CAS News

Good News for 529 Plan Savers: More Investment Flexibility

Call it a holiday gift. Thanks to legislation passed in December, beginning in 2015, owners of 529 accounts will be able to change the investment options on their existing plan contributions twice per calendar year instead of just once. This increased flexibility is a welcome option for parents and grandparents who use 529 plans to save for their children’s or grandchildren’s college education.

Call it a holiday gift. Thanks to legislation passed in December, beginning in 2015, owners of 529 accounts will be able to change the investment options on their existing plan contributions twice per calendar year instead of just once. This increased flexibility is a welcome option for parents and grandparents who use 529 plans to save for their children’s or grandchildren’s college education.

Previously, if an account owner had exhausted his or her once-per-year investment change allowance, the only way to change investment options again on existing contributions in the same year was to change the beneficiary of the account, which may not have been desirable or feasible.

Many college savers–and even states that manage 529 plans–have characterized the once-per-year rule as too restrictive and have called for changing it. Congress listened once before. During the stock market downturn that began in 2008, Congress passed a rule allowing 529 account owners to change their investment options on existing contributions twice per year, but only for 2009. The once-per-year rule kicked back in for 2010.

Although a jump from one investment change to two isn’t earth-shattering (some would argue it’s not nearly enough), it still offers a bit more flexibility for 529 plan savers who want to make an additional investment change during the same calendar year.

Note: Investors should consider the investment objectives, risks, charges, and expenses associated with 529 plans before investing. More information about specific 529 plans is available in each issuer’s official statement, which should be read carefully before investing. Also, before investing, consider whether your state offers a 529 plan that provides residents with favorable state tax benefits. As with other investments, there are generally fees and expenses associated with participation in a 529 savings plan. There is also the risk that the investments may lose money or not perform well enough to cover college costs as anticipated.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014

Video – Data Breaches: Fighting Identity Theft with New Technologies

Economic Update – Fourth Quarter 2014

While market participants and forecasters had their share of surprises and disappointments in 2014, many investors were rewarded as U.S. stocks had a solid year overall. That was not the case for most bellwether international and emerging-market indexes.

The Dow Jones Industrial Average was up 7.5% in 2014 while the S&P 500 experienced its third straight annual increase of over 10%. These two major indexes outperformed the broader market—the NYSE Composite Index rose a little more than 4% for the year.

Perhaps one of the more telling signs for 2015 was that the bull rested on the last two days of the trading year. In fact, U.S. stocks took most of the last week of 2014 off, finishing more than 1% lower. This prompted many market analysts to predict that 2015 could bring a return to more volatility than investors experienced in 2014. The late drop was attributed to an absence of buyers, not a plethora of sellers. Dan Greenhaus, Chief Strategist at BTIG Research, said, “With volumes so low, you can’t read much into the action. The market’s inertia is up until something comes along to change it.”

Bond investors also fared well in 2014. Most Wall Street professionals were off target as they predicted the government bond market to extend its selloff from 2013 and lead to higher interest rates. Thanks to slowing economic growth and declining inflation—especially in Europe—bond prices rose and yields fell.

2014 MARKET RETURNS (Source: yahoofinance.com)

Bonds were also helped when the Federal Reserve signaled that even though they ended their stimulus efforts, they were in no hurry to raise short-term interest rates. This added to the year’s bullish rally for income investors whose holdings were in government or investment grade bonds. Those who invested in sub-investment grade bonds did not fare as well. Russel Kinnel, director of manager research at Morningstar, said many non-traditional bond funds used wide mandates to bet on interest rates rising, “and that was not a great recipe for a year like 2014.” While income investors fared well in 2014, 2015 may look less attractive.

2014 was certainly a year to remember. Let’s review some notable highlights:

- January 31st – The New Year begins badly, as aftershocks from a sell-off in emerging markets hit the U.S.

- February 3rd – Leadership of the Federal Reserve passes to Janet Yellen, but Ben Bernake’s policies still rule.

- February 28th – Russian leader Vladimir Putin invades Crimea, sowing regional turmoil as the West shudders.

- July 3rd – First day the Dow Jones Industrial Average closes above 17,000.

- July 23rd – Oil prices peak at over $100 a barrel before sliding more than 40% in the second half to under $55.

- September 26th – Bond titan Bill Gross leaves Pimco for Janus, sparking huge redemptions at his old firm.

- October 31st – Bank of Japan’s Haruhiko Kuroda grabs the baton from the Fed and doubles down on monetary stimulus.

- November 4th – Republicans gain control of both the House and the Senate after midterm elections as a rebuke to President Obama.

- December 23rd – First day the Dow Jones Industrial Average closes above 18,000.

(Source: Barron’s, 12/2014)

As we look back at 2014, analysts are citing that the U.S. economy is looking better. Financial experts are pointing to the fact that we are experiencing falling unemployment, rising stock prices and an uptick in housing starts. Although at first many predictions for 2014 were met with skepticism, it would be difficult to argue with the average strategists’ 2013 prediction for a 10% rally in 2014.

As we look back at 2014, analysts are citing that the U.S. economy is looking better. Financial experts are pointing to the fact that we are experiencing falling unemployment, rising stock prices and an uptick in housing starts. Although at first many predictions for 2014 were met with skepticism, it would be difficult to argue with the average strategists’ 2013 prediction for a 10% rally in 2014.

Looking Ahead to 2015

Although there are still some strong contrarians out there, the consensus for 2015 appears to be bullish. Many analysts are suggesting that the market will continue to rise based on many factors, including:

- The U.S. economy will continue to move forward in a reasonable manner

- Unemployment figures will continue to go lower

- The European economy will get better

- Japan’s recession will ease

- The Federal Reserve will raise the federal funds rates

- Stocks will remain attractive compared to U.S. Treasuries

Bob Doll, Senior Portfolio Manager and Chief Equity Strategist of Nuveen Asset Management, believes 2015 will be the year of “increasing belief.” In other words, 2015 could be the year that we feel better about the U.S. economy than we do about the stock market. Doll said, “I think the dichotomy between a mediocre U.S. economy and a really good, if not great, U.S. stock market has been the reason people have not gotten enthusiastic.” Doll predicts it will be a good economic year, with low inflation, consumer spending picking up, an improving job market, and a solid year of earnings growth. The biggest risk, however, is the risk of deflation outside the U.S., led by a decline in oil prices. (Source: WealthManagement.com, 1/2015)

While it’s easy for investors to want U.S. stocks to have another strong year in 2015, we still need to remember that the current bull market started in 2009. In fact, some analysts conclude that stocks are no longer cheap—and under certain financial metrics valuations, are high. According to Bloomberg, after gaining 10% in 2014, consensus earnings-per-share growth for U.S. corporations is expected at 8% in 2015.

While no one can predict the future, there seems to be agreement on which factors will most influence investment outcomes. Adam Parker, Chief U.S. equity strategist at Morgan Stanley, says that “everyone is talking about rates, the dollar and oil.”

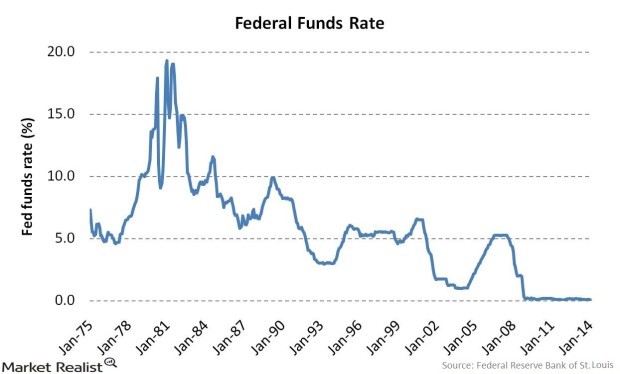

Interest Rates

(Source: Wall street Journal 12/2014)

Interest rates will play a role for investors again in 2015. The Federal Reserve has already signaled that it plans to raise interest rates and phase out the easy money policies that were designed to stimulate the faltering economy from the 2008 financial crisis. Having said that, their timeline for doing so still remains uncertain and financial experts are split on whether interest rates will actually go up in 2015.

Jurrien Timmer, Director of Global Macro in Fidelity’s Global Asset Allocation Division, says that “Federal Reserve uncertainty could mean more volatility for investors. This is particularly true at the beginning of a rate cycle, when the market is trying to gauge the speed and magnitude of the Fed’s plans. Indeed, big questions remain as to whether the Fed will follow a carefully choreographed rate-normalization script in 2015 or whether it will be forced to speed things up or slow them down.”

Most analysts started 2014 with what they considered a can’t-miss notion that interest rates would rise. They fell. Again in 2015, many feel rates could rise. The Fed’s short-term policy affects other rates, but longer-dated bonds depend more on a variety of market-based factors. 2014 results proved those factors can overpower even talks of Fed policy changes. While a growing U.S. economy and a deteriorating European outlook should exert pressure on 30-year Treasury bond yields, inflation needs to pick up meaningfully before that yield can rise significantly. (Source: Barron’s, Dec.15, 2014)

Remember—in many cases, bonds are supposed to provide portfolios with stability and hopefully help against stock market swings. Conservative investors should not try to chase speculative returns in bonds.

In their 2015 Investment Outlook, Delaware Investments wrote, “We believe returns will be lower than they have been in recent years.” They say that bond investing “will be transitioning into a new reality, one in which return expectations ought to be tempered.”

Jeffrrey Gundlach, who oversees $64 billion dollars at DoubleLine and is often referred to as the King of Bonds, agrees with others that the Federal Reserve will begin to raise the federal funds rates this year. However, he also predicts that the result will be the opposite of conventional wisdom, with longer-term yields declining in 2015 and investors facing a flattening yield curve.

As financial professionals, we intend to be very watchful of both the Federal Reserve’s movements and interest rates this year. We would be glad to recheck your personal situation during your next review or at any other time.

U.S. Employment

U.S. Employment

One of the barometers that the Federal Reserve looks to for direction is U.S. employment statistics. The unemployment rate, obtained from a separate survey of U.S. households, was 5.6% in December, down two-tenths of a percentage from November and its lowest level since June 2008. In December of 2014, U.S. employers added to payroll at a brisk rate. While economists surveyed by The Wall Street Journal had predicted that payrolls would rise by 240,000 in December, the actual number of non-farm payrolls rose to a seasonally adjusted 252,000 according to the Labor Department. This brought unemployment down to 5.6%.

Altogether, employers added 2.95 million jobs in 2014, the biggest calendar increase since 1999. Of course, the U.S. population has grown significantly in that time, to a population of more than 318 million in 2014, from 279 million in 1999. (Source: Wall Street Journal, 1/2015)

Oil Prices

Energy stocks have been among the year’s worst performers, as oil prices declined almost 50% from their mid-year peak of over $100 a barrel.

Many investors are questioning if there are bargains in beaten-down energy shares. Some analysts see value, while others fear that oil prices still have to stabilize. Lower oil prices help consumers at the pump, but they can wreak real havoc on unemployment, capital spending, loan collateral values, energy-company balance sheets and the junk-bond market.

Jeffrey Gundlach alerts investors that “the boost to U.S. consumers from lower pump prices is the first shoe to drop, but the negative secondary effects from the crude-oil price lapse take longer to surface.” He also reminds investors that “when you have a market that showed extraordinary stability for five years—trading consistently at $90 a barrel or above—undergo a catastrophic crash like this one, prices usually go down a lot harder and stay down a lot longer than people think is possible.” (Source: Barron’s, 1/2015)

“It’s not clear that anyone can answer how low [oil prices] will go,” said Ed Morse, global head of commodities research for Citigroup Inc. He adds, “It’s always hard to call a bottom.” Oil prices and their fluctuations can create market disruption and uncertainty. Oil prices will be on the list of items that we will monitor in 2015. (Source: Bloomberg.com, 1/2015)

International Concerns

For many market strategists, the bullish case for equities includes a stronger European economy and the end of the current recession in Japan.  Like the U.S., Europe and Japan will benefit from lower oil costs. Their exports are currently cheaper because they have depreciating currencies andtheir borrowing costs are low. Most analysts feel that the European Central Bank will follow the Federal Reserve’s example and provide Quantitative Easing and an asset buying program. These measures allow the European Central Bank to bolster their countries’ money markets by making funds available for banks to borrow on more favorable terms. (Source: Barron’s, 12/2014)

Like the U.S., Europe and Japan will benefit from lower oil costs. Their exports are currently cheaper because they have depreciating currencies andtheir borrowing costs are low. Most analysts feel that the European Central Bank will follow the Federal Reserve’s example and provide Quantitative Easing and an asset buying program. These measures allow the European Central Bank to bolster their countries’ money markets by making funds available for banks to borrow on more favorable terms. (Source: Barron’s, 12/2014)

Russia and China also present concerns for investors. Russia “is in bad shape, due to lower oil prices, but it wants to remain relevant on the world stage,” according to John Praveen of Prudential International Investment Advisors. He and others also caution that China will be another concern for forecasting markets in 2015. Investors will need to see if the Chinese central bank can provide sufficient stimulus to help their economy continue its expansion in 2015. (Source: Barron’s, 12/2014)

U.S. Politics

U.S. Politics

As we head into 2015, the political landscape in the U.S. has changed dramatically. Following six years of gridlock and brinksmanship, 2015 could prove to be a very interesting one.

With Republicans taking control of both the House and the Senate, analysts are predicting an active year in Washington. Jason Furman, Chairman of President Obama’s Council of Economic Advisors, said, “There’s no reason why we can’t continue to have a strong economy in 2015” after coming off a year of solid economic performance marked by improvements in hiring, wages, and corporate investment. President Obama only has 24 months remaining—a short period of time for him to cement his legacy. Analysts feel that comprehensive tax reform, especially closing some loopholes and revamping corporate taxes, could prove to be a big win for investors. The U.S. political scene is another area investors need to pay attention to this year. (Source: Barron’s, 1/2015)

Conclusion: What Should an Investor Do?

Although the U.S. stock market isn’t filled with bargains, most analysts see the potential for U.S. stock market gains in 2015. Jurrien Timmer, Director of Global Macro in Fidelity’s Global Asset Allocation Division, encourages investors to “continue to view the U.S. market as the best house on the street. As we all know, the best house is usually the most expensive, and for good reason.” While many analysts are predicting growth for U.S. stocks, that growth might not come easily. In the last three years the S&P 500 has risen from a humble 11.7 times next-four-quarter earnings estimates to an ambitious 16.5 times. Investors might be best served structuring their portfolios to weather stock market turbulence. (Source: Barron’s, 12/2014)

Some analysts expect that the Fed might raise the short-term federal funds rate at mid-year, but not enough to destroy any good times for investors. Columbia Management’s Barry Knight reminds investors that “the case for higher interest rates is a little stronger than last year’” and he feels that getting the Fed’s moves right is the single most important factor in making an accurate market prediction for 2015.

Some analysts expect that the Fed might raise the short-term federal funds rate at mid-year, but not enough to destroy any good times for investors. Columbia Management’s Barry Knight reminds investors that “the case for higher interest rates is a little stronger than last year’” and he feels that getting the Fed’s moves right is the single most important factor in making an accurate market prediction for 2015.

So what can investors do?

Continue to be watchful. Perhaps some of the optimism can be attributed to holiday cheer; however, even the most optimistic need to be aware of some of the warning signs.

Long term investors should try to not change their outlooks based on short-term market forecasts. It might be in your best interest to prepare your portfolio for turbulence and focus on risk. Two of the questions investors need to ask themselves are:

- How much risk do I pose to my portfolio?

- How much risk do I need to take?

These are great starting places for investors for 2015. Generic and non-specific advice might not be best during volatile and confusing times.

Focus on your own personal objectives. During confusing times it is always wise to revisit your personal timelines. It is typically in your best interest to create realistic time horizons and return expectations for your own personal situation and to adjust your investments accordingly. For example, it’s important to consider your time horizon when looking at an investment. If you will need more cash flow from your investments over the next one to five years, you might consider different choices than someone with a ten-to-fifteen-year time horizon.

Understanding your personal commitments and categorizing your investments into near-term, short-term and longer-term can be helpful. We are skilled at this and are happy to help you.

Be cautious with income investments. While some income investors did well in 2014, this year the menu is less attractive. With the Federal Reserve and interest rates in the spotlight, this is a good time to understand your true income and cash flow needs. Again, this is one of our strengths and we are happy to provide you with help. To review your situation, either call our office or wait for your next review.

Don’t try to predict the market. Investment decisions driven by emotion can cause problems for investors. Vanguard Investments reminds us that in the face of market turmoil, some investors may find themselves making impulsive decisions or, conversely, becoming paralyzed, unable to implement an investment strategy or to rebalance a portfolio as needed. (Source: Vanguard.com, 2014)

Discipline and perspective can help investors remain committed to their long-term investment programs through periods of market uncertainty.

Discuss any concerns with us.

Our advice is not one-size-fits-all. We will always consider your feelings about risk and the markets and review your unique financial situation when making recommendations.

We strongly believe it is prudent for investors to work with an advisor who offers constant communication and frequent discussions, as well as one who is continually reviewing economic, tax and investment issues and drawing on that knowledge when offering direction and strategies to their clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy. Through changes in the aggregate market value of 500 stocks representing all major indices. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Sources: yahoo.com; Wall Street Journal, Barron’s; WealthManagement.com; Bloomberg.com; mic.com; forbes.com; businessinsider.com; thefiscal.times.com

© Academy of Preferred Financial Advisors, Inc.

CAS Rochester Volunteer Day – Fall Clean-up for Heritage Christian Services

Bundled up team members of CAS Rochester braved the cool temperatures and falling snow on November 13th to tackle fall clean-up of the yard of a Heritage Christian Services group residence. Spring cleanup of the same property was undertaken in May and included mulching, trimming, and weeding.

Bundled up team members of CAS Rochester braved the cool temperatures and falling snow on November 13th to tackle fall clean-up of the yard of a Heritage Christian Services group residence. Spring cleanup of the same property was undertaken in May and included mulching, trimming, and weeding.

The four-member fall team engaged in pruning, raking, and general winterizing in the morning. The timeliness of the outing was ironic. As the crew convened inside for a delicious lunch, snow descended on the leaf-free lawn!

CAS is proud to support the community in which we reside. We look forward to future outings that connect our team with those for whom assistance is greatly appreciated.

Deductions: Charitable Gifts

What is a charitable gift?

A charitable gift is a contribution of cash or property to, or for the use of, a qualified charity. A gift is “for the use of” an organization when it’s held in a legally enforceable trust for the qualified organization or in a similar legal arrangement. Americans give billions of dollars to charities each year, partly because charitable donations are tax deductible. To receive a tax deduction for your gift, you must itemize your deductions and make the gift to a qualified organization, not to a specific person. For example, a gift that’s for the benefit of an individual flood victim isn’t deductible, but a gift to a qualified organization that helps flood victims generally is deductible.

Tip: For tax years prior to 2014, persons aged 70½ and older can exclude from their gross income qualified charitable distributions of up to $100,000 a year from a traditional IRA or a Roth IRA. Distributions must be made directly from the IRA to the charity, and all the usual requirements for charitable deductions must be met.

Tip: To deduct a charitable contribution, you must file Form 1040 and itemize deductions on Schedule A.

What is a qualified organization?

In general:

Not all contributions to tax-exempt organizations are tax-deductible. Instead, the contribution must be to a qualified organization. Churches, synagogues, temples, mosques, and governments automatically get qualified organization status. Other organizations must apply to the IRS, which provides data on eligible organizations on its website (www.irs.gov) through its Exempt Organizations Select Check tool. The list maintained by the IRS, however, is not all-inclusive (i.e., there are some qualified organizations for which the deductions are tax deductible that aren’t yet on the list). If you want to donate to a charity but you’re not sure if it’s a qualified organization, ask the charity or the IRS.

Five specific types of qualified organizations:

- Any community chest, corporation, trust, fund, or foundation organized or created in or under the laws of the United States, any state, the District of Columbia, or any U.S. possession and operated solely for religious, charitable, educational, scientific, or literary purposes or for the prevention of cruelty to children or animals. For example, organizations such as the Red Cross, the United Way, and the Salvation Army fall within this category, as does the National Park Foundation.

- War veterans’ organizations, including posts, auxiliaries, trusts, or foundations organized in the United States or its possessions.

- Domestic fraternal societies, orders, and associations operating under the lodge system–if your contribution is to be used solely for charitable, religious, scientific, literary, or educational purposes or for the prevention of cruelty to children or animals.

- Certain nonprofit cemetery companies or corporations–if your contribution is not to be used for the care of a specific lot or mausoleum crypt.

- The United States or any state, the District of Columbia, a U.S. possession, a political subdivision of a state or U.S. possession, or an Indian tribal government or any of its subdivisions that performs a substantial government function–if the contribution is to be used solely for public purposes.

Charitable contributions in general

Generally, you can deduct a contribution of money or property that you make to, or for the use of, a qualified organization. The amount that you can deduct in any given year is limited to a specific percentage of your adjusted gross income (AGI), as discussed in the following sections. If you receive a benefit as a result of making a contribution, you can deduct only the amount of your contribution that exceeds the value of the benefit received.

You may deduct your entire payment to a charity if you receive only a token item in return and the charity correctly tells you (1) that the item’s value isn’t substantial, and (2) that you can deduct your full payment.

If you make a contribution to a college or university and as a result receive the right to buy tickets to an athletic event in the facility’s athletic stadium, you can deduct 80 percent of your payment as a charitable contribution.

Limits based on adjusted gross income (AGI)

Deductions limited to 50 percent of adjusted gross income (AGI)

Your deduction for charitable contributions cannot amount to more than 50 percent of your AGI for the year, and lower percentage limits can apply, depending on the type of property that you give and the type of organization to which you contribute. The 50 percent limit applies to gifts you make to qualified organizations that are public charities or private operating foundations, such as churches, certain educational organizations, hospitals, and certain medical research organizations associated with the hospitals. Most organizations can tell you whether or not they are 50 percent limit organizations.

Deductions limited to 30 percent of adjusted gross income (AGI)

- Your deduction for charitable contributions made to organizations that are not 50 percent limit organizations (see above) cannot be more than 30 percent of your AGI for the year. Organizations that are not considered 50 percent limit organizations include veterans’ organizations, fraternal societies, nonprofit cemeteries, and certain private nonoperating foundations.

- In addition, if you make a charitable contribution for the use of any organization (e.g., you make a gift in trust), as compared with an outright gift, your deduction is limited to 30 percent of your AGI.

- Capital gain property (property that would have resulted in realized long-term capital gains if sold) given to a 50 percent limit organization is also subject to the 30 percent limit.

Caution: The 30 percent limit does not apply when you choose to reduce the fair market value (FMV) of the property by the amount that represents the long-term gain that would result if you sold the property. In this case, the 50 percent limit applies.

Deductions limited to 20 percent of adjusted gross income

All gifts of capital gain property, to or for the use of organizations that are not 50 percent limit organizations, are limited to 20 percent of your AGI.

Five-year carryover of unused charitable deductions

You can carry over your contributions that you aren’t able to deduct in the current year because they exceed your AGI limits. You can deduct this carryover amount until it is used up but not beyond five years. The same AGI percentage limitations that apply in the year the deduction originated will apply in the year(s) to which it is carried. So, for example, contributions subject to a 20 percent AGI limitation this year will be subject to a 20 percent AGI limitation if carried forward to a future year.

Caution: Special rules apply if you use the standard deduction (rather than itemizing) in any of the years in which you carry forward unused charitable deductions. Essentially, the carryover amount must be reduced by the amount that you would have been able to deduct had you itemized.

Example(s): Jack’s AGI for the current tax year is $50,000. In August of the current tax year, he gave his church $2,000 in cash (a 50 percent charity). He also gave his church land with an FMV of $30,000 and a basis of $22,000. The land was held for investment for more than 12 months. The donation of the land is subject to the special 30 percent limitation. He also gave $5,000 of capital gain property to a private foundation that is a non-50 percent charity. The $5,000 contribution is subject to the 20 percent limitation.

Example(s): Jack’s charitable contribution deduction is computed as follows: The total charitable contribution deduction can’t exceed $25,000 (50 percent of $50,000). The cash contribution is considered first, since Jack made it to a 50 percent charity. Other charitable contributions are considered in the following order, not to exceed 50 percent of AGI in the aggregate:

- Contributions of noncapital gain property to non-50 percent charities, to the extent of the lesser of: (a) 30 percent of AGI, or (b) 50 percent of AGI reduced by all contributions to 50 percent charities.

- Contributions of capital gain property to 50 percent charities, up to 30 percent of AGI.

- Contributions of capital gain property to non-50 percent charities, to the extent of the lesser of: (a) 20 percent of AGI, or (b) 30 percent of AGI less contributions of capital gain property to 50 percent charities.

Example(s): Jack’s donation of land to the church is subject to the special 30 percent of AGI limit described in item 2. It is included at FMV ($30,000) in applying the 30 percent limitation. Therefore, Jack can deduct a maximum of $15,000 (30 percent of $50,000 AGI) for the donation of the land. The unused special 30 percent contribution ($15,000) may be carried over to later years. The $5,000 contribution to the private foundation is nondeductible because of the limitation described in item 3 [(30 percent of $50,000 AGI) – $30,000 contribution of land = 0] and carries over to the following tax year.

Example(s): Therefore, Jack’s current tax year deduction is limited to $17,000 ($2,000 + $15,000). The aggregate 50 percent limitation wasn’t reached. Both carryovers continue to be subject to the special 30 percent and 20 percent limits, respectively.

What if you give property instead of cash?

You generally can deduct the fair market value (FMV) of the property at the time you give it to the charity. FMV is the price a willing seller receives from a willing buyer for the property, with both knowing relevant facts about the property. If the property has gone up in value since you purchased it, you may have to make an adjustment to the amount of your deduction (generally this is true if, had you sold the property, you would have recognized ordinary income or short-term capital gain–in such a case, the amount you can deduct may be limited to FMV less the amount that would have been ordinary income or short-term capital gain if you had sold the property). If the property has decreased in value, you may deduct its FMV. IRS Publication 561 (Determining the Value of Donated Property) can help you to determine FMV.

Caution: An accurate assessment is important because you may be liable for a special penalty if you overstate the value of donated property and underpay your tax by more than $5,000 due to the overstatement.

In general, you cannot deduct a charitable contribution of less than your entire interest in property. That normally includes a contribution of the right to use your property (since that represents less than your entire interest in the property). There are exceptions to the partial interest rule, however, including the donation of a remainder interest in your home.

If you contribute property that’s subject to a debt or mortgage, for purposes of calculating your deduction you generally have to reduce the FMV of the property by any allowable deduction for interest you have paid (or will pay) that is attributable to any period after the contribution. (This prevents you from taking the same amount as both an interest deduction and a charitable deduction.)

Special rules apply to the contribution of certain types of property, including clothing and household items, as well as cars, boats, and airplanes. For example, you cannot take a deduction for clothing or household items donated unless the clothing or household items are in good used condition or better. However, an exception exists if you claim more than $500 for an individual item and include a qualified appraisal with your return.

If you donate a patent or other intellectual property, your deduction is limited to the basis of the property or the FMV of the property, whichever is less. You also may be able to claim additional charitable contribution deductions in the year of the contribution and years following, based on any income generated by the donated property. Your ability to claim additional deductions based on the earnings of the donated intellectual property is subject to limitation, and is phased out over a 12-year period. Consult a tax professional.

Can you deduct your out-of-pocket expenses?

If you incur expenses while providing services to a qualified organization, you may generally deduct unreimbursed amounts that are directly connected with the services you provided. For example, you may deduct the cost and upkeep of uniforms that you must wear while performing charitable services if the uniforms aren’t appropriate for everyday use. You can also deduct car expenses, such as gas and oil, if they’re directly related to using your car to provide services and you can provide reliable written records of your expenses. Instead of deducting actual expenses, you can choose to deduct a standard mileage rate of 14 cents per mile. You can also deduct parking and tolls. Depreciation and insurance are not deductible.

If you travel away from home to perform services as a chosen representative for the qualified charity, you can deduct the expenses you incur if there’s no significant element of personal pleasure, recreation, or vacation in the travel. This doesn’t mean you can’t enjoy yourself while providing charitable services. It does mean, however, that you can’t deduct the expenses of a Caribbean cruise just because you provide nominal charitable services while on the boat. If you receive a daily allowance from the charity to cover your reasonable travel expenses, you must include in your income the amount of that allowance that is more than your deductible travel expenses. You may still be able to deduct the amount you spend over the allowance. Deductible travel expenses include air, rail, or bus transportation; out-of-pocket expenses for your car; transportation between the airport or station and your hotel; lodging costs; and the cost of meals.

What kinds of contributions aren’t deductible?

In general, the following cannot be deducted as charitable contributions:

- A contribution to a specific person –You may deduct a donation to a qualified organization that provides aid to the homeless but not a donation to a homeless person you encounter on the street.

- A contribution to a non-qualified organization –The organization must meet IRS criteria of a qualified organization.

- Any part of your contribution from which you receive or expect to receive a benefit –You can deduct only the amount of your donation that exceeds the value of the benefit you receive. If you pay more than FMV to a charity for merchandise, goods, or services, you may deduct the amount you pay that’s more than the value of the item if you pay it with the intent to make a charitable contribution. (You may deduct your entire payment to a charity if you receive only a token item and the charity correctly tells you (1) that the item’s value isn’t substantial, and (2) that you can deduct your full payment.)

- The value of your time or services –You may deduct unreimbursed amounts that are directly connected with the services you provide and which you incurred only because of the services you gave, but you may not deduct the value of your time or services.

- Your personal expenses –You may not deduct expenses that are your personal, living, or family expenses.

- Certain contributions of partial interests in property –Generally, you may not deduct a transfer of a partial interest in property to a qualified organization. There are some exceptions to the general rule, however, including a contribution of a remainder interest in your personal home or farm; an undivided part of your entire interest; a partial interest that would be deductible if transferred to certain types of trusts; and a qualified conservation contribution.

Qualified conservation contributions

In general, the charitable contribution of a partial interest in property is not deductible. A qualified conservation contribution is an exception to this rule. A qualified conservation contribution is a contribution of a qualified real property interest to a qualified organization exclusively for conservation purposes.

Technical Note: A qualified real property interest is (1) the entire interest of the donor other than a qualified mineral interest, (2) a remainder interest, or (3) a restriction (granted in perpetuity) on the use that may be made of the real property.

Technical Note: Qualified organizations include certain governmental units, public charities that meet certain public support tests, and certain supporting organizations.

Technical Note: Conservation purposes include (1) the preservation of land areas for outdoor recreation by, or for the education of, the general public; (2) the protection of a relatively natural habitat of fish, wildlife, or plants, or similar ecosystem; (3) the preservation of open space (including farmland and forest land) where such preservation will yield a significant public benefit and is either for the scenic enjoyment of the general public or pursuant to a clearly delineated Federal, State, or local governmental conservation policy; and (4) the preservation of an historically important land area or a certified historic structure.

Qualified conservation contributions of capital gain property are generally subject to the same limitations and carryover rules as other charitable contributions of capital gain property (i.e., a related deduction would generally be subject to a 30-percent AGI limitation). However, special rules apply to qualified conservation contributions made prior to tax year 2014.

Under the special rules, the 30-percent AGI limitation that applies to contributions of capital gain property does not apply to qualified conservation contributions. Instead, individuals may deduct the fair market value of any qualified conservation contribution, up to 50 percent (100 percent for qualified farmers and ranchers) of AGI reduced by the total deduction for all other allowable charitable contributions. Qualified conservation contributions are not taken into account in determining the amount of other allowable charitable contributions. Individuals are allowed to carry over any qualified conservation contributions that exceed the AGI limitation for up to 15 years.

Can you deduct the costs of having a foreign exchange student live with you?

Yes. If you meet the criteria, you can deduct qualifying expenses for a foreign or American exchange student. The student must:

- Live in your home under a written agreement between you and a charity as part of a program to provide educational opportunities for the student

- Not be your dependent or relative

- Be a full-time student in the 12th grade or lower at a U.S. school

You can deduct up to $50 per month for each month the student lives with you at least 15 days. Qualifying expenses include books, tuition, food, clothing, transportation, medical and dental care, entertainment, and other amounts you actually spent for the well-being of the student. You may not deduct expenses such as home depreciation, lodging, and general household expenses. You also may not deduct expenses if the student is living with you under a mutual exchange program whereby your child will live with a family in a foreign country.

Record keeping

Cash contributions

For your cash contributions, regardless of the amount, you must keep either a bank record (e.g., cancelled check, credit card statement) or a written communication (receipt or letter) from the charitable organization that shows (1) the name of the charitable organization, (2) the date of the contribution, and (3) the amount of the contribution. If you make a charitable contribution through payroll deduction, you must keep a pay stub, W-2, or other documentation from your employer showing the date and amount of contribution, and a pledge card or other documentation from the qualified organization.

If you claim a deduction for a contribution of $250 or more, you must have an acknowledgment of your contribution from the qualified organization (or certain payroll deduction records). The acknowledgment:

- Must be written

- Must include the amount of cash you contributed; whether the organization provided goods or services as a result of your contribution (and an estimate of the value of such goods or services); and a statement that the only benefit you received was an intangible religious benefit, if that was the case

- Must be in your possession on or before the earlier of the date you file your return for the year you make the contribution, or the due date, including extensions, for filing the return

If the acknowledgment does not show the date of the contribution, you will also need a bank record or receipt that shows when the contribution was made.

A noncash contribution under $250

To deduct a noncash contribution under $250, you must get a receipt from the organization that includes your name, the date, the location of the organization, and a reasonably detailed description of the property. You must also have reliable written records for each item you donated. You are not required to get a written receipt when it is impractical to get one (e.g., at an unattended drop-off site).

A noncash contribution between $250 and $500

You need a receipt like the one required for a noncash contribution under $250, but it must also include details on whether the charity gave you any substantial goods or services for your contribution, as well as a description and good faith estimate of the value of any goods or services you received. You have to get this receipt on or before the earlier of the date you file your return or the due date (including extensions) for filing the return.

A noncash contribution between $500 and $5,000

You need a receipt that includes details on whether the charity gave you any substantial goods or services for your contribution and a description and good faith estimate of the value of any goods or services you received. Additionally, your records must include how and when you got the property and how much you paid for it. You must also complete Form 8283, Noncash Charitable Contributions, and attach it to your return.

A noncash contribution over $5,000

You need a receipt and records like those required for noncash contributions between $500 and $5,000, but you also need a qualified written appraisal of the property from a qualified appraiser. Appraisal fees incurred in determining FMV of donated property are not part of a charitable contribution but can be deducted as a miscellaneous deduction on Schedule A.

Technical Note: The IRS defines a qualified appraiser as an individual who (1) has earned an appraisal designation from a recognized professional appraisal organization or has otherwise met minimum education and experience requirements, (2) regularly performs appraisals for which he or she receives compensation, (3) can demonstrate verifiable education and experience in valuing the type of property for which the appraisal is being made, (4) has not been prohibited from practicing before the IRS at any time during the three years preceding the appraisal, and (5) is not excluded from being a qualified appraiser under Treasury regulations.

A noncash contribution over $500,000

If you claim a deduction of more than $500,000 for a contribution of property, you must attach a qualified appraisal of the property to your return. If you do not attach the appraisal, you cannot deduct your contribution. This does not apply to contributions of cash, inventory, publicly traded stock, or intellectual property.

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014

Key Numbers 2015: Tax reference numbers at a glance

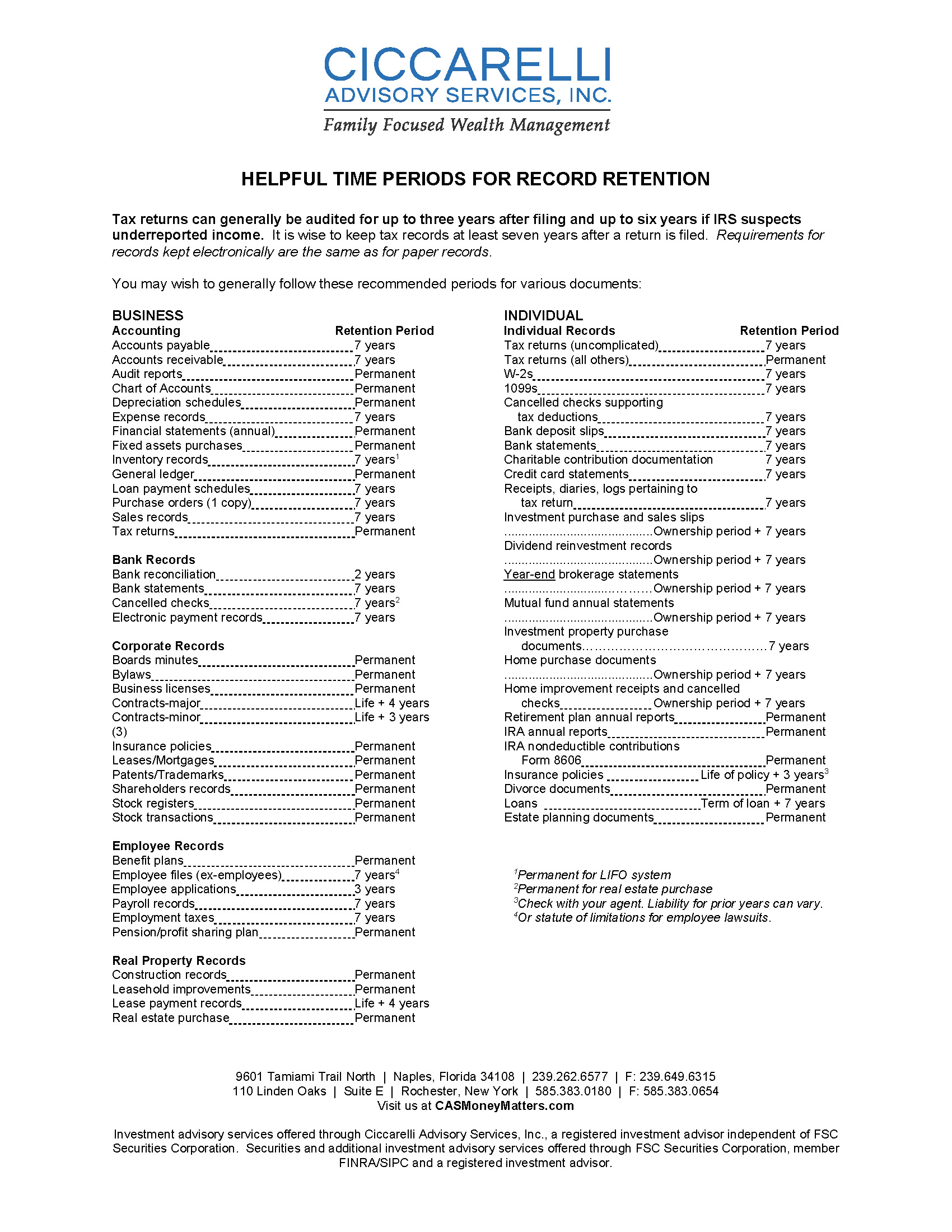

Helpful Time Periods for Record Retention

Tax returns can generally be audited for up to three years after filing and up to six years if the IRS suspects under-reported income. It is wise to keep tax records at least seven years after a return is filed. Requirements for records kept electronically are the same as for paper records.

You may wish to generally follow these recommended periods for various documents…

For a printer friendly version, CLICK HERE

Naples Depot “Ticket-to-the-Past” Event

Turning Complex Strategies into Universal Language the Whole Family Can Understand

Jill Ciccarelli Rapps | Life in Naples Magazine

Jill Ciccarelli Rapps | Life in Naples Magazine

Just as each of us has unique characteristics, we also have our own language. A way of organizing thoughts and communicating that makes sense to us based on our perception of the world. This makes financial communication somewhat challenging between family members. One hurdle is with spousal communication, or should I say, the lack of communication regarding financial strategies. We hear typical responses: “Oh my spouse does that, I don’t have to worry”, or “I don’t want to even discuss my spouse not having the ability to manage our affairs”. Unfortunately, these responses usually do not lead to a happy ending. Many people wonder how their children will handle their inheritance, and alternatively children are asking, “I wonder if my parents have all their finances in order?”

The first suggestion, deal with this problem head on. Get your financials in order, but in a manner the whole family can understand, not just in your language. Start with a balance sheet listing all your assets with account numbers, how they are owned, and a most recent valuation. Most of the time doing this exercise uncovers issues that need to be addressed. Most people think that their wills or trusts control who will get what when they die. Surprisingly, many assets are transferred based on provisions which can contradict but supersede your will or trust. Be sure your financial advisor and/or your estate planning attorney review all the titling of your assets to be sure they align with your estate plan. All too often, mistakes are uncovered that can cause the family unnecessary taxes and financial losses as well as a significant amount of grief.

Creating a visual flowchart of estate documents, financial assets, and cash flow for the family is most useful. Who has time to read through estate documents, and for that matter, understand legalese? Imagine taking the complex details and creating a visual that your spouse, family, or trustee can use to easily understand the foundation of your strategic financial and estate plan in just minutes!

So where do you keep all this? Somewhere easily accessible by family members, or whomever you named to step up for you. Here in Florida, if you keep everything in a safe deposit box but you do not have an additional signor besides your spouse, it will be difficult and time consuming for someone to access your documents quickly.

Once you have things organized, don’t forget you need to communicate what you think is important for your family to know. One of the most effective ways to do this is to “call to order” a family meeting. Remember you can communicate as little or as much as you see fit, showing asset valuations or not. Have a third party involved who can facilitate the meeting with your family. The facilitator may also help with ideas and best practices so the entire family walks away with a great experience. This will bring your family communication to a whole new level and it may also enhance your planning significantly, in ways you never imagined. In my next article, I will address the power of family meetings, and share ideas you may incorporate to get started. Until then, start by re-examining the way you document your financial and estate planning strategies and ensure they are in a format the whole family can understand.

The views expressed in this article may not reflect the views of FSC Securities Corporation. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice.

The Enduring Gift

Jill Ciccarelli Rapps | Life in Naples Magazine

Don’t spoil your children and grandchildren, help them on their way to financial security with a gift that will last a lifetime and beyond.

A newborn baby may not be able to read the financial journals, but you can give them a head start by opening a savings account with a small gift or an education account that may be tax deferred and tax free for their education. By adding just $100 per month at a hypothetical return of 6 percent, at age twenty it would be worth $45,665 and at age fifty it would be worth $359,725. Supplement this gift with something tangible like a multi- purpose “piggy bank” where a young child can learn good financial habits early. They will have fun deciding where to save their change – towards their education, savings, charity, or fun! Why shouldn’t every newborn be given this opportunity?

As children start to earn wages, a Roth IRA account is a fabulous idea to start building savings for their future. With a Roth account, up to $5,000 or all earnings, whichever is the least amount, can be deposited each year. A great idea is to match whatever they can save into their accounts. At this age, they should participate in their investments; pay them to do research, read selective books, and write reports on financial subjects you think are important for them to know. The key at this age is encouraging them to “pay themselves first” – to save a portion of every dollar that comes their way.

For children who are 40 and over, it is not too late! Consider paying for a gift of a financial checkup – this will allow them to work with a financial planner who will help them put the necessary planning in place today and for their future. It is a great way to keep their privacy, while feeling comfortable they are getting the right guidance. At this age, make gifts with a purpose, like setting aside savings for a health care account, paying for a long-term care policy or setting up an account that can supplement their retirement.

Speak with your advisor to decide what kind of gifts can have the most significant impact on each of your family members.

The holidays are around the corner; why not make a gift to last a lifetime and beyond to your children and your grandchildren today?