Uncategorized

Women’s History Month; Learning From our Past

By Jill Ciccarelli Rapps CFP®

What do Women’s History Month and financial planning have to do with each other? It turns out, a lot!

Looking back in history, women did not take the primary role in their financial future and today many women still do not feel knowledgeable and powerful with their finances. What we learn from our past role models can help women pave their way to taking charge of our financial future. Let’s first take a look at some of these amazing women who broke barriers and created a “can-do” attitude when it comes to finances.

Abigail Adams (1744-1818) was the second First Lady of the United States, but she had another title that isn’t widely known: Investor. As her husband John Adams was busy with his career as a lawyer and statesman, he left the management of their family farm and business dealings to Abigail. She invested in government and war bonds, considered risky at the time, and quadrupled the family’s fortune.

Maggie Lena Walker (1864-1934), the daughter of slaves, went to work to help her mother after her father died. She started the St. Luke Penny Savings Bank in 1902, becoming the first woman to charter a bank in the U.S.; her goal was to encourage saving and economic independence in the Black community.

Muriel Siebert (1928-2013), was the first woman to have a seat on the New York Stock Exchange in 1967. She was the only woman among 1,365 men. Often referred to as “The First Woman of Finance,” Siebert founded and served as the president of Siebert Financial Corp., which made her the first woman to run one of the NYSE’s firms. Siebert was also the first woman to hold the role of Superintendent of Banks for the State of New York, a position she held for five years.

We all have the power and ability to be financially independent. Women have amazing, natural capabilities, such as being caretakers, multi-taskers, masters of balancing risk and reward and being planners. This helps to be naturally good financial stewards of money, but often many of us do not trust these abilities for one reason or another.

There are four elements you need to master to be as powerful as our leading ladies above:

#1 Documenting your vision (a great way to do this is through a vision board) of what you want your money “used” for – what gives you the greatest pleasure. When you write it or visualize it, it becomes ten times more powerful and gives you clarity about what you want to achieve.

#2 Have a spending plan and know how much it takes to cover your lifestyle. Create a budget and make sure you can save money consistently and that you have enough to allocate to your future goals.

#3 Prepare and update a balance sheet at least once a year. This is a listing of all your assets and liabilities. A balance sheet is a great tool to measure your success, documenting where you are today, and have clarity about the financial decisions you need to make for the future.

#4 Have a financial tracking system to easily see how you are achieving your goals. Today it is common to have a secure website where all your financials download to a full view of your net worth, investment values, and spending. With a click of a button, you can get a “bird’s eye” view of your finances that can help you see if any adjustments need to be made.

We believe in empowering women to be financially smart, independent (meaning taking care of yourself first), and confident about the financial decisions you make. Having a plan in place empowers you to live your life to the fullest. If you need guidance on any of the steps above, do not hesitate to reach out to your financial advisor team to help guide you; you will be glad you did!

Red Flags That Your Identity was Used to Apply for a Fraudulent PPP or EIDL Loan

This week we have a guest contributor to our newsletter. Carrie Kerskie is a nationally recognized identity theft, fraud, and cyber threat lecturer, author, and consultant. She is the president of Kerskie Group, LLC, a leader in personalized identity theft restoration and prevention. To learn more visit www.Kerskie.com.

Did you recently receive a letter from the SBA regarding your Paycheck Protection Program “PPP”, or Economic Injury Disaster Loan “EIDL”? If you did and you didn’t apply for either one of these, you could be a victim of PPP or EIDL identity fraud.

If you received a letter from the SBA regarding your PPP or EIDL loan, don’t throw it away. Some people that received these letters thought it was junk mail or a scam and threw it away. It was a warning sign that a fraudulent loan was taken out using their identity, either personal or business.

Let’s look at what these programs are and how the bad guys were able to exploit them for profit.

What are the PPP and EIDL

The PPP is a non-repayable, forgiven loan from the SBA to help businesses retain employees during the COVID crisis. As long as the employer used the funds as required, the loan should be forgiven.

The EIDL was created to help meet the financial needs of struggling businesses that were negatively impacted by COVID. The EIDL, unlike the PPP, must be repaid. If certain criteria were met, the business could refinance the EIDL into a PPP and have the loan forgiven.

Opportunity for Fraud

While these programs were a lifeline for many businesses during the crisis, they also presented an opportunity for fraud. In my opinion, the SBA made some fatal mistakes when rolling out these programs.

Businesses were originally required to apply with their bank. In an attempt to further streamline the approval process, the SBA announced that a business could apply with any financial institution, including virtual (online) banks.

Because PPP loans are forgivable, a credit check was not required. The application process for these SBA loans was streamlined to expedite the approval process.

Where Does the Application Information Come From?

Due to data security breaches, since 2005, over one BILLION personal records were exposed nationwide. The odds of your personal information available for sale online are high.

Did you know that anyone with internet access can purchase a name, date of birth, and SSN for less than $1.00?

Yep, it is that easy.

With this information, the bad guys completed the applications using fictitious businesses, along with fake financial documents. In many of the cases we are aware of, the bad guys used the victim’s first or last name followed by “Farms” as the business name.

Since the victim’s SSN was used, as opposed to a business FEIN, if the victim’s credit was good, the loan was likely to be approved.

Many of the loans we are aware of were for $48,900 or less.

As far as proof of ID, the bad guys applied online with the virtual banks. Most, if not all, require very little information or no information for proof of identity. If a driver’s license was required, bad guys can easily make a fake one. The banks do not confirm the photo on the ID matches the photo in the state’s DMV database.

Fraudulent Applications for Real Businesses

But not all the applications were for fake businesses. We received calls from a few businesses that discovered someone used their business identity to apply for a loan or multiple loans.

In many states, business records are available to the public. For example, in Florida, anyone can search for businesses registered to conduct business in the state by visiting www.sunbiz.org. The information listed for each business often includes the business address, officers, and FEIN, information required on the PPP and EIDL application.

Other Warning Signs

Some of the victims noticed a hard credit inquiry from the SBA on their credit report. The EIDL required a credit check, while the PPP defaulted to the discrepancy of the financial institution.

Some organizations ran credit checks. Some did not.

If you saw an inquiry from the SBA on your credit report, you might be a victim.

If you own a business, check your business credit report. Do you see an inquiry from the SBA? If so, your business might be a victim.

If you received a letter from the SBA regarding a fraudulent PPP or EIDL loan, contact the financial institution where the loan was approved and the SBA.

Identity theft, fraud, and cyber threats are constantly changing. Don’t get left behind. Sign up for my newsletter at CarrieKerskie.com. No spam, just tips, and tricks to protect yourself from identity theft, fraud, and cyber threats.

You can also attend my upcoming webinar with Ciccarelli Advisory Services on Thursday, March 11, 2021, at 4 PM EST where I will be discussing protecting your assets from pandemic scams and threats. You can CLICK HERE to register for the webinar.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Securities and additional investment advisory services offered through FSC Securities Corporation, member FINRA/SIPC and a registered investment adviser. 9601 Tamiami Trail North, Naples, FL. 239-262-6577.

CNR Economic Webinar Recording Now Available

We are honored to have had so many attend our Live Economic Webinar with City National Rochdale CEO, Garrett R. D’Alessandro CFA, CPWA®, CAIA, AIF®.

If you were unable to attend or would like to view the webinar again or share with a friend or family member, we have made a recording of the webinar available on YouTube!

Tax Considerations for the 2020 Tax Season

Paul F. Ciccarelli CFP®, CHFC®, CLU®

2020 was a whirlwind of a year. With the vast array of ongoing events and calamities, it is understandable if tax season has slipped your mind. However, as you gather your tax information for your CPA, keep in mind the important items below. Because of the various ACTS due to the COVID-19 virus, many of the tax planning opportunities we took advantage of this past year are not necessarily reported on a 1099 or other IRS notifications. You will have to include additional tax information on stimulus checks received, RMD rollbacks, ROTH conversions which were done in 2020. Below are some provisions you may want to consider for the 2020 tax season.

Retirement Plans

The CARES Act and the SECURE Act both have provisions affecting retirement accounts.

Both acts significantly impact required minimum distributions (RMDs). For example, under the SECURE Act, the beginning age for taking RMDs rises from 70½ to 72. (This change only applies to account owners who turn 70½ after 2019.)

The CARES Act allowed seniors to skip their RMDs in 2020 without penalty. In addition, the CARES ACT allowed individuals to rollback any RMD’s taken during 2020 as long as the rollback occurred before August 15th, 2020. It is important that you provide any information on rollbacks that were done during the 2020 tax year to your CPA so that they ensure you do not pay taxes on a distribution that was rolled back to your IRA. Also, important to provide your CPA with any ROTH conversions done during the year so your CPA can properly account for them on your 1040 return.

The SECURE Act also allows owners of traditional IRAs to make contributions past the age of 70½ starting in 2020 if they have earned income (either W-2 or 1099misc).

In addition to the RMD suspension mentioned above, the CARES Act includes a few other key retirement-related tax breaks for 2020. First, it waives the 10% penalty on pre-age-59½ payouts from retirement accounts for up to $100,000 of coronavirus-related payouts. A coronavirus-related distribution can also be included in income in equal installments over a three-year period, and you have three years to put the money back into your retirement account and undo the tax consequences of the distribution. If you’ve taken advantage of this coronavirus-related easing, you must attach Form 8915-E to your return to spread out the tax on the distributions. Second, the CARES Act allowed eligible individuals to borrow more from workplace plans such as 401(k)s—up to the lesser of $100,000 or 100% of the account balance—until September 23, 2020. Repayments on retirement plan loans due in 2020 are also delayed for one year.

Many key dollar limits on retirement plans and Simple IRAs are higher in 2020, too. The maximum 401(k) contribution for 2020 is $19,500, but those born before 1971 can put in $6,500 more (both amounts are $500 higher than in 2019). The caps apply to 403(b) and 457 plans as well. The 2020 cap on contributions to SIMPLE IRAs is $13,500 ($500 more than in 2019), plus $3,000 extra for people age 50 and up. The 2020 contribution limit for IRAs remained at $6,000 (or $7,000 for individuals age 50 or above).

Recovery Rebate Credits

Under the Coronavirus Aid, Relief, and Economic Security (CARES) Act and the COVID-Related Tax Relief Act, most Americans received one or two stimulus checks in 2020. Both the first- and second-round payments were phased out for joint filers with adjusted gross incomes above $150,000, head-of-household filers with AGIs above $112,500, and single filers with AGIs above $75,000.

Technically, your stimulus checks were an advance payment of a special 2020 tax credit known as the recovery rebate credit. When you file your 2020 return, your CPA will have to reconcile the stimulus checks you received with the recovery rebate credit you’re entitled to claim. Your CPA will need to know the amount of the checks you received during 2020 so they may report it on your tax return.

For most people, the combined total of your stimulus check payments will equal the tax credit allowed. In that case, your credit will be reduced to zero. However, if your stimulus checks were less than your credit amount, the tax you owe will be reduced by the difference (and you might even receive a refund). And if the combined total of your stimulus checks was more than your credit amount, you generally won’t have to repay the difference to the IRS. Also, note that the stimulus check payments are not taxable!

If you haven’t maxed out your IRA or ROTH IRA contributions for 2020, you still have time to do so before April 15, 2021.

Keep in mind, because of all of the one-time tax provisions we received in 2020, you may need to provide more information to the CPA at tax time so they can be sure to complete the 1040 returns correctly. We suggest you pull the information and place it in your 2020 tax file as you prepare it for your CPA. We will be providing information to you and your CPA on opportunities we assisted you with in 2020.

If you have any questions or concerns about filing for 2020, now is a great time to reach out to your financial advisor and CPA to ensure you are on track.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Securities and additional investment advisory services offered through FSC Securities Corporation, member FINRA/SIPC and a registered investment adviser. 9601 Tamiami Trail North, Naples, FL. 239-262-6577.

Could A Major Tax Hike Be in Store for You?

By Kay Anderson, CFP®

As we head into February, our mailboxes are filling up with various tax documents. With the ongoing pandemic and USPS mail delays, it will be important this year to maintain a “2020 Tax Folder” to collect your documents as received and deliver them to your CPA. We suggest giving the majority of your items to your CPA with a note if you are missing a late filing K1 or 1099.

Many companies now provide copies in both hard copy form and online access. Your online access may be a good place to check if you are missing expected documents.

After the recent election as well as the ongoing pandemic, many are concerned with how their taxes may be impacted. Historically speaking, after downward economic conditions, it is not uncommon for taxes to be raised on high earners. Following WWII, income tax rates for high earners remained significantly higher than they are today for decades, with the top federal income tax rate at 91% for most of the 1950s. If we are to follow similar projections, this could mean some major tax hikes may be in store.

Some tax areas that the new administration has indicated they will adjust includes:

• Taxing long-term capital gains on incomes above $1 million at ordinary income rates instead of the current rates.

• Eliminating the step-up in basis that allows heirs to minimize taxes on inherited assets.

• Reducing the estate exemption and unified credit prior to the current sunset due 2026.

• Imposing the Social Security payroll tax on wages above $400,000.

• Limiting the value of itemized deductions to 28% for those with incomes above $400,000.

President Biden has indicated that he will not be increasing the tax rate for individual W-2 wage earners. However, depending on your income, the deductions that are available to you could be impacted. He has previously proposed limiting itemized deductions, such as the mortgage interest deduction, for individuals with higher incomes.

It is important to keep in mind that these changes have only been proposed so far. After an election, there is often a great deal of discussion of tax changes, but not all proposals come to fruition and it can take time to implement.

While we don’t know for sure what is ahead, we do know there are some planning techniques that are still available now:

• IRA Contributions – A traditional or Roth IRA contribution can be made up until April 15, 2021 (subject to contribution and income limitations)

• Self Employed Retirement Plan Contributions – A SEP IRA contribution can be made prior to tax filing up until April 15, 2021, or extension (subject to contribution and income limitations)

• Health Savings Account – A prior year contribution can be made up to $3,550 for individual plans and $7,100 for the family plan; for those over age 55 a $1,000 catch up contribution is available

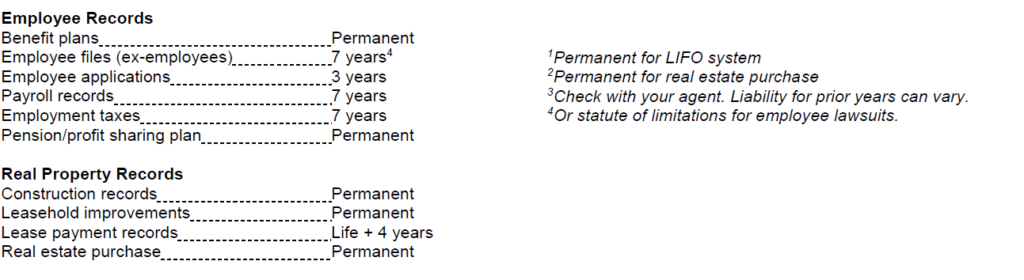

The pandemic has provided for extra downtime at home allowing us to focus on clearing out those closets, garages, and file cabinets that continue to accumulate through the year. It can be difficult to know what documents to keep and what can be tossed or shredded. Please see below our Retention Guidelines for reference…..if in doubt, reach out to our office and we are happy to review with you.

This is an excellent time to plan strategically for your future and future generations. Please reach out to schedule a time with your CAS advisory team.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Securities and additional investment advisory services offered through FSC Securities Corporation, member FINRA/SIPC and a registered investment adviser. 9601 Tamiami Trail North, Naples, FL. 239-262-6577.

Organize Your Personal Finances for the New Year

By Josh Espinosa CFP®, CIMA®

It’s not just your house that might need a little straightening up. Your finances can also benefit from a “cleaning” every now and again. And what better time than the beginning of the new year! Why not take a look at everything you may have put off, and start organizing your personal finances to align with your vision for the future? Below are some areas you may want to start with.

Determine Your Net Worth

Your net worth is the total of your assets minus your liabilities, and determining it can help you lay the groundwork for an organized financial future. In other words, your net worth is the figure you get when you add up everything you own from the equity in your home to the cash in your bank account to your investment accounts with CAS and then subtract from that the value of all of your debts which may include a mortgage, car, student loans, or credit card balances.

When it comes to your financial health, there is no single net worth number you should be striving for. It is unique to you and your financial roadmap. You could use your net worth to track your progress from year to year and to hopefully see it grow over time.

Go Paperless

Those bulky paper files take up more than physical space, they can make it harder to keep track of statements and bills. With a paperless system, there is a simple, online backup of everything. Your files can travel with you wherever you go.

If you have regular access to a computer, setting up online payments for your bills can go a long way towards streamlining the organization of your finances. In many cases, you can choose to have monthly deductions taken automatically from your bank account or you can choose to manually initiate each payment.

You can also keep your most important files in an online vault, like our cas360, which allows you to easily organize and categorize your files so they are always accessible and protected from floods, fires, and loss.

Consolidate

You may want to take the time each year to consolidate and update accounts so they align with your current usage and financial situation. Have a checking account you no longer use? Close it! Have a will that has not factored in a change in family situation or lifestyle? Change it! Now is the perfect time to really decide what you need, and which documents need a bit of TLC.

Some other areas you may want to look at include:

- Gather new quotes for car, home, and life insurance and adjust coverage levels if needed.

- Check your mortgage rates and see if it makes sense to refinance.

- Check your credit with a credit checking site. However, you are only allowed one free copy of your report from each of the three credit bureaus per year. You either can check one bureau (Experian, TransUnion, or Equifax) every four months, or you can check all three at one time and wait 12 months to check again.

- Check fees on phone, cable, and other bills to see if you are paying for services you don’t use.

- Confirm your beneficiaries are correct on retirement accounts, life insurance policies, and annuities. Often, due to personal changes such as marriage, divorce, or the birth of children, the original beneficiaries may not be who you currently desire.

Organizing your finances takes time, patience, and discipline, but could be well worth it in the end. The new year doesn’t need to be the only time you organize; you should keep up-to-date as often as possible, but it can be an opportunity to start the year off with less worry and stress. If you have any concerns about your personal finances, your CAS financial advisor can assist to help you stay on track and be prepared for the future.

New Year Downsizing

By Lynn Ferraina, Advisor

A new year is new beginnings. This could mean learning a new language, tackling a new hobby, or perhaps decluttering your living space. Whether you are downsizing to a new home or decluttering your current home, the task can seem overwhelming. One of the best ways to stay on track and organized is to have structure. Below are 6 ways to help you declutter in an organized manner.

- Give yourself a head start as soon as possible

Time is of the essence, and the more time you have to space out your downsizing, the smoother it will likely go. Schedule your day the same way you would a workday, planning out specific tasks you will complete each day. If you have others helping with the declutter, this will keep everyone on schedule.

- Start Big

There is nothing worse than finally moving and realizing your furniture will not fit. Start by measuring out the dimensions of your room sizes and the largest pieces you own. Determine which pieces of furniture will comfortably fit, while still leaving room for your other belongings. This will leave ample time to determine whether to sell the pieces or have them removed.

- Consider what to keep and what to pass on

Everyone comes to the conclusion, sometime in their life, that they have too much “stuff.” Determine which of your belongings you truly need or derive “joy” from. Have boxes at the ready, labeled “keep”, “donate”, and “dispose”. Ask your loved ones if there are special items they would like, and gift them now so that you may have the pleasure of watching them enjoy your treasures.

- Contact local donation centers

Find out what local donation centers are looking for and if they will pick up large items. Many donation centers have the ability to come pick up furniture that is in good condition. Donating items can be helpful to the community and there may also be a tax benefit to you. According to the Internal Revenue Service (IRS), a taxpayer can deduct the fair market value of donated clothing, household goods, used furniture, shoes, books, and so forth, up to the published limits allowed.

- Store files in an online vault

Keeping only physical copies of important documents not only takes up space- it can be a real hazard! Fires, floods, mold, and yellowing of paper all threaten your documents, and unless your filing system is immaculate, searching for a particular document could take up your valuable time. An online vault, which we provide in our cas360 system, digitizes your files and allows you to keep them in one place for easy access by you or a family member.

- Avoid Putting everything in a storage unit

It can be tempting to pack up all of your extra items and place them in a storage unit, however that defeats the purpose of decluttering and adds an extra monthly expense. If you take the time and really discern what you need and what you don’t, you will most likely feel greater comfort and less cluttered.

Decluttering can be a stressful process and can take some real mental fortitude to complete, but once done it will hopefully provide relief. It can be surprising how fast your belongings can accumulate and make your space feel smaller. You may want to have a one-in, one-out rule as you buy new items to avoid clutter again. As you tackle decluttering, our team is here to provide support for the financial road ahead.

Happy Holidays from Ciccarelli Advisory Services!

As the 2020-year closes, it is important to take a moment to reflect on our gratitude for those who make this time so special – you and your family!

This has been a trying year for most, and we hope you have been able to find moments of joy and solace through the turbulence. Your strength and resilience have been inspiring. While we can only connect from afar, it has meant a great deal to our team.

Thank you for your continued confidence in us. The relationship we share is the cornerstone of our business, and we sincerely appreciate the privilege of serving you.

On behalf of the Ciccarelli Advisory Services family, we send wishes your way for a safe and happy holiday season.

From our home to yours…. Merry Christmas or Happy Hanukkah and a very Happy New Year to you and your family!

Is an Intrafamily Loan Right for Your Family?

Samantha R. Webster, CFP®

Family is a gift that keeps on giving, and one of the greatest gifts you could provide your family members is the gift of helping them achieve their goals and dreams. One of the biggest obstacles many people face when trying to further their goals is finding the money to do so. Traditionally, it is expected that if you do not have the money for a large purchase such as a house or business, you must apply for a loan with a bank or financial institution. You are then subject to their terms, interest rates, as well as time constraints. This can be a difficult and unnecessary option for some families who may be able to provide the loan directly with an intrafamily loan.

Intrafamily loans are typically made from parent to child or grandparent to grandchild, but they are often utilized as a means of keeping wealth in the family and avoiding traditional lenders who may charge higher interest rates. If your child or grandchild does not meet the credit requirements for a traditional loan, there is a good chance they will either be turned away or be left with a high-interest rate determined by the lender. With an intrafamily loan, you could help fund their future and prevent unnecessary expenses.

For some families, this can also be an estate planning strategy of where the dollars are removed from the lender’s estate by placing them in an irrevocable trust. The trust then makes the loan and then the loan payments are returned to the trust, keeping the transfer of wealth seamlessly within the family.

With an intrafamily loan, interest still has to be applied to avoid later tax complications for the family lender, but you are able to charge the minimum market rate that is based on the IRS’s Applicable Federal Rates (AFRs). These rates are updated monthly and are determined by a variety of economic factors, including the prior thirty-day average market yields of corresponding US treasury obligations, such as T-bills. When deciding the appropriate IRS Applicable Federal Rate for a family loan, the lender should determine:

- The length of the loan repayment;

- The IRS Applicable Federal Rate for that repayment term during the month in which the loan is made.

To determine the current rates, you can check the IRS’s AFRs for the month of the loan HERE. There are three AFR tiers based on the repayment term of a family loan:

(1) Short-term rates, for loans with a repayment term up to three years.

(2) Mid-term rates, for loans with a repayment term between three and nine years.

(3) Long-term rates, for loans with a repayment term greater than nine years.

It is important to note that since an intrafamily loan is made with the full intent of repayment, it is important that the terms of the loan are recorded in a promissory note with tracking of the payments of interest and principal. If not properly recorded and tracked, the IRS may classify the loan as a gift and tax accordingly.

Intrafamily loans could be a helpful option for many families looking to ease the financial burden that may come from a traditional loan and could help family members transfer wealth. It requires important attention to detail and careful record-keeping, so if you are considering such a loan, it may be beneficial to discuss it with your advisor.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Securities and additional investment advisory services offered through FSC Securities Corporation, member FINRA/SIPC and a registered investment adviser. 9601 Tamiami Trail North, Naples, FL. 239-262-6577.

A Thanksgiving Message From Ciccarelli Advisory Services

In the spirit of Thanksgiving, we would like to take a moment to express our gratitude for the special relationship we share with you.

We are thankful for the trust and confidence you have placed in our firm. Trust is the bedrock upon which all relationships are built, and we are proud to have established such a strong foundation of trust in our relationship with you.

Our team understands that many of you will be separated from friends and family this year, and celebrations may be taking place from afar. We want to offer our support and sincere gratitude for your continued strength and fortitude.

As our client, you have played an integral role in the success of Ciccarelli Advisory Services. Your wisdom, experience and insight have greatly enhanced our ability to advocate for your family’s financial future. We appreciate the many gifts that you bring to the table.

Lastly, we’d like to appreciate all the simple blessings we enjoy in our lives – family, friendship, food, shelter and so much more. Thanksgiving is the perfect occasion to reflect on how fortunate we truly are.

We wish you and your family a joyous Thanksgiving weekend!