CAS News

SPELLIFE Women’s Wellness Summit

CAS is a proud sponsor of the 3rd annual SPELLIFE Women’s Wellness Summit on Saturday, April 2, 2016 from 9:00 AM – Noon in Naples, Florida. The SPELLIFE Summit is an annual women’s wellness event dedicated to sharing the knowledge and services within our community that help women live physically, emotionally and financially richer lives. Their mission is to inspire women to a proactive and preventative approach to life, using dynamic speakers, valuable community resources, and services that center around the eight dimensions of wellness: Spiritual, Physical, Environmental, Leisure, Local, Intellectual, Financial and Emotional. This year’s summit is centered on the theme of “Brain Power,” featuring keynote speaker Dr. Jill Bolte Taylor, a Harvard-trained neuroanatomist, TED Talk Presenter and author of the New York Times bestseller, My Stroke of Insight. Tickets and more information available at: https://SLWWS2016.eventbrite.com

CAS Profiles – Jessica Barton (Florida)

Jessica joined the Ciccarelli Team on September 20, 2010, as a Client Service Associate to Lynn Ferraina. Over the years, her responsibilities have grown to also include Graphic Design and Marketing for the firm. Jessica (a.k.a. Jess) brings joy and humor to our Florida office with her delightful wit and positive outlook, so it is no surprise her favorite quote is “A day in which we have not laughed is a day that is wasted,” by Nicholas Chamfort.

Jessica joined the Ciccarelli Team on September 20, 2010, as a Client Service Associate to Lynn Ferraina. Over the years, her responsibilities have grown to also include Graphic Design and Marketing for the firm. Jessica (a.k.a. Jess) brings joy and humor to our Florida office with her delightful wit and positive outlook, so it is no surprise her favorite quote is “A day in which we have not laughed is a day that is wasted,” by Nicholas Chamfort.

Jessica was born in Kansas City, Missouri. Her family moved to Naples when she was six and her father and brother still continue to live locally. Her pride and joy are her two dogs, Henry Higgins and Holly Golightly, both named after characters in movies starring Audrey Hepburn. Jess loves adventure, including backroad trails and geocaching. As an active participant in her church, Jessica leads the music program and is instrumental in the church’s marketing and website design. If not in finance, Jessica would have pursued ministry. She describes working at CAS as “A blessing…and never boring,” and her keys to success are authenticity and the search for truth in all situations.

Jessica is not registered with FSC Securities Corporation or Ciccarelli Advisory Services, Inc.

Economic Update – Fourth Quarter 2015

Investor Update: Shortly after this economic report was written, equity markets experienced an unusually turbulent start to 2016. Experts feel that this recent market volatility is in reaction to a slowdown of growth and further currency devaluation in China combined with continued oil price weakness. As advisors, we are trained to make non-emotional decisions and the advice we offer clients is based on their personal situations. Our goal is to continue to carefully monitor the markets for our clients and keep a regular line of communication. If you need to talk with us prior to our next scheduled meeting, please call our offices.

When the final day of trading closed on New Year’s Eve, the U.S. stock market finished a disappointing year for investors. Despite all the optimism that 2015 began with, there was limited, if any, joy by year end. The Dow Jones Industrial Average lost 2.2% for the year and the Standard and Poor’s 500 index was down 0.7%. This annual drop was the first since 2008. The NASDAQ was one of the only bright spots, gaining nearly 6% for 2015 despite the small-cap Russell 2000 index falling 5.7% and down 12.3% from its peak. (Source: Barron’s 1/4/2016, USA Today 12/31/2015)

When the final day of trading closed on New Year’s Eve, the U.S. stock market finished a disappointing year for investors. Despite all the optimism that 2015 began with, there was limited, if any, joy by year end. The Dow Jones Industrial Average lost 2.2% for the year and the Standard and Poor’s 500 index was down 0.7%. This annual drop was the first since 2008. The NASDAQ was one of the only bright spots, gaining nearly 6% for 2015 despite the small-cap Russell 2000 index falling 5.7% and down 12.3% from its peak. (Source: Barron’s 1/4/2016, USA Today 12/31/2015)

Starting the year 2015, market strategists were looking for a 10% or higher rise in stocks. The final results of 2015 concluded a roller coaster year, to which many investors will likely say, “good riddance.” The U.S. dollar aside, most asset classes didn’t fare well.

Four factors that contributed to the weakness of stocks this year were: a further and unexpected decline in commodity prices, particularly oil; continued strength in the dollar; soft economic growth and a currency devaluation in China; and a Federal Reserve that only in December felt confident enough about the U.S. economy to begin raising interest rates. A year ago, many analysts expected that to happen as early as the first quarter of 2015.

“These cumulative head winds became too much….there was a deeply rooted fear that China’s growth might hit a wall,” says Thomas Lee, head of research at Fundstrat Global Advisors. “The market had a hard time standing up to all that.”

“Most people thought it would be a better year,” says Kate Warne, investment strategist at Edward Jones. After all, the S&P 500 index hit an all-time high of 2,131 in May. However, since August investors have been subject to heavy volatility.” (Source: Barron’s 12/19/2015)

Moving into 2016, caution still remains the top priority for most investors. Many analysts are still staying positive about the prospects for U.S. stocks in 2016, however, most reports conclude they are still bullish, but cautious. In their annual survey of prominent market strategists at big banks and investment firms, Barron’s found that this group expected moderate gains for the year ahead. (Source: Barron’s 12/14/2015)

Equities are not intended as an investment vehicle for investors with time horizons of one year, so any one-year projection can easily be wrong. The analysts Barron’s surveyed in 2015 were incorrect, so before we look at 2016, it might be helpful to review some key highlights from 2015.

A Review of 2015

A Review of 2015

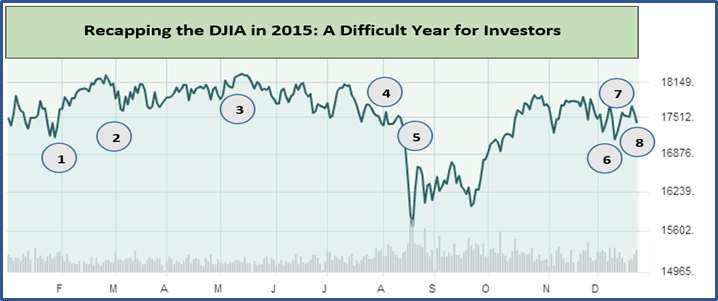

The year 2015 was a difficult one for investors. A brief review of some interesting events are spotlighted on the chart of the Dow Jones Industrial Average’s (DJIA) course during the year. As the recapping chart shows, the year began on a good note following a strong performance for investors in 2014. Interest rates were a major story all year and on February 2nd the 10-year Treasury yield made a low for the year at 1.67% (data point 1 on the chart).

Most investors enjoyed the bullish momentum during the 1st quarter and on March 13th, the U.S. dollar surged to a new high (data point 2 on the chart), which was later eclipsed (Source: Barron’s 12/14/2015)

In May, the Dow Jones Industrial average reached an all-time peak of 18,321 (data point 3 on the chart) and investors were still enjoying market gains. As the chart shows, the first half of 2015 was a mild one and many investors entered the summer in an encouraging mode.

China stunned the world’s financial markets on August 11th and 12th by devaluing its currency for two consecutive days, triggering fears its economy was in worse shape than investors believed (data point 4 on the chart). The Chinese authorities acted after a string of poor economic figures showed that previous efforts to boost exports and growth against the headwind of an overvalued currency had failed. As a result, the Yuan hit a 4-year low. A cheaper Yuan was sought to help Chinese exports by making them less expensive on overseas markets.

Many experts asked, why did the Chinese government do this? The most common answer was that despite the Chinese economy being the second largest in the world, after the U.S., it had been underperforming for the past year or so, according to Loren Brandt, a professor at the University of Toronto’s department of economics. So they clearly felt they had to do something to get exports moving again. “This is kind of a normal course of action that is seen in most weak economies,” Brandt says. “Their exchange rate adjusts and it provides a margin with which to try to help the economy recover.”

In 2014, China’s economic growth fell to 7.4%, a noted drop off from years of double-digit growth. China’s slowed economy made this type of action unsurprising to Brandt, who says it was a question of when, not if, the government would intervene. This measure was taken as a way to stimulate the Chinese economy which was still growing, but not at the pace that was previously anticipated. (Source: The Guardian 8/12/2015)

August 2015 was a challenging month for investors. For the first time in over 6 years, equity investors experienced a correction. On August 25th (data point 5 on the chart), U.S. stocks bottomed out for the year after a 12% correction. Fears of slowing global growth fueled the downturn and volatility had returned to the markets in a considerable way. (Source: Barron’s 12/14/2015)

Although the markets stayed volatile for the next three months, they clawed back some lost ground and on December 11th (data point 6 on the chart) WTI crude oil hit a six-year low of $35.62 a barrel. This meant a 33% price plunge for 2015. The drop in oil prices rewarded consumers at the pump, but punished energy stocks and investors as oil and energy related company share prices were hit hard.

For the entire year investors asked, “will they or won’t they” raise interest rates each time the Fed’s policy committee met. This was the most watched event throughout 2015 for investors. On December 16th, (data point 7 on the chart) Janet Yellen ended all of the debates that dominated investor discussions since December of 2008 when the central bank set its Federal funds target rate at 0% to 0.25% by raising that range by 25 basis points to 0.25% to 0.50%. This long awaited and much predicted rate increase was the first increase in interest rates and marked the end of an era of near 0% rates. (Source: Barron’s 12/21/2015)

Finally, by the year end (data point 8 on the chart), the Dow Jones Industrial Average finished the year down 2.2%, disappointing most analysts and investors.

Warren Buffet perform in 2015?

Warren Buffet perform in 2015?

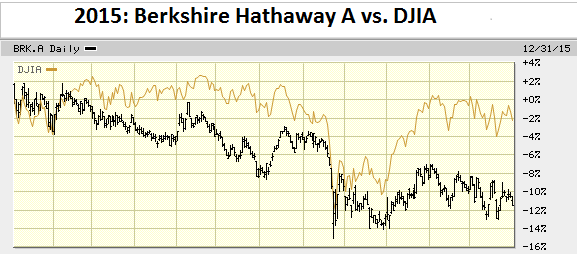

Many investors suffered losses and had a rough year in 2015. Legendary investor Warren Buffet, through his holding company Berkshire Hathaway, has mightily underperformed the S&P 500 in 2015. His flagship BRK.A shares were down 11.47% compared with a 2.2% decrease in the DJIA. The media noticed as the Financial Times trumpeted “Buffett’s Worst Year Since 2009″ in a headline Wednesday, December 30th. (Source: Forbes 12/31/2015)

Indeed, 2015 was a rough year for conservative and value oriented investors like Mr. Buffet. As Investorplace.com reported, Berkshire Hathaway may have struggled in 2015, but that doesn’t mean the Oracle of Omaha has lost his touch. They reminded investors that although it shouldn’t need repeating, Warren Buffett is a long-term investor. They accurately report that the review of his one-year performance is more noise than signal because the data sample is far too short. They challenge investors to review his 5 year or longer term results. (Source: Investorplace.com)

His performance is so extraordinary it puts Warren Buffett in a super-elite pool, one that holds less than 1% of the population of investors, according to an analysis by Salil Mehta, a statistician and econometrician.

Still listed as one of the wealthiest men in the world, this was not Buffet’s first rough year; 2008 was also a bad year for Buffet and his holding company, Berkshire Hathaway. Buffett seeks out businesses that exhibit favorable long-term prospects. His timeframe is longer than one year, so like most good investors no one year dictates his success or lack thereof. Buffett says, “if you don’t feel comfortable owning a stock for 10 years, you shouldn’t own it for 10 minutes.” Buffet feels that the stock market will swing up and down, but in good times and bad, he stays focused on his goals. This is a great lesson for all investors. (Source: Investopia.com)

2016 Outlook

A big question on the mind of all investors: where is the currently erratic U.S. stock market headed in 2016?

Obviously no one will know till year end, but currently, not a single Wall Street stock strategist is calling for a complete bear market, or 20% drop. If they are right, the bull market will turn seven in March and stocks — which have tripled in value since March 2009 — will keep chugging higher. However, they say there’s a chance investors will see a replay of 2015 and the market could again trade sideways and deliver almost flat returns. That’s the takeaway from year-end 2016 S&P 500 price targets from 17 Wall Street strategists. The predictions range from a high of 2,360 — or 15.5% above the year-end close — to a low of 2,100, which equates to a gain of just 2.7%. Brian Belski, Chief Investment Strategist at BMO Capital Markets, feels that the U.S. stock market is in year seven of a 20-year secular, or long-term, bull run. What he is saying is that the S&P 500 will likely see a “cycle high” and suffer a “corrective phase” in 2016 that will leave the S&P 500 up just slightly at year end. “2016 could likely be bumpy,” Belski warned in his 2016 Outlook. As a reminder, the S&P 500 finished 2015 with a 0.7% loss for the year. (Source: USA Today 12/31/2015)

Here are some specific areas investors should watch in 2016:

Interest Rates

Now that the Fed has increased rates for the first time in seven years, almost every financial analyst and publication has a prediction for interest rate movements in 2016. For now, investors can expect more “will they or won’t they?” drama from the Federal Reserve.

The staff of Fortune magazine recently assembled its predictions for 2016. They forecast that the federal funds rate at the end of 2016 will be 0.5%, up from 0.25%. They expect the Federal Reserve to raise its interest rate targets once in 2016—but only once, as U.S. economic growth stays steady but slow, while inflation and wage growth also remain modest. Fortune sites that fears of seeming “political” during a presidential election year, sluggish growth in the Eurozone and a slowdown of the Chinese economic juggernaut will keep Janet Yellen and the rest of the Federal Open Markets Committee from pulling the trigger more often. They predict the Fed’s vacillation will be one of the year’s longest-running (and least loved) dramas. (Source: Fortune, 12/14/2015)

It is anyone’s guess when the Fed will raise interest rates and by how much. In December, Federal Reserve Chairperson Janet Yellen stated that “The committee expects economic conditions will evolve in a manner that will warrant only gradual increases in the federal-funds rate.”

As for rates paid on bank deposits, they are not getting off the floor just yet. Barron’s writes that “investors should not look for money market yields to rise enough to be discernable without a magnifying glass.” For 2016, interest rates are an issue that investors need to keep a watchful eye on. (Source: Barron’s 12/21/2015)

China

China is still one of the world’s largest and strongest economies. Both the Chinese economy and their stock markets are areas for investors to monitor in 2016. “In many countries the stock market can be seen as a leading indicator of the economy. But that is not true in China,” wrote Jeffrey Kleintop, Chief Global Investment Strategist at Charles Schwab. “You really can’t get any less related than the Chinese stock market and its economy.” Investors are encouraged to focus less on gyrations in China’s stock markets, and to pay more attention to the country’s economy. There, a gradual, expected slowdown is taking place.

Experts have known for a long time that China’s growth would slow as Beijing made reforms designed to shift the country away from building roads, railways and housing to generate growth to an economy powered by consumer spending. That’s happening now and economists expect a final growth of 6.8% in 2015, and around 6.5% this year. China is a far cry from the potent days when it posted GDP growth of 10% on a regular basis. But it should also be strong enough to maintain employment levels as difficult reforms are implemented. Slowdowns in China can have impacts on investors worldwide and investors need to pay attention. (Source: CNN Money 1/5/2016)

Oil

Oil prices were at highs of $100 per barrel in June 2014. Since then they have retreated to a new multi-year low of about $35 per barrel in December. While this rewarded consumers at the pump, there have been more than 200,000 oil related layoffs in 2015 and there are more projected for 2016. The energy industry has idled more than 1,000 rigs and slashed more than $100 billion in spending this year to cope with the bust, according to Bloomberg. More than 250,000 energy workers from around the world have lost their jobs since the start of the downturn. (Source: Houston Press 12/30/2015)

Energy and oil related stocks suffered big losses in 2015 and analysts are mixed on whether they will rise or continue to drop in 2016. The fluctuation of oil prices is another subject that investors need to monitor this year.

Corporate Earnings

Price-to-earnings (P/E) ratios are still a key factor in the valuation of equities for many analysts. According to Jurrien Timmer, Director of Global Macro at Fidelity Investments, the outlook for 2016 really seems to be more of an earnings question. The U.S. earnings cycle peaked in early 2015, profit margins are near record levels, and more than half of corporate earnings are coming from share buybacks. He feels that it remains to be seen what we can expect from earnings growth in 2016, especially if the sectors that are most tied to the global economy (industrials, energy, and materials) remain depressed. Mid-single-digit earnings growth might be a reasonable expectation. That’s where it was in 2013 and 2014, and where it would have been in 2015 if energy had been stripped out.

Fortunately, valuations seem reasonable, with the forward price-to-earnings ratio at 16 times earnings for the S&P 500 Index. Timmer believes valuations should remain reasonable even if yields do rise—provided such an increase is accompanied by an acceleration in earnings growth. Although valuations can be considered high by some measures, Timmer does not think they represent heavy danger. (Source: Fidelity 12/18/2015)

Conclusion

Conclusion

Volatility should continue in the equity markets and investors need to proceed with caution. For many analysts there is a growing uncertainty about the sustainability of the path the global economy and markets have been on for the last seven years. At a minimum, this confluence of factors signals a considerable level of volatility in 2016.

Analysts are focused on the Fed, China, oil prices and stock valuations. So where does that leave us? Investors need to prepare for 2016 with a sense of caution. Individual investors still have to look at their own situations first. It is important to be cautious, but it is just as important to determine your own personal risk. That’s where we can help.

Now is a good time to ask yourself:

- Has my risk tolerance changed?

- What are my investment cash flow needs for the next few years?

- What is a realistic return expectation for my portfolio?

Your answers to these questions will govern how we recommend investment vehicles for you to consider. We can help you determine which investments to avoid and how long to hold each of your investment categories before making major adjustments. For example, if your cash flow needs have changed for the next few years, you might consider different investments than someone who has limited to no cash flow needs.

Investment needs are not one size fits all, so we continually review economic, tax and investment issues and draw on that knowledge to offer specific direction and strategies to our clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for our team on the issues that affect our clients.

A good financial advisor can help make your journey more comfortable. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting, or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation, Inc. and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major indices. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Sources: Barron’s, Forbes.com, Investorplace.com, Investopedia.com, USA Today, Fortune, CNN Money, Houston Press, The Guardian, Fidelity

Contents provided by The Academy of Preferred Financial Advisors, Inc. ©

Five Questions and Answers About New Social Security Claiming Rules

When Congress unexpectedly eliminated two Social Security claiming strategies as part of the Bipartisan Budget Act of 2015, retirement planning got a little more complicated for people who expected to use those strategies to boost their retirement income. Here are some questions and answers that could help if you are wondering how the new rules might affect you.

When Congress unexpectedly eliminated two Social Security claiming strategies as part of the Bipartisan Budget Act of 2015, retirement planning got a little more complicated for people who expected to use those strategies to boost their retirement income. Here are some questions and answers that could help if you are wondering how the new rules might affect you.

What’s Changing?

The provision of the budget bill called “Closure of Unintended Loopholes” primarily addresses two Social Security claiming strategies that have become increasingly popular over the last several years. These two strategies, known as “file and suspend” and “restricted application for a spousal benefit,” have often been used to increase cumulative Social Security income for married couples. The budget bill has eliminated those strategies for most future retirees, but you may still have time to take advantage of them, depending on your age.

File and Suspend

Under the old rules, an individual who had reached full retirement age could file for retired worker benefits in order to allow a spouse or dependent child to file for a spousal or dependent benefit. The individual could then suspend the retired worker benefit in order to accrue delayed retirement credits and claim an increased worker benefit at a later date, up to age 70. For some couples and families, this strategy increased their total lifetime combined benefit.

Under the new rules, effective for suspension requests submitted on or after April 30, 2016 (or later if the Social Security Administration provides additional guidance), the worker can file and suspend and accrue delayed retirement credits, but no one can collect benefits on the worker’s earnings record during the suspension period, effectively ending the file-and-suspend strategy for couples and families. The new rules also mean that a worker who files and suspends can no longer request a lump-sum payment in lieu of receiving delayed retirement credits for the period during which benefits were suspended. (This previously available option was helpful to someone who faced a change of circumstances, such as a serious illness.)

Restricted Application

Under the old rules, a married individual who had reached full retirement age could file a “restricted application” for spousal benefits after the other spouse had filed for retired worker benefits. This allowed the individual to collect spousal benefits while delaying filing for his or her own benefit, in order to accrue delayed retirement credits.

Under the new rules, an individual born in 1954 or later who files a benefit application will be deemed to have filed for both worker and spousal benefits, and will receive whichever benefit is higher. He or she will no longer be able to file only for spousal benefits.

The Bottom Line

A limited window still exists to take advantage of these two claiming strategies. If you are currently at least age 66 or will be by April 30, 2016, you may be able to use the file-and-suspend strategy to allow your eligible spouse or dependent child to file for benefits, while also increasing your future benefit. To file a restricted application and claim only spousal benefits at age 66, you must be at least age 62 by the end of December 2015. At the time you file, your spouse must have already claimed Social Security retirement benefits or filed and suspended benefits before the effective date of the new rules.

Why Did Congress Act Now?

Both the file-and-suspend and the restricted application strategies were made possible by the Senior Citizens Freedom to Work Act of 2000. Part of this Act’s original intent was to enable individuals to change their minds in the event they determined that they wanted to work longer but were already receiving Social Security retirement benefits. However, this opened up some claiming strategies, that while legal, went beyond the original intent of the legislation. Congress used the budget bill to close these loopholes in order to save money and slightly reduce the long-range actuarial deficit faced by the Social Security trust funds.

What if You’re Already Using One of These Strategies?

If you are already using the file-and-suspend or the restricted application strategy, you will not be affected by the new rules. You have already met the age requirements.

How Are Benefits for Surviving Spouses Affected?

Rules affecting surviving spouses have not changed. If you are eligible for both a survivor benefit and a retirement benefit based on your own earnings record, you can still opt to receive one benefit first, then switch to the other higher benefit later.

What Planning Opportunities Still Exist?

Even if you can no longer take advantage of the file-and-suspend and restricted application strategies, you may still benefit from considering your Social Security filing options. The age when you begin receiving Social Security benefits can significantly affect your retirement income and income that is available to your survivors.

Basic options for claiming Social Security remain unchanged. Currently, the earliest age at which you can receive Social Security retirement benefits is 62, but if you choose to take benefits before your full retirement age (66 to 67, depending on the year you were born), your benefit will be permanently reduced by as much as 30%. On the other hand, if you delay receiving Social Security benefits past your full retirement age, you’ll receive delayed retirement credits, which will increase your benefit by 8% for each year you delay, up to age 70.

Determining when to file for Social Security benefits is one of the biggest financial decisions you’ll need to make as you approach retirement. There’s no “one-size-fits-all” answer–it’s an individual decision that must be based on many factors, including other sources of retirement income, whether you plan to continue working, how many years you expect to spend in retirement, and your income tax situation. It’s especially complicated when you’re married because you and your spouse will need to plan together, taking into account the Social Security benefits you each may be entitled to, including survivor benefits.

Although some claiming options are going away, plenty of planning opportunities remain, and you may benefit from taking the time to make an informed decision about when to file for Social Security.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2015. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

How Involved Should Your Family Be In Your Wealth Management?

Jill Ciccarelli Rapps | Life In Naples Magazine | December 2015

Jill Ciccarelli Rapps | Life In Naples Magazine | December 2015

If you’re like most, you have spent a considerable amount of time and energy on developing and growing your current level of wealth. All that hard work really does reward in more ways than just financial – the pride and contentment you can feel knowing that you have created something is very satisfying.

But there is much more to life than just money and wealth; the intangible legacy you leave your family is likely just as important to you as anything else. However, many find that it is hard to involve their family in their wealth management efforts. There are plenty of reasons for this and it’s worth taking a few minutes to look at some basic points to figure out just how involved your family should be.

It’s important to note that no two families, individuals, or wealth management scenarios are the same. As such, the final decision will always be up to you. However, looking at the following things can certainly help you make the right decision.

How Involved Are They Already? The first step is to look at just how involved your family is in your assets and wealth at the current moment. For example, are you a business partner with a son or sibling? Do you just employ a few loved ones? If your loved ones are already involved in the wealth generation, you may want to take extra steps to involve them further in your wealth management plans.

What Is Your Plan? Once you move past figuring out who is already involved, you need to figure out your overall financial wealth plan. This can be far more difficult than many realize, especially when you consider things like:

- Will you set up a living trust or a standard trust? Who is the trustee to be?

- Who gets what?

- What about non-monetary assets and wealth?

That last factor can be a hard one to discuss with loved ones, and it is easy for feelings to be hurt and for loved ones to feel slighted. The more you can communicate to your heirs, the more significant your legacy can be to make a difference in their lives.

Preparing Your Heirs

A lot of time is spent by anyone preparing their living trust, organizing their will, generating wealth, and more. But something that is often overlooked is simply the process of preparing your heirs. While you may decide not to involve your family directly in the process of planning out your wealth management efforts, it’s a good idea to at least prepare them.

There are numerous issues that can come from an ill-prepared heir situation, ranging from hurt feelings to difficulty with asset transition to trouble properly managing the wealth once it is in their name. Preparing your heirs early on can help with this dramatically. A few points to remember:

- Discuss the process of wealth and asset transition with them fully. This can help them understand what to expect so they aren’t frustrated or challenged by the process.

- Explain the basics of the division of assets so nobody faces any surprises. This can help make the transition process a bit easier as well.

- Ensure that the people who are to be in charge of different aspects of your assets understand how to properly manage them and align them in such a way that it benefits the family. Many times, a dress rehearsal is appropriate; giving them a certain amount of money to manage and see how they do.

Taking these basic steps can help you get more from the process of preparing and planning wealth and ensure that you are able to give them everything they deserve.

Why Involve Family? Obviously, some will feel that involving the family isn’t prudent. But consider the simple fact that these are your loved ones, and that while it can seem like a hassle or a burden, it is something that they will likely want to be a part of to some degree. This in turn can help you rest easy knowing that they are prepared and aware of what is to come and that they can handle the responsibilities.

If you need help with the planning process or want to consult with someone about just what the best steps are for your specific situation, Ciccarelli Advisory Services, Inc. can help. Contact us today to find out more about your options and what we can do to help you and your family prepare for the future in the best way possible.

New Enhanced Website for CAS

We are very excited to announce that our website, CASMoneyMatters.com, will have a new look and feel soon! We have added new colors and graphics and laid things out a bit differently for easier viewing. All of the content that you’ve come to rely on will be available including our upcoming events, our blog, our newsletter, and other topics of interest. In addition, we have also made our website more user-friendly for your cell phone or tablet.

We are very excited to announce that our website, CASMoneyMatters.com, will have a new look and feel soon! We have added new colors and graphics and laid things out a bit differently for easier viewing. All of the content that you’ve come to rely on will be available including our upcoming events, our blog, our newsletter, and other topics of interest. In addition, we have also made our website more user-friendly for your cell phone or tablet.

Once you are on the homepage of our website you can continue to access your account information from the account access area in the upper right-hand corner of the homepage – it’s still that simple!

We hope you will enjoy the new look and feel of our website. As always, if you have any questions please feel free to contact our offices.

NCH Hospital Ball Success

Saturday, November 14th marked a festive and successful date for our community! Jan and Kim Kantor, co-chairs for the 57th annual NCH Hospital Ball, are pleased to announce “not only did we have an absolute ball at the ball, we raised in excess of $1 million dollars towards improving stroke care delivery to residents and visitors of Collier County.” Ciccarelli Advisory Services and the Ciccarelli Family offered their support as presenting sponsors for the evening.

Saturday, November 14th marked a festive and successful date for our community! Jan and Kim Kantor, co-chairs for the 57th annual NCH Hospital Ball, are pleased to announce “not only did we have an absolute ball at the ball, we raised in excess of $1 million dollars towards improving stroke care delivery to residents and visitors of Collier County.” Ciccarelli Advisory Services and the Ciccarelli Family offered their support as presenting sponsors for the evening.

The festively dressed entertainers meandered through the exquisitely dressed ball guests, where gowns and tuxes made it a night for special occasion and great photography. The Chairman’s Reception featured the live auction items of diamonds and a world cruise, with luxury cars awaiting the crowd in the courtyard as they headed for dinner in the Vanderbilt ballroom at the Ritz Carlton Beach Resort. Paul Todd, a featured concert for bid, performed in the Silent Auction Reception where phones were busy with electronic bids on travel, wines, sports items, and dining experiences, the multitude of items graciously donated.

Music and entertainers led the guests through the Physician and Nurse honorees greeting line where they stood proudly in front of their photo board display. They were awaiting their salute and the announcement of the “Physician of the Year” and “Nurses of the Year” awards. In the elegant dining room, tables were set in whites, accented with beautiful florals and the glitter of crystals and candles. All focus was to center stage where the program began with Peter Busch as the Master of Ceremonies.

The results were a success! A much needed robot was one of the contributions set forth by a donor for $150,000 and a number of attendees raised their paddle to support the “Fund a Need” that was highlighted that evening. The funds raised will be used to support the purchase of a bi-plane at the NCH North Naples Campus. To learn more about the NCH Stroke Program, reach out to the NCH Healthcare Foundation at 239-624-2000. Watch the magazines and papers for their coverage of a great evening! Be sure to mark your calendar for next year’s evening of elegance and philanthropy as November 12th is the date for the 58th NCH Hospital Ball hosted by the Ritz Carlton Beach Resort, Naples.

You Are Ready To Retire – Now What?

For most of us, we move through our lives towards goals that we have set for ourselves. And in many instances, one of the key goals is certainly retirement. Being able to reach a point when we can stop working, have flexibility of time, live confidently off our investments, and enjoy the latter part of our lives is something that nearly everyone strives towards.

For most of us, we move through our lives towards goals that we have set for ourselves. And in many instances, one of the key goals is certainly retirement. Being able to reach a point when we can stop working, have flexibility of time, live confidently off our investments, and enjoy the latter part of our lives is something that nearly everyone strives towards.

It’s a great feeling to reach the point when you’re ready to retire. The entire world is in front of you and all the things you never had time to do are now possible; but still many people are overburdened when the time comes.

So once you reach the point where you are ready to retire, what is next? Luckily, there are a few things that you can do to make sure your transition into retirement is a good one.

The Preparation Process

The first thing you need to do when you think you are ready to retire is to be sure that you are. There are several steps that any good investment professional will give to you and it is important to follow each of them carefully. They include the following:

- Plan Your Life – While each day can be an adventure when you are retired, it is still important that you think seriously about how you’ll be living in retirement. Step away from looking at your financial numbers and consider what you will be doing. Are you moving to a new home? Relocating to a new area? Starting a small business based on your lifetime hobby? Spending focused time on planning how your life will be once you retire is important.

- Set Up Your Spending Budget – The odds are pretty good that you reached your retirement goals by living on a budget and you’ll want to carry that through your retirement. Set up a budget based on your current unavoidable expenses and what you want to do. Don’t forget to consider future health care costs and legacy goals for your heirs. A sound budget is necessary to ensure you don’t end up short.

- Consider Social Security – Many people take their Social Security benefits as soon as they can. It is worthwhile to review your options with a financial advisor, as there are several, and based on your individual circumstance and your health, picking the right option can make a significant difference. Did you know that waiting about 8 years – until you are 70 – can boost the size of your benefit by as much as 8% a year? If you plan it properly, you may be able to get more.

Continuing To Draw An Income

Turn your nest egg into a source of sustainable income. Some retirees do so by creating a business that they have dreamed of running, but for others just things like setting up an annuity that may create consistent income to supplement pensions and or social security, or just drawing a percentage of your retirement nest egg each year from specific assets can help. The key here is making sure that you do not end up needing to go back to work, and while you are retired, it is good to put your money to work for you.

Enjoying Life

Once you have made sure that you can afford to retire and considered the steps listed above, all that is left to do is make sure that you enjoy yourself. Many who retire end up unhappy since they feel like they have no focus anymore. But a few steps can help with that, including:

- Retire somewhere with friends nearby. Studies have shown that retirees with friends nearby are about 3 times more likely to be happier.

- Stay focused and create your purpose Pick out a hobby or passion and devote your time to it. Consider taking a class on finding your purpose (Blue Zones Project of Southwest Florida presents regular local workshops) or work through a retirement coach.

- Live smart; follow your dreams, stay healthy, stay active, and move your body.

Simply put, your retirement is a time that should be enjoyed and should be special. Friends and family can help, and so can being sure that you’ve planned out your retirement in the best possible way. The tips above should help make it easier to do, and speaking with a retirement specialist can as well. Feel free to contact Ciccarelli Advisory Services, Inc. today to find out more about getting ready for your retirement.

CAS New York: Financial Fair – Client Education Event

A spectacular turnout of clients and guests convened recently for this festive and educational event held on Saturday, October 17th. Invited speakers engaged their audiences on estate planning topics including the Responsibilities of a Power of Attorney, Executor and Trustee, as well as Eldercare Planning. Another session that focused on mitigating Identify Theft was offered twice to suit the demand. Over 200 were in attendance at this event which was held at the Burgundy Basin Inn in Bushnell’s Basin.

A fair-themed lunch was enjoyed by all while Ray Ciccarelli delivered his always popular Annual Market Wrap.

At the conclusion of the program, those in attendance were still greatly interested in obtaining more information on these and other topics. Given the interest for additional information relevant to one’s overall financial well-being, additional programs are already in the works for 2016.

CAS New York Fall Clean Up

Team members Jessica Beach, Ray Ciccarelli, Jordan Ramsay, and Geral Smith (not pictured) of CAS New York, along with Kellen Leone of Park Central Tax Office, enjoyed an extraordinarily warm and beautiful fall day on November 4th as they once again assisted with the fall yard clean-up at a Heritage Christian Services group residence. This endeavor originated in conjunction with the United Way’s Day of Caring which is held every spring, and has continued to be an enjoyable spring and fall experience for the entire CAS team. The team spent the day mulching, trimming, raking, and weeding, and were treated to a delicious lunch at the residence as well. We couldn’t have asked for better weather or a better day!

Team members Jessica Beach, Ray Ciccarelli, Jordan Ramsay, and Geral Smith (not pictured) of CAS New York, along with Kellen Leone of Park Central Tax Office, enjoyed an extraordinarily warm and beautiful fall day on November 4th as they once again assisted with the fall yard clean-up at a Heritage Christian Services group residence. This endeavor originated in conjunction with the United Way’s Day of Caring which is held every spring, and has continued to be an enjoyable spring and fall experience for the entire CAS team. The team spent the day mulching, trimming, raking, and weeding, and were treated to a delicious lunch at the residence as well. We couldn’t have asked for better weather or a better day!

CAS is proud to support the community in which we reside. We look forward to future outings that connect our team with those for whom assistance is greatly needed.