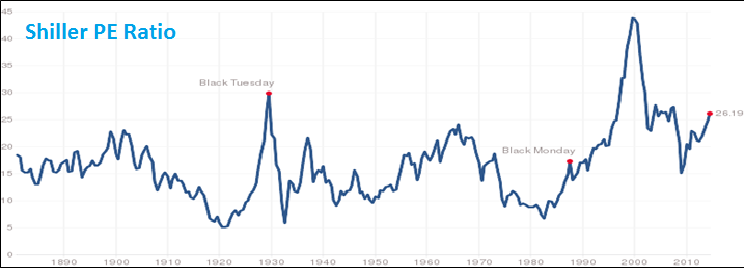

PRICE–TO–EARNINGS RATIO

Price-to-earnings (P/E) ratios have risen over the last two years, as improving investor confidence helped drive market gains. Some are focused on the current valuations which are slightly above the long-term average, 17.1 versus 15.1. The higher the P/E, the more likely the stock market is overpriced. Although most stock indices are at an all-time high, the market valuation is nowhere near its 2001 peak. (Source: Fidelity.com)

Even with a gain in the first half of 2014, bears exist. Nobel Prize-winning professor Robert Shiller notes that currently the market looked more expensive on a cyclically adjusted price/earnings basis only three other times in the past 130 years—1929, 2000 and 2007. The Shiller P/E ratio for the S&P 500 is based on average inflation-adjusted earnings from the previous 10 years. Despite this statistic in today’s low interest rate environment, Shiller is not telling investors to sell all of their holdings and to retreat to a bunker. He just thinks it might be time to be cautious and lighten up.

STOCK BUYBACKS

Many investors do not realize that one of the stock market’s biggest drivers today is stock buybacks. Companies buying back their own shares represent the single biggest category of stock buyers today, according to a study by Jeffery Kleintop, Chief Market Strategist at LPL Financial. (Source: Wall Street Journal, June 30, 2014)

Stock buybacks are also a source of controversy. Some economists say they allow companies to provide artificial support for stock prices by increasing demand for shares. Also, if a company reduces its number of shares, simple math shows that the earnings per share will rise even if the total earnings go nowhere. Most professional money managers look primarily at earnings per share, so buybacks can improve a company’s apparent earnings performance, even if overall earnings aren’t rising at all. Executives may use buybacks to manipulate share prices, helping them hit earnings targets, receive bonuses, and other benefits.

According to Mr. Kleintop, half of the first quarter’s S&P 500 per-share earnings gains came from declining share count, not from increases in actual earnings. (Source: Wall Street Journal, June 30th)

That doesn’t mean all buybacks are misguided, he added. In some cases, buybacks are better than dividends as a way to return money to shareholders because investors pay taxes on dividends and don’t pay taxes on buybacks unless they sell their shares.

GLOBAL

Financial markets worldwide are getting a boost from recent upbeat economic data out of China that is improving the outlook for global growth. China has increased its manufacturing activity and many economists believe that its appetite for raw materials will continue.

Many markets were rattled earlier this year by worries that China’s slowing growth would lead to a hard landing. However, the Chinese government has taken various measures to build investor confidence, including credit easing, more spending on highways, and business tax breaks.

After a massive credit boom in recent years, China continued to struggle to balance the competing objectives of tapering down its excessive credit expansion, preventing financial instability, and maintaining a fast pace of growth. Foreign capital inflows have risen and become more short-term in nature, increasing China’s vulnerability to shifts in global capital flows. (Source: Fidelity)

The U.K. and Germany remain the primary drivers of the European Economic Expansion, but there have now been indicators that other European economies have improved significantly, suggesting that Europe’s cyclical upturn continues to become more broad-based.

INTEREST RATES

Central bankers around the world debate whether very low interest rates, adopted in many economies since the 2008 financial crisis to spur stronger recoveries, are actually feeding market bubbles that could burst and potentially cause new financial turmoil. In June, Mario Draghi, President of the European Central Bank (ECB), made a bold move by cutting the main lending rate from 0.25% to a record low 0.15%. This pushed the deposit rate from zero to a minus 0.1%, effectively charging banks to park funds at the central bank. Following that move, Mr. Draghi said, “Are we finished? The answer is no. If need be, within our mandate, we aren’t finished here.” (Source: Barrons, June 2014)

The Fed has held short-term interest rates near zero since late 2008 and is winding down its bond-buying program. Recently, Janet Yellen, Chairperson of The Federal Reserve, assured investors and the public that the Fed won’t raise interest rates abruptly simply because some markets may look a bit volatile. The Fed has taken pains to reassure investors that interest rates will remain low even as the economic recovery picks up. (Source: Wall Street Journal, July 3, 2014)

Most Fed officials have indicated they expect to start raising interest rates in 2015, but the final decision will depend on whether the economy continues to strengthen as they forecast. The Fed has also stated that when it actually does increase rates, it will do so gradually and short‑term interest rates are unlikely to rise as high as they have in previous recoveries.

Many investors think that the rise in interest rates could happen sooner than the Fed’s estimate and the pace of increases could be more rapid than currently expected.

Historically, low interest rates and strong profitability have allowed U.S. corporations to reduce interest expense, improve their balance sheets, and accumulate liquid assets. Companies have used high cash balances to return capital to shareholders as both dividends and share buybacks, maintaining relatively high yield even though equity prices have continued to rise.

INFLATION

Inflation finally nudged above the 2% level that the Fed says is its long-term target. Compared with a year ago, the Consumer Price Index (CPI) is up 2.1% (not including food or energy). Although that might make the Fed happy, it sent a tremor of worry through analysts, investors, and economists.

Ongoing weak wage growth has continued to eliminate inflationary pressures in many developed economies. Weaker economic outlooks may help bring down inflation in some emerging markets’ economies over time. However, the rapid rise in agricultural prices could create inflationary pressures in many emerging economies, where food represents a higher proportion of consumer expenses. (Source: Fidelity)

UNEMPLOYMENT

On Wednesday, July 2, a report on the U.S. labor market was better than expected in that 281,000 private-sector jobs were created in June compared with an estimated increase of 210,000.

Although this is certainly good news, many investors say that stocks will need continued evidence of an improving economy to sustain the move higher. (Source: Wall Street Journal, July 3, 2014)

CONCLUSION

Equities have provided a nice return for the first half of 2014, so now what should an investor do? Your answer could depend upon your “worry level.” Some believe that stocks will benefit from robust earnings and low interest rates, while many other financial professionals are spending sleepless nights focusing on downward equity outlooks. The Federal Reserve has been a key factor in why equity markets have done well since 2009, but they have already started paring back their bond purchase programs and they will need to raise interest rates eventually.

Several money managers are suggesting that the five-year-plus bull market may be getting long in the tooth, but few are selling the bulk of their portfolios and leaving the room. Those money managers who sided with caution so far in 2014 have underperformed the indexes; however, even the great Confucius once said “the cautious seldom err.” Money managers that sometimes hold large cash positions don’t always move in sync with peers or benchmark indexes. Approaching market tops, they may become increasingly cautious, while peers remain fully invested. Thus, it is common for such money managers to trail peers when stocks are moving higher like they did in the first half of this year.

Several money managers are referring to the current period as the “new neutral.” Although U.S. stock indexes are pushing through fresh records and valuations have passed pre-financial crisis levels, some analysts believe markets aren’t overvalued yet.

“Sure, the S&P 500’s valuations look high on historical standards, but it’s really about ultra-low yields,” Bill Gross, chief investment officer at Pimco, told CNBC recently, citing Pimco’s “new neutral” mantra that the neutral federal funds rate will be lower for longer. “Based upon our assumption that this new neutral stays low, they’re not as bubbly as some would suggest,” Gross said.

“If fed funds going forward stops at 2% instead of 4%, which is historical, then [the Dow Jones Industrial Average, or DJIA] at 17,000 and high yield spreads at 350 basis points over Treasurys are attractive and are less bubbly than some would imagine,” he said.

In a blog post on July 2, Gross said that the “new neutral” means “all financial assets might logically be repriced relative to historical experience.”

Gross also noted that while the S&P 500’s 10-year cyclically adjusted P/E ratio, or cost adjusted P/E (CAPE), typically has predictive value of whether shares are overvalued, the “new neutral” indicates the CAPE’s historical median valuation of 17 times earnings may need to be adjusted to around 20-22 times. “That would mean the S&P 500’s current CAPE of 25 times isn’t terribly bubbly.”(Source: CNBC.com, July, 2014)

With the stock market setting new highs, investors face unusually tough choices. An examination of historical valuations points to proceeding with caution in the stock market. Normally during these times bonds would provide a safe harbor. Sadly, with interest rates still near historic lows, bonds might not provide the same portfolio protection as in years past and, potentially even worse, bond prices will decline when interest rates rise.

Fed Chairperson Janet Yellen warned investors on July 2 that, “Falling corporate bond spreads and volatility indicators are signs that investors may not fully appreciate the risk of future losses.” She continued her prepared remarks for a speech at the International Monetary Fund by also sharing, “that said, I do see pockets of increased risk-taking across the financial system.”

It’s not easy to structure a portfolio in the face of these risks, but investors still have to make some decisions. Perhaps the best advice is to continue to focus on your personal situation and timelines. Consider these three important questions:

- What is a realistic time horizon for my personal situation?

- What is a realistic return expectation for my portfolio?

- What is my risk tolerance?

Your answers to these questions will help us recommend what type of investment vehicles you should consider, which investments to avoid and how long to hold each of your investment categories before making major adjustments. For example, if you will need more cash flow from your investments over the next few years, you might consider different choices relative to someone who has a ten- to fifteen-year time horizon.

We are continually reviewing economic, tax and investment issues and drawing on that knowledge to offer direction and strategies to our clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

On a final note, remember, one of the major causes of a stock market decline may not be investment performance—sometimes it’s investor behavior.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the “emotions” out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

P.S. During this year’s big Treasury rally, the question has been, “Who’s buying all those bonds?” The answer is the Federal Reserve. During the six months ended in May, the Fed bought 73% of all new Treasurys, notes Strategas Research Partners’ Daniel Clifton. That’s the largest percentage since the start of quantitative easing.

The reason isn’t greater demand, but reduced supply. With the budget deficit falling, the amount of bonds issued has declined faster than the Fed’s taper, or reduction in bond buying. That leaves a limited supply of bonds for others to buy, according to Clifton. Perhaps that’s why bonds have held up in the first half of 2014.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. The investor should note that investments in lower-rated debt securities (commonly referred to as junk bonds) involve additional risks because of the lower credit quality of the securities in the portfolio. The investor should be aware of the possible higher level of volatility, and increased risk of default.

The payment of dividends is not guaranteed. Companies may reduce or eliminate the payment of dividends at any given time.

Sources: CNN Money; Shiller PE Ratio; Barron’s, June 2014; Bob LeClair’s Finance, June 2014; Fidelity; Bob LeClair’s Finance, June 28, 2014; Wall Street Journal; CNBC.com 7/2014 Contents © 2014 Academy of Preferred Financial Advisors, Inc.

Chart: Ten-Year History of U.S. Average Gasoline Prices

Gas prices fluctuated widely in 2008, peaking at a high of $4.11 during the second week of July, then plummeting to $1.81 by the first week of December. Since 2008, gasoline prices have generally been on an upswing, but have leveled off during the past three years, as this chart shows. According to the U.S. Energy Information Administration (EIA), average gasoline prices are even expected to decline slightly in 2015, although projections are far from certain.

Gas prices fluctuated widely in 2008, peaking at a high of $4.11 during the second week of July, then plummeting to $1.81 by the first week of December. Since 2008, gasoline prices have generally been on an upswing, but have leveled off during the past three years, as this chart shows. According to the U.S. Energy Information Administration (EIA), average gasoline prices are even expected to decline slightly in 2015, although projections are far from certain.

Sources: Short-Term Energy Outlook, May 6, 2014, U.S. Energy Information Administration, www.eia.gov; Chart data is from the EIA’s Weekly U.S. Regular Conventional Retail Gasoline Prices (chart shows average dollars per gallon as of the second week of May of each year).

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

Gas Prices: Why are you paying more at the pump?

Have you ever stood at the pump wondering why you’re paying so much to fill up your vehicle? The answer is … complicated. According to the U.S. Energy Information Administration (EIA), many factors contribute to the cost of a gallon of gasoline, including the price of crude oil (which accounts for the majority of the cost), refining costs and profits, taxes, and distribution and marketing expenses.

Have you ever stood at the pump wondering why you’re paying so much to fill up your vehicle? The answer is … complicated. According to the U.S. Energy Information Administration (EIA), many factors contribute to the cost of a gallon of gasoline, including the price of crude oil (which accounts for the majority of the cost), refining costs and profits, taxes, and distribution and marketing expenses.

The price of crude oil is dependent on global supply levels relative to demand, and can be influenced by political events in major oil-producing countries, supply disruptions (which often result from hurricanes and storms in supply zones), and market speculation. Supply and demand is also one of the reasons that U.S. gas prices tend to fluctuate seasonally, with prices generally rising in the spring and remaining higher in early summer. But refining costs also play a role. Prices tend to rise as refineries shift from winter to summer gasoline blends in order to meet federal and state environmental guidelines. Gasoline must be blended with other ingredients to reduce emissions, and costlier ingredients are used in the summer blend.

How much you pay for gasoline also depends on where the pump is located and who owns it. For example, prices are generally highest on the West Coast due to higher state taxes and transportation costs from distant refineries. But no matter where you live, you know that prices also vary locally from one station to the next. Why? Generally it’s because the cost of doing business for an individual station owner varies. The price the station pays for gasoline, the station’s location and volume of business, and whether it must match or beat prices from local competitors all contribute to how much you pay for a gallon of gas.

What’s the outlook for the future? The EIA expects the average price of gasoline to fall in 2015 to $3.39 per gallon. Despite the increasing demand from emerging economies, U.S. crude oil reserves and production are expected to increase, and U.S. demand is expected to decrease as vehicles become more fuel efficient.

Sources: “Factors Affecting Gasoline Prices” and “Short-Term Energy Outlook”, May 6, 2014, www.eia.gov

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

Charitable Giving: Unite together for the benefit of others

Kim Ciccarelli Kantor | Life in Naples Magazine | May 2014

Kim Ciccarelli Kantor | Life in Naples Magazine | May 2014

Charitable giving is a precious gift and a way to join together with family for a common goal. Here is an example of a Letter to family:

“Dear family,

In our hearts, we hold a special place for those organizations who have directly or indirectly served our family, our community or country. As a family, we have united together for common interests and strive to continue the best level of gifting we can do. From the interactions we experienced, we found a common element that is necessary with all families…the art of giving.

Charitable giving, either with our time as volunteers or monetary support through financial resources, has been integral to how we live. As a side line benefit, we have been able to maximize our legacy, financial and otherwise, by minimizing taxes and uniting family members with differing financial capabilities. We have found a common thread among families that is not painful – the art of philanthropy – and giving money that has been set aside to gift was something not only worthwhile but feasible. It can actually be done.

Our purpose is to continue the enriching experience we gained during our lifetimes through our family Donor Advised Fund. We are making an additional gift to this fund at the time our legacy passes to you. It is your dad’s and my hope that as you work together in addressing issues, challenges and celebrating differences and successes of family members, you will unite together for important work to support charitable interests that need you.

Use our fund to bring together the younger generations, your children, nieces, nephews… our grandchildren and great grandchildren as they are so bright a generation and can get involved by researching charities that may benefit from a gift or that need help with a project.

If we have not yet done so, develop a family website where formal grant procedures can be put in place. Your families can share what is most important to them in addition to the philanthropic common element on an ongoing basis. Young members can develop the important art of giving back by preparing presentations and interviewing the organizations, followed by volunteer work. They can tell of their experience and why the charity of their choice should be granted an award from the family DAF charitable fund. The family can work together to make decisions on how much should be given.

They can learn to review portfolios and, as a great side benefit to all this, work towards a common mission to develop the ability to have intelligent, open discussions about money. An outcome can be seen through development of a family mission statement of your own. Learn the art to facilitating a family meeting where you can set an example for the fiscal responsibilities they will assume with our and your legacy one day. They will develop legacies of their own that will extend beyond this charitable fund. They may gift to this fund on their own and help to grow it, and the continued endowment to fund great purposes for nonprofit organizations in the communities which they live.

In the businesses you work, focus a piece of your time and resources on philanthropy. We have been blessed and can help. Love Mom and Dad”

Seek the privileges of giving back and search out the options that fit best for your family. They will appreciate what you pass on and the gift you leave them of giving.