CAS News

Interest Rates Decrease Slightly on Federal Student Loans

Each year, thousands of students take out federal loans to help pay for college or graduate school. The interest rates on federal student loans are fixed for the life of the loan but reset each year on July 1 for new loans. This year, there’s some good news for students and parents. Rates on new loans issued during this academic year–July 1, 2015, through June 30, 2016–are slightly lower than they were for the 2014/2015 academic year.

Each year, thousands of students take out federal loans to help pay for college or graduate school. The interest rates on federal student loans are fixed for the life of the loan but reset each year on July 1 for new loans. This year, there’s some good news for students and parents. Rates on new loans issued during this academic year–July 1, 2015, through June 30, 2016–are slightly lower than they were for the 2014/2015 academic year.

The federal government pays the interest on subsidized Stafford Loans while the student is in school, during the six-month grace period after graduation, and during any loan deferment periods. With unsubsidized Stafford Loans, the student pays the interest during these periods. Eligibility for subsidized Stafford Loans is based on financial need, as determined by the federal government’s financial aid application, the FAFSA. Graduate students aren’t eligible for subsidized Stafford Loans.

©2015 Broadridge Investor Communication Solutions, Inc.

Identify and Avoid Phone Scams

By Carrie Kerskie, Kerskie Group, Inc.

By Carrie Kerskie, Kerskie Group, Inc.

In the age of technology scammers still rely on good-old-fashioned methods to steal your money or your personal information. One of these methods is the phone scam.

The greatest warning sign of a phone scam is the fact that it is an unsolicited phone call, a call that you did not initiate or were not expecting, often from someone that you do not know. However, scammers will pretend to be calling from a well known organization for instant credibility. To help you determine the legitimacy of a call here are a few common phone scams.

Travel scam: Unsolicited calls offering you “free” or “low cost” vacations are a scam. Often these vacations end up having numerous hidden fees or you could end up paying for a vacation that does not exist.

Credit and loans: Unsolicited offers to lower your credit score, payday loans, advance fee loans or credit card protection are all scams. These types of phone scams are typical during a down economy. They will promise a service in exchange for paying them a fee. You pay the fee but the service is never rendered. Or you provide them with your credit card and bank account information so they can “help” you but they only help themselves to using your accounts.

Business and investment opportunities: Unsolicited offers for business or investment opportunities are a scam. Scammers are relying on the fact that business and investing can be complicated and that most people do not research the investment. The caller will sound very professional and convincing, promising you a guaranteed return on your investment. The only thing that is guaranteed is that you will never see your money again.

Charitable causes: Unsolicited requests for recent disaster relief or donations to well known charities are scams. These scams are successful because they tug the heart-strings. Unfortunately it is difficult to determine if the caller is actually with the stated charity or if he is merely using it as a front to steal your money or information. You are better off contacting the charitable organizations that you know directly to make a donation as opposed to making a donation through an unsolicited call.

Lottery or prize winner: Unsolicited calls notifying you of winning a lottery in which you did not actively participate is a sure sign of a scam. Further, participation in foreign lotteries is illegal. Callers will often state that you are required to pay a fee or tax before they can send you your prize. Or they will ask you for your bank routing and account information so they can wire you the prize. ALL OF THESE ARE SCAMS.

Extended car warranties: Unsolicited calls selling you an extended car warranty are scams. Scammers can easily find out what kind of car your drive and when you bought it. Both of these are used to gain your trust so they can urge you to buy an overpriced, or worthless, extended warranty.

Extended car warranties: Unsolicited calls selling you an extended car warranty are scams. Scammers can easily find out what kind of car your drive and when you bought it. Both of these are used to gain your trust so they can urge you to buy an overpriced, or worthless, extended warranty.

“Free” trial offers: Unsolicited calls regarding “free” trial offers are a scam. These companies use the free trial offer to sign you up for products which cost you lots of money. What they neglect to tell you is that when the free trial period ends you will be billed every month until you cancel. They will also make it very difficult for you to cancel the service.

Owe money or arrested: Unsolicited calls stating that you owe money and if you do not pay immediately an arrest warrant will be issued are scams. These are the worst type of call as they use fear and intimidation to coerce you in to complying with their request. Scammers will often claim to be with the IRS or some other governmental agency. This is done to instill fear. When you begin to question them they become aggressive and threaten to have you arrested.

What Can You Do

Your best defense is to simply hang up the phone. You do not owe them your time or an explanation. You do not have to be nice to them or worry about hurting their feelings. They are professional scammers. Their only goal is to steal from you. The more you try to tell them “no” the harder they will pressure you. If you consistently hang up the phone the scammers will move on to an easier target, one that will play their game.

After receiving a scam call you should tell someone. This could be your local law enforcement, a relative, or a trusted advisor. By telling someone you help warn others about the scam so they too can be prepared. Sometimes, if law enforcement receives enough complaints about a scam call they will notify the public through the media.

Still Not Sure

If you are still not sure if the call you received was legitimate or a scam here are a few things to remember.

- An unsolicited call is often the first warning sign of a scam.

- The IRS will NEVER call you regarding owed taxes.

- Was there a sense or urgency, you must do it now or else? This is a favored tactic of scammers. Take your time, ask a trusted advisor before sending money or agreeing to an offer.

- If someone threatens you with arrest, contact local law enforcement immediately.

- Caller ID can be manipulated to display whatever the caller wants it to display.

- If the call is claiming to be from your bank or a company you do business with hang up and call the business directly. NOTE: Do not call the number shown on your caller ID.

- Scammers can build a profile on you from public records found online.

- Speak with your financial advisor about business or investment offers. That is why you have him or her.

- IF IT SOUNDS TOO GOOD TO BE TRUE, IT IS A SCAM.

There is a reason phone scams have been around since the invention of the telephone – they work and are very profitable. In this day and age we can no longer trust then verify. We must verify, verify again, and verify again before even thinking about trusting or your too will become the next victim of a phone scam. You have the right to ask questions, or better yet, simply hang up the phone.

Carrie Kerskie and Kerskie Group, Inc. are not affiliated with FSC Securities Corporation. Published with permission.

Backdoor Roth Unveiled

Steven R. Merkel, CFP®, ChFC® | Life in Naples Magazine | August 2015

Steven R. Merkel, CFP®, ChFC® | Life in Naples Magazine | August 2015

Without hesitation, most financial professionals will unarguably agree that the Roth IRA is hands down the best individual retirement arrangement on the planet. Benefits such as tax-free growth, no RMD requirements at age 70 ½, and penalty-free early withdrawal of principal are just a few of the many benefits.

To date, it is the only IRA retirement plan that offers 100% tax-free withdrawals of principal and earnings after age 59 ½, provided that the Roth was established for at least five years before the distribution occurs. Why wouldn’t everyone have one?

Limitations and Restrictions

Eligibility to contribute directly to a Roth IRA is phased out at certain modified adjusted gross income (MAGI) levels. Roth contribution eligibility (indexed for 2015) ends at MAGI limits for single tax filers at $131,000 and $193,000 for those married filing jointly. If you have earned income under these MAGI levels, you can contribute directly to a Roth for both you and your spouse – at a maximum of $5,500 each per year or $6,500 if you’re age 50 or older.

In 2010, the government removed the $100,000 income limitation for Roth conversions. Roth conversions allow taxpayers to convert full or partial Traditional IRA funds (both deductible and non-deductible) to Roth IRAs by paying tax on the untaxed amount converted in the year of conversion. The removal of this rule also opened up some amazing strategic planning opportunities for both low and high-income earners.

Backdoor Roth

If your earned income MAGI exceeds the direct contribution limits to the Roth IRA, there’s still a possible solution for you. The IRA rules allow those individuals that can no longer benefit from deductible IRA contributions to make non-deductible contributions to a Traditional IRA (make sure your CPA files Form 8606 with your tax return to acknowledge the non-deductible contribution). Immediately after your contribution posts to your non-deductible IRA, you should convert the funds to your Roth IRA account. Presto… you now have a Roth IRA and you converted it without paying any tax!

How? There were no earnings in the non-deductible Traditional IRA at the time of conversion and you never took any tax deduction for the contribution, so there was nothing new there for the IRS to tax since your initial contribution was comprised of after-tax dollars.

Watch out for the Pro-Rata Rule

The catch to this strategy is if you already have existing IRA accounts. In this case, the IRS would look at the aggregate value of all of your Traditional IRA accounts and tax the amount of your conversion based as a percentage of the overall value of all of your IRA accounts. This is not the best scenario because you would still owe some tax on the conversion amount based on the pro-rata formula. If conversion still interests you, keep in mind that you do not have to convert the entire IRA to a Roth in the same tax year, so many individuals are still able to spread the tax consequence over several years by only converting a partial amount of their deductible (taxable) IRAs each year.

Avoiding the Pro-Rata Rule

Should you desire to reduce your pre-tax IRA values to zero in order to avoid paying tax on the conversion amount, you could consider rolling over your IRA accounts into a 401K plan prior to opening a non-deductible IRA. Since many employers do not allow outside pre-tax IRA monies to rollover into their plan, if you have self-employment or 1099 income, consider opening a Uni or Solo 401K to rollover the funds. If you get your aggregate IRA values down to zero, you can then utilize the Backdoor Roth with no tax due.

The Backdoor Roth is an excellent strategy if you do not have any existing pre-tax Traditional IRA accounts or you’re able to roll over those funds into a 401K account. The ability to convert non-deductible IRA funds to a Roth IRA tax-free is an amazing tax and investment strategy that can provide family generations of tax-free earnings and distributions. There’s no other product out there like it. Even retirees with no earned income may want to consider partial Roth conversions (paying tax now on the conversion amount of course).

So what are you waiting for? Contact your financial planner today to fully understand your personal tax situation and then get the ball rolling on this incredible opportunity before the IRS fully catches on and makes changes to the tax code.

A Roth IRA distribution is qualified if you’ve had the account for at least five years and/or the distribution is made after you’ve reached age 59½, due to total and permanent disability, in the event of your death or for first-time homebuyer expenses. Distributions made prior to age 59 1/2 may be subject to a federal income tax penalty. If converting a traditional IRA to a Roth IRA, you will owe ordinary income taxes on any previously deducted traditional IRA contributions and on all earnings. A conversion may place you in a higher tax bracket than you are in now. Since Roth IRA conversions may not be appropriate for all investors and individual situations vary we suggest that you discuss tax issues with a qualified tax advisor. There are several choices investors have when rolling over money from one plan to another. Since each choice has its own implications, it is recommended that you discuss and compare all potential fees, expenses, commissions, taxes, and legal ramifications with your qualified advisor before making a rollover decision.

Record Retention: Deciding Which Financial Records to Keep

Keep critical documents and records safe and secure but accessible in a time of need

Certain documents and records are too important to retain in an ordinary file drawer. Fortunately, they are also the ones you tend to need least frequently. If they are stolen or destroyed by a catastrophe such as flood or fire, replacing them could be extraordinarily difficult, if not impossible. One of the best places to retain such items is a safety deposit box. These can be rented for a small monthly fee at many banks. The boxes are actually locked drawers within the bank’s vault. Various sizes are often available to meet individual needs. A home safe is another option, provided that it is adequately rated to protect contents from fire, water, explosions (gas leaks), and other calamities. Documents deserving extra protection include:

- Property deeds

- Trust documents

- Insurance policies

- Automobile titles

- Stock and bond certificates

- Wills and estate plans

- Personal property inventory

- Marriage and birth certificates

- Military discharge papers

- Passports

Keeping copies of vital records can save time, money, and headaches

There may be times when you need to know certain information contained on documents you’ve placed in safekeeping but don’t need the actual document. Avoid the inconvenience of obtaining the original documents by making copies of them for your file.

Tip: Create one file that includes copies of all documents you’ve placed in safekeeping (e.g., a “Safety Deposit Box” file). Then, you not only can turn to it for vital facts, but if you are incapacitated, whoever handles your important affairs will be able to locate key documents quickly.

Caution: The specific contents of some documents, such as wills and trusts, may be inappropriate to keep in more highly accessible home files. Instead of a photocopy, you might simply file a page containing those key facts that are less confidential in nature or obliterate very sensitive items on the copy.

Make backup copies of all computerized records

These days, many people keep important records on their personal computer. This can be an easy way to keep your records organized and updated, but it is important to keep a backup copy of these records in a safe place. If your hard drive has a meltdown, you’ll need to be able to recreate the important financial information that was lost.

Financial management software can be beneficial in tracking your finances, but it will take some time to learn how to use it properly. Don’t forget that you must still retain original documents as evidence of past transactions.

Save all essential records, receipts, and documents that your budgeting system requires

There are many reasons to save important records. If you apply for a loan (such as a mortgage, auto loan, or education loan), you will have to provide proof of your income. If you notice that money is disappearing out of your checking account, you’ll need your bank statements to back up your claim of unauthorized transactions. If you own financial securities, capital gains taxes are based on the price you paid for them on the date purchased. You’ll be required to verify this information. Potential tax audits will be far less intimidating if you have kept records to substantiate your tax return claims. An unsubstantiated claim will cost you not only the unpaid tax but interest charges and possibly, a hefty penalty.

Tip: Most of us realize it’s important to keep expense records, but for those with income sources other than employers, a cash receipts log can be invaluable. A small notebook or a few sheets in a separate file folder will do for recording income as it arrives. If you don’t recall later whether you received a particular dividend or rent payment, the log provides a quick answer.

Caution: Certain items, such as tips or business-related use of a car, require special tax treatment and records. Therefore, your record-keeping system must track these and retain any related documents.

Keep records as long as appropriate

Different records need to be saved for different periods of time. Divide your records into categories, such as short-term, medium-term, and long-term. There are no concrete rules about how long records must be saved, so you will often have to use your own judgment. The following guidelines may help:

Short-term (1-3 years)

- Household bills, except those that support tax deductions (items such as heat, water, and electricity are generally short-term unless you deduct them for home office use or a rental)

- Expired insurance policies

Medium-term (6-7 years)

- Tax returns and supporting information

- Income and expense records (including lottery tickets and winnings)

- Bank and credit union statements

- Brokerage house statements

- Canceled checks and check registers (checks for major purchases may be kept longer)

- Paid-off loan documents

- Personal property sales receipts

Long-term (indefinitely)

- Tax dispute records

- Evidence of retirement plan contributions

- Investment records

- Medical history information

- Pension/retirement plan documents

- Social Security information

Other (as noted)

- Home ownership/sale documents: 7 years after sale or indefinitely

- Home improvement records: 7 years after sale

Caution: The IRS typically has three years after a return is filed to audit a return, or two years after you’ve paid the tax, whichever is later. However, if income was underreported by at least 25 percent, the IRS can look back six years after the return is filed, and there is no time limit for fraudulent tax returns. An audit requires that you provide documentation to substantiate the return being audited.

Tip: Canceled checks do not necessarily prove why a given payment was made, only that the payment was made. Having dated receipts, invoices, sales slips, credit card statements, and bank statements can provide valuable proof if needed, whether for an IRS auditor or an insurance claims adjuster.

Save space: Annually review retained records and discard those no longer needed

Some records and documents can be discarded after all potential usefulness has passed. Depending on circumstances, records can accumulate quickly and require extensive storage space. Discarding records that are no longer necessary saves space and makes finding a record you need easier.

Tip: Expired product warranties and insurance policies are excellent candidates for the trash can.

Tip: For easier future access, retain records for each year in separate files.

Caution: Keep your important records and financial files separate from information you might want to retain for other purposes. If you clip articles, jot notes, and save information you receive on items of potential interest, create a separate set of information files for them. These might contain vacation ideas, recipes, home improvement items, personal letters, or the kids’ school papers. Keeping them apart from vital records and financial files makes both easier to find and manage.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2015.

Ciccarelli Advisory Services, Inc. Selected as a Finalist for “Florida Companies to Watch”

We are proud to announce that Ciccarelli Advisory Services, Inc. was selected as one of four companies in Collier County as a finalist for the “Florida Companies to Watch” awards program.

This awards program is presented by GrowFL- the Florida Economic Gardening Institute (in association with Edward Lowe Foundation) – state economic development program at the University of Central Florida. It seeks to identify, serve, and celebrate these Florida companies that have the best potential to contribute to Florida’s economy- those companies with solid increasing revenue growth and new job creation potential.

The distinctive awards program is specifically designed to seek out second-stage businesses from a wide range of industries throughout Florida. GrowFL’s definition of “Second-Stage” companies are those identified as a company somewhere between a start-up and a large firm- with a common ground of being poised for growth. These companies have 10-99 employees and $1 million to $50 million in revenue. Companies selected for the award have been determined to strengthen the economy of the region and support the spirit of the entrepreneurs who live among us.

Third-party rankings and recognitions are no guarantee of future investment success and do not ensure that a client or prospective client will experience a higher level of performance or results. These ratings should not be construed as an endorsement of the advisor by any client nor are they representative of any one client’s evaluation. Please see http://flctw.growfl.com/ for more information about this awards program. There were approximately 500 nominees for the award and no fee was paid for nomination.

Kim Ciccarelli Kantor named one of Barron’s 2015 Top 100 Women Financial Advisors

The prestigious Barron’s Business and Financial Weekly has named Naples’ Kim Ciccarelli Kantor, CFP® CAP™, President of Ciccarelli Advisory Services, Inc., to its “Top 100 Women Financial Advisors” for 2015. Ms. Kantor was ranked 48th. She has previously been named to this esteemed list in 2014, 2013, 2012, 2011, 2010 and 2007. The ranking reflects the volume of assets overseen by Ms. Kantor and her team, and the quality and professionalism of her practice. Investment performance is not explicitly a criterion.

The prestigious Barron’s Business and Financial Weekly has named Naples’ Kim Ciccarelli Kantor, CFP® CAP™, President of Ciccarelli Advisory Services, Inc., to its “Top 100 Women Financial Advisors” for 2015. Ms. Kantor was ranked 48th. She has previously been named to this esteemed list in 2014, 2013, 2012, 2011, 2010 and 2007. The ranking reflects the volume of assets overseen by Ms. Kantor and her team, and the quality and professionalism of her practice. Investment performance is not explicitly a criterion.

Kim has served families in the SW Florida community, along with additional family members, for over 30 years. The firm was founded as an independent advisory company, from the Ciccarelli Family team mission, to serve clients based on their needs throughout different stages in their lives, placing family values as a top priority.

“We are so thankful to our clients, who have expressed their confidence and appreciation for the work we accomplish together. It is a joy to serve when we believe in and are passionate about what we do. I am so very proud of everyone in our company, those who are responsible for the privilege of this recognition”, says Kim.

The firm provides comprehensive financial planning and investment management, including financial discussions for proper cash flow planning, income tax planning, charitable desires, advanced estate solutions, long-term care planning, portfolio design and monitoring, family meetings and education. Ciccarelli Advisory Services is a family-owned and operated wealth management firm with offices in Naples, Florida, and Rochester, New York, serving communities nationwide.

The “Barron’s Top 100 Women Financial Advisors” – The rankings are based on qualitative criteria: professionals with a minimum of seven years financial service experience, acceptable compliance records, client retention reports and customer satisfaction reports. Advisors are quantitatively ranked based on varying types of revenues and asset advised by the financial professional, with weightings associated for each. Additional qualitative measures include: in depth interviews and discussions with senior management, peers and customers. Because individual client’s portfolio performance varies and is typically unaudited, this ranking focused on customer satisfaction and quality of advice. Please see http://online.barrons.com/report/top-financial-advisors for more information.

Third-party rankings and recognitions are no guarantee of future investment success and do not ensure that a client or prospective client will experience a higher level of performance or results. These ratings should not be construed as an endorsement of the advisor by any client nor are they representative of any one client’s evaluation.

Economic Update – Second Quarter 2015

With the most recent stock market volatility, many investors are looking over their shoulders and wondering if the gains of the past few years are in jeopardy. Many market strategists predicted that volatility would return to the equity markets in 2015 and the first half of the year has supported those forecasts.

With the most recent stock market volatility, many investors are looking over their shoulders and wondering if the gains of the past few years are in jeopardy. Many market strategists predicted that volatility would return to the equity markets in 2015 and the first half of the year has supported those forecasts.

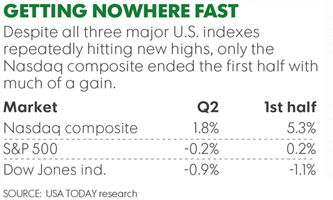

Despite all three major indexes hitting new highs this quarter, only the NASDAQ finished the first half of 2015 with much of a gain. By the end of the quarter, the Dow Jones Industrial Average was negative, down 1.1% for the year. The S&P 500 index finished up 0.2%, or about where it started. The NASDAQ rose approximately 5.3% for the first half of 2015.

There continues to be talk and debate amongst financial analysts and publications about the remainder of 2015. At Barron’s midyear roundtable, the annual gathering of 10 investment market strategists felt that although the market isn’t cheap, they were still optimistic about the remainder or 2015. Some analysts are saying a long over-due correction is imminent. According to CNN Money, the U.S. stock market is long overdue for a big fall, but the solution isn’t to exit stocks. Instead, they suggest that there may be opportunities during market dips. They remind investors that stocks often go up after a correction. Corrections do not always mean the bull market is done. (Source: CNNMoney 6/4/2015)

According to Jeff Reeves at Market Watch, a market correction is not ‘due’. He suggests that perhaps the most important data point of all for the bears to remember is that rallies do not end simply because they’ve gone on for a few years and are “due” to correct. To support this theory, he suggests investors study the bull market of 1987 to 2000, which lasted 4,494 days and saw a roughly 585% increase in the S&P 500. He adds that this is not to discourage investors from thinking critically or skeptically about the numbers. Obviously, it’s human nature to wonder when the party is going to end, but he warns against predicting the end just because we’ve had a long run-up. (Source: MarketWatch, 6/15/2015 )

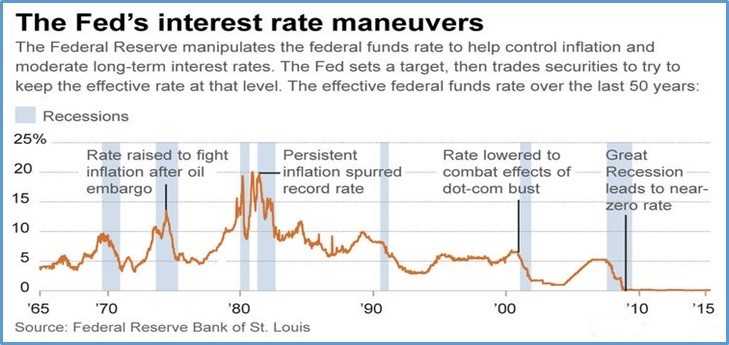

Interest Rates

Again this quarter, interest rates and Fed watching continues to feel like a spectator sport for investors. Investors are carefully watching federal funds rates in anticipation of a rate increase. Fed statements, notes and pre- and post- meeting discussions have been monitored and debated by most financial media professionals and outlets.

The federal funds rate is an important benchmark in financial markets. It is the interest rate that the borrowing banks pay to the lending banks to borrow funds. It is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate.

According to CNBC on June 23rd, Federal Reserve Governor Jerome Powell, a voting member on the policy-setting committee said he sees conditions for an interest rate liftoff as soon as September and an additional increase in December. Powell added that he believes the dollar and oil prices have broadly stabilized. He estimated the economy will grow at around a 2 percent pace this year. Powell said he’s seen positive signs in the economy, including a pickup in wages and an uptick in the labor participation rate. (Source: CNBC.com, 6/23/2015)

Currently, interest rates and the Federal Funds rate are at the center of many discussions for investment decisions. To combat the financial crisis of 2008, the previous Federal Reserve Chairman Ben Bernanke lowered the rate by aggressively dropping it ten times in 14 months. The Federal Reserve policymakers have kept the Federal Reserve funds rate at near zero since December 2008 in an attempt to stimulate economic growth. Although the economy has still not fully recovered, it is stronger, suggesting that a small interest rate move is coming. Having said that, here are some common questions about interest rates and how the central bank uses them to try to help the economy.

Exactly what interest rate is the Fed looking to raise?

Exactly what interest rate is the Fed looking to raise?

When you hear that the Fed is raising interest rates, they are referring to the federal funds rate. The reserves that banks are required to hold at the Fed are known as federal funds. Because these funds fluctuate daily, banks with a surplus of funds lend money overnight to banks with a shortfall. The interest rate that banks use for these overnight loans is known as the federal funds rate.

How does the Fed control the federal funds rate?

The decision to change the target federal funds rate is overseen by the 12 members on the Federal Open Market Committee, better known as the FOMC. Centered on the prevailing economic conditions, the committee votes on the desired target interest rate that they believe will help keep the economy running smoothly. Consistently, the targeted interest rate has always been a specific number. But since 2008, the targeted rate has been between zero to 0.25%.

Why does the Fed maneuver the federal funds rate?

The FOMC’s goal is to use the federal funds rate to prevent unnecessary shocks to the overall economy. Congress enacted the Federal Reserve with control over the federal funds rate to provide maximum employment, keep inflation low, and provide reasonable long-term interest rates. When the economy is straining, the federal funds rate is lowered to reduce borrowing costs for banks to help stimulate lending and increase economic activity. If the economy is growing too quickly, the rate is increased to raise borrowing costs and curb any growing inflation.

The FOMC alters the rate to find a balance between economic growth and low inflation. Committee members keep a close eye on economic indicators to help them establish whether the economy is speeding up too quickly (causing inflation) or slowing down and shrinking (forming a recession). Fed policy makers raised the interest rate up to 20% in 1980-81 to stop runaway inflation during that time. And when the Great Recession hit in 2008, the Fed dropped rates as low as possible to the zero lower bound – from zero to 0.25%. The Fed hasn’t raised rates since June of 2006 when the federal funds rate was 5.25%.

How does the federal funds rate affect other interest rates?

While the federal funds rate is only directly applicable to banks that lend to one another, it has become a benchmark for consumer and business loan rates. Business executives and investors keep a close eye on the federal funds rate and the FOMC’s position on the economy to help them adapt their business plans accordingly.

The prime rate, for example, is established by banks and is offered to their best customers. It is used to determine interest rates for a variety of loans, including credit cards, car loans, small business loans, and home equity lines of credit.

While the Fed has no direct control over the prime rate, it has historically been three percentage points higher than the federal funds rate. When the Fed lowered the benchmark rate from 0.75% to near zero in 2008, banks followed in turn and lowered their prime rate from 4% to 3.25%.

Does the federal funds rate influence mortgage rates?

Because most mortgages are longer term and are affected more by supply and demand of the mortgage market, the federal funds rate has less of a direct effect. However, the federal funds rate can and does influence the mortgage market. Individual mortgages are regularly packaged into investment securities that are traded throughout the economy. The Fed can actually purchase these securities to drive up demand. This is known as quantitative easing. The Fed performed several rounds of quantitative easing after the housing market crash in 2007 by purchasing hundreds of billions of dollars in mortgage-backed securities and Treasury bonds to help lower mortgage rates and increase home value. Some analysts also say that long-term rates reflect the direction of a series of short-term interest rate changes. Therefore, multiple increases of the federal funds rate could raise mortgage and other long-term rates higher.

We still live in a slow-growth, low inflation world that is likely to keep interest rates low for the immediate future. Currently, 27 of the world’s 34 major central banks are making an effort to suppress interest rates. Investors need to keep a watchful eye on interest rates, but also need to avoid over focusing on rate hikes. (Source: Fidelity 6/5/2015)

Should you have any concerns about your holdings we would be glad to recheck your personal situation during your next review or at any other time.

Greece’s Monetary Issue

The 2008 financial crisis put a strain on Greece’s fiscal budget, which was already in poor shape. In 2010, the Greek government took billions of euros in bailout money from the European Union and International Monetary Fund. The lenders required Greece to implement heavy spending cuts and tax increases, which then created skyrocketing unemployment and plummeting living standards.

Since then, Greece has faced a choice: either stick with the bailouts and endure the pain of austerity, or reject the terms of the bailout — likely leading to default and, possibly, leaving the Eurozone entirely.

Greeks elected a new government in January 2015 that opted for a third option: renegotiating the terms of the bailout to require less severe austerity measures. This strategy failed, partly because Greek leaders have no leverage, and partly because European politicians feared that granting Greece’s demands would anger other countries who’ve accepted bailout money — like Spain, Portugal, or Ireland.

While this issue is still outstanding as of the quarter’s end, the Greek government has officially imposed capital controls to try to contain the economic crisis. That means, for example, that it has shuttered all banks until after the referendum on the bailout deal and issued strict regulations on other use of financial institutions. ATM withdrawals are limited to €60 per day, per account. Transfers of money outside Greece are banned and exceptions require Finance Ministry approval. Pension and wage payments are to proceed as normal, as does internet banking and debit card transactions.

The basic reason behind these rules is to prevent bank runs. If people take too much cash out of the country’s banks, then they’ll cease being able to make loans and the country will fall into a financial crisis.

Greek citizens have strong reasons to want to take their money out of the banks. Deposits could be raided to help keep banks solvent, as happened in Cyprus. Another possibility is that Greece could abandon the euro, convert all deposits into its new currency (probably the drachma, the country’s pre-euro currency), and then devalue that currency dramatically.

If Greece vanished today, the world economy would contract 0.3 per cent, once. Economically, the loss would scarcely be noticed. Since Greece has only 11 million people, a financial crisis wouldn’t be the same as a United States or global financial crisis. It is not big enough to hurt. (Source: NBC World News)

How will the Greek issues affect the markets?

In reaction to Greece’s concerns, the Dow plummeted 350 points June 29th, its worst day of the year. Some analysts believe the effect may be short-lived: S&P Capital IQ published a 70-year historical analysis of past market shocks that found events like this produce an average decline of 2.4 percent on the next trading day, which has been recovered in an average of 14 trading days.

“Greece represents less than 2 percent of the EU’s GDP,” S&P strategist Sam Stovall wrote. “By itself, its default or exit won’t upend the EU. … Yet if this drachma drama triggers a market decline in excess of 10 percent, not seen since October 2011, it may be a blessing in disguise. As history has shown, prior market shocks have usually proven to be better opportunities to buy than bail, primarily because the events did not dramatically alter the course of global economic growth.” (Source: NBC World News)

China’s Equity Markets

China had a tumultuous quarter. The economy continued to slow, growing only 7% in the first quarter, the slowest in six years. Some analysts are concerned that what happens in the Shanghai stock market may not stay there.

The Shanghai Composite, which was a rising star for the last year, is off nearly 22% from its peak in mid-June, including a 3.3% fall on June 29th. China’s interest-rate cut on the prior weekend did little to restore investor confidence.

Historically, the movements of China’s stock market have had little impact on the broader economy. After the last Chinese equity bubble burst in 2007 to 2008, China’s stock prices were low for more than five years. During this same time period China posted impressive GDP growth rates.

The Chinese government has been pulling a number of levers to try to stimulate the economy. Despite this uncertain growth picture, the Shanghai SE Composite Index, despite falling 7.3% in the last month, has gained 14.1% in the last three months, and 32.2% for the year to date.

The Chinese government has been pulling a number of levers to try to stimulate the economy. Despite this uncertain growth picture, the Shanghai SE Composite Index, despite falling 7.3% in the last month, has gained 14.1% in the last three months, and 32.2% for the year to date.

Fewer than 10% of Chinese households own shares, compared with more than half of American ones. The “wealth effect” that is seen in the U.S. and other developed countries, whereby households tend to feel wealthier when stocks rise, or poorer when they fall, and adjust their spending plans accordingly, hasn’t been as strong in China. However, some analysts are warning that it would be a mistake to assume that China will shrug off this market meltdown. (Sources: Morningstar 7/1/2015, Wall Street Journal 6/29/2015)

Conclusion: What Should an Investor Do?

Investors are concerned about return. After all, the market has been up. On June 24th, in an article entitled Will the DJIA hit 16,000 or 20,000 first?, the Chief Market Strategist for Convergex noted that the Dow Jones Industrial Average was up 324 points for the year to date – which meant an increase of 1.8%. Although there are 30 companies in this oldest broad market measures, just 2 names made up all that performance (and then some, actually). Goldman Sachs was up 12% year to date, adding 174 points to the Dow and UnitedHealth’s 21% return was worth another 164. You’d think it would be the other way around, but GS’s higher stock price gives it a heftier weighting. The other 28 names in the Dow netted out to zero impact for the year. (Source: www.convergex.com)

The first half of 2015 was not easy for investors. By many measures, the equity markets are not cheap. However, experts are still upbeat for 2015. As advisors, we are faced with the tough task of balancing portfolios between risk free rates, risk premiums and market returns. (Source: Fidelity 6/15/2015)

The first half of 2015 was not easy for investors. By many measures, the equity markets are not cheap. However, experts are still upbeat for 2015. As advisors, we are faced with the tough task of balancing portfolios between risk free rates, risk premiums and market returns. (Source: Fidelity 6/15/2015)

So what can investors do?

Safety comes with a price. Rates on longer-term certificates of deposit got a small bump in Bankrate.com’s June 24 survey of interest rates. The average one-year CD yield was 0.27% for the 15th straight week. The typical five-year yield was up 1 basis point to 0.87% (a basis point is one-hundredth of 1%). Jumbo CDs sport slightly higher yields for a $100,000 deposit. The average one-year jumbo CD yield was 0.3% for the seventh consecutive week. The average five-year CD yield was up 1 basis point to 0.92%.

For the 37th week in a row, the average money market account yield was 0.09%. (Source: www.bankrate.com)

For many investors these low fixed rates will not help them achieve their desired goals. Most investors attempt to build a plan that includes risk awareness. Many times this can lead to lower but safer returns. Traditionally, bonds have been the de facto standard to hedge against market risk, but with bond values at historical highs they no longer offer the kind of protection they once did and quite possibly pose a greater threat of loss than stocks. Investing is not about keeping pace with the market (who likes losing 40% during years like 2008?) or beating the market – it’s all about hedging risk so your portfolio suits your individual needs regardless of the market.

Have a Strategy. Investors need to be prepared. Market volatility should cause you to be concerned, but panicking is not a plan. Market downturns do happen and so do recoveries. This is the ideal time to ensure that you fully understand your time horizons, goals and risk tolerances. Looking at your whole picture can be a helpful exercise in determining your strategy.

Focus on your own personal objectives. During confusing times it is always wise to create realistic time horizons and return expectations for your own personal situation and to adjust your investments accordingly. Understanding your personal commitments and categorizing your investments into near-term, short-term and longer-term can be helpful.

Make sure you are comfortable with your investments. Equity markets will continue to move up and down. Even if your time horizons are long, you could see some short term downward movements in your portfolios. Rather than focusing on the turbulence, you might want to make sure your investment plan is centered on your personal goals and timelines. Peaks and valleys have always been a part of financial markets and it’s highly likely that trend will continue.

Discuss any concerns with us.

Our advice is not one-size-fits-all. We will always consider your feelings about risk and the markets and review your unique financial situation when making recommendations.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment.

Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. The P/E ratio (price to earnings ratio is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher P/E ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower P/E ratio. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Estate Planning Key Numbers

You will find here some key numbers associated with estate planning, as well as the federal gift tax and estate tax rate schedules for 2014 and 2015.

1 The basic exclusion amount

2 Deceased spousal unused exclusion amount (for 2011 and later years)

3 The GST tax exemption is not portable

2014 and 2015 Gift Tax and Estate Tax Rate Schedule

Key Estate Planning Documents You Need

There are five estate planning documents you may need, regardless of your age, health, or wealth:

- Durable power of attorney

- Advanced medical directives

- Will

- Letter of instruction

- Living trust

The last document, a living trust, isn’t always necessary, but it’s included here because it’s a vital component of many estate plans.

Durable power of attorney

A durable power of attorney (DPOA) can help protect your property in the event you become physically unable or mentally incompetent to handle financial matters. If no one is ready to look after your financial affairs when you can’t, your property may be wasted, abused, or lost.

A DPOA allows you to authorize someone else to act on your behalf, so he or she can do things like pay everyday expenses, collect benefits, watch over your investments, and file taxes.

There are two types of DPOAs: (1) an immediate DPOA, which is effective immediately (this may be appropriate, for example, if you face a serious operation or illness), and (2) a springing DPOA, which is not effective unless you have become incapacitated.

Caution: A springing DPOA is not permitted in some states, so you’ll want to check with an attorney.

Advanced medical directives

Advanced medical directives let others know what medical treatment you would want, or allows someone to make medical decisions for you, in the event you can’t express your wishes yourself. If you don’t have an advanced medical directive, medical care providers must prolong your life using artificial means, if necessary. With today’s technology, physicians can sustain you for days and weeks (if not months or even years).

There are three types of advanced medical directives. Each state allows only a certain type (or types). You may find that one, two, or all three types are necessary to carry out all of your wishes for medical treatment. (Just make sure all documents are consistent.)

First, a living will allows you to approve or decline certain types of medical care, even if you will die as a result of that choice. In most states, living wills take effect only under certain circumstances, such as terminal injury or illness. Generally, one can be used only to decline medical treatment that “serves only to postpone the moment of death.” In those states that do not allow living wills, you may still want to have one to serve as evidence of your wishes.

Second, a durable power of attorney for health care (known as a health-care proxy in some states) allows you to appoint a representative to make medical decisions for you. You decide how much power your representative will or won’t have.

Finally, a Do Not Resuscitate order (DNR) is a doctor’s order that tells medical personnel not to perform CPR if you go into cardiac arrest. There are two types of DNRs. One is effective only while you are hospitalized. The other is used while you are outside the hospital.

Benefits of a will:

•Distributes property according to your wishes

•Names an executor to settle your estate

•Names a guardian for minor children

Will

A will is often said to be the cornerstone of any estate plan. The main purpose of a will is to disburse property to heirs after your death. If you don’t leave a will, disbursements will be made according to state law, which might not be what you would want.

There are two other equally important aspects of a will:

- You can name the person (executor) who will manage and settle your estate. If you do not name someone, the court will appoint an administrator, who might not be someone you would choose.

- You can name a legal guardian for minor children or dependents with special needs. If you don’t appoint a guardian, the state will appoint one for you.

Keep in mind that a will is a legal document, and the courts are very reluctant to overturn any provisions within it. Therefore, it’s crucial that your will be well written and articulated, and properly executed under your state’s laws. It’s also important to keep your will up-to-date.

Letter of instruction

A letter of instruction (also called a testamentary letter or side letter) is an informal, nonlegal document that generally accompanies your will and is used to express your personal thoughts and directions regarding what is in the will (or about other things, such as your burial wishes or where to locate other documents). This can be the most helpful document you leave for your family members and your executor.

Unlike your will, a letter of instruction remains private. Therefore, it is an opportunity to say the things you would rather not make public.

A letter of instruction is not a substitute for a will. Any directions you include in the letter are only suggestions and are not binding. The people to whom you address the letter may follow or disregard any instructions.

Other benefits of a living trust: •Gives someone the power to manage your property if you should become incapacitated •Lets a professional manage your property for you •May circumvent state laws that limit your ability to give to charity, or force you to leave a certain percentage of your property to your spouse

Living trust

A living trust (also known as a revocable or inter vivos trust) is a separate legal entity you create to own property, such as your home or investments. The trust is called a living trust because it’s meant to function while you’re alive. You control the property in the trust, and, whenever you wish, you can change the trust terms, transfer property in and out of the trust, or end the trust altogether.

Not everyone needs a living trust, but it can be used to accomplish various purposes. The primary function is typically to avoid probate. This is possible because property in a living trust is not included in the probate estate.

Depending on your situation and your state’s laws, the probate process can be simple, easy, and inexpensive, or it can be relatively complex, resulting in delay and expense. This may be the case, for instance, if you own property in more than one state or in a foreign country, or have heirs that live overseas.

Further, probate takes time, and your property generally won’t be distributed until the process is completed. A small family allowance is sometimes paid, but it may be insufficient to provide for a family’s ongoing needs. Transferring property through a living trust provides for a quicker, almost immediate transfer of property to those who need it.

Probate can also interfere with the management of property like a closely held business or stock portfolio. Although your executor is responsible for managing the property until probate is completed, he or she may not have the expertise or authority to make significant management decisions, and the property may lose value. Transferring the property with a living trust can result in a smoother transition in management.

Finally, avoiding probate may be desirable if you’re concerned about privacy. Probated documents (e.g., will, inventory) become a matter of public record. Generally, a trust document does not.

Caution: Although a living trust transfers property like a will, you should still also have a will because the trust will be unable to accomplish certain things that only a will can, such as naming an executor or a guardian for minor children.

Tip: There are other ways to avoid the probate process besides creating a living trust, such as titling property jointly.

Caution: Living trusts do not generally minimize estate taxes or protect property from future creditors or ex-spouses.

CAS New York – Spring Clean-up for Heritage Christian Services

Team members of CAS Rochester enjoyed a beautiful spring day on May 14th as they once again assisted with the spring yard work at a Heritage Christian Services group residence. This endeavor was in conjunction with the United Way’s Day of Caring, a day in which thousands of volunteers participate in various projects in the Rochester area. The team spent the day mulching, trimming, raking, and weeding, and were treated to a delicious lunch at the residence as well.

Team members of CAS Rochester enjoyed a beautiful spring day on May 14th as they once again assisted with the spring yard work at a Heritage Christian Services group residence. This endeavor was in conjunction with the United Way’s Day of Caring, a day in which thousands of volunteers participate in various projects in the Rochester area. The team spent the day mulching, trimming, raking, and weeding, and were treated to a delicious lunch at the residence as well.

Last year two CAS teams assisted with the spring and fall cleanup of the same residence. Who knew we had such a talented landscaping crew!

CAS is proud to support the community in which we reside. We look forward to future outings that connect our team with those for whom assistance is greatly needed.