CAS News

Strategic Planning for a Better Memory

Our very own Anthony Curatolo will be a guest speaker during a series of memory workshops developed by Bill E. Beckwith, Ph.D.

Our very own Anthony Curatolo will be a guest speaker during a series of memory workshops developed by Bill E. Beckwith, Ph.D.

Have you ever hunted for your car? Keys? Glasses? Have you ever left home without your grocery list? Have you ever had a senior moment? How do you know if it is a sign of future memory loss? Do you live with or care for someone who is forgetful or has memory loss? If so, this workshop will help. Remembering What Not to Forget is designed for baby boomers, older adults and caregivers of those with mild to moderate memory loss. After completing the workshop, you will have practical and ready to use strategies for improving memory and protecting your future.

You will learn:

- How memory works. The difference between long-term and short-term memory.

- How memory normally changes as we age.

- How to tell the difference between normal aging and memory loss. Stages of change so you can be proactive about your future.

- Strategies for improving memory as you age. What life style changes help and which do not. Strategies for managing financial challenges that may arise.

Upcoming Workshops:

Date: February 25, 2014

Time: 4:00 – 7:00 PM

Date: March 11, 2014

Time: 1:00 – 4:00PM

Where: Hampton Inn, 3210 Tamiami Trail North, Naples, FL

Reservations required.

For more information, contact Anthony at (239) 262-6577![]() (239) 262-6577

(239) 262-6577

Rules Eased for Health FSAs

Recent changes announced by the Internal Revenue Service (IRS) modify the “use-it-or-lose-it” rule that applies to health flexible spending arrangements (FSAs). Plan sponsors will now have the option of allowing participants in health FSAs to carry over up to $500 of unused funds in a health FSA to the following plan year.

Recent changes announced by the Internal Revenue Service (IRS) modify the “use-it-or-lose-it” rule that applies to health flexible spending arrangements (FSAs). Plan sponsors will now have the option of allowing participants in health FSAs to carry over up to $500 of unused funds in a health FSA to the following plan year.

Background

Health FSAs are tax-advantaged employer-provided benefit plans that employees can use to pay for qualifying medical expenses. While generally funded through voluntary employee salary reductions, employers are able to contribute as well. Prior to the start of a plan year, employees decide how much to contribute to the health FSA (the maximum annual employee contribution to a health FSA that is part of a cafeteria plan is $2,500 for 2014). Contributions to the plan are excluded from income for federal income tax purposes, as are any reimbursements made from the plan for qualified medical expenses, including co-payments, deductibles, and dental and vision care expenses.

Any funds left unspent in the health FSA at the end of the plan year are forfeited–this is commonly referred to as the “use-it-or-lose-it” rule. Plan sponsors have the option of providing for a grace period of up to 2½ additional months after the end of the plan year (e.g., a calendar year plan might cover expenses incurred through March 15).

New rules

In Notice 2013-71, the IRS modified the “use-it-or-lose-it” rule that applies to health FSAs:

- Plans may now be amended to allow participants to carry over up to $500 of unused health FSA funds at the end of a plan year.

- Any carryover will not count against the $2,500 limit in the next plan year.

- A plan may allow participants a grace period, as described above, or the ability to carry over unused funds–but not both.

- A plan does not have to allow either the grace period or the carryover option.

- To adopt the carryover option, plans must be amended on or before the last day of the plan year from which amounts may be carried over, and may be retroactive to the first day of the plan year, provided certain requirements, including participant notification, are met.

- Special rules apply to plan years beginning in 2013–these plans may be amended to retroactively adopt the carryover provision at any time on or before the last day of the plan year that begins in 2014.

Word of caution

A health FSA plan can’t have both a grace period and a carryover option, so plans with existing grace periods will have to be amended to remove the grace period feature in order to add carryovers. Plan sponsors should consult carefully with a benefit specialist before taking any action, however, as eliminating an existing grace period feature raises potential issues relating to the Employee Retirement Income Security Act of 1974 (ERISA). IRS Notice 2013-71 itself states that “the ability to eliminate a grace period provision previously adopted for the plan year in which the amendment is adopted may be subject to non-Code legal constraints.”

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

“A Lucky Boy from Buffalo” Booksigning Event

Join Ciccarelli Advisory Services, Inc. for a special booksigning event

featuring the narrative memoir, A Lucky Boy from Buffalo, by author Patrick Blewett.

A Lucky Boy from Buffalo tells the story of a young boy who could not stay in school but could look beyond childhood mistakes, steadfastly love his hard-working family, forge fast friendships, win back the girl he once rejected and capitalize on the uncanny call to challenge – wherever he found it.

For more information on this heartwarming memoir, click here to read the press release.

Wednesday, January 15, 2014 | 5:00 PM

Wine & Cheese Reception

Ciccarelli Advisory Services – Florida Office

9601 Tamiami Trail North

Naples, Florida 34108

A portion of the book sales from this event will be donated to the Jamaica Outreach Program.

Space is limited. To RSVP please call:

239.262.6577 or email Ciccarelli@CAS-NaplesFL.com

“To parents of a rowdy son or an impetuous daughter, this tale will provoke smiles. To youthful readers who march to their own drummer, this book will offer hope.” – Patrick Blewett

Patrick Blewett is not affiliated with FSC Securities Corporation.

2013 Year-End Tax Report

Year-End Tax Moves for 2013

One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current on ever-changing tax reduction strategies. This special report covers the details of many year-end tax strategies for 2013. Remember—every situation is different and not all strategies will be appropriate for you. Please discuss all tax strategies with your tax preparer prior to making any final decisions.

Income Tax Rates for

Income Tax Law Changes

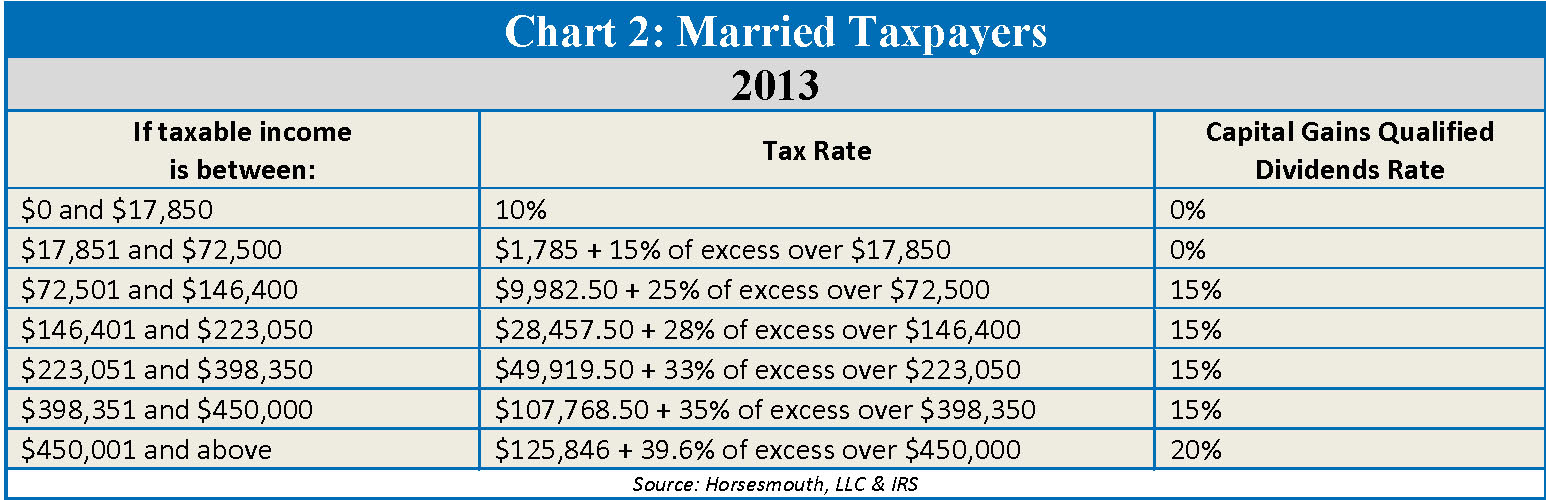

Thanks to the American Taxpayer Relief Act of 2012 (ATRA), taxes rose sharply in 2013. The top marginal ordinary income tax rate for all taxpayers increased from 35% in 2012 to 39.6% in 2013. Additionally, the top marginal capital gains tax rate on long-term capital gains and qualified dividends increased from 15% in 2012 to 20% in 2013.

Medicare Tax

There are two major changes to the Medicare tax. The first is an additional 0.9% Medicare tax on wages and other earned income (such as self-employment income) exceeding certain thresholds. The other more expansive change is a 3.8% Medicare surtax on “net investment income” for wealthy taxpayers. The 3.8% Medicare surtax is on top of ordinary income and capital gains taxes, meaning long-term capital gains and qualified dividends may be subject to taxes as high as 23.8%, while short-term capital gains and other investment income (such as interest income) could be taxed as high as 43.4%!

The Medicare surtax is imposed only on “net investment income” and only to the extent that total “Modified Adjusted Gross Income” (“MAGI”) exceeds $200,000 for single individuals and $250,000 for taxpayers filing joint returns. The chart below shows which types of income are subject to this new Medicare tax.

For those of you who will be subject to this new Medicare surtax, some of the strategies that we can consider will take time to implement. Now is a good time to review your situation. For example, you might:

- Consider investing in tax-advantaged vehicles such as: tax-exempt bonds, qualified retirement accounts, qualified annuities, or cash value life insurance policies (assuming that the cost of acquisition and maintenance does not exceed the tax savings).

- Convert passive real estate activities to active interests.

- Marry someone who has large capital loss carry-forwards, or currently has large net operating losses (NOLs).

For specific ideas, please call our office or bring this up at your next review.

Capital Gains and Losses

Looking at your investment portfolio can reveal a number of different tax saving opportunities. Start by reviewing the various sales you have realized so far this year on stocks, bonds, and other investments. Then review what’s left and determine whether these investments have an unrealized gain or loss. (Unrealized means you still own the investment and haven’t yet sold it, versus realized, which means you’ve actually sold the investment.)

Know your basis. In order to determine if you have unrealized gains or losses, you must know the tax basis of your investments, which is usually the cost of the investment when you bought it. However, it gets trickier with investments that allow you to reinvest your dividends and/or capital gain distributions. We will help you calculate your cost basis.

Consider loss harvesting. If your capital gains are larger than your losses, you might want to do some “loss harvesting.” This means selling certain investments that will generate a loss. You can use an unlimited amount of capital losses to offset capital gains. However, you are limited to only $3,000 of net capital losses that can offset other income, such as wages, interest and dividends. Any remaining unused capital losses can be carried forward into future years indefinitely.

Be aware of the “wash sale” rule. If you sell an investment at a loss and then buy it right back, the IRS disallows the deduction. The “wash sale” rule says you have to wait at least 30 days before buying back the same security in order to be able to claim the original loss as a deduction. However, while you cannot immediately buy a substantially identical security to replace the one you sold, you can buy a similar security—perhaps a different stock in the same sector. This strategy allows you to maintain your general market position while utilizing a tax break.

Sell worthless investments. If you own an investment that you believe is worthless, ask your tax preparer if you can sell it to someone other than a related party for a minimal amount, say $1, to show that it is, in fact, worthless. The IRS often disallows a loss of 100% because they will usually argue that the investment has to have at least some value.

Always double check brokerage firm reports. If you sold a stock in 2013, the brokerage firm reports the basis on an IRS Form 1099-B in January 2014. Unfortunately, there were a number of problems implementing the new reporting rules last year, so we suggest you double-check these numbers to make sure that the basis is calculated correctly and does not result in a higher amount of tax than you need to pay.

Zero Percent Tax on Long-term Capital Gains

You may qualify for a 0% capital gains tax rate for some or all of your long-term capital gains realized in 2013. The strategy is to calculate how much long-term capital gain you would need to recognize to take advantage of this tax break.

The 0% long-term capital gains tax rate has been permanently extended for taxpayers who end up in the 10% or 15% ordinary income tax brackets, which is up to $36,250 for single filers and $72,500 for joint filers. If your taxable income goes above this threshold, then any excess long-term capital gains will be taxed at a 15% capital gains tax rate and/or 20% capital gains tax rate, depending on how high your taxable income is for the year. (NOTE: The 0%, 15% and 20% long-term capital gains tax rates only apply to “capital assets” (such as marketable securities) held longer than one year. Anything held one year or less is considered “short-term capital gains” and is taxed at ordinary income tax rates.)

If you are eligible for the 0% capital gains tax rate, it might be appropriate to sell some appreciated stocks to take advantage of it. Sell just enough so your gain pushes your income to the top of the 15% tax bracket, then buy new shares in the same company. You do not have to comply with the “wash sale” and wait 30 days. With “gains harvesting,” you can actually sell the stock and buy it back in the same day. Of course, there will be transaction costs such as commissions and other brokerage fees. At the end of the day you will have the same number of shares, but with a higher cost basis. Please remember, you must also review your state income tax rules to determine whether or not these gains will be tax-free at the state level.

If you’re ineligible for the 0% capital gains tax rate, but you have adult children in the 0% bracket, consider gifting appreciated stock to them. Your adult children will pay a lot less in capital gains tax than if you sold the stock yourself and gifted the cash to them.

Taxation of Social Security Income

Social Security income may be taxable, depending on the amount and type of other income a taxpayer receives. If a taxpayer only receives Social Security income, this income is generally not taxable (and it is possible that the taxpayer might not even need to file a federal income tax return).

If a taxpayer receives other income in addition to Social Security income, and one-half the Social Security benefits plus the other income exceeds a “base amount,” then up to 85% of the Social Security income could be taxable. The “base amount” is $25,000 for single filers, $32,000 for married taxpayers filing a joint return. A complicated formula is necessary to determine the amount of Social Security income that is subject to income tax. (We suggest using the worksheet in IRS Publication 915 to make this determination.)

Finally, please note that Social Security income is included in the calculation of “Modified Adjusted Gross Income” (“MAGI”) for purposes of calculating the 3.8% Medicare surtax on “net investment income” (as discussed earlier). Therefore, taxpayers having significant net investment income will have more reason to defer Social Security benefits.

Kiddie Tax

When you make gifts to minors, pay close attention to the “kiddie tax.” This tax was tightened up a few years ago, so in more cases investment income earned by minors will be taxed at their parents’ highest marginal tax rate. Generally, the kiddie tax kicks in when a child’s investment income exceeds $2,000 for the year and the child was under age 19 (or under 24 if a full-time college student). It doesn’t matter if the parents claim the child as a dependent. (Details about the kiddie tax can be found in IRS Publication 17, IRS Publication 929 and in the instructions to IRS Form 8615, which are available for free at www.irs.gov.)

Itemized Deductions & Exemptions

Taxpayers are entitled to take either a standard deduction or itemize their deductions on IRS Form 1040, Schedule A. Itemized deductions include, but are not limited to, mortgage interest, certain types of taxes, charitable contributions and medical expenses. Unfortunately, itemized deductions are subject to several limitations. For example, starting in 2013 medical expenses are now deductible only to the extent that they exceed 10% of AGI in any given year. (The deductible was only 7.5% of AGI in 2012, which represents an increase of the deductible by 33% in only one year!) If you or your spouse are over 65, the deduction limit will stay at 7.5% until December 31, 2016.

Many taxpayers don’t have enough itemized deductions to reduce their taxes more than if they take the standard deduction. If you find you miss the threshold by only a small amount per year, it may be best to “bunch” your deductions every other year, taking a standard deduction in the alternate years. The standard deduction for 2013 is $6,100 for singles, $6,100 for married persons filing separate returns, and $12,200 for married couples filing jointly. However, for 2014, it is $6,200 for singles, $6,200 for married persons filing separate returns, and $12,400 for married couples filing jointly.

Confirm that you are taking all available dependent exemptions. It might be best to support your parents to make them dependents. Providing more than one-half of the support of a parent qualifies for the $3,950-per-dependent exemption and the ability to deduct medical, dental and educational expenses incurred for the parent or parents.

Miscellaneous Year-End Tax Reduction Strategies

Prepare a tax projection for 2013 and possibly 2014 to determine which tax bracket you are in. Then make use of the following strategies if they apply to your situation.

- If your itemized deductions/standard deduction and personal/dependency exemptions are greater than your gross income, you will have negative taxable income, with a $0 income tax liability. (This is often the case with seniors who receive tax-free Social Security income.) Thus, it may be prudent to increase your income from negative taxable income to zero taxable income (still zero tax!).

– One way to do this is to do a partial Roth IRA conversion (see later discussion).

– Another option would be to postpone some deductible expenses to 2014, which will increase your taxable income.

- If you are itemizing your deductions in 2013, you may want to consider accelerating some of these deductions before the end of this year (assuming that you have a taxable income this year). You can make your January 2014 mortgage payment in December 2013, maximize your payments of state or sales taxes (for example, by buying big ticket items in December), prepay state income taxes, or pay all your property taxes in 2013 rather than deferring them to 2014.

– Remember the credit card rule: a deductible expense is deducted in the year it is charged against your credit card regardless of the year in which you pay the credit card bill. So, you can still charge a deductible expense in 2013, deduct it on your 2013 tax return and not have to pay for it until 2014. Please remember that interest expense paid on personal debt, which most interest on credit cards is, is not deductible even if you itemize.

It is important to note that some itemized deductions (such as state income taxes, real estate taxes and miscellaneous itemized deductions) are not allowed when computing the “Alternative Minimum Tax” (“AMT”). If you are subject to the AMT, it is often best to delay payment on the disallowed deductions and push them off until 2014 or later tax years (when AMT is no longer an issue). It is always possible you might be able to use the deductions next year. We suggest that you talk with your tax preparer about AMT prior to using any deduction and exemption strategies we have mentioned.

Paying taxes is bad enough. Paying a penalty is even worse. If you face an estimated tax shortfall for 2013, have the extra tax withheld on an IRA distribution. Withheld taxes are treated as if you paid them evenly to the IRS throughout the year. This can make up for any previous underpayments, which could save you penalties.

If you turned age 70½ during 2013, you must take a “required minimum distribution” (“RMD”) from your traditional IRAs and/or qualified retirement plans (such as a 401(k) plan) on or before April 1, 2014. If you do not take out the entire amount of your first RMD by April 1, 2014, you will be faced with a 50% penalty on the amount that you failed to take out. Also, keep in mind that once you start taking RMDs, you will need to take them until you die. Failure to take out the entire RMD in any given year will result in a 50% penalty on the difference between the RMD and the amount you actually took out. (NOTE: If your first RMD is due by April 1, 2014, you will be responsible for taking out two RMDs in 2014. This will often put you in a higher tax bracket in 2014. Therefore, if you need to take out your first RMD by April 1, 2014, you may want to take your first RMD out on or before 12/31/2013.)

Charitable Giving

This is a great time of the year to clean out your garage and give your items to charity. However, please remember that you can only write off these donations to a charitable organization if you itemize your deductions. Sometimes the donations can be difficult to value. You can find estimated values for your donated clothing at http://turbotax.intuit.com/personal-taxes/itsdeductible/.

Send cash donations to your favorite charity by December 31, 2013, and be sure to hold on to your cancelled check or credit card receipt as proof of your donation. If you contribute $250 or more, you also need a written acknowledgement from the charity.

If you plan to make a significant gift to charity this year, consider gifting appreciated stocks or other investments that you have owned for more than one year. Doing so boosts the savings on your tax returns. Your charitable contribution deduction is the fair market value of the securities on the date of the gift, not the amount you paid for the asset, and therefore you avoid having to pay taxes on the profit!

Do not donate investments that have lost value. It is best to sell the asset with the loss first and then donate the proceeds, allowing you to take both the charitable contribution deduction and the capital loss.

Up through December 31, 2013, taxpayers age 70½ and older can transfer up to $100,000 directly from their IRA over to a charity, satisfying all or part of the required minimum distribution (RMD) with this IRA-to-charity maneuver.

Retirement Plans

In 2013, the maximum 401(k) and 403(b) contribution is $17,500 (plus a $5,500 catch-up contribution for those 50 or older by the end of the year). If you are self-employed, you have other retirement savings options. We can review these alternatives with you at your next appointment.

You can also contribute to a traditional IRA and/or Roth IRA for the 2013 tax year all the way up to April 15, 2014. The maximum traditional/Roth IRA contribution is $5,500 with a catch-up provision of $1,000. The traditional IRA deduction phases out depending on your MAGI and whether you or your spouse is covered by a workplace retirement plan. Depending upon your income level, you may be eligible to contribute to a Roth IRA. To determine your best decision, call our office or ask us at your next review.

Roth IRA Conversions

Some IRA owners are considering converting part or all of their traditional IRAs to a Roth IRA. This is never a simple and easy decision. Roth IRA conversions can be helpful, but they can also create immediate tax consequences and can bring additional rules and potential penalties. It is best to run the numbers and calculate the most appropriate strategy for your situation. Call us if you want to review your options.

Step-Up in Basis Rules

If someone gifts you an appreciated asset while he/she is alive, then your basis is the same as the basis of the donor (not the current fair market value). However, if you inherit certain appreciated assets, you receive a step-up in basis to the fair market value as of the date of the decedent’s death. This new cost basis is often much greater than the original basis that the decedent had in this investment. (Some investments, such as tax-deferred accounts like traditional IRAs, do not receive a step-up in basis.)

So, if you’re the one doing the gifting, how do you determine which asset is the best one to give?

- High-basis assets or cash are usually best, especially if you’re in poor health.

- Low-basis assets (properties with big gains) usually aren’t good gifts because gifted assets don’t usually receive a step-up in basis, so the recipient’s basis will be the same as your basis. The recipient will owe capital gains taxes on all the appreciation since you first bought the asset when they decide to sell. Holding such an asset in your estate until you die allows it to pass by way of inheritance, which grants the recipient a step-up in basis.

- Appreciated assets can be much better than cash if you are worried about the recipient spending the money instead of investing it. There are also other ways to reduce the chance that the recipient will sell the assets and spend the proceeds, such as giving through a trust, partnership or other vehicle.

- Appreciated assets can also be a good idea when the recipient is in the 0% capital gains tax bracket.

Estate and Gift Tax Opportunities

In 2013, each taxpayer can pass up to $5,250,000 (minus prior taxable gifts) to children and/or other beneficiaries without having to pay gift and/or estate taxes. Any transfers in excess of the $5,250,000 exemption amount are subject to a flat 40% tax rate. Each $1 of the gift tax exemption you use during lifetime reduces your estate tax exemption by $1. (NOTE: The $5,250,000 exemption amount is for federal gift and estate taxes only. Depending on which state you live in, there could be state gift, estate and/or inheritance taxes imposed.)

Many people believe that with the estate tax exemption set at over $5,000,000 per person, they don’t need to worry about shrewd, tax-wise ways to give wealth. However, these people might want to rethink their strategy. Congress can change the law (and has changed the law in the past), and your wealth could grow faster than expected, thereby subjecting you to estate tax. Nevertheless, before you gift something away, you need to consider the income tax effects of making a particular gift. Giving away the wrong asset can cost your family some unnecessary taxes.

Make use of the annual gift tax exclusion. You may gift up to $14,000 tax-free to each person in 2013. These “annual exclusion gifts” do not reduce your lifetime gift tax exemption. (NOTE: The annual exclusion gift is doubled to $28,000 per recipient for joint gifts made by married couples or when one spouse consents to a gift made by the other spouse.)

Help someone with medical or education expenses. There are opportunities to give unlimited tax-free gifts when you pay the provider of the services directly. The medical expenses must meet the definition of deductible medical expenses. Qualified education expenses are tuition, books, fees, and related expenses but not room and board. You can find the detail qualifications in IRS Publications 950; and the instructions for IRS Form 709 at www.irs.gov.

Don’t give loss property. When you give loss property, the recipient’s basis is the current fair market value. It may be better for you to sell the property and deduct the loss on your tax return, and then you can give the cash proceeds.

Review state gift tax rules. Make sure that any strategies you use also apply to your state. In fact, some taxpayers actually move to another state and establish residency in that state before selling or gifting any property.

Contribute to a 529 plan on behalf of a beneficiary. This qualifies for the annual gift-tax exclusion. Withdrawals (including earnings) used for qualified education expenses (tuition, books and computers) are income tax free. The tax law even allows you to give the equivalent of five years’ worth of contributions up front with no gift-tax consequences. Non-qualifying distribution earnings are taxable and subject to a 10% tax penalty.

Consider the beneficiary’s situation before making a sizable gift. Keep in mind that these gifts may actually backfire tax-wise in some cases. For example, a gift might make a student ineligible for college financial aid, or the earnings from the gift might trigger tax on a senior recipient’s Social Security benefits.

Make gifts to trusts. These gifts often qualify for the annual exclusion ($14,000 in 2013) if the gift is direct and immediate. A gift that meets all the requirements removes the property from your estate. The annual exclusion gift can be contributed for each beneficiary of a trust. We are happy to review the details with your estate planning attorney.

Consider discounted gifts. These are gifts in which the value of the property for tax purposes is less than the current value of the property, usually because there are some restrictions or defects that reduce the value to the beneficiary. Discounted gifts can be made to trusts or other vehicles. Discounted values are often 20% or more.

A gift that exceeds the annual exclusion gift either reduces your lifetime gift/estate tax exemption or it is subject to current gift tax. If you make a taxable gift, the IRS requires a gift tax return to be filed so it can track the reduction in your lifetime gift/estate tax exemption and also track any lifetime gift taxes you might pay. You should consider filing a gift tax return even when one isn’t required in order to hold the IRS to the three-year statute of limitations (there is no statute of limitations when no return is filed, so the IRS can come back years or decades later, argue that the property was undervalued, and impose a lot of penalties and interest on you or your estate). The gift tax return is IRS Form 709 which is available with instructions for free at www.irs.gov.

Conclusion

Are you having trouble keeping up with changes in the tax laws? In April 2011, IRS commissioner Shaulmen reported that there have been about 3,500 tax law changes since the year 2000. Remember, it was Albert Einstein that said, “The hardest thing in the world to understand is the income tax.” He said that way before it became a whopping 25-volume edition with over 70,320 pages.

Here are some numbers directly from the IRS; the average taxpayer who files an IRS Form 1040 needs about 23 hours to prepare the return. America spends more than 7.6 billion hours and over $193 billion each year just to figure out what taxes we owe—more than the hours used to build every car, van, truck and airplane manufactured in America.

One of our primary goals is to keep clients aware of tax law changes and updates. This report is not a substitute for using a tax professional. Please note that many states do not follow the same rules and computations as the federal income tax rules. Make sure you check with your tax preparer to see what tax rates and rules apply for your particular state.

There are many other additional tax reduction strategies that will vary depending on your financial picture. We encourage all of our clients and prospects to come in so that we can review your particular situation and hopefully take advantage of those tax rules that apply to you. We look forward to seeing you soon.

The views expressed are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. This article is for informational purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice as individual situations will vary. For specific advice about your situation, please consult with a financial professional. Contents Provided By MDP, Inc. Reviewed by Keebler & Associates. Copyright 2013 MDP, Inc.

When a Long Term Care Facility Must Be Selected

Kim Ciccarelli Kantor | Naples Daily News | December 11, 2013

There could come a time when the selection of a nursing home is necessary. Aside from what is generally a stressful and emotional time for the family, a “special needs” family member requires proper decisions made on their behalf.

Nursing home care can range from skilled to intermediate to custodial care. Nursing homes are for individuals who cannot do things for themselves. It is possible that the family is forced to choose a nursing home because a family member is being discharged from a hospital, and needs full-time care. Regardless of the circumstances, the selection of a nursing home can be one of the most expensive and ill-informed decisions a consumer can make. Often, families or caretakers are facing the selection of a nursing home during a time of crisis and have time constraints that hamper a well informed decision. The selections may be limited depending on the geographical area and/or financial capabilities. Families should become aware of the type of facilities available should the need arise, regardless of whether the requirement is an interim stay or a permanent stay.

First, contact the area agency on aging, county departments of social services, or other senior housing referral sources. In our offices, we try to maintain information on retirement communities and full care homes for our clients. Lifetime care is an integral part of a family’s financial and estate plan. There are several choices you could look at:

- Senior retirement housing

- Personal care boarding homes

- Adult foster care

- Homemaker services

- Home health care

- Home and community-based services

The type of setting you choose will be dependent on your special needs, the family member’s physical health, and mental ability; you will want to carefully select just the right setting for your loved one.

Some of the steps you may want to start within your search could include:

- Visiting the retirement community and meeting personally the administrator and the staff. This should help you determine how they work with the people for whom they are caretakers.

- Studying the general appearance and cleanliness of the community. Is it a pleasant environment?

- Inquiring about the size of the staff, the turnover employment rate, their qualifications, and how well they like their work. Determine how many staff per residents, and if round-the clock care is available, and if needed, at what additional fee.

- Observing the general activity and care of the residents.

- Visiting the community around meal time to see the quality and palatability of the food served to the residents, noting the dining area’s attractiveness.

- Consider the visiting hours available to guests and family, accessible outdoor area for residents, availability of telephone, and wheelchair accessibility. Is it a secure facility from the standpoint of security, as well as for the resident’s protection from wandering, etc.?

- Other questions to ask may be related to the variety of programs and activities available for residents, both with the home and as a field trip.

An important part of caring for a family member who is living at the nursing home is the family’s participation in patient care conferences.

Federal law provides for a nursing home resident’s “Bill of Rights” and a list of these rights, not a summary, should be provided when the individual becomes a resident of the home. These rights are designed to insure the dignity and respect of the resident. The contract with the home should make reference to the resident’s rights. Other considerations should include Medicare acceptance, medical consents, the use of blanket waivers, responsible party(s), the admission agreement, transfer and discharge policies, bed-hold policies, notice time of any changes, and grievance procedures.

Begin doing your homework early on so you as a family may become comfortable with your planning when and if the need arises for nursing home care.

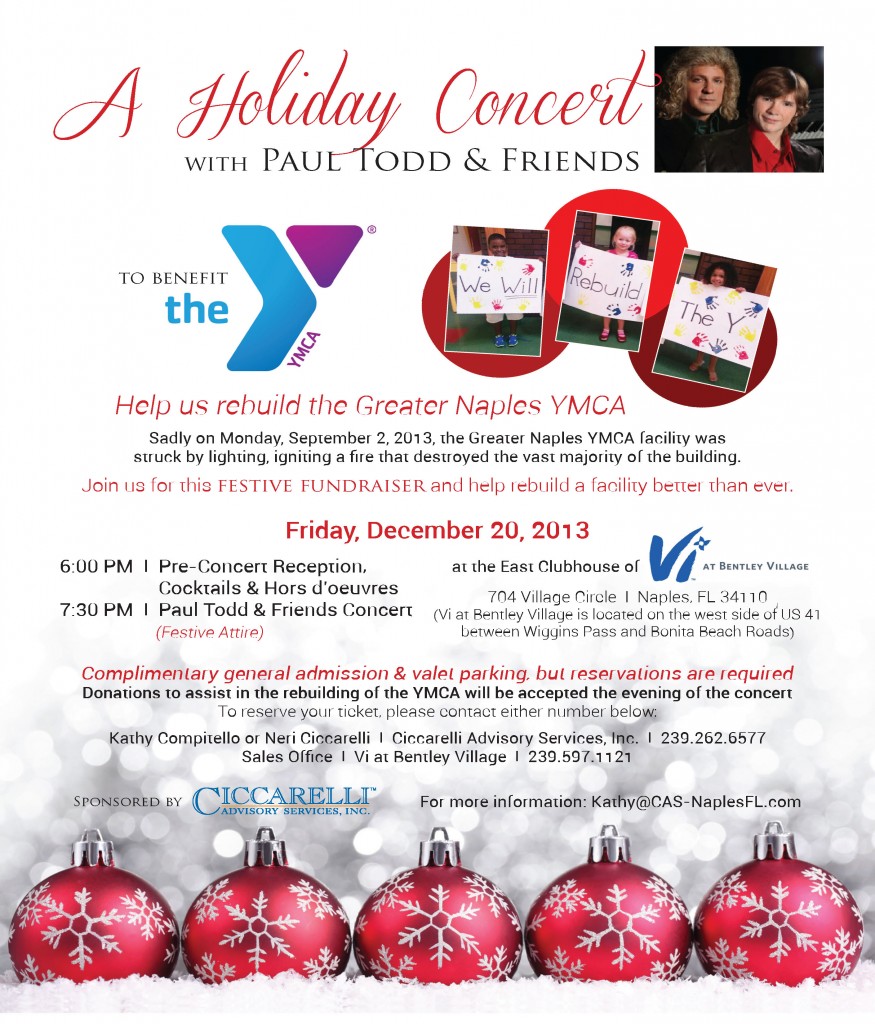

A Holiday Concert with Paul Todd & Friends to benefit the Greater Naples YMCA rebuilding

On September 2, 2013, lightning struck the Greater Naples YMCA, igniting a fire that destroyed the vast majority of their building. You’re invited to a festive fundraiser on December 20th, starring Paul Todd & Friends, and together we can rebuild a facility better than ever. For more details, click on the invitation below…

For directions to Vi at Bentley Village, click the map below…

For more information regarding the tragedy at the YMCA and their efforts to rebuild, click on their brochure below…

For more information on donating to the Greater Naples YMCA rebuilding fund, contact Kathy Compitello at (239) 262.6577

Teaching young children about money

Kim Ciccarelli Kantor | Naples Daily News | November 15, 2013

When I was young, learning about money was a natural occurrence in our household. My parents insisted we learn about being Entrepreneurs, and we learned that knowledge itself could create wealth. Early on, we were encouraged to read and write and were compensated accordingly – $1.00 for a poem, $5.00 for a book report. We were given incredibly large zllowances. With this money, we were responsible for our school lunches, our supplies, and recreational activities. Each of us quickly developed spending or saving habits. These habits form when children are young, and it is our responsibility as parents to help our children learn the value of money. As soon as children can count, introduce them to money. Take an active role and regularly communicate, as they grow, about your values, money and how to save it, make it grow, how to use it sensibly and most importantly, how to spend it wisely. Support your children in developing good spending decisions and learning the difference between needs, wants and wishes.

Children can absorb information quickly, and it is with perseverance we teach them the concept of compound interest. Encourage them to save. Pay interest on their savings or develop a matching program. If you give your children an allowance, say – $5.00, give it in such a way that makes saving easier. If five $1.00 bills are given, then encourage one $1.00 to be saved. The amount is not important; developing the habit is.

Teach your children/grandchildren priority spending. If they have $10.00 to spend today, what could they buy if they chose to save? Teach your child to do his homework and compare for value, quality, quantity, etc.

Encourage young people to make spending decisions, whether good or poor, and then encourage a discussion of pros and cons — before spending takes place. Teach children about spending by choice, choosing from several items, and then narrowing those choices once the decision to spend has been made.

Helping your child evaluate media and marketing ads and differentiate between expense and value can be a worthwhile education to their money success in the future. Daily, our children are encouraged to spend. Oftentimes, the item is not even needed or wanted, but nonetheless, we buy. Equally important is the ability to use credit wisely. Alert young people to the dangers of buying and paying interest. Charge interest on small loans you make to them so they can learn how to evaluate the cost of renting someone else’s money. For example, buying a bike for $499 over 18 months at 18.8% interest or $31.85 per month really means a true cost of $575.00 for the bike. In actuality, the cost is higher. The loss of earnings on the child’s money has to be also calculated. If $31.85 per month was saved at an interest rate of 6.0%, the total would equal about $620 after 18 months. The child could then pay $499 cash for the bike and still have $121 in savings.

Credit cards for young children can be a learning experience or a disaster. Emergency use can be helpful, or having a credit card to establish good credit is fine, but a child should learn that credit cards should not be used for cash advances, or “wants” when the money is not available to pay cash. The National Center for Financial Education (www.nationalfinancialeducationcenter.org), offers books and resources for young children and young adults that encourage proper education. These are great birthday gifts or Christmas stocking stuffers.

Establish a regular schedule for a family discussion about finances. Topics can include spending, use of credit, savings, investment growth, and the effects of the earning. Be creative. Above all, teach your children/grandchildren that money is relatively unimportant, and the way to keep it this way is to have it, respect it, so that we may concentrate our energies on the real priorities of life. Help to assist your children/grandchildren to develop a net worth, cash flow statement and implement a spending plan. The basics will remain through their lifetime. The differences will mostly be in adding zeroes to the numbers as the years go by.

Good luck! Good Teaching.

Kim Ciccarelli Kantor, CFP® CAP™ is president and founder of Ciccarelli Advisory Services Inc., a Family Focused Wealth Management Firm in Florida and New York.

Be charitable, but be smart in your gift-giving

Kim Ciccarelli Kantor | Naples Daily News | October 24, 2013

Donor gifts come in all forms: artwork, furniture, clothes, stocks and cash, to name a few.

Some donors create charitable trusts for future gifting, and others create a continued legacy through a family foundation or community foundation family fund.

Are you making direct gifts or leaving a bequest by will? If so, it will benefit you to review the many charitable giving plans available. By creating your own specifically designed philanthropic plan, more significant benefits might pass to your selected charities, with a greater personal fulfillment for the family.

Gifting through a donor advised fund is one such example. This DAF, coordinated with a charitable remainder trust, provides tax benefits and current income. If desired, the DAF can continue as an endowment after your lifetime to involve your children and grandchildren in philanthropy.

The key is to discuss your wishes first, then discuss options best suited to your needs with a competent adviser versed in charitable planning.

A Charitable Reminder Trust, for example, is a split-interest trust. More than one beneficial interest exists in the trust. One interest belongs to income beneficiaries who receive income for their lifetimes.

The second interest are charitable organizations named to receive the assets after the death of the last surviving income beneficiary.

If your trust already exists, the second interest beneficiary can be updated to a modern day DAF.

And, to ease any administration or due diligence, more clearly focusing the family’s efforts on the charitable work, a local community foundation can partner with you to accomplish what is most important.

The trust is a complicated document, but a flexible, useful document for your philanthropy. The design world of trusts is anything but limiting.

A CRT is a tax-exempt entity. As a general rule, income taxes and estate taxes are not paid by the trust. This permits a tax-efficient method for investing portfolio assets. There is generally no tax on property transferred to a trust.

An exception would be the transfer of your IRA or deferred annuity assets during your lifetime. The trust is irrevocable and the ultimate beneficiary is your designated charitable organization. This organization might be your DAF. Proposed tax laws might adjust the amount of available deduction, so be sure to check with your advisors before proceeding.

As income beneficiary, you have two choices for income: receive a fixed income yearly amount (annuity trust) or a defined percentage of the value of the CRT assets (a unitrust). Once established, additional future gifts can be made only if you select a unitrust.

An annuity trust or unitrust, might invade principal to pay out the income beneficiary, but care must be taken that a charity ultimately will benefit. Additional trust designs apply if you wish to defer cash flow from the trust, or wish not to invade principal.

The creator – you – may retain the right to change charities that ultimately benefit from your kindness. This gives you a flexible, lifetime customization plan for favored charities. You also might consider a donor advised family fund as beneficiary under the local community foundation. The ease to update beneficiaries or define a special interest gift can be captivating.

A community foundation removes the administrative burden of planning a continuing endowment for several charities, or distributing desired gifts. A DAF can accept the gifts from your CRT at the last income beneficiary’s death.

Kim Ciccarelli Kantor, CFP® CAP™ is president and founder of Ciccarelli Advisory Services Inc., a Family Focused Wealth Management Firm in Florida and New York.

Shutdown? Default? Consequences?

It’s possible that you’ve heard a news report or two about the government shutdown that started October 1, and now a dispute over raising the U.S. debt ceiling and possibly defaulting on the government’s debt obligations as soon as October 17. The question for an increasingly nervous investing public is: how will this affect the U.S. economy and (not to be too selfish here) my retirement portfolio?

Interestingly, it is starting to look like the government shutdown, if it runs for weeks instead of months, might have almost no effect on the economy at all. Why? The economic impact that had economists worried was the loss of income suffered by tens of thousands of federal employees. But the Defense Department has continued paying all of its civilian personnel, simply by declaring all of them “essential employees.” Not only were the leaders of the House of Representatives not inclined to argue; they have quietly passed legislation that would give back-pay to all federal workers who have been furloughed, just as soon as the stalemate ends. The Senate and the President are likely to go along, giving the country the worst of all worlds: paying most government employees for staying home and not providing a wide variety of services to the public.

Ironically, the way the politics are working, one can almost guarantee that there will be some kind of a stock market selloff before the shutdown ends. For the Republican leaders in the House, there is little cost to holding their ground so long as there is not a public outcry and loss of voter confidence. One of the sources of that pain would be a big drop on Wall Street. Indeed, if you listen closely to the speeches by President Obama and the Democratic leadership, you hear dire warnings that the of a market drop as a result of the shutdown–which is their way of focusing the public’s attention on who to blame when it happens.

What is interesting about that is that the markets often deliver corrections after long, accelerating uptrends like what we have experienced in the U.S. since March of 2009, and with the 20+% returns that Wall Street has delivered so far this year. It wouldn’t have surprised anyone to see some kind of a quick downturn this Fall regardless of whether the government was operating at full capacity or at a standstill. A week of small leaks in stock prices could lead to something larger as people realize they are sitting on nice gains and have no idea what Congress will or won’t do next. The last time the government was shut down, stocks dropped 20%, the Republican leadership realized it wasn’t winning any popularity contests and the stalemate ended. We’ve seen this script before.

A more consequential issue is the debt ceiling. Congress must raise the total amount that the U.S. government can borrow (by selling Treasury bonds) to pay its various obligations, including, of course, interest on its current Treasury bonds. Contrary to popular belief, raising the debt ceiling does not increase the federal debt; that debt exists whether or not Congress authorizes additional borrowing.

Failure to authorize the government to pay its legal obligations would create a self-induced fiscal crisis–ironic for a country whose representatives claim that they never want to become another Greece, and then talk about voluntarily defaulting on the nation’s debt obligations, which even Greece has avoided.

One recent article suggested that a default on Treasuries would ripple through the global economy, among other things, causing anxious investors to demand higher interest rates and dramatically raising U.S. borrowing costs. That, in turn, would raise rates on mortgages, credit cards and student loans, pushing the U.S. toward or into recession and putting pressure on the stock market. One report suggests that if the U.S. misses just one interest payment, the downward impact on stock prices would be greater than the Lehman Brothers bankruptcy. In THAT aftermath, the stock market lost half its value.

Bigger picture, a default would undermine the role of the U.S. in the world economy.

The irony of the debt ceiling debate is that the gap between government spending and tax revenues has been closing rapidly on its own. In July, the Congressional Budget Office reported that the deficit had fallen by 37.6%, the result of tax increases and sequester-related cuts in spending. As a percentage of America’s GDP, the deficit has fallen from more than 10% at the end of 2009 to somewhere around of 4% currently. Last June, the government actually posted a surplus of $117 billion, paying down the overall deficit, and the Congressional Budget Office has projected that September will also bring government surpluses.

Most observers seem to think that all of this will get worked out. After all, what rational person–in Congress or elsewhere–wants to self-impose these problems when we have plenty of economic challenges already? The stock market’s calm trading days tell us that investors expect a compromise on the government shutdown in the near future. It may take a sharp day of selling to prod Congress off the dime. Foreign investors are still lending to the U.S. government at astonishingly low interest rates (despite modest increases over the past week), which tells us they aren’t worried about a default.

The last time we went through this, the stock market plunges proved to be buying opportunities for investors. One of the great things about uncertainty and volatility is that it causes investments to periodically go on sale, and creates such anxiety that only disciplined investors are able to take advantage. There’s no reason to think this isn’t more of the same.

Sources:

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/10/06/maybe-the-government-shutdown-wont-clobber-the-economy-after-all/

http://www.cbsnews.com/8301-505123_162-57606253/debt-ceiling-understanding-whats-at-stake/

http://krugman.blogs.nytimes.com/2013/08/13/what-people-dont-know-about-the-deficit/

http://www.moneynews.com/newswidget/default-Catastrophe-lehman-demise/2013/10/07/id/529564?promo_code=125A8-1&utm_source=125A8Moneynews_Home&utm_medium=nmwidget&utm_campaign=widgetphase1

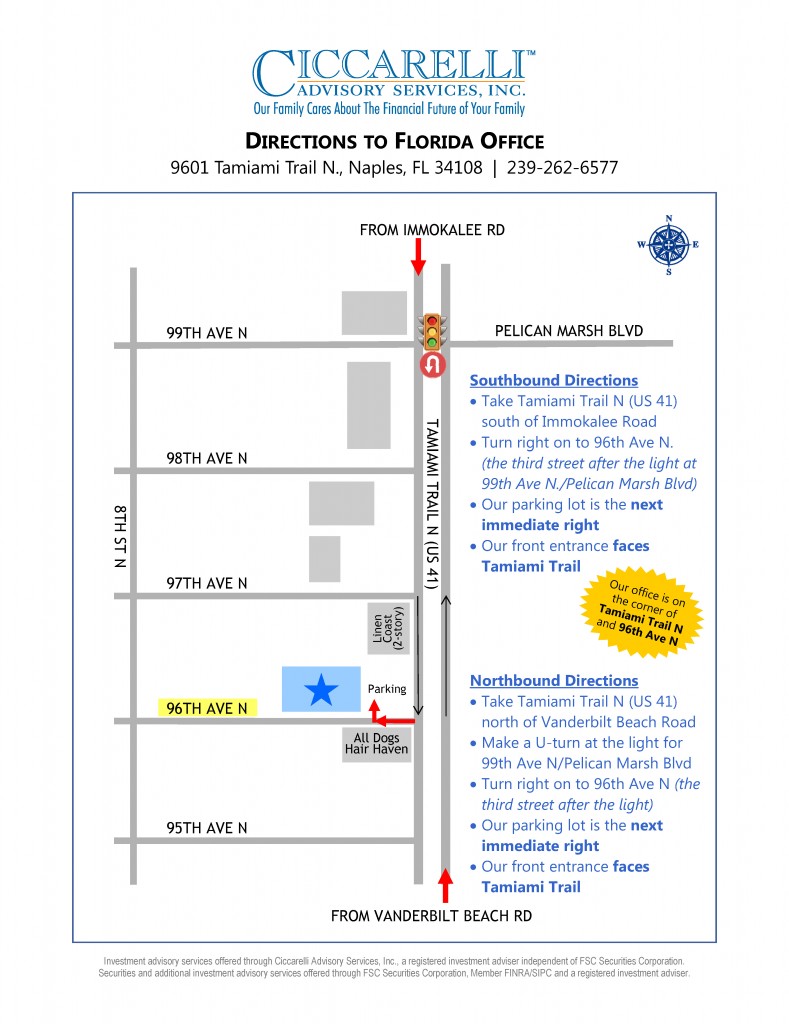

Our Florida Offices Have Combined, and Moved!

We are proud and excited to announce that we at the Florida offices of Ciccarelli Advisory Services have purchased a building of our own! We found a once-in-a-lifetime opportunity and acquired a property that is centrally located between our previous offices in Naples and Bonita Springs.

You know how exhilarating and thrilling it is to move into a place and make it “yours”! Over the past month we painted, carpeted, decorated; in other words, made our new home your new home.

We are especially excited and privileged to be able to serve our Southwest Florida families from one central location, as well as continuing to serve those families who may be located farther away. Our new location is at 9601 Tamiami Trail North in Naples, Florida 34108. Our telephone number is 239.262.6577 and our fax number is 239.649.6315.

We think you will be delighted with our new location and we look forward to having you visit, whether it is in person or through our website (www.casmoneymatters.com) and Facebook page (www.facebook.com/CiccarelliAdvisoryServicesInc).

Please feel free to reach out to us by telephone or email with any questions you may have.

Click on the image below for a map to our new location.