CAS News

2015 Year-End Economic Update

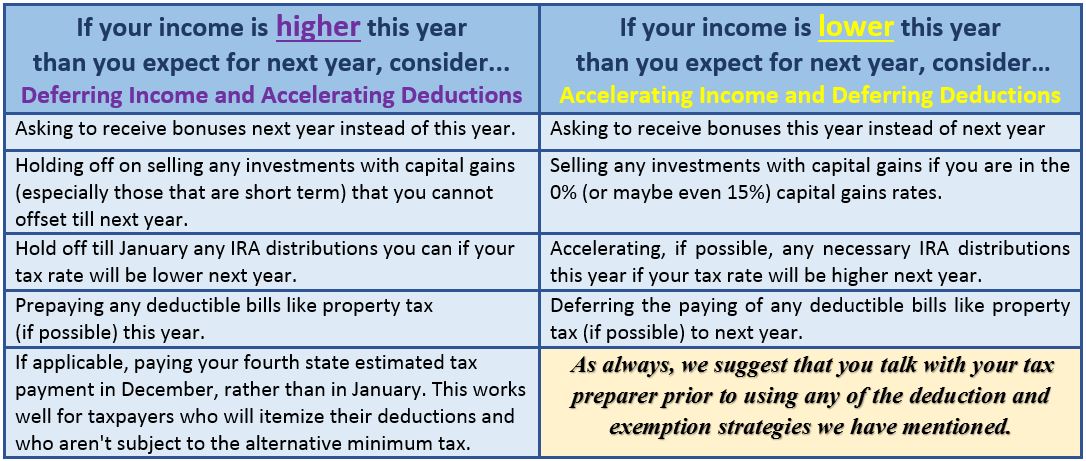

Year-End Tax Moves for 2015

Year-End Tax Moves for 2015

One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current on ever-changing tax reduction strategies. This special report covers the details of many year-end tax strategies for 2015.

Remember—every situation is different and not all strategies will be appropriate for you. Please discuss all tax strategies with your tax preparer prior to making any final decisions.

Income Tax Rates for 2015

Tax brackets have changed slightly for 2015. For example, for the 2014 tax year, the top of the 15% federal income tax bracket for married couples filing jointly was $73,800. In 2015, that figure has been increased to $74,900. Below is a table of federal income tax rates for 2015.

Year End Tax Planning For 2015

As you read through this report you will find some key aspects of the current 2015 tax laws and how they may apply to your situation. Late-breaking decisions in Washington, D.C., always make it difficult to plan ahead. This year is no different, with dozens of provisions waiting to be renewed.

One tax break that remains as an open-ended question is a tax deduction for contributions to charitable organizations directly from an individual retirement account (IRA). Some retirees are holding off on taking their required minimum distributions until they know what happens with this law. Right now, some lawmakers say this and other tax breaks, like the deductibility of sales tax in some states that do not have income taxes, might be renewed. However, nothing is a sure thing until a final bill is passed.

Despite this uncertainty, there are many year-end tax moves around income and expenses you can make to lessen your tax liability based on what you do know. To the extent that income or expenses can be moved between 2015 and 2016, for many investors, year-end tax planning often is about determining the best decision in which year to earn additional income or to incur more tax deductions. Now is the time to focus on how to optimize your situation between these two years.

The goal of this report is to share strategies that could be effective if discussed and implemented before year-end. Choosing the appropriate strategies will depend on your income, as well as a number of other personal circumstances. As with all tax strategies it is always in your best interest to discuss your personal situation with your tax preparer before making any moves or final decisions.

While everyone’s situation is unique, we urge you to begin your final year-end planning now!

Consider All of Your Retirement Savings Options for 2015

If you have earned income or are working, retirement savers should consider contributing to retirement plans. This is an ideal time to make sure you maximize your intended use of retirement plans for 2015 and start thinking about your strategy for 2016. For many investors, retirement plans represent one of the smarter tax moves that you can make. Here are some retirement plan highlights:

- Higher 401(k) contribution limits. The elective deferral (contribution) limit for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is $18,000. The catch-up contribution limit for employees aged 50 and over who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is an additional $6,000 ($24,000 total). As a reminder, these contributions must be made in 2015.

- IRA contribution limits unchanged.The limit on annual contributions to an Individual Retirement Arrangement (IRA) remains unchanged at $5,500. The additional catch-up contribution limit for individuals aged 50 and over is not subject to an annual cost-of-living adjustment and remains $1,000. IRA contributions can be made all the way up to the April 15, 2016 filling deadline.

- Higher IRA income limits.The deduction for taxpayers making contributions to a traditional IRA is phased out for singles and heads of household who are covered by a workplace retirement plan and have modified adjusted gross incomes (AGI) of $61,000 and $71,000 for 2015. For married couples filing jointly, in which the spouse who makes the IRA contribution is covered by a workplace retirement plan, the income phase-out range is 98,000 to $118,000 for 2015. For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered, the deduction is phased out in 2015 as the couple’s income reaches $183,000 and completely at $193,000 for 2015. For a married individual filing a separate return who is covered by a workplace retirement plan, the phase-out range is $0 to $10,000 for 2015. Please keep in mind, if your earned income is less than your eligible contribution amount, your maximum contribution amount equals your income.

- Increased Roth IRA income cutoffs.The AGI phase-out range for taxpayers making contributions to a Roth IRA is $183,000 to $193,000 for married couples filing jointly in 2015. For singles and heads of household, the income phase-out range is $116,000 to $131,000 in 2015. For a married individual filing a separate return, the phase-out range is $0 to $10,000 for 2015. Please keep in mind, if your earned income is less than your eligible contribution amount, your maximum contribution amount equals your income.

- Largersaver’s credit threshold. The AGI limit for the saver’s credit (also known as the retirement savings contribution credit) for low- and moderate-income workers is $61,000 for married couples filing jointly in 2015, $45,750 for heads of household, $30,500 for married individuals filing separately, and increasing to $30,500 for singles.

- Be careful of the IRA one rollover rule. IRA investors were always limited to one rollover per year, per IRA. Beginning on January 1, 2015, investors were limited to make only one rollover from all of their IRAs to another in any 12-month period. A second IRA-to-IRA rollover in a single year could result in income tax becoming due on the rollover, a 10 percent early withdrawal penalty, and a 6 percent per year excess contributions tax as long as that rollover remains in the IRA. Individuals can only make one IRA rollover during any one-year period, but there is no limit on trustee-to-trustee transfers. Multiple trustee-to-trustee transfers between IRAs and conversions from traditional IRAs to Roth IRAs are allowed in the same year. If you are rolling over an IRA or have any questions on this, please call us.

Roth IRA Conversions

Some IRA owners are considering converting part or all of their traditional IRAs to a Roth IRA. This is never a simple and easy decision. Roth IRA conversions can be helpful, but they can also create immediate tax consequences and can bring additional rules and potential penalties. It is best to run the numbers and calculate the most appropriate strategy for your situation. Call us if you would like to review your Roth IRA conversion options.

Capital Gains and Losses

Looking at your investment portfolio can reveal a number of different tax saving opportunities. Start by reviewing the various sales you have realized so far this year on stocks, bonds, and other investments. Then review what’s left and determine whether these investments have an unrealized gain or loss. (Unrealized means you still own the investment and haven’t yet sold it, versus realized, which means you’ve actually sold the investment.)

Know your basis. In order to determine if you have unrealized gains or losses, you must know the tax basis of your investments, which is usually the cost of the investment when you bought it. However, it gets trickier with investments that allow you to reinvest your dividends and/or capital gain distributions. We will be glad to help you calculate your cost basis.

Consider loss harvesting. If your capital gains are larger than your losses, you might want to do some “loss harvesting.” This means selling certain investments that will generate a loss. You can use an unlimited amount of capital losses to offset capital gains. However, you are limited to only $3,000 of net capital losses that can offset other income, such as wages, interest and dividends. Any remaining unused capital losses can be carried forward into future years indefinitely.

Be aware of the “wash sale” rule. If you sell an investment at a loss and then buy it right back, the IRS disallows the deduction. The “wash sale” rule says you have to wait at least 30 days before buying back the same security in order to be able to claim the original loss as a deduction. However, while you cannot immediately buy a substantially identical security to replace the one you sold, you can buy a similar security—perhaps a different stock in the same sector. This strategy allows you to maintain your general market position while utilizing a tax break.

Sell worthless investments. If you own an investment that you believe is worthless, ask your tax preparer if you can sell it to someone other than a related party for a minimal amount, say $1, to show that it is, in fact, worthless. The IRS often disallows a loss of 100% because they will usually argue that the investment has to have at least some value.

Always double check brokerage firm reports. If you sold a stock in 2015, the brokerage firm reports the basis on an IRS Form 1099-B in early 2016. Unfortunately, sometimes there could be problems when reporting your information, so we suggest you double-check these numbers to make sure that the basis is calculated correctly and does not result in a higher amount of tax than you need to pay.

Zero Percent Tax on Long-term Capital Gains

You may qualify for a 0% capital gains tax rate for some or all of your long-term capital gains realized in 2015. The strategy is to figure out how much long-term capital gain you might be able to recognize to take advantage of this tax break.

The 0% long-term capital gains tax rate is for taxpayers who end up in the 10% or 15% ordinary income tax brackets, which is up to $37,450 for single filers and $74,900 for joint filers (See chart on page 1). If your taxable income goes above this threshold, then any excess long-term capital gains will be taxed at a 15% capital gains tax rate and/or 20% capital gains tax rate, depending on how high your taxable income is for the year.

NOTE: The 0%, 15% and 20% long-term capital gains tax rates only apply to “capital assets” (such as marketable securities) held longer than one year. Anything held one year or less is considered “short-term capital gains” and is taxed at ordinary income tax rates.

If you are eligible for the 0% capital gains tax rate, it might be a good time to consider selling some appreciated investments to take advantage of it. Sell just enough so your gain pushes your income to the top of the 15% tax bracket, then buy new shares in the same company. The “wash sale” requirement to wait 30 days does not apply for gains. With “gains harvesting,” you can actually sell the stock and buy it back in the same day. Of course, there will be transaction costs such as commissions and other brokerage fees. At the end of the day you will have the same number of shares, but with a higher cost basis. Please remember, you must also review your state income tax rules to determine whether or not these gains will be tax-free at the state level.

If you’re ineligible for the 0% capital gains tax rate, but you have adult children in the 0% bracket, consider gifting appreciated stock to them. Your adult children will pay a lot less in capital gains tax than if you sold the stock yourself and gifted the cash to them.

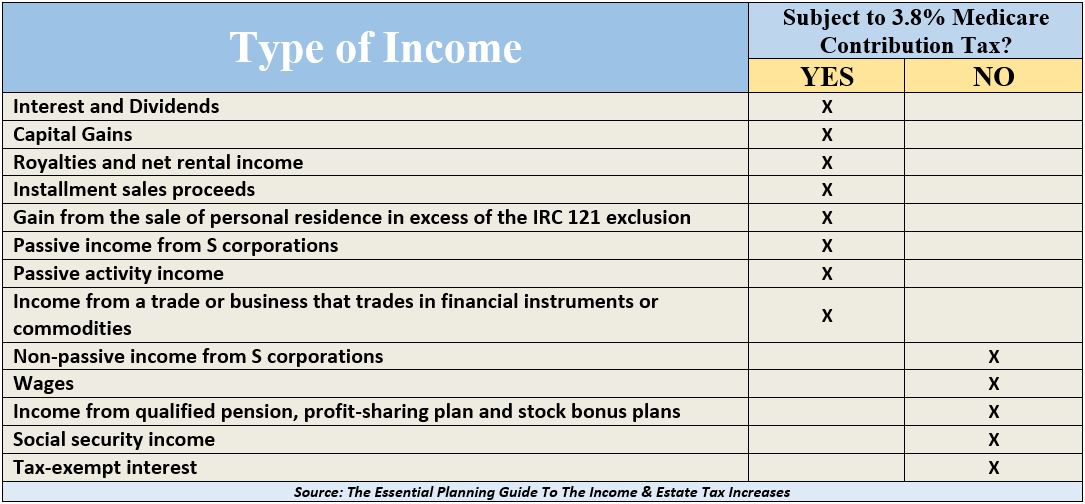

Medicare Tax

In 2015, a 3.8% Medicare surtax on “net investment income” remains in place for wealthy taxpayers. The 3.8% Medicare surtax is on top of ordinary income and capital gains taxes, meaning long-term capital gains and qualified dividends may be subject to taxes as high as 23.8%, while short-term capital gains and other investment income (such as interest income) could be taxed as high as 43.4%!

The Medicare surtax is imposed only on “net investment income” and only to the extent that total “Modified Adjusted Gross Income” (“MAGI”) exceeds $200,000 for single individuals and $250,000 for taxpayers filing joint returns. The chart attached shows which types of income are subject to this new Medicare tax.

For those of you who are subject to this new Medicare surtax, some of the strategies that we can consider will take time to implement. Now is a good time to review your situation. For example, you might:

- Consider investing in tax-advantaged vehicles such as: tax-exempt bonds, qualified retirement accounts, qualified annuities, or cash value life insurance policies (assuming that the cost of acquisition and maintenance does not exceed the tax savings).

- Convert passive real estate activities to active interests.

- Marry someone who has large capital loss carry-forwards, or currently has large net operating losses (just joking!).

Taxation of Social Security Income

Social Security income may be taxable, depending on the amount and type of other income a taxpayer receives. If a taxpayer only receives Social Security income, this income is generally not taxable (and it is possible that the taxpayer might not even need to file a federal income tax return).

If a taxpayer receives other income in addition to Social Security income, then up to 85% of the Social Security income could be taxable. There is a “floor” ($32,000 married filing jointly; $0 married filing separately; $25,000 all other taxpayers) whereby a portion of Social Security benefits become taxable and that the 85% inclusion kicks in once provisional income goes above a “ceiling” ($44,000 married filing jointly; $0 married filing separately; $34,000 all other taxpayers). For married taxpayers filing a joint return and for married persons filing separately who do not live apart from their spouses for the whole year, the “provisional income” threshold is $0. A complicated formula is necessary to determine the amount of Social Security income that is subject to income tax. (We suggest using the worksheet in IRS Publication 915 to make this determination.)

Finally, it is important to note that Social Security income is included in the calculation of “Modified Adjusted Gross Income” (“MAGI”) for purposes of calculating the 3.8% Medicare surtax on “net investment income” (as discussed earlier). Therefore, taxpayers having significant net investment income might have more reason to defer Social Security benefits.

Itemized Deductions & Exemptions

Taxpayers are entitled to take either a standard deduction or itemize their deductions on IRS Form 1040, Schedule A. Itemized deductions include, but are not limited to, mortgage interest, certain types of taxes, charitable contributions and medical expenses. Unfortunately, itemized deductions are subject to several limitations. For example, in 2015 medical expenses are deductible only to the extent that they exceed 10% of AGI this year. However, if you or your spouse are over 65, the deduction limit is still at 7.5% until December 31, 2016.

Consider “bunching” your deductions. Many taxpayers don’t have enough itemized deductions to reduce their taxes more than if they take the standard deduction. If you find you often miss the threshold by only a small amount per year, it may be best to “bunch” your deductions every other year, taking a standard deduction in the alternate years. The standard deduction for 2015 is $6,300 for singles, $6,300 for married persons filing separate returns, and $12,600 for married couples filing jointly.

Charitable Giving

This is a great time of the year to clean out your garage and give your items to charity. Please remember that you can only write off these donations to a charitable organization if you itemize your deductions. Sometimes your donations can be difficult to value. You can find estimated values for your donated clothing at http://turbotax.intuit.com/personal-taxes/itsdeductible/.

Send cash donations to your favorite charity by December 31, 2015, and be sure to hold on to your cancelled check or credit card receipt as proof of your donation. If you contribute $250 or more, you also need a written acknowledgement from the charity.

If you plan to make a significant gift to charity this year, consider gifting appreciated stocks or other investments that you have owned for more than one year. Doing so boosts the savings on your tax returns. Your charitable contribution deduction is the fair market value of the securities on the date of the gift, not the amount you paid for the asset, and therefore you avoid having to pay taxes on the profit!

Do not donate investments that have lost value. It is best to sell the asset with the loss first and then donate the proceeds, allowing you to take both the charitable contribution deduction and the capital loss. Also remember, if you give appreciated property to charity, the unrealized gain must be long-term capital gain in order for the entire fair market value (FMV) to be deductible. (The amount of the charitable deduction must be reduced by any unrealized ordinary income, depreciation recapture and/or short-term gain.)

The laws allowing taxpayers age 70½ and older to transfer up to $100,000 directly from their IRA over to a charity, satisfying all or part of the required minimum distribution (RMD), have not been renewed for 2015; in 2014 this was renewed very late in the year. We will keep you informed if this IRA-to-charity strategy is passed.

Other Year-End Tax Strategies and Ideas

Other Year-End Tax Strategies and Ideas

Make use of the annual gift tax exclusion. You may gift up to $14,000 tax-free to each person in 2015. These “annual exclusion gifts” do not reduce your lifetime gift tax exemption. (NOTE: The annual exclusion gift is doubled to $28,000 per recipient for joint gifts made by married couples or when one spouse consents to a gift made by the other spouse.)

Help someone with medical or education expenses. There are opportunities to give unlimited tax-free gifts when you pay the provider of the services directly. The medical expenses must meet the definition of deductible medical expenses. Qualified education expenses are tuition, books, fees, and related expenses but not room and board. You can find the detail qualifications in IRS Publications 950 and the instructions for IRS Form 709, which are available for free at www.irs.gov.

Contribute to a 529 plan on behalf of a beneficiary. This qualifies for the annual gift-tax exclusion. Withdrawals (including earnings) used for qualified education expenses (tuition, books and computers) are income tax free. The tax law even allows you to give the equivalent of five years’ worth of contributions up front with no gift-tax consequences. Non-qualifying distribution earnings are taxable and subject to a 10% tax penalty.

Make gifts to trusts. These gifts often qualify for the annual exclusion ($14,000 in 2015) if the gift is direct and immediate. A gift that meets all the requirements removes the property from your estate. The annual exclusion gift can be contributed for each beneficiary of a trust. We are happy to review the details with your estate planning attorney.

If possible, prepare a tax projection for 2015 and 2016 to determine if you will have a change in your tax situation. Then consider the following strategies if they apply to your situation.

It is important to note that some itemized deductions (such as state income taxes, real estate taxes and miscellaneous itemized deductions) are not allowed when computing the “Alternative Minimum Tax” (“AMT”). If you are subject to the AMT, it is often best to delay payment on the disallowed deductions and push them off until 2016 or later tax years (when AMT is no longer an issue). It is always possible you might be able to use the deductions next year. Therefore, we suggest that you talk with your tax preparer about AMT prior to using any of the deduction and exemption strategies we have mentioned.

Conclusion

One of our primary goals is to keep clients aware of tax law changes and updates. This report is not a substitute for using a tax professional. In the 1980’s, one teenager was preparing his tax return. He came across a negative number that he had to put in, and there was nothing in the instructions about dealing with negative numbers, so he just left it the way it was. His tax refund amounted to roughly $30. The IRS did not accept his return because according to them he was supposed to put “0” anywhere there was a negative number, even though there was nothing written in the instructions. The IRS showed the instructions for the next year’s tax return which did specify that rule. After many years of writing back and forth, the taxpayer finally went to the local IRS and proved to the IRS agent that he was right. He finally got his refund years later after many hours wasted on explaining his situation to the IRS. (Source: efile.com)

One of our primary goals is to keep clients aware of tax law changes and updates. This report is not a substitute for using a tax professional. In the 1980’s, one teenager was preparing his tax return. He came across a negative number that he had to put in, and there was nothing in the instructions about dealing with negative numbers, so he just left it the way it was. His tax refund amounted to roughly $30. The IRS did not accept his return because according to them he was supposed to put “0” anywhere there was a negative number, even though there was nothing written in the instructions. The IRS showed the instructions for the next year’s tax return which did specify that rule. After many years of writing back and forth, the taxpayer finally went to the local IRS and proved to the IRS agent that he was right. He finally got his refund years later after many hours wasted on explaining his situation to the IRS. (Source: efile.com)

Please note that many states do not follow the same rules and computations as the federal income tax rules. Make sure you check with your tax preparer to see what tax rates and rules apply for your particular state.

There are many other additional tax reduction strategies that will vary depending on your financial picture. We encourage all of our clients and prospects to come in so that we can review your particular situation and hopefully take advantage of those tax rules that apply to you.

The views expressed are not necessarily the opinion of FSC Securities Corporation, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. This article is for informational purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice as individual situations will vary. For specific advice about your situation, please consult with a financial professional. Contents Provided By the Academy of Preferred Financial Advisors, Inc. Reviewed by Keebler & Associates. © Academy of Preferred Financial Advisors, Inc.

NCH Hospital Ball

Ciccarelli Advisory Services, Inc. is pleased to be a presenting sponsor of the 57th Annual NCH Hospital Ball, to be held on Saturday, November 14, 2015 at The Ritz Carlton Beach Resort in Naples, Florida. We are honored to have as Chairs of this year’s event, our own Kim Ciccarelli Kantor and Jan Kantor, both who have a long history of philanthropic interests.

Ciccarelli Advisory Services, Inc. is pleased to be a presenting sponsor of the 57th Annual NCH Hospital Ball, to be held on Saturday, November 14, 2015 at The Ritz Carlton Beach Resort in Naples, Florida. We are honored to have as Chairs of this year’s event, our own Kim Ciccarelli Kantor and Jan Kantor, both who have a long history of philanthropic interests.

Each year, the proceeds raised through support of the NCH Ball help to fund various projects of the NCH Healthcare system, a non-profit organization helping to provide care to those in need. Over $7,000,000 has been raised to date, adding valuable equipment and services to our community.

This year’s NCH Ball will benefit the NCH Foglia Comprehensive Stroke Center. In 2014, our Hospital treated over 700 patients who showed symptoms of, or who experienced a full blown stroke. It is the primary cause of severe long-term disability and the 4th leading cause of death within the U.S. Each year, stroke affects over 795,000 Americans, with over 130,000 deaths[1]. The costs also add up. Costs in the U.S. alone, total an estimated $34 billion each year[2]. Stroke is not discriminatory, giving no distinction to ethnicity, gender or even age. It can affect everyone and anyone. The need, therefore, for a state of the art stroke care center in Collier County is crucial. The proceeds will specifically benefit the addition of a new bi-plane to the NCH North Campus to ensure the provision of timely stroke care.

The Ball will feature a night of dinner and dancing and live and silent auctions to raise money to fund this year’s mission. Anyone who wishes to support the event and its mission are welcomed to purchase tickets to attend at www.NCHmd.org/hospitalball. There will also be an opportunity to participate in the auction two weeks prior to the event by bidding on auction items online.

Please join Ciccarelli Advisory Services, Inc. in lending your support for this worthy cause. For more information, contact Monica at the NCH Healthcare Foundation at 239-624-5000.

[1] Source: http://www.cdc.gov/stroke/facts.htm

[2] Source: http://www.cdc.gov/stroke/facts.htm

Ciccarelli Advisory Services, Inc. Attend ConnectED Conference

Advisors from Ciccarelli Advisory Services Inc., affiliated with FSC Securities Corp, recently attended AIG Advisor Group’s 2015 ConnectED conference. Attendees included Kay Anderson, Paul Ciccarelli, Ray Ciccarelli, Carol Girvin, Anthony Curatolo, Lynn Ferraina, Jasen Gilbert, Kim Ciccarelli Kantor, Christopher LaFountain, Steve Merkel, Jill Ciccarelli Rapps, Geral Smith, Judy Alexander-Wasley and Samantha Webster. The annual event was hosted at the Henry B. Gonzalez Convention Center in San Antonio from September 28 to October 1. Over 3,000 attendees, including financial advisors from FSC Securities Corporation, Royal Alliance Associates, Inc., SagePoint Financial, Inc. and Woodbury Financial Services, Inc., AIG Advisor Group’s four broker-dealers, were present at the event.

Advisors from Ciccarelli Advisory Services Inc., affiliated with FSC Securities Corp, recently attended AIG Advisor Group’s 2015 ConnectED conference. Attendees included Kay Anderson, Paul Ciccarelli, Ray Ciccarelli, Carol Girvin, Anthony Curatolo, Lynn Ferraina, Jasen Gilbert, Kim Ciccarelli Kantor, Christopher LaFountain, Steve Merkel, Jill Ciccarelli Rapps, Geral Smith, Judy Alexander-Wasley and Samantha Webster. The annual event was hosted at the Henry B. Gonzalez Convention Center in San Antonio from September 28 to October 1. Over 3,000 attendees, including financial advisors from FSC Securities Corporation, Royal Alliance Associates, Inc., SagePoint Financial, Inc. and Woodbury Financial Services, Inc., AIG Advisor Group’s four broker-dealers, were present at the event.

“ConnectED has grown into one of our most successful education events for all advisors in the AIG Advisor Group network,” said Erica McGinnis, President and CEO of AIG Advisor Group. “This year we provided attendees with the exclusive opportunity to really hone in on business and practice development tools and resources. We’re confident that advisors left the conference with new and applicable knowledge to better serve their clients and grow their businesses.”

ConnectED 2015’s keynote speakers included Malcolm Gladwell, journalist and best-selling author, as well as Peter H. Diamandis, engineer, physician, author, Chairman/CEO of the X Prize Foundation and Executive Chairman of Singularity. The conference also featured more than 120 educational sessions on a range of topics reflecting the most current industry trends, best practices, products and policies.

Video: Chasing Performance – Ciccarelli Advisory Services

Chasing performance can be like running in reverse. Remember: it’s not a race, it’s a marathon.

Turtles on the Town

Ciccarelli Advisory Services, Inc. is pleased to announce our participation in “Turtles on the Town,” a Naples, Florida community arts project featuring 50 loggerhead sea turtle sculptures. These turtles will take up residence at various locations throughout Collier County, including one sculpture at our Florida office, beginning in November 2015 and continuing through February 2016. Local artists have lent their talents in making these sculptures come to life with ocean-based themes.

We’d like to introduce you to our turtle, whom we’ve affectionately named Terrance. His theme is “Under the Sea” and was commissioned to be completed by artist Nancy Job. Nancy hails from Rockford, Illinois but has made Naples, Florida her home for a number of years. Her work has been displayed in many venues including the Von Liebig Art Gallery, the University of Wisconsin and the United Arts Council at Rookery Bay.

We’d like to introduce you to our turtle, whom we’ve affectionately named Terrance. His theme is “Under the Sea” and was commissioned to be completed by artist Nancy Job. Nancy hails from Rockford, Illinois but has made Naples, Florida her home for a number of years. Her work has been displayed in many venues including the Von Liebig Art Gallery, the University of Wisconsin and the United Arts Council at Rookery Bay.

Terrance is 4’ high by 4’ wide and weighs about 75 pounds. His design comprises beautiful sea-based hues of blues and greens, reminiscent of the vibrance of the under-water world, with splashes of gold. He is brought to life using various mediums including acrylic, glitter and sea glass. Nancy’s inspiration comes from her passion for landscapes and wildlife. She wanted Terrance to reflect the colors of the sea and the coral reefs, but also sparkle like the sun’s rays reflecting on the ocean’s surface.

The Turtles on the Town Exhibition is ultimately for the benefit of three local charities – the Community Foundation of Collier County, the Conservancy of Southwest Florida, and the United Arts Council of Collier County. Supporters will have an opportunity to bid to purchase their turtle of choice at a Gala to be held at the Conservancy of Southwest Florida on March 9, 2016. For more information on the Turtles on the Town project, please visit http://www.turtlesonthetown.com/

The turtles “hatch” in November 2015. Be sure to stop by our office to meet and “sea” Terrance the Turtle. He will be more than happy to greet you.

Economic Update – Third Quarter 2015

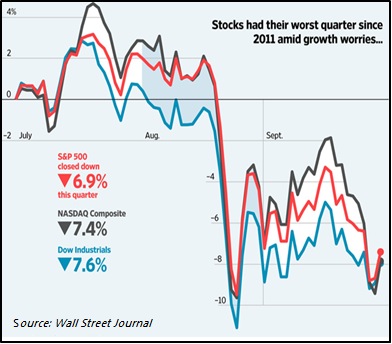

This past quarter was a difficult one for even the smartest of investors. Many money managers were hoping for a chance to purchase equities at cheaper prices, however they forgot the old adage, “Be careful what you wish for.” Those money managers learned that lesson this quarter. For nearly four years,

This past quarter was a difficult one for even the smartest of investors. Many money managers were hoping for a chance to purchase equities at cheaper prices, however they forgot the old adage, “Be careful what you wish for.” Those money managers learned that lesson this quarter. For nearly four years,

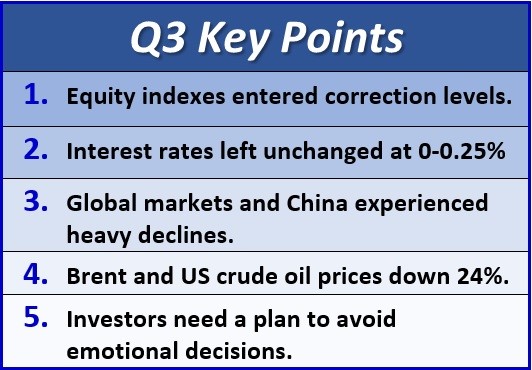

stocks had been heading in one direction—up—and some money managers were all but begging for a selloff so they could purchase great companies at bargain-basement prices. They got their chance in August when the Standard & Poor’s 500 index officially entered a correction—defined as a decline of 10% or more—with some of the market’s most revered companies declining in price for little or no reason.

After several healthy years the equity markets have taken a break from their continuous upward movements. For the quarter, the Standard and Poor’s 500 index fell 6.9%, leaving most investors with losses. This was the index’s worst quarter since 2011. After a few years of what now is being referred to by many as slow, calm and steady movements, the stock market has returned to some of the most gut-wrenching price swings since the 2007-2009 financial crisis. (Source: Wall Street Journal, 9/30/2015)

Although most long term investors understand that over long periods of time the equity markets can provide reasonable returns, the market swings of this past quarter have been confusing and even some of the most disciplined investors have been afraid to buy on the dips. During these times, Vanguard Investments reminds investors that, “It’s natural to have lots of questions when the market swings up and down. Volatility is common, and often the wisest thing to do is stick with your investment plan.” They go on to reason that in highly volatile market environments investors need to remember what they refer to as market volatility Rule #1: Recognize that volatility and periodic corrections are common in equity markets. Vanguard suggests that the key to getting through unexpected turbulence is to understand that swings in the financial market are normal—and relatively insignificant over the long haul. (Source: Vanguard.com, 9/2015)

Market pull backs are not a new concept but now that it’s Fall, investors are bracing for additional large price swings across stocks and bonds heading into a month that is usually associated with market tumult. Although the markets are down, many analysts said other signals of a U.S. recession haven’t materialized. They still expect the U.S. economy to expand at a modest but healthy 2.5% annual rate this year and point out that unemployment is at its lowest levels since early 2008. Consumer spending, another major growth driver, is strengthening. (Source: Wall Street Journal, 9/30/2015)

The S&P 500 is down more than 5% since the end of July. This means that the S&P 500 trades at 16.7 times the past 12 months of earnings, compared with its 10-year average of 15.7, according to FactSet. In early August, before the S&P 500 fell into correction territory, it traded at 18.2 times the past year of earnings.

Commentary from some market strategists seems to be less upbeat than in past years, however overall it still remains optimistic. The main dissention in the group is over how fast and how far markets will move. “U.S. stock valuations are reasonable given the prospects for growth and inflation,” says Russ Koesterich, Global Chief Investment Strategist at Blackrock, who worried about “stretched” valuations in December. Near term he feels stocks are still “particularly attractive relative to bonds.” Dubravko Lakos-Bujas, Chief U.S. Equity Strategist at JPMorgan Chase agrees. He feels that compared with International markets, the U.S. provides stocks of superior quality. (Source: Barron’s, 9/7/2015)

Commentary from some market strategists seems to be less upbeat than in past years, however overall it still remains optimistic. The main dissention in the group is over how fast and how far markets will move. “U.S. stock valuations are reasonable given the prospects for growth and inflation,” says Russ Koesterich, Global Chief Investment Strategist at Blackrock, who worried about “stretched” valuations in December. Near term he feels stocks are still “particularly attractive relative to bonds.” Dubravko Lakos-Bujas, Chief U.S. Equity Strategist at JPMorgan Chase agrees. He feels that compared with International markets, the U.S. provides stocks of superior quality. (Source: Barron’s, 9/7/2015)

Analysts are cautious for now, but among 21 strategists followed by Birinyi Associates, the average S&P 500 price target for 2015 is currently 2177. If it ends the year at that level, it would mark a gain of 5.8%, lower than the 8.4% increase forecast in the middle of this year, but still up. (Source: Wall Street Journal, 9/30/2015)

Interest Rates

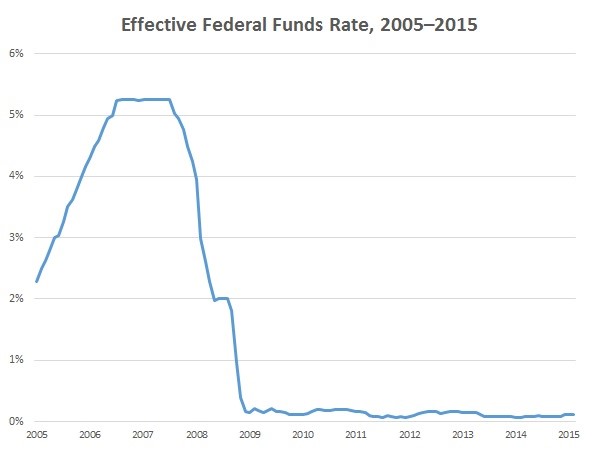

Will the Fed raise rates or won’t they? That still remains the main question when it comes to interest rates. Despite the insistence that they were using a monetary based policy to decision making, every time analysts felt the Fed was going to raise interest rates, they came away feeling like participants in the movie Groundhog’s Day.

All throughout the quarter Janet Yellen and her colleagues took a wait—and—see approach which analysts feel contributed to the market’s volatility. When it was all said and done the Federal Open Market Committee left the Federal Funds rate (the rate banks charge each other for overnight loans of funds maintained at the Fed) unchanged at 0%—0.25%. They also left no clear direction as to exactly when they would raise rates. While they spoke of raising them before year-end, they also said they would have to carefully watch several factors like the job market and the risks created by overseas turmoil. Without decisive action from the Fed, or greater clarity about its intentions, analysts are predicting the markets will continue to be volatile. (Source: Barron’s, 9/21/2015)

History has shown that the first interest-rate hike in a Federal Reserve tightening cycle is not the start of a market or economic downturn. In the past, economically sensitive assets, such as equities, have performed well during the period immediately after the initial hike. A Fed rate hike might also remove the unclear feeling that some investors may have about monetary policy and the U.S. economy, which may have the offsetting impact of boosting investor confidence. Even if later this year in October or December, the Federal Reserve issues its first interest rate hike in over nine years, analysts feel it won’t give the economy a sharp kick. They are suggesting it will be more of a gentle nudge, though significant. Once again investors will need to keep a watchful eye on interest rate movements. (Source: Fidelity 10/2015)

Global Concerns & China

This quarter, global markets and investors also experienced difficulties. Global stock markets saw their weakest quarterly performance in four years with trouble predicted in the world’s two largest economies. After a sustained collapse in commodity prices, China’s equity markets dropped and then Chinese officials announced a shocking currency devaluation. Continued fears of a Greek default made the past three months a summer to remember (or forget) for investors.

“Global equities are closing in on their worst quarter since 2011, with a number of factors fueling fears in an already jittery market, including weak global growth, driven by deceleration in emerging markets, particularly China,” Barclays analysts said in a late September report. China’s benchmark Shanghai Composite appeared to be one of the world’s worst performers of the quarter with a 25% loss, its weakest performance since 2008. In Europe, Germany’s Dax experienced a 15% decline, -11% for the French CAC, -8% for Italy and -13% for Spain’s IBEX. Moving forward, many analysts are expecting a cloud of pessimism to loom over global equity markets for a while. (Source: CNBC, 9/30/2015)

Oil Prices

Oil prices have fallen a long way over the last year. For the quarter, both Brent and U.S. crude oil were down 24% for their sharpest decline since the end of 2014. Heading into the fourth quarter, analysts are predicting that energy markets should stabilize as production in the U.S. subsides. The falling of oil prices has both positive and negative impacts on the economy. On the negative side, prices of oil stocks and employment in oil and oil-related industries has declined. This hit to the energy sector has taken a toll on the earnings of oil related stocks and has delayed or canceled many of their planned capital expenditures. On the positive side, consumer relief at the pumps will hopefully turn into more savings or ability to spend for consumers.

Analysts also feel that it now appears the majority of the damage has been done and oil prices may be stabilizing. Oil prices contributed to the market’s decline and are another concern that need to be monitored by investors. (Source: Seeking Alpha 10/4/2015)

Conclusion: What Can an Investor Do?

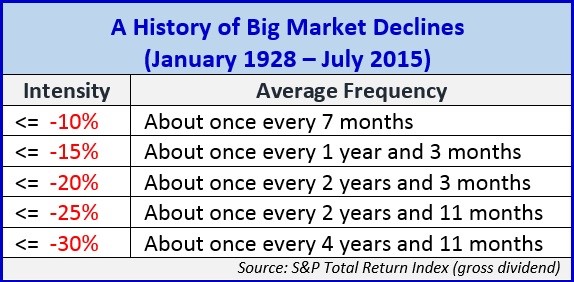

The more often you update yourself on the market’s fluctuations, the more volatile and risky it will appear to you — even though short, sharp declines of 5% to 25% are common. The U.S. stock market has, in the past few years, been extraordinarily placid by historical standards. Even the sudden drops of the past month are well within the long-term norm. Fixating on fluctuations in the short term will make it harder for you to remain focused on your long-term investing goals. (Source: Wall Street Journal, 9/30/2015)

Have a plan. Even the savviest of investors need a plan. When equity markets are gyrating on a daily basis it is easy to make emotional decisions that could prove to be wrong.

Focus on your own personal objectives. During confusing times it is always wise to create realistic time horizons and return expectations for your own personal situation and to adjust your investments accordingly. Understanding your personal commitments and categorizing your investments into near-term, short-term and longer-term can be helpful.

Don’t try to predict the market. Investment decisions driven by emotion can cause problems for investors. Discipline and perspective can help investors remain committed to their long-term investment programs through periods of market uncertainty. The best investors try not to constantly look back and second guess their decisions. They make decisions based on facts and data points.

A portfolio strategy can assist in helping you weather ups and downs of the market. Corrections are a normal part of investing. With a strong plan in place, many investors need not worry or adjust their approach at all. Even for those who are retired, it’s helpful to consider an income strategy that includes enough regular flow of money—including Social Security, pensions, or other income sources—to cover housing, food, and other essential & discretionary expenses whether the market is up or down.

Make sure you have adequate liquidity. When the market is down, cash can be a valuable shock absorber. You may want to consider using the cash portion of your portfolio to delay the need to sell equities while the market is down. Selling equities in a downturn leaves you with less invested when a recovery comes, turning what may be a temporary market decline into a permanent “dent” in your portfolio. Having cash on hand may help give you the opportunity to participate in a recovery.

Get used to volatility. As the chart of market declines shows, volatility and market declines are a part of investment history. Legendary investor Warren Buffett maintains that, just because markets were volatile doesn’t mean that for a long-term investor — which is the prism through which Buffett sees markets — the stock market was necessarily riskier. He advises investors not to confuse volatility with risk.

Get used to volatility. As the chart of market declines shows, volatility and market declines are a part of investment history. Legendary investor Warren Buffett maintains that, just because markets were volatile doesn’t mean that for a long-term investor — which is the prism through which Buffett sees markets — the stock market was necessarily riskier. He advises investors not to confuse volatility with risk.

As always, discuss any concerns with us.

Our advice is not one-size-fits-all. We will always consider your feelings about risk and the markets and review your unique financial situation when making recommendations.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

P.S. Janet Yellen is plotting the monetary future using complex data points that consider inflation, employment, and productivity. But one strategist is resorting to more tangible evidence: bacon cheeseburgers.

P.S. Janet Yellen is plotting the monetary future using complex data points that consider inflation, employment, and productivity. But one strategist is resorting to more tangible evidence: bacon cheeseburgers.

Nicholas Colas, chief market strategist at Convergex, a global brokerage based in New York, tracks “off the grid” economic indicators. He found that measuring the prices of ingredients in a bacon cheeseburger can determine the impact of inflation.

Colas tracked prices for ground beef, cheese, and bacon since 1980—he left off the bun “in deference to history and those on a low-carb diet.” It turns out the bacon-cheeseburger index reveals deflation over the past few months. On a year-over-year basis, the ingredients fell 2.9% in June, 1.2% in July, and 2.7% in August. Historically, bacon-cheeseburger deflation has signaled a slowing economy, he notes.

“Go back through the price history, and negative 3% to 4% price declines for bacon cheeseburgers are often a sign that the Fed needs to cut interest rates and push liquidity into the domestic economy. I know that sounds weird, but the last time our bacon cheeseburger showed negative price trends of this magnitude was in 2009. Before that, it was 1998 [Asia crisis] and 1991-92 [Gulf War I].”

Will Yellen heed the warning and delay rate hikes? Colas urges her to sink her teeth into this issue, “Even if bacon cheeseburgers aren’t on the cafeteria menu at Fed HQ, Chair Yellen would do well to heed the sizzle of deflationary pressures.” (Source: Barron’s, 10/2/2015)

Note: The views stated in this letter are not necessarily the opinion of FSC Securities Corporation and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results. The Standard and Poors 500 index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy. Through changes in the aggregate market value of 500 stocks representing all major indices. The Dow Jones Industrial average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. © The Academy of Preferred Financial Advisors, Inc. Sources: Wall Street Journal, Barron’s, Vanguard, Seeking Alpha, Fidelity

Caring for Your Aging Parents

Caring for your aging parents is something you hope you can handle when the time comes, but something you probably hope you never have to do. Caring for your aging parents means helping them plan for the future, and this can be overwhelming, both physically and emotionally. When the time comes for you to take care of your parents, you may be certain of only two things: Your parents need you, and you need help.

(Download the Caring for Aging Parents Checklist.)

Start planning

Talk to your parents about the future

Start caring for your aging parents by talking with them about their needs and wishes if they are able. In some cases, however, they may not be willing to talk to you about their future, either because they are afraid to face it or because they resent your interference. If this is the case, you may need to do as much planning as you can without them, or, if their safety or health is in danger, step in as caregiver anyway.

Prepare a personal data record

The first step you should take is to ask your parents to help you prepare a personal data record (if they are unable to help you, you’ll have to search for the information yourself). A personal data record is a document that lists information that you might need in case your parents become incapacitated or die. Information that should be included is financial information, legal information, medical information, insurance information, and information regarding professional advisors and the location of important records. Example(s): When Marcia and her mother prepared a personal data record, Marcia realized that her mother did not have a durable power of attorney or health care proxy in case she became incapacitated and could not make decisions about her medical care. The next day, Marcia made an appointment with her mother’s lawyer to discuss this issue.

Get advice

You can’t know everything, and you probably don’t have enough time to learn everything you need to know to care for your parents. That’s why you should seek advice from professionals. Some advice will be free, and some you will have to pay for. If you live far from your parents or are too overwhelmed to handle all your parents’ affairs, you can hire a geriatric care manager who will evaluate your parents’ situation, suggest options, and coordinate professionals who can help. In addition, talk to your employer. Some employers have set up employee assistance programs that offer advice and assistance to people who are dealing with personal challenges, including caring for aging parents.

Get support

Don’t try to care for your parents alone. Many local and national caregiver support groups and community services are available to help you cope with caring for your aging parents. If you don’t know where to start finding help, call the Eldercare Locator, an information and referral service sponsored by the federal government that can direct you to resources available nationally or in your area. Call the Eldercare Locator at (800) 677-1116.

What kind of advice will you need?

Housing and health care advice

If your parents are like many older individuals, where they live will depend upon how healthy they are. As your parents grow older, their health may deteriorate so much that they can no longer live on their own. At this point, you may need to find them in-home health care or health care within a retirement community or nursing home. On the other hand, you may want them to move in with you. In addition, you will need information on managing the cost of health care, long-term care insurance, major medical insurance, Medicare, and Medicaid.

Contact:

- National Association for Home Care

- Visiting Nurse Associations of America

- Centers for Medicare & Medicaid Services (formerly known as the Health Care Financing Administration)

- American Association of Homes and Services for the Aging

- American Association of Retired Persons (AARP)

- Health Insurance Association of America

Financial advice

If your parents need help managing their finances, you may need to contact professionals whose advice both you and your parents can trust, including one or more of the following individuals or organizations.

Contact:

- Your financial planner

- Your banker

- Your investment counselor

- Your tax attorney

- The Social Security Administration

Legal advice

Legal advisors can help you plan for your parents’ incapacity (including preparing documents such as power of attorneys, medical directives, and living wills), contact nursing home ombudsmen, set up and monitor guardianship, prepare wills, give tax advice, and provide bill payment and representative payee assistance. Many states provide funds for the delivery of free legal services to the elderly and many attorneys specialize in elder law, so finding legal advice shouldn’t be difficult.

Contact:

- Your attorney

- National Association of State Units on Aging

- American Bar Commission on the Legal Problems of the Elderly

- Legal Counsel for the Elderly

What kinds of support and community services will you need?

Caring for your aging parents will be easier if you know what kinds of support and community services are available and where to locate them. The following is a list of the kinds of support and community services you can find locally and nationally, along with specific suggestions of who to contact for information.

Adult day care

If you need to work or run errands and you can’t leave your parents alone, consider using adult day care. These programs are located in hospitals, churches, temples, nursing homes, or community centers. Many are private nonprofit organizations. Adult day care can be expensive but is sometimes subsidized by the government, and fees may be based on a sliding scale. In addition, Medicare, Medicaid, long-term care insurance, or your health insurance may pay part of the cost.

Contact:

- Your local senior center or community center

- National Institute on Adult Day Care

- The Alzheimer’s Association

Caregiver support groups (self-help)

Many self-help groups are available to provide information and emotional support on broad topics (such as aging) or specific topics (such as heart disease). You may find these support groups helpful if you know little about caring for your aging parents. Such groups might also provide an opportunity to help others by sharing your experiences.

Contact:

- The Alzheimer’s Association

- Children of Aging Parents

- National Self-Help Clearinghouse

Caregiver training/health education

You may feel better about taking care of your parents if you are armed with knowledge. You may want to complete first-aid courses or take classes in gerontology.

Contact:

- Your local college or university

- Your local hospital

- The American Red Cross

Geriatric assessment

If you are uncertain of your parent’s mental or physical capabilities, ask his or her doctor to recommend somewhere you can take your parent to undergo an assessment. These assessments can be done at hospitals or clinics. Your parent will be evaluated to determine his or her capabilities. The evaluation determines whether the individual can take care of himself or herself on a day-to-day basis, including such things as bathing, dressing, eating, using the telephone, doing housework, and managing money. Based on this evaluation, you and your parent will receive advice regarding care options.

Contact:

- Your doctor

- Your lawyer

- The National Association of Professional Geriatric Care Managers

- Aging Network Services

Respite care

When you are caring for your aging parents, you may feel guilty or even resentful because you don’t have limitless energy. Taking care of your parents is hard work, however, and everyone needs a break once in a while. If you are caring for your aging parents, look into respite care. Medicaid may pay for some respite-care services.

Contact:

- Your doctor

- Your local hospital

- The Alzheimer’s Association

- National Association for Home Care

Financial and tax considerations for you

Caring for your aging parents is not only an emotional burden for you but may be a financial one as well, depending upon how well off your parents are and how much caring for them costs. Because many adults today are becoming first-time parents in their thirties, and others are remarrying and rearing second families, increasing numbers of adults are finding themselves in the “sandwich generation.” They face having to pay expenses of growing children (including college expenses), plan for their own retirement, and support their aging parents financially. Thus, it’s important to plan not only your parents finances, but your own as well.

Financial planning for your parents

Making sure that your parents won’t outlive their money is a critical step in ensuring that your own finances will remain sound. In particular, you’ll need to make sure that your parent is receiving all the benefits to which he or she is entitled and that his or her money is invested wisely. You’ll also need to create a financial profile for your parents, a statement that includes income, expenses, and net worth. If, after considering your parent’s financial condition, it’s clear that they won’t have enough resources to pay for their own care, you’ll need to find ways to supplement their income. You may need to look at Supplemental Security Income (SSI) , for instance, or ask other relatives for help. You’ll also have to determine how much financial support you can give your parents (see below).

Financial planning for you

Besides caring for your parents, you have a lot of other financial obligations. Before you can determine the best way to help your parents financially, you’ll have to look at your own financial picture. Not only will you need to consider your current expenses, but you’ll have to look down the road a few years, considering how much you’ll need to save for your own retirement and, perhaps, for your child’s education.

Tip: Due to the complexities inherent in providing adequately for several generations in the same family, consider seeking the advice of a financial professional.

Tax benefits for children supporting aging parents

Federal income tax law provides several tax benefits to you if you are supporting your parents financially. If you have a dependent care account at work, you can put pretax dollars into the account that you can use to pay for some costs associated with caring for your dependent parents. You may be able to claim an exemption for your parents as dependents, and you may be entitled to claim a dependent care credit. In addition, you may be able to file your taxes as head of household and deduct medical expenses you paid for your parents. For more information consult your tax advisor.

If you are financially supporting your parent, is he or she entitled to receive Social Security benefits based on your earnings?

If you are providing at least one-half of your parent’s support at the time of your death, and he or she is age 62 or over and is not entitled to a retirement benefit that is equal to or larger than the amount he or she would receive based on your earnings record, then he or she may be entitled to receive a parent’s Social Security benefit equal to 82.5 percent of your primary insurance amount (PIA).

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2015

Old Age

By Pops & Mom (Frank & Joan Ciccarelli)

To live a quality of life at an old age, you must create and stimulate a very special mindset, with considerable change to the normal process of aging.

Here are our rules:

Foremost, you must have an Unshakable Faith and practice that faith: Your prayers should be for strength to handle critical fears, changes, and tragedies, not to avoid them, because that is not possible.

Change Your Expectations: Do not expect your children or grandchildren to call and visit, but imagine the joy when they do. Don’t lay your aches and pains on them. Expect to lose your bags when you travel and if you don’t – ooh la la.

Do Not Hate Anyone: Hate destroys the hater and accomplishes nothing but personal stress.

Give Your Love With No Conditions: Forgive, forgive, forgive.

Today is a Present: When you wake up in the morning, look out the window; if you see the grass you are on the right side, it’s a great day! This is called the present, because it is a present. Our family philosopher, and sister-in-law, Marie Biehl, taught us this.

Do Not Associate With Depressed People: It is contagious. Have a positive attitude, it’s also contagious.

Do not ask old people how they are; instead say, “Nice to see you.”

Embrace Humor: Laugh often and laugh at yourself. Tell dumb jokes to your grandchildren. In our family, we call them Poppy Jokes. Frank has a considerable supply, thanks to Christmas and our granddaughter, Lina Anderson, who documented them for us.

Simplify Your Life: Do not become emotionally involved with any material things; you cannot take them with you. Give clothes you do not wear to charity. Throw away junk! Consider giving some of your jewelry to your children and grandchildren.

Control Your Fears: Concern is common sense. Fears destroy. Live a good quality of life as long as you can.

Accept Who You Are: Live within your means.

Fight Depression: The world has always been in turmoil and always will be. One of my favorite prayers, “God grant me the serenity to accept the things I cannot change, the courage to change the things I can, and the wisdom to know the difference.”

The Most Powerful Force In The World Is Love: The more you give away, the more you receive.

Frank and Joan Ciccarelli are not affiliated with FSC Securities Corp.

Market Month: August 2015

The Markets (as of market close August 31, 2015)

The Markets (as of market close August 31, 2015)

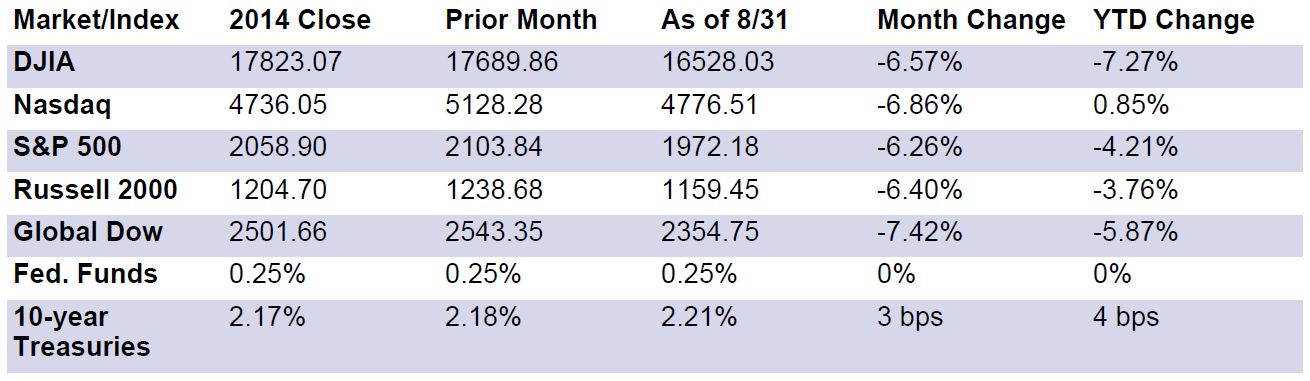

Despite favorable economic news later in the month, the U.S. stock market was unable to recover all of its losses and closed in negative territory compared to July. Key factors in the downturn include fear that China’s economy is weakening, the steep drop in the price of oil, lackluster corporate earnings reports, and the potential for an imminent interest rate hike. Each of the major market indexes listed here dropped between 6% and 7.50% for the month. The Dow, down more than 6.50%, marked its largest percentage decline since May 2010. Year-to-date, only the Nasdaq remained in positive territory–but only barely.

At the close of August, the price of gold (COMEX) was $1,134.90. Crude oil (WTI) prices remained below $50 a barrel, selling at $47.86/barrel by month’s end.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

The Month in Review

- August saw Greece and its creditors formally agree on the terms of an 86 billion euro bailout, which may have allowed the country to remain in the eurozone. Greek Prime Minister Alexis Tsipras, despite campaign promises to write off debt and ease austerity, negotiated the terms of the new deal, which ultimately included stricter austerity measures than had previously existed. With the new debt agreement formalized and his ruling party split, Tsipras resigned, paving the way for an election likely to be held sometime in September. Nevertheless, it would appear that the latest deal has eased economic tensions in Greece, at least for now.

- August also saw China’s economy continue its dramatic slowdown, causing turmoil in stock markets around the globe. When the second-largest economy contracts, other markets feel the heat. The Chinese government has responded by cutting interest rates and lowering bank reserve requirement ratios, allowing for more money to be available to borrow for investment. It is to be determined whether these measures will increase investors’ confidence concerning China’s economic growth, which is presently predicted to be at its slowest pace in over 20 years.

- The second quarter GDP continued to expand, increasing at an annual rate of 3.7% compared to the first quarter’s growth rate of 0.6%. The second quarter showed increased consumer spending, strong residential investment, and an uptick in exports. Also of note is the GDP’s price index, which came in at 2.1%–right at the Fed’s stated policy goal of 2.0% inflation.

- Speaking of the Federal Open Market Committee, it did not meet in August, but provided enough discourse on a potential interest rate increase to draw significant attention. Nevertheless, the August release of the minutes of the committee’s July meeting revealed no clear consensus among committee members as to when rates should be raised.

- August’s U.S. Treasury report for July revealed a budget deficit of $149.2 billion, attributable, in part, to a shifting of payments up to July that had previously been scheduled for August. The total budget deficit through July 2015 was $465.5 billion, or about $5.0 billion over the same ten-month period last year.

- U.S. retail and food services sales advance estimates for July were $446.5 billion, an increase of 0.6% from June, and up 2.4% over July 2014, according to the U.S. Census Bureau. Total sales for the three-month period of May 2015 through July 2015 were up 2.3% compared to the same period in 2014.

- Inflation increased in July, but only by the slightest of margins. The overall Consumer Price Index rose 0.1% in July from a month earlier, according to the Bureau of Labor Statistics. Over the last 12 months, the unadjusted price index for all items increased by 0.2%. However, excluding the volatile food and energy components, the index has gained 1.8% for the 12 months ended July 2015.

- U.S. producers in July received slightly higher prices for their goods and services. The Bureau of Labor Statistics Producer Price Index for goods and services rose a seasonally adjusted 0.2% in July, following an increase of 0.4% in June and 0.5% in May. Even with these moderate price increases, the PPI has generally declined over the past year with overall producer prices down 0.8% compared to the 12-month period ended July 2014.

- Despite lagging a month, the Labor Department’s Job Openings and Labor Turnover Survey (JOLTS) provides useful information on the labor market–particularly job openings, hires, and separations. The number of job openings in June fell slightly to 5.25 million from 5.56 million in May. The decrease in the number of job openings may be due, in part, to an increase in the number of new hires, which rose 0.1% to 3.7%. Over the 12 month period ended June 2015, hires totaled 60.6 million while separations totaled 57.9 million, yielding a net employment gain of 2.7 million.

- Evidencing continuing weakness in goods exports, the U.S. trade deficit for June came in at $43.8 billion–up $2.9 billion from May’s revised total. Compared to May, exports for June dropped by $136 million, while imports increased by $2.8 billion.

- Imports and exports prices continue to feel deflationary pressures. Import prices for goods bought in the United States, but produced abroad fell 0.9% in July, after recording no change in June. Export prices for goods sold abroad but produced domestically were down 0.2% following a 0.3% drop in June, according to the Bureau of Labor Statistics.

- The housing market has remained a consistently performing sector. Compared to June, sales of new homes rose 5.4%, while existing home sales were up 2.0%. In both cases, demand has thinned supply to around five months.

- In other developments, for the week ended August 22, there were 271,000 initial claims for unemployment insurance, and 2,269,000 continuing claims for the week ended August 15, which yielded an insured unemployment rate of 1.7%. Compared to last month, the national average retail regular gasoline price dropped from $2.745 per gallon on July 27, 2015, to $2.637 per gallon on August 24–a fairly significant decrease of $0.108. Overall, consumer confidence rebounded in August, increasing to 101.5 compared to 90.9 in July, according to The Conference Board’s Consumer Confidence Index.

Eye on the Month Ahead

China’s tumbling stock market clearly impacted U.S. stocks in August. Market recovery in September will be tied, at least in part, to whether China can boost its sagging economy. The results of the FOMC meeting in September may finally provide a firm indication of when interest rates will be increased and by how much. It appears that as the third quarter comes to a close, market volatility may continue.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.

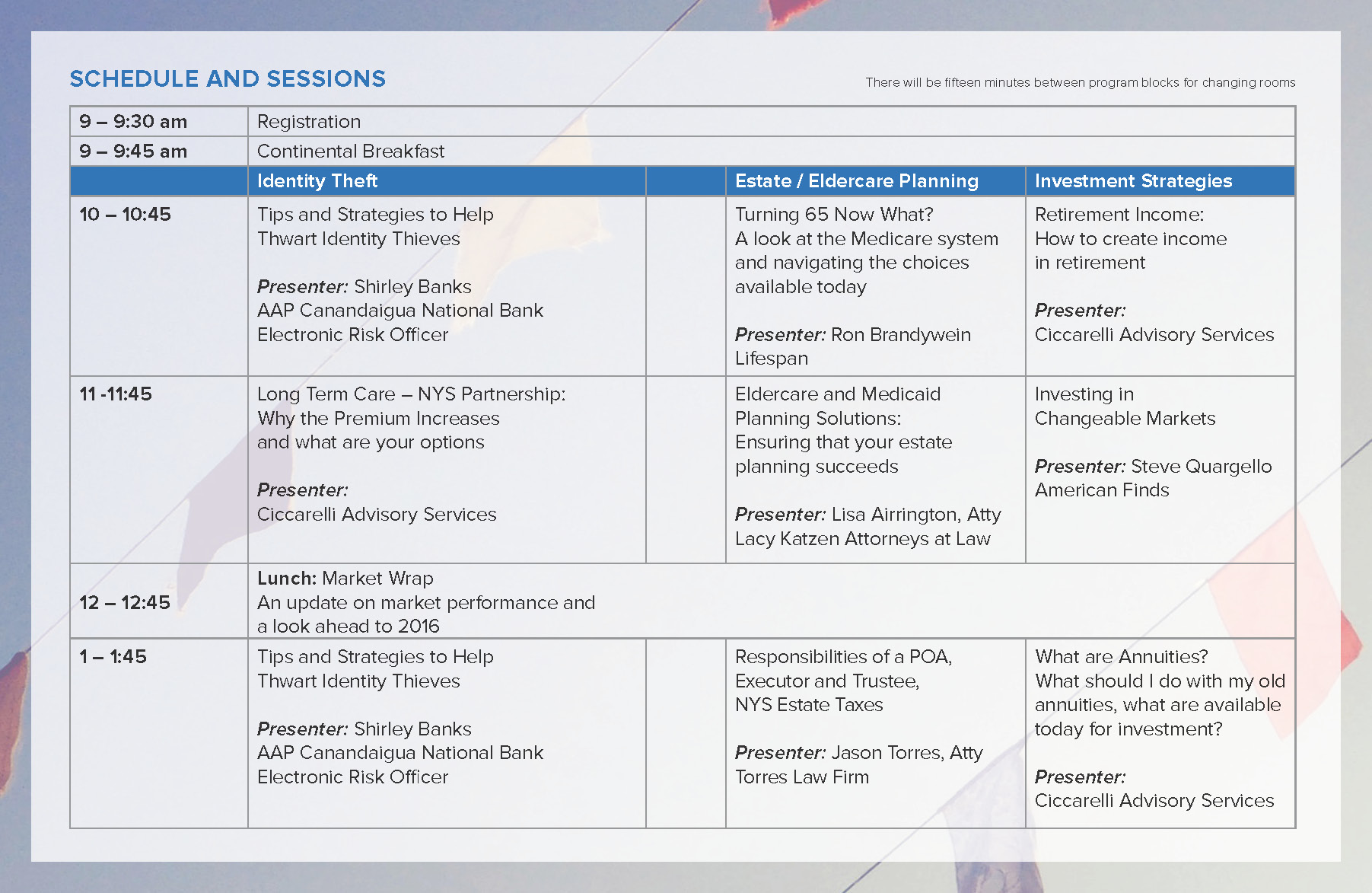

CAS New York: Financial Fair

Please join us “Under the Big Top” for Ciccarelli Advisory Services’ “Financial Fair” on Saturday, October 17th, at the Burgundy Basin Inn in Pittsford, New York!

We have planned a fun and informative day for you! This day will include a number of sessions for you to attend, hosted by guest speakers from our area. Topics include Tips and Strategies to Help Thwart Identity Thieves; Long Term Care Premium Increases and Your Options; Turning 65?: A Look at the Medicare System; Responsibilities of a POA, Executor, and Trustee, and more! Our traditional October Market Wrap session will be offered during lunch.

We welcome you and a guest! Seating is limited so please call our New York office soon at 585.383.0180 to register for the event. If you are bringing a guest please provide their name, address, and phone number when you call to register so that we may send them detailed information.

We look forward to seeing you on the 17th!