Could A Major Tax Hike Be in Store for You?

By Kay Anderson, CFP®

As we head into February, our mailboxes are filling up with various tax documents. With the ongoing pandemic and USPS mail delays, it will be important this year to maintain a “2020 Tax Folder” to collect your documents as received and deliver them to your CPA. We suggest giving the majority of your items to your CPA with a note if you are missing a late filing K1 or 1099.

Many companies now provide copies in both hard copy form and online access. Your online access may be a good place to check if you are missing expected documents.

After the recent election as well as the ongoing pandemic, many are concerned with how their taxes may be impacted. Historically speaking, after downward economic conditions, it is not uncommon for taxes to be raised on high earners. Following WWII, income tax rates for high earners remained significantly higher than they are today for decades, with the top federal income tax rate at 91% for most of the 1950s. If we are to follow similar projections, this could mean some major tax hikes may be in store.

Some tax areas that the new administration has indicated they will adjust includes:

• Taxing long-term capital gains on incomes above $1 million at ordinary income rates instead of the current rates.

• Eliminating the step-up in basis that allows heirs to minimize taxes on inherited assets.

• Reducing the estate exemption and unified credit prior to the current sunset due 2026.

• Imposing the Social Security payroll tax on wages above $400,000.

• Limiting the value of itemized deductions to 28% for those with incomes above $400,000.

President Biden has indicated that he will not be increasing the tax rate for individual W-2 wage earners. However, depending on your income, the deductions that are available to you could be impacted. He has previously proposed limiting itemized deductions, such as the mortgage interest deduction, for individuals with higher incomes.

It is important to keep in mind that these changes have only been proposed so far. After an election, there is often a great deal of discussion of tax changes, but not all proposals come to fruition and it can take time to implement.

While we don’t know for sure what is ahead, we do know there are some planning techniques that are still available now:

• IRA Contributions – A traditional or Roth IRA contribution can be made up until April 15, 2021 (subject to contribution and income limitations)

• Self Employed Retirement Plan Contributions – A SEP IRA contribution can be made prior to tax filing up until April 15, 2021, or extension (subject to contribution and income limitations)

• Health Savings Account – A prior year contribution can be made up to $3,550 for individual plans and $7,100 for the family plan; for those over age 55 a $1,000 catch up contribution is available

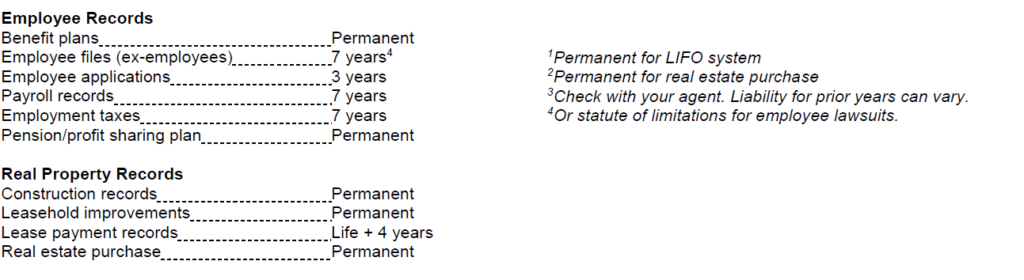

The pandemic has provided for extra downtime at home allowing us to focus on clearing out those closets, garages, and file cabinets that continue to accumulate through the year. It can be difficult to know what documents to keep and what can be tossed or shredded. Please see below our Retention Guidelines for reference…..if in doubt, reach out to our office and we are happy to review with you.

This is an excellent time to plan strategically for your future and future generations. Please reach out to schedule a time with your CAS advisory team.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Securities and additional investment advisory services offered through FSC Securities Corporation, member FINRA/SIPC and a registered investment adviser. 9601 Tamiami Trail North, Naples, FL. 239-262-6577.