CAS News

2017 Inaugural Estate Planning Summit

Fill out the form below to RSVP for this enlightening discussion!

Kay Anderson Earns CFP® Certification

![]() We are proud to announce that Kay Anderson has earned her CERTIFIED FINANCIAL PLANNER™ certification!

We are proud to announce that Kay Anderson has earned her CERTIFIED FINANCIAL PLANNER™ certification!

By successfully completing the rigorous educational requirements of the CFP® program, Kay has mastered a wide range of topics that are essential to wealth management: the financial planning process and regulatory environment, insurance planning, income taxation, planning for retirement needs, estate planning and investment management.

She affirmed her knowledge by passing the six-hour, comprehensive CFP® examination.

Kay’s achievement exemplifies our passion for providing clients with knowledgeable advice and financial planning expertise.

“In addition to her 10 years of hands-on experience at our firm, Kay’s completion of the CFP® program has empowered her to develop a deeper understanding for how to best serve our client families,” said Kim Ciccarelli Kantor, President of Ciccarelli Advisory Services.

The CFP® designation is widely regarded as one of the most prestigious financial educational programs. In light of Kay’s accomplishment, Ciccarelli Advisory Services now has seven CERTIFIED FINANCIAL PLANNER™ professionals on our team.

At Ciccarelli Advisory Services, we focus on what matters to your family because we are a family. We embrace a holistic approach to wealth management and financial planning. Our family of advisors and staff is dedicated to promoting the financial well-being of your family – today and for generations to come.

Find Your Balance & Take Control of Your Finances

Jill Ciccarelli Rapps | éBella Magazine | November 2016

Jill Ciccarelli Rapps | éBella Magazine | November 2016

Finding balance in your life is a challenging yet rewarding undertaking. When you achieve true balance – meaning that all elements of your life are in a healthy equilibrium – you position yourself to live life to the fullest.

While certain skills will come naturally to you, other facets of your life will require more attention in order to find balance. For instance, multitasking, nurturing others, and staying organized are often innate skills for women. In contrast, many women struggle to take control of their finances.

The Financial Balancing Act

Gaining a fresh perspective on your finances – and feeling empowered by your financial plan – are the keys to finding balance in your life.

Connect your finances with the big picture. Establish a link between your finances and other important aspects of your life. Start with the big picture: What is most important to you? How should your money align with your priorities? For example, if community involvement is an essential part of your life, consider donating to charities and causes that inspire you. The amount of money you allocate to charity should reflect your current financial situation and life goals.

In order to achieve life balance, you need to properly oversee your finances on an ongoing basis. Control your financial life in the same way you would manage your family or operate a business.

Treat your finances like a travel itinerary. When you plan a trip, you usually have a written itinerary to guide you through your journey. Envision your personal finances in the same light: document your goals in a way that is easy for you to understand, and plan to revisit your itinerary often.

Creating a financial flow chart is a useful exercise for visualizing the big picture. With this foundation in place, you will likely find it easier to dive into more detail. By moving from general to specific, you simplify the decision-making process – enabling yourself to carefully plan a spending budget. Following this process also helps you to measure growth and success over time, and allows you to make adjustments along the way.

Prioritize your spending. Many women feel uneasy when they spend money because they don’t know if they are in a position to spend. Setting up a budget allows you to plan out exactly what you should spend and helps to alleviate any concerns about spending. Ideally, you should spend money on the most significant aspects of your life and limit spending on less important areas.

A well-thought-out budget will help you visualize your financial situation – enabling you to make quicker decisions, feel good about your spending, and move towards financial stability.

Take time to identify and review your most important values. On occasion, you may feel that you have lost your financial balance. Often times, this feeling indicates that your spending habits are not aligned with your values.

Your values should be an integral part of your financial plan. When you regularly reflect on your highest values – the areas of your life that are most important and vital to you – making financial decisions becomes less overwhelming. If you need some help identifying your top values, there are many quick, easy exercises available online.

Meet the Challenge

Your financial wellness has a tremendous impact on your life. For this reason, it’s important to meet the challenge of mastering your finances head-on. Many women enjoy the challenge and thrill of achieving this goal, as mastering your finances can be a major source of pride.

If you aren’t currently taking control of your finances, an advisor can help you document your finances and gain clarity – guiding you towards a healthier life balance.

Andrea Mitchell Joins CAS

We are pleased to announce a new addition to our growing, family-focused firm: Andrea Mitchell.

We are pleased to announce a new addition to our growing, family-focused firm: Andrea Mitchell.

As an Administrative Associate at our Naples office, Andrea will assist Kim Ciccarelli Kantor and Paul Ciccarelli by preparing client portfolios for annual reviews, generating reports and maintaining up-to-date client records.

“Andrea has been a wonderful addition to our CAS family,” said Susan Hansen, Director of Administration at Ciccarelli Advisory Services. “Her work behind the scenes and with our clients will be a tremendous asset to the firm.”

Andrea has performed a variety of administrative roles throughout her life. She worked as an administrative assistant for a local insurance broker agency for several years, and also served in a similar capacity at a retirement planning firm.

At Ciccarelli Advisory Services, we focus on what matters to your family because we are a family. We embrace a holistic approach to wealth management and financial planning. Our family of advisors and staff is dedicated to promoting the financial well-being of your family – today and for generations to come.

Andrea Mitchell is not registered with FSC Securities Corporation or Ciccarelli Advisory Services, Inc.

CCCR Networking Event – “De-Stressing” before the Holidays

We kick-started the holiday season with a charity networking event at our Naples office!

Our event – De-Stressing before the Holidays – not only provided an opportunity for guests to relax, but also served as a forum for meeting fellow professionals from the community. In additional, we generated awareness and funds for Collier Child Care Resources.

CCCR operates several early childhood education centers in the Naples area, which provide top-notch educational opportunities for families in need. We welcomed more than 80 guests from the CCCR Business 100, a group of business owners and professionals who annually pledge their support for the organization’s admirable mission.

Our visitors dined on a delicious dish of paella from Fire & Rice, savored decadent desserts from Here’s Howe Catering, and sipped on wine throughout the evening. We also featured a quartet of string musicians from Gulf Coast High School and a massage room that was furnished by Cloud9 Float and Spa – providing an extra touch of relaxation for our Naples business community.

Volunteer Day – Fall Clean-Up

Left to right: Lisa Buckert, Carrie Reeves-Hillyard, Jessica Beach, and Jordan Ramsay

On a spectacular 60-degree day, our CAS Rochester family once again helped our friends at Heritage Christian Services with fall clean-up at one of their residential homes in Webster.

Armed with rakes, tarps, clippers, and sunglasses, our team of volunteers – Lisa Buckert, Carrie Reeves-Hillyard, Jessica Beach, and Jordan Ramsay – tackled an enormous amount of leaves, which continued to fall as they were working!

Our Volunteer Day is one of the many ways that CAS supports the communities where we live and work.

Give the Gift that Lasts a Lifetime

Jill Ciccarelli Rapps | Life in Naples Magazine | November 2016

It’s hard to believe that the holiday season is nearly upon us! As we celebrate the festivities with our families and loved ones, many of us are searching for the perfect holiday gift for our children and grandchildren.

While we may feel compelled to buy the latest tech gadget or a flashy new toy, you may want to consider the gift that lasts a lifetime: financial knowledge.

An Unforgettable Lesson

Growing up in western New York, I remember going on “road trips” with my parents and siblings. We would visit a company and take a tour of their facilities, or spend time exploring a farm. Our experiences on the road with Mom and Dad served a valuable purpose: educating my siblings and me about saving and investing.

At an early age, we learned which goods were produced in the factories and farms we visited, and that the demand for those goods would go up and down over time. We learned that we could invest our money in the companies we visited – as demand for their products increased, we could earn money without actually working as a farmer or a laborer.

Above all, our parents taught us the importance of starting to save early in life, and to save a little bit of every dollar that comes your way. These simple but powerful lessons have had an enduring impact on our lives, leading us down the road towards financial success.

Give Your Grandchildren a Jump Start

Engaging your grandchildren in a financial conversation can pay dividends for years to come. Everyone can benefit from having this valuable discussion, regardless of their age or level of interest.

Imagine you are having lunch with your 8-year-old grandchild. You recently set up a mutual fund for her. How do you discuss this topic with him or her? The best approach is to keep it simple and build on their knowledge over time.

Start by explaining that there are many companies in the fund and that he or she owns part of these companies – which means they will make money when the companies make money. While your grandchild probably won’t remember everything you say, you will plant the seeds for further education throughout her life.

The next step is to provide your grandchild with a memorable gift that relates to their investment. For instance, if the mutual fund holds Tesla, purchase him or her a model Tesla car and explain that they own part of the company that builds those cars.

As your grandchild continues to grow and mature, you can introduce more detailed concepts. You can talk about how stocks work and why the prices fluctuate, and give him or her an update on the performance of her investments. To add even more value to your financial lessons, you can supplement your conversation with interactive financial tools (many resources are available online) or enlist the expertise of a financial advisor.

With adult grandchildren, I recommend starting a conversation about 401(k) plans. Many young people don’t understand how a 401(k) plan works; as a result, they don’t participate in the plan and miss out on the benefits. Emphasize the value of making regular contributions. Explain that most employers will match your contributions, and illustrate how their money will gain compounding interest throughout their entire career. This is the perfect opportunity for you to impart valuable lessons that can guide your grandchild towards financial wellness.

To reinforce the wisdom you share with your grandchild, you can give them tangible gifts that promote financial success. A powerful way to encourage your grandchild to save is to match their savings. Another idea is gifting time with a financial advisor, who will guide them in identifying their current needs and their financial goals for the future.

Books can also provide a wealth of financial knowledge that will benefit your grandchild. I highly recommend these books, which are two of my favorite reads:

- The Richest Man in Babylon by George S. Clason

- Five: Where will you be five years from today? by Dan Zadra

It’s never too early to share your financial experience with your family. This holiday season, capitalize on the opportunity to help your children and grandchildren prepare for a lifetime of financial success. Give the gift that lasts a lifetime!

CAS Rochester Market Wrap

More than 180 CAS clients and staff gathered together amidst the picturesque views of the Casa Larga Vineyards and Winery at our 2016 Market Wrap in Rochester.

Ray delivered an informative update on our firm and offered an enlightening commentary on market conditions. Carol Girvin then introduced the 15 members of our Rochester CAS family, followed by a Q & A session.

After the educational portion of the event, we treated our guests to an extravagant dessert buffet. With more than 1200 handmade desserts to feast upon, our annual Market Wrap certainly ended on a sweet note!

How will the election impact your portfolio?

By now, most voters have made up their mind about who they want to serve as their next President. But what can they look forward to, from an investment and tax standpoint, if their candidate wins or loses? How will the election affect their portfolio and future net worth?

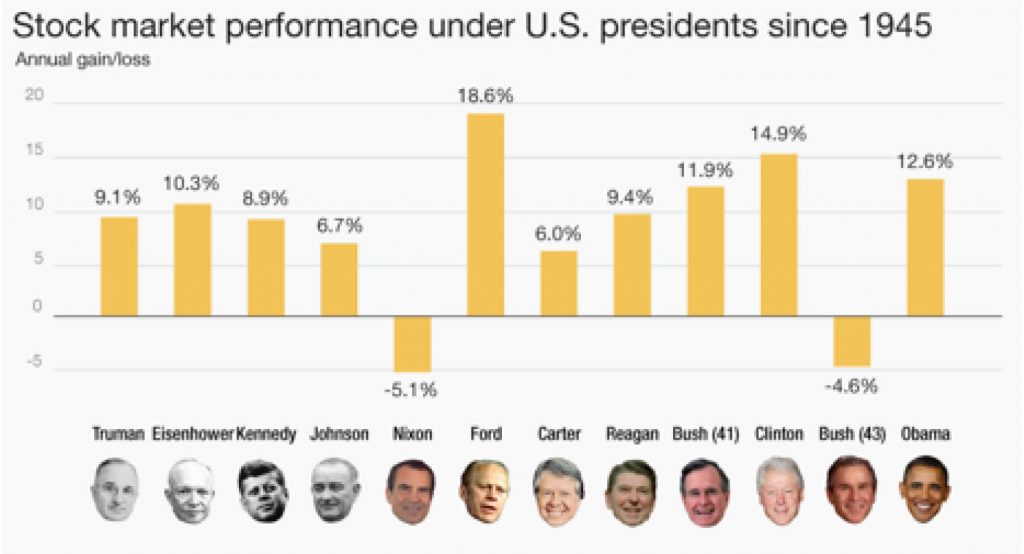

Let’s look at the least predictable factor. An analysis of historical market returns under different administrations gives a frustratingly incomplete picture.

When a President comes into office and immediately enjoys a few boom years, is that due to his great policies or the policies of his predecessor? Similarly, when a President enters office in the middle of a recession (think Obama in 2009 and George W. Bush in 2001), can we attribute the weak market performance to any policies he hasn’t had a chance to enact?

The cliche that Republicans are better for markets than Democrats is hard to support based on the raw statistics. As you can see from the chart, Richard Nixon and George W. Bush are the only presidents who presided over a net loss in the markets, while Bill Clinton and Barack Obama are second and third behind Gerald Ford as the presidents associated with the highest total gains.

The record is too mixed, and too complicated, to make predictions based simply on the party that wins the white house.

But what about something more concrete, like tax policy or budget deficits? Surely here we can read the tea leaves about the future.

Once again, the historical record can be misleading. President Reagan, known as a great tax cutter, lowered taxes with the 1981 tax act and promptly raised them again with new measures a year later. Democratic President Bill Clinton’s administration presided over the only budget surpluses of the modern era, while Republican President George Bush and Democratic President Barack Obama added more to the deficit than all previous presidents.

The most reliable clue we have about the fiscal and investment impact of a Donald Trump or Hillary Clinton presidency is the actual proposals by the candidates. But even here, we have to proceed with caution. It is unlikely that the Democrats will win the Presidency plus a majority in both the Senate and the House of Representatives, which means that a Clinton wish list will be either stymied or compromised by divided government.

Nevertheless, if Clinton is elected, we know to expect certain changes to the tax code. There will be at least an attempt to add a 4% surtax on incomes above $5 million, an end to the carried interest deduction favored by hedge fund managers and other Wall Street executives, plus a cap on itemized deductions when people reach the 28% tax rate.

In addition, the existing $5.45 million estate tax exemption would be reduced to $3.5 million ($7 million for couples), and estate amounts above that figure would be taxed at a 45% rate. Wall Street brokers would be hit with an unspecified surtax on high-frequency trading activities.

A President Trump would be more likely to get his wishes, but his exact wishes are far less certain. You can get a picture of the fuzziness of his policy proposals when you look at his promise of infrastructure spending.

When Clinton proposed spending $275 billion on road, airport and electrical grid repairs (surely not enough to move the needle on U.S. GDP growth), Trump immediately proposed spending $550 billion on the infrastructure—doubling his opponent’s figure without any apparent analysis.

Many of the proposals have been made off-the-cuff and some are contradictory, but you can expect a President Trump to make an effort to cut taxes by reducing the ordinary income tax brackets to 12% (up to $75,000 for joint filers), 25% ($75,000 to $225,000) and 33% (above $225,000).

Under Trump, the standard deduction would double, but itemized deductions would be capped at $100,000 for single filers ($200,000 for joint filers). Corporate tax rates would be reduced from a maximum of 35% to a maximum of 15%. Federal estate and gift taxes would be eliminated, but the step-up in basis would also be eliminated for estates over $10 million.

Lumping together Clinton and Trump’s various proposals (and making a variety of assumptions to cover the fact that the Trump plan is light on details), the Tax Foundation estimates that the Clinton proposals, in the unlikely event that they were fully-enacted, would reduce GDP by 1% a year and reduce the budget deficit by $498 billion. Candidate Trump’s proposals would reduce tax revenues by between $4.4 trillion and $5.9 trillion over the next decade, but the Tax Foundation believes they would add 6.9% to GDP.

Turning back to the markets, the investment herd prefers certainty and status quo to uncertainty and rapid change. A Clinton presidency checked by either the Republican House or a Republican House and Senate would provide a measure of stability.

A President Trump, with Republicans controlling both houses of Congress, would represent significant uncertainty, and off-the-cuff policy proposals introduced into the news media at random times would likely spook investors. Loose talk about “renegotiating” America’s debt with Treasury bond holders here and abroad (read: default, followed by demanding a haircut) could, all by itself, lower America’s bond rating once again, following the downgrade aftereffect of the government shutdown.

A Clinton presidency would almost certainly have a negative impact on the coal industry, and to the extent that there are new environmental regulations—which can be imposed by regulation without consulting Congress—it could also negatively impact the energy sector overall. It would not be surprising to see a carbon trading initiative, and more broadly a requirement that whatever environmental degradation companies impose on society will have to be paid for by the companies themselves in some form or fashion.

A Trump presidency would seem to favor industry in a variety of ways. The proposals are frustratingly unspecific, but we could expect less regulation (particularly environmental regulation), no raising of the minimum wage, lower corporate taxes across the board and protectionism.

On the other hand, if candidate Trump is serious about deporting undocumented immigrants, the U.S. labor supply would diminish in unpredictable ways. The policy would likely have the biggest negative impact on the farming and construction industries.

Perhaps the biggest risk in this election involves trade. A Trump Presidency would be seen, initially, at least, as a drag on the Mexican markets, and it might see America rip up its trade agreements and pick currency and trade wars with the emerging economic colossus that is China.

Interestingly, the Trans-Pacific Partnership agreement, which both candidates now reject, was an effort by the U.S. to create economic ties to Singapore, Korea, Vietnam and other countries in the Asian rim, the better to counter Chinese economic influence. In terms of global trade, China stands to win no matter who wins this election.

The bottom line: prepare for the possibility (but not the certainty due to gridlock) of higher taxes under a Hillary Clinton presidency, and a more certain (but hard to predict the details) lower-tax environment under a President Trump.

If you’re a Wall Street trader, you’re going to lose money under a Clinton presidency, and Southeast Asian nations stand to lose expected trade benefits under either president.

Despite the usual stereotypes, the deficit would likely go up under a Trump presidency and it might go down under a Clinton one — again with the caveat that comes with a divided government. The economic outlook would be much harder to predict.

The reality is that no matter who wins, America will still represent the most dynamic economy in the world, and whoever wins the White House is unlikely to change that.

Sources:

http://taxfoundation.org/article/details-and-analysis-hillary-clinton-s-tax-proposals

http://taxfoundation.org/article/details-and-analysis-donald-trump-tax-reform-plan-september-2016

CAS Referral Dinner – A Magical Experience

Our CAS family hosted an elegant dinner on October 25, to express our gratitude to Rochester clients who have referred their friends or family members to our firm.

More than 50 clients joined our advisors and staff from the Rochester office at the Rabbit Room restaurant in Honeoye Falls, NY. In addition to a delicious meal, cocktails and great company, we treated our clients to “up-close magic” from Jimmy C.

Without a doubt, our 2016 Referral Dinner was a magical and memorable evening.

Thank you again to all of our Rochester clients who attended the event! We appreciate you spreading the word about our family-focused firm, and we are grateful for the opportunity to guide you towards your financial goals and vision for the future.