CAS News

There’s Still Time to Contribute to an IRA for 2015

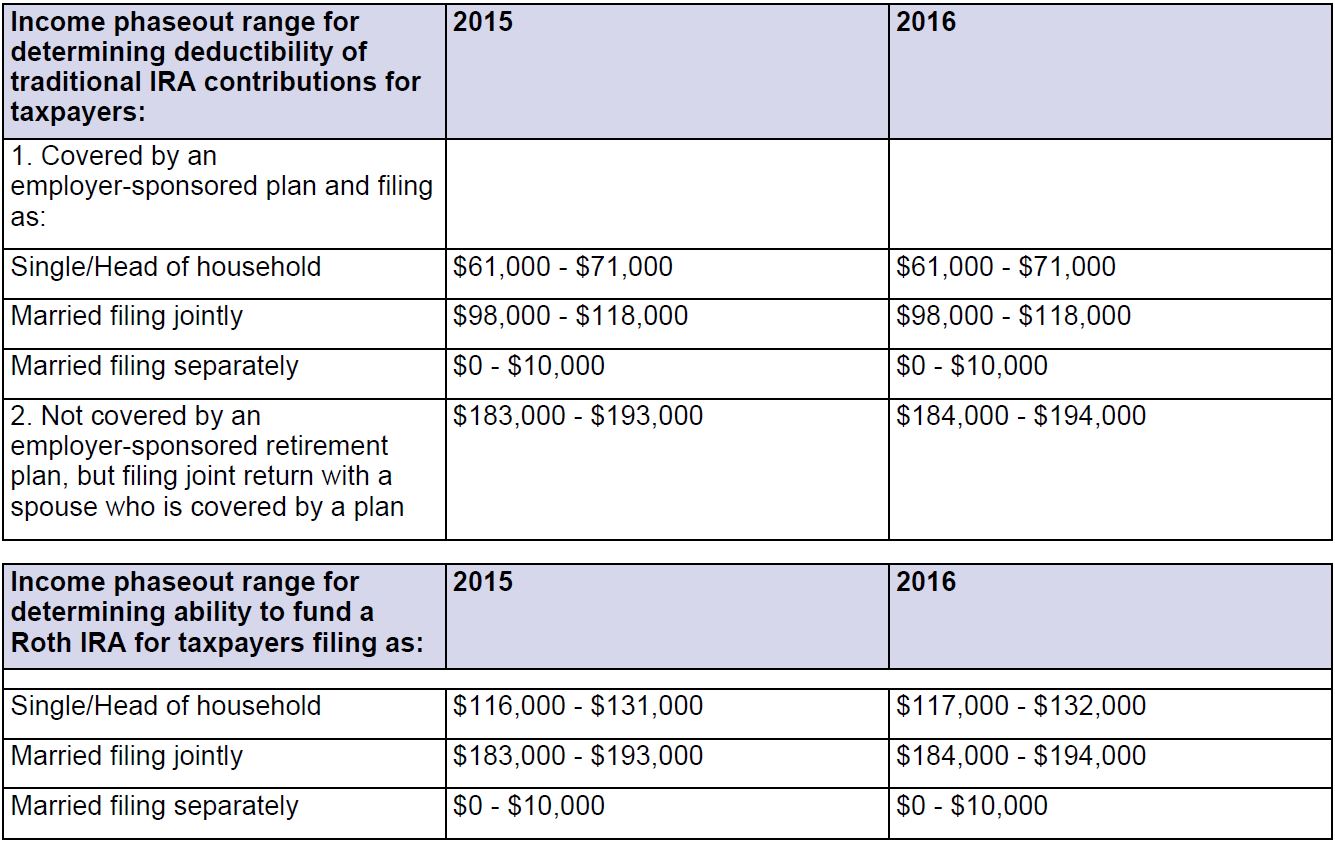

There’s still time to make a regular IRA contribution for 2015! You have until your tax return due date (not including extensions) to contribute up to $5,500 for 2015 ($6,500 if you were age 50 by December 31, 2015). For most taxpayers, the contribution deadline for 2015 is April 18, 2016 (April 19, 2016, if you live in Maine or Massachusetts).

You can contribute to a traditional IRA, a Roth IRA, or both, as long as your total contributions don’t exceed the annual limit (or, if less, 100% of your earned income). You may also be able to contribute to an IRA for your spouse for 2015, even if your spouse didn’t have any 2015 income.

Traditional IRA

You can contribute to a traditional IRA for 2015 if you had taxable compensation and you were not age 70½ by December 31, 2015. However, if you or your spouse was covered by an employer-sponsored retirement plan in 2015, then your ability to deduct your contributions may be limited or eliminated depending on your filing status and your modified adjusted gross income (MAGI) (see table below). Even if you can’t deduct your traditional IRA contribution, you can always make nondeductible (after-tax) contributions to a traditional IRA, regardless of your income level. However, in most cases, if you’re eligible, you’ll be better off contributing to a Roth IRA instead of making nondeductible contributions to a traditional IRA.

Roth IRA

Roth IRA

You can contribute to a Roth IRA if your MAGI is within certain dollar limits (even if you’re 70½ or older). For 2015, if you file your federal tax return as single or head of household, you can make a full Roth contribution if your income is $116,000 or less. Your maximum contribution is phased out if your income is between $116,000 and $131,000, and you can’t contribute at all if your income is $131,000 or more. Similarly, if you’re married and file a joint federal tax return, you can make a full Roth contribution if your income is $183,000 or less. Your contribution is phased out if your income is between $183,000 and $193,000, and you can’t contribute at all if your income is $193,000 or more. And if you’re married filing separately, your contribution phases out with any income over $0, and you can’t contribute at all if your income is $10,000 or more.

Even if you can’t make an annual contribution to a Roth IRA because of the income limits, there’s an easy workaround. If you haven’t yet reached age 70½, you can simply make a nondeductible contribution to a traditional IRA, and then immediately convert that traditional IRA to a Roth IRA. Keep in mind, however, that you’ll need to aggregate all traditional IRAs and SEP/SIMPLE IRAs you own–other than IRAs you’ve inherited–when you calculate the taxable portion of your conversion. (This is sometimes called a “back-door” Roth IRA.)

Finally, keep in mind that if you make a contribution to a Roth IRA for 2015–no matter how small–by your tax return due date, and this is your first Roth IRA contribution, your five-year holding period for identifying qualified distributions from all your Roth IRAs (other than inherited accounts) will start on January 1, 2015.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The

information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Money Management Lessons from Dad and Other Wise Folk, Part I

Kim Ciccarelli Kantor | Naples Daily News | September 12, 2012

Kim Ciccarelli Kantor | Naples Daily News | September 12, 2012

Money lessons are hard to come by for most people. Perhaps we want to hear something different from what we know as solid, reasonable advice.

Less-experienced investors want glamour and quick fixes.

It was years before I understood a story my father told me: The lesson he passed on was that wealth would be achieved by doing the right thing, consistently and patiently, as long as you were headed in the right direction.

He would say, “Focus on what you can control—avoiding mistakes.” Do your homework and think through your decision before taking action.

It was James P. Owen, author of “The Prudent Investor: The Definitive Guide to Professional Money Management,” who wrote of the 10 most common mistakes affluent investors make and how to avoid them.

I have found these to be powerful lessons for any investor and will share them in this and my next two columns:

- Not Running Your Finances Like a Business

Treating your investments like a part-time job does not place them in a top priority position. Highly successful people who are casual or haphazard about investing are most likely oblivious to the amount of money it takes to maintain their lifestyle. No matter what your situation, if you are investing assets of $1 million, $2 million, $5 million or more, you have a great deal at stake. At this level, managing your money is like running a business. As the CEO of your investment “company,” you must make sure your assets are invested in a systematic, disciplined way.

To do so, you must have a business plan that covers both the short and the long term; quantifiable goals against which to measure results—incorporating both life goals and investment goals; a strategy to attain your goals; and the right professionals to do the job.

- Not Defining Your Investment Policy

When you let fad statements like “bonds are safe” or “this isn’t the right time to buy stocks” shape your investment approach, you are vulnerable to missed opportunities at best, and costly errors at worst. What is an investment policy? It is a strategic, long-term framework that defines for one, your asset allocation policy.

This lays the foundation for the mix of your investments with the balance of risk and return that is proper for you.

This policy should be in place and created with your financial consultant before hiring any manager or selecting specific investments for your portfolio.

To create a successful investment policy, consider your time horizon, income requirements, tolerance for risk and volatility, and return expectations.

Investment policies, like any other part of your planning, should be periodically reviewed. You may need to make some adjustments if your goals have shifted in any meaningful way.

- Trying to Time the Market

It is only human nature to want to time the market. Many investors continue to try time and time again, despite all evidence they will never succeed.

On Wall Street, and in the homes of seasoned investors, the consensus is clear: It is time—not timing—that makes you successful in the market.

The problem is it is virtually impossible to time the market correctly, consistently.

Historically, markets are an upward trend over time, and stocks make the most gains in short, climatic spurts. Missing just 30 of the best market days can make for a significant underachievement of your goals. Waiting for the right time to jump back in after a recovery is a difficult, if not impossible, challenge.

The lessons learned today evolve from mistakes that may be avoided if planned for properly. The errors investors make are simple yet complex, profound yet clear. Don’t fall victim to what you might be able to avoid—common mistakes in investing.

Additional common mistakes investors should avoid will be discussed next month in Part II.

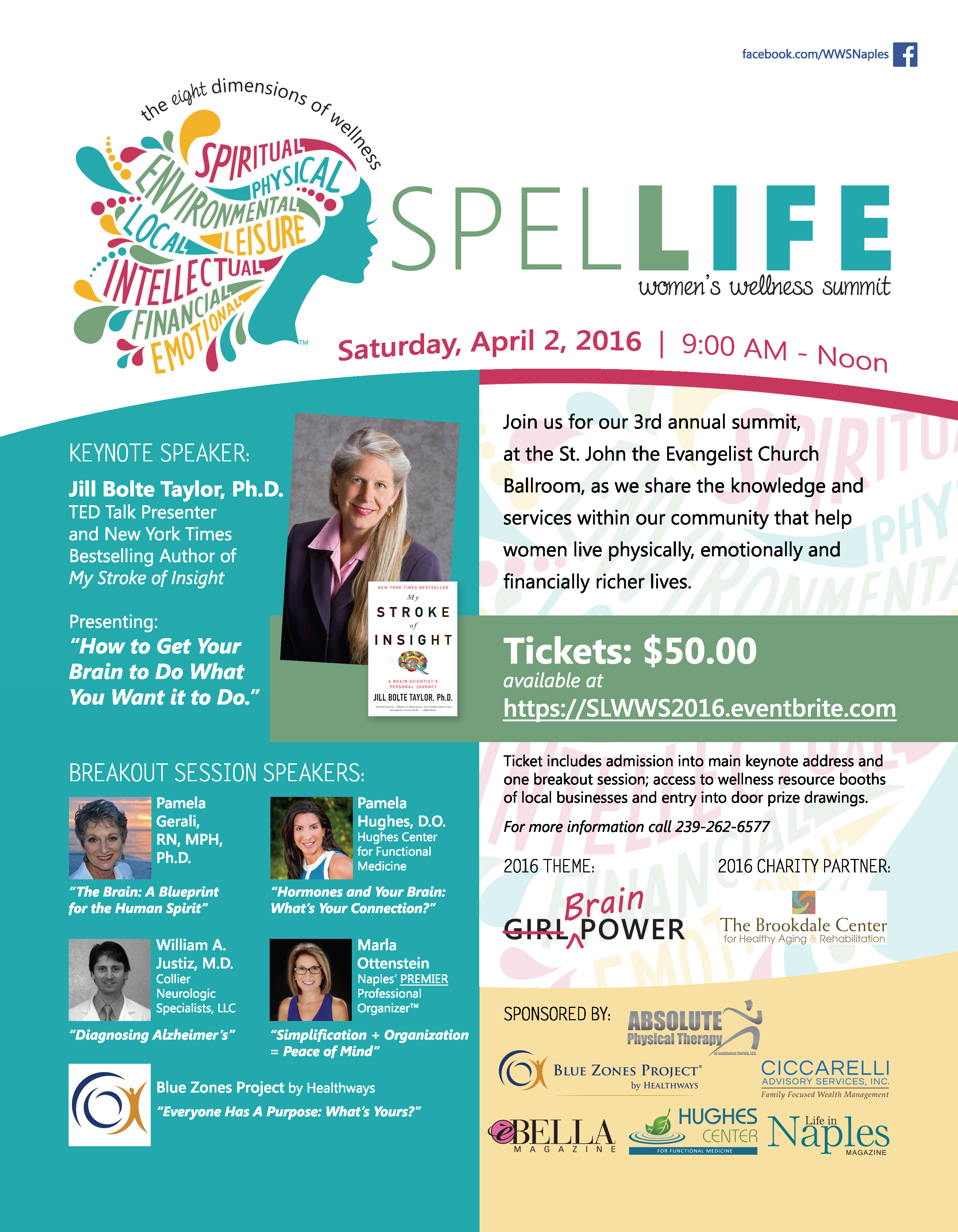

SPELLIFE Women’s Wellness Summit

DATE: April 2, 2016

TIME: 9:00 AM – Noon

WHERE: St. John the Evangelist Church Ballroom, Naples, FL

TICKETS: $50.00 available at https://SLWWS2016.eventbrite.com

Click image below to download a copy

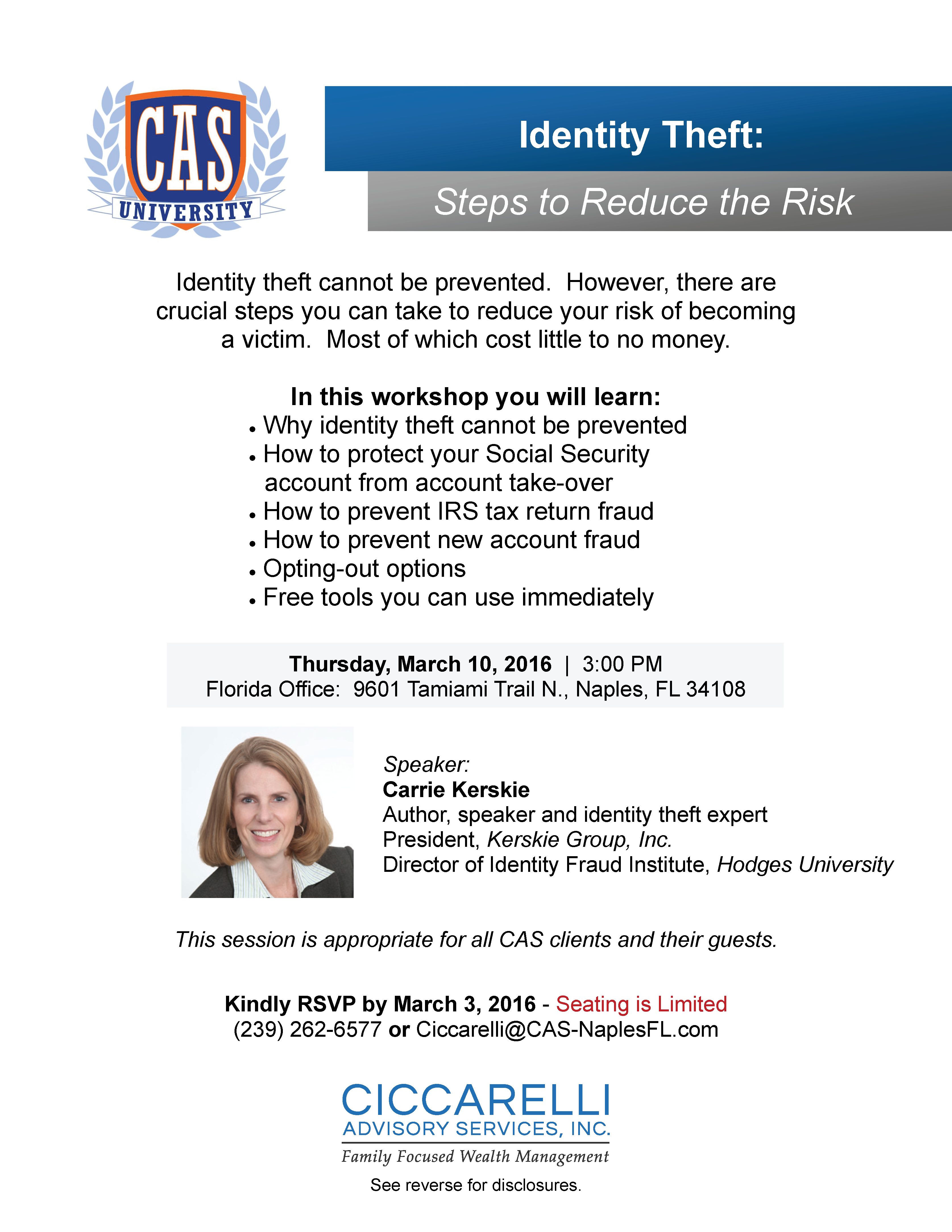

Event – “Identity Theft: Steps to Reduce the Risk”

DATE: March 10, 2016

TIME: 3:00 PM

WHERE: CAS Florida Office

RSVP: 239-262-6577 or Ciccarelli@CAS-NaplesFL.com

Click image below to download a copy

CAS Profiles – Lisa Buckert (New York)

Lisa became part of the Ciccarelli Family in October 2005 and is currently a Client Services Associate for Judith Alexander-Wasley.

Lisa became part of the Ciccarelli Family in October 2005 and is currently a Client Services Associate for Judith Alexander-Wasley.

Lisa is from Rochester, New York, and has many brothers and sisters who still live in the area. She has two grown children, Jonathan and Brianne. She and her husband recently welcomed their first grandchild, Jameson, and you can hear the joy in her voice when she speaks of him! When she isn’t spending time with family, especially her grandson, her interests include reading, bowling, and ceramics. In the warm months, she likes to garden and her favorite flowers are mums and roses. She also enjoys baking.

Lisa enjoys working at CAS. The people are great and she feels like they are family. If she was not in the financial services industry, Lisa would be a teacher. She has a special gift with children and loves working with and being around them.

We are very lucky to have her as part of our CAS family!

Lisa is not registered with FSC Securities Corporation.

The Good Side of Bad Markets

After the recent downturn in the U.S. and global stock markets, you can be pardoned if you wished that the markets were a bit tamer. Wouldn’t it be nice to get, say, a steady 4% return every year rather than all these ups and downs?

After the recent downturn in the U.S. and global stock markets, you can be pardoned if you wished that the markets were a bit tamer. Wouldn’t it be nice to get, say, a steady 4% return every year rather than all these ups and downs?

Be careful what you wish for. There are at least three reasons why you should hope the markets continue scaring investors half out of their wits.

- The very fact that stock downturns scare people is one reason why stocks deliver a higher return than bonds. Economists call it the “risk premium;” which can be roughly translated as: people are not willing to pay as much for an investment that will periodically frighten them to death as they would pay for an investment that delivers a less exciting investment ride. Over their history, stocks have been a fairly consistent bargain relative to less volatile alternatives, which is another way of saying that they’ve delivered higher long-term returns than bonds and cash.

- If you’re accumulating for retirement by putting money in the market every month or quarter, every downturn means that you can buy shares at a bargain price while many other investors are selling out at or near the bottom. Over time, as the market recovers, this can give a little extra kick to your overall return.

- Market downturns give an advantage to those who are willing to practice disciplined rebalancing among different asset classes. Basically, that means that when stocks go down, any new cash goes disproportionately into stocks to bring them back up to their former share of the overall portfolio. This, too, allows you to buy extra shares when the prices are low, and can also boost long-term returns.

There’s no question, the downward plunge on the stock market roller coaster is scary. It’s hard to maintain your discipline when the voice in the back of your brain is telling you to bail out on the bouncy trip before somebody gets hurt.

But unless this is the first time in history that the market goes down and stays down forever, we will ultimately look back on the decline and see a buying opportunity, rather than a great time to sell and jump to the sidelines. The patient, disciplined, long-term investor should see market volatility as one of your best friends and allies in your journey toward retirement prosperity.

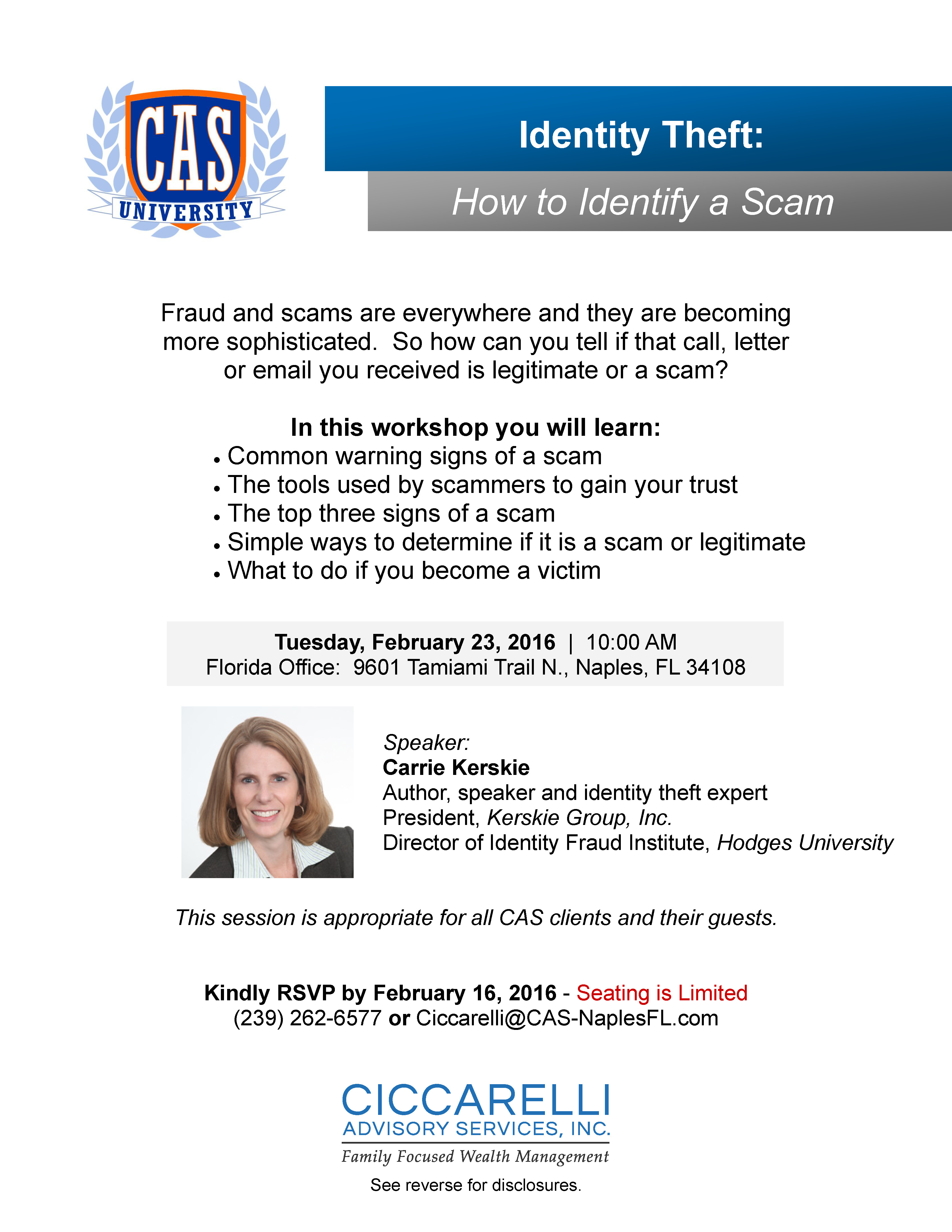

Event – “Identity Theft: How to Identify a Scam”

DATE: February 23, 2016

TIME: 10:00 AM

WHERE: CAS Florida Office

RSVP: 239-262-6577 or Ciccarelli@CAS-NaplesFL.com

Click image below to download a copy

New Legislation Makes Many Tax Provisions Permanent

The Protecting Americans from Tax Hikes (PATH) Act of 2015

The Protecting Americans from Tax Hikes (PATH) Act of 2015

In one of its final actions for calendar year 2015, Congress passed the Consolidated Appropriations Act, 2016, a massive spending bill that will keep the federal government funded for fiscal year 2016. Signed into law on December 18, 2015, the legislation includes the Protecting Americans from Tax Hikes (PATH) Act of 2015 (Division Q of the Consolidated Appropriations Act), which addresses a host of popular but temporary tax provisions–commonly referred to as “tax extenders”–that had expired at the end of 2014, making many of them permanent. Some of the major provisions addressed are listed below.

Individuals

- American Opportunity Tax Credit

The American Opportunity Tax Credit (a modified version of the original Hope Credit) and the credit rules–including maximum credit amount, number of years of education covered, income phaseout ranges, and refundability provisions–are made permanent. - Child tax credit

The lower $3,000 earned income threshold for determining the refundable portion of the tax credit is made permanent (if the credit exceeds tax liability, an amount equal to 15% of earned income over $3,000 may be refunded). - Credit for nonbusiness energy property

The credit is extended for two additional years (through 2016); lifetime cap of $500 remains. - Deduction for classroom expenses paid by educators

The $250 above-the-line deduction is made permanent–the rules that applied in 2014 are retroactively extended for 2015; starting in 2016, the limit will be indexed for inflation, and qualifying professional development expenses will be considered eligible expenses for purposes of the deduction. - Deduction for qualified higher-education expenses

The above-the-line deduction, worth up to $4,000, is reinstated for 2015 and extended through 2016. - Deduction for state and local general sales taxes

Individuals who itemize deductions on Schedule A of IRS Form 1040 can elect to deduct state and local general sales taxes in lieu of the deduction for state and local income taxes–this is made permanent. - Discharge of qualified personal residence debt

The exclusion from gross income of the discharge of debt associated with a qualified principal residence is reinstated for 2015 and extended through 2016. - Earned income tax credit

The increased credit percentage for families with three or more qualifying children and the increased threshold phaseout range for married couples filing joint returns are made permanent. - Employer-provided mass transit benefits

The monthly exclusion for employer-provided transit pass and vanpool benefits will be permanently set to the same level as the exclusion for employer-provided parking (applies retroactively to 2015, increasing the exclusion from $130 to $250 monthly). - Mortgage insurance premiums

The provision allowing premiums paid for qualified mortgage insurance to be treated as deductible qualified residence interest on Schedule A of IRS Form 1040 (subject to phaseout based on income) is extended for two additional years, through 2016. - Qualified charitable distributions (QCDs)

The provision allowing individuals age 70½ or older to make qualified charitable distributions (QCDs) from their IRAs, and exclude the distribution from gross income (up to $100,000 in a year), is made permanent. - Qualified conservation contributions of capital gain real property

Special rules for qualified conservation contributions of capital gain real property are made permanent; new rules for qualified contributions by certain Alaska Native Corporations are added for years after 2015.

Businesses

- Bonus depreciation

Additional 50% bonus depreciation is reinstated for 2015 and extended through 2019; the bonus percentage is reduced to 40% in 2018 and 30% in 2019 for most property types. - Exclusion of gain on qualified small business stock

The 100% exclusion of capital gain from sale or exchange of qualified small business stock held for more than 5 years is made permanent; it applies to alternative minimum tax as well as regular income tax. - IRC Section 179 expensing

Increased dollar amounts ($500,000/$2,000,000) associated with Section 179 expensing are made permanent and indexed for inflation after 2015; $250,000 limit on qualified real property eliminated after 2015. - Research credit

The research tax credit is made permanent, with new provisions effective in tax years beginning after 2015 that will provide additional benefits to some small businesses. - Work Opportunity Tax Credit

The tax credit is extended through 2019 and expanded (after 2015) to apply to employers who hire qualified long-term unemployment recipients.

Other changes

In addition to the tax extender provisions, the Consolidated Appropriations Act contains multiple other tax provisions, including:

- The Act delays imposition of the excise tax on high-cost employer-sponsored health coverage (the so-called “Cadillac tax”) for two years; the tax, originally scheduled to take effect after 2017, will now be effective for tax years beginning after December 31, 2019.

- The Act eliminates the requirement that ABLE accounts (tax-favored savings vehicles intended to benefit disabled individuals) be established only in the ABLE account owner’s state of residence.

- Rules relating to 529 plans are modified for tax years after 2014, including expansion of the definition of qualified expenses to include the purchase of a computer, peripheral equipment, computer software, and Internet access if used primarily by the beneficiary while enrolled at an eligible education institution.

- The Act permits funds to be rolled over to a SIMPLE IRA from employer-sponsored retirement plans and traditional IRAs once a participant has participated in the SIMPLE IRA for a two-year period (effective for rollover contributions made after December 18, 2015).

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

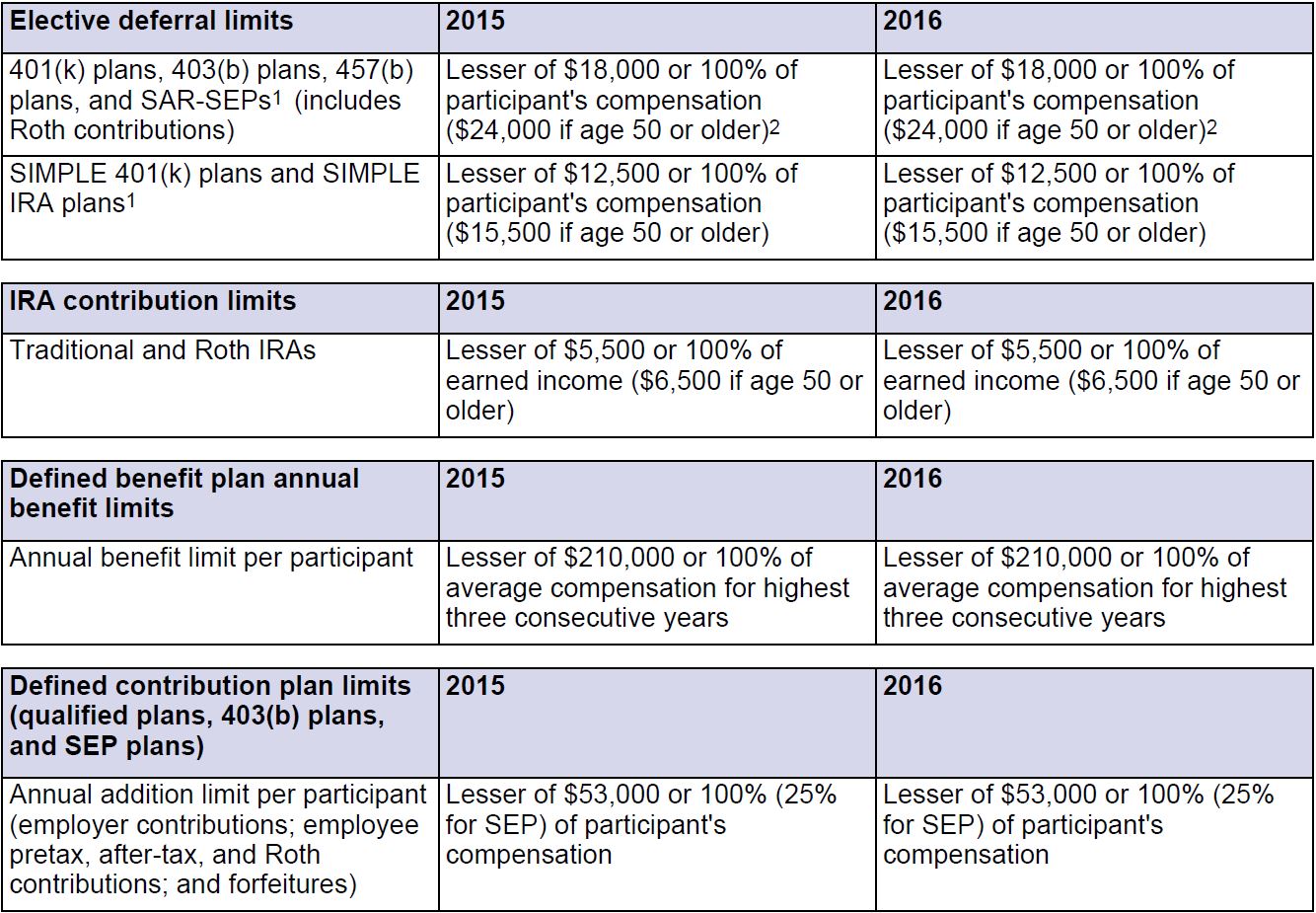

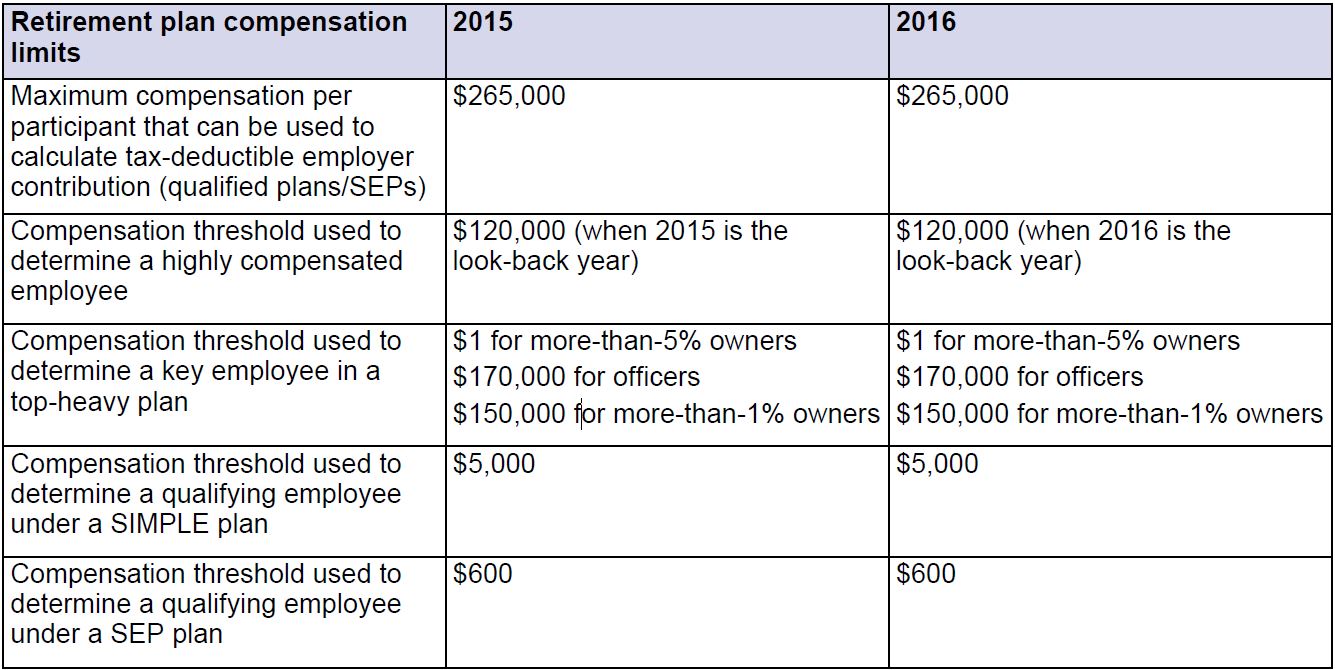

Retirement Planning Key Numbers

Certain retirement plan and IRA limits are indexed for inflation each year, but only a few of the limits eligible for a cost-of-living adjustment (COLA) have increased for 2016. Some of the key numbers for 2016 are listed below, with the corresponding limit for 2015. (The source for these 2016 numbers is IRS Information Release IR-2015-118.)

1 Must aggregate employee deferrals to all 401(k), 403(b), SAR-SEP, and SIMPLE plans of all employers; 457(b) contributions are not aggregated. For SAR-SEPs, the percentage limit is 25% of compensation reduced by elective deferrals (effectively a 20% maximum contribution).

2 Special catch-up limits may also apply to 403(b) and 457(b) plan participants.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

How to Capitalize Your Wealth in Your Living Trust

Jill Ciccarelli Rapps | Life in Naples Magazine | January 2016

Jill Ciccarelli Rapps | Life in Naples Magazine | January 2016

As you move through life, it’s important that you take the right steps to ensure your financial future and the future of your loved ones. That’s why it is important to consider capitalizing the benefits of a living trust. It could be the right call for you and for your family, and it’s something that deserves a closer look.

Of course, just as with anything else, it’s important to begin by fully understanding the basics behind the process of doing so – not to mention why it’s worth thinking about.

WHAT IS A LIVING TRUST?

- A living trust is a popular estate planning tool that lets you (1) retain control over the trust property while you are alive, (2) avoid guardianship in case you become incapacitated and can no longer handle your own financial affairs, and (3) pass trust property outside of probate when you die.

- Legally, a living trust is a separate entity that you create while you are living to “own” property, such as a house, boat, jewelry, or mutual funds. The trust is revocable, which means that you can make changes to it, or even end it, at any time.

SO WHY SET ONE UP?

There are several reasons that setting up a trust is something well worth taking the time to do. Some of these include:

- Peace of mind for you knowing that your loved ones will receive their legacy without the interference of the courts after your death. This is especially important if you are passing on ownership of a business. Estimates suggest that about 3-5% of the value of your property may be spent on lawyer fees and court costs. That’s money and time that may be wasted for your loved ones, and a living trust allows you to avoid that.

- The ability to better plan for your future and your family’s future if you are unable to manage your assets during your lifetime.

- The possibility to protect your children from litigation or divorce by having them inherit their legacy via trust.

WHAT ARE SOME KEY STEPS TO TAKE?

You’ve likely gone through your life making smart decisions – especially if you’ve reached the point where you’re planning on a living trust. For a living trust, there are a few key steps you’ll need to take:

- Create the trust. This can be drawn up with the help of an attorney and your financial advisor. Because it is likely that your financial advisor knows so much about you and your family, they can assist you in bridging what is most important to you with your legal documents that your attorney will draft.

- Many people forget to put assets in their trust and the benefits of the trust are not realized. There are some assets, because of other lifetime benefits, that should not be owned by your trust. This is an important area to work closely with your financial advisor and attorney so they can help you to properly “fund” your trust.

- Prepare your loved ones. This is often overlooked, but it’s incredibly important. You need to ensure that your heirs are ready for the responsibilities that come with their inheritance. You’ll want to ensure that they understand the basics of asset transition, what to do afterwards, and more. Sometimes, updating your estate planning documents is a great excuse to have a family meeting to educate your heirs about your desires.

Simply put, a living trust is a wise move that could help you capitalize your wealth for yourself and your loved ones. If you are wondering how to get started, contact Ciccarelli Advisory Services, Inc. today.