CAS News

FULL WEBINAR: Investing in the Next Generation

View Part III of our 2018 CAS Webinar Series below!

Discover how to preserve your family wealth and intangible values for generations to come.

CAS panelist: Kim Ciccarelli Kantor, CFP®, CAP®.

Guest panelists: LaDonna Cody, Esq. (Cody & Linde, PLLC) and memoirist Mary Jane Robinson.

A Florida-Grown Family Legacy

Jill Ciccarelli Rapps, CFP® | èBella Magazine | March 2018

Jill Ciccarelli Rapps, CFP® | èBella Magazine | March 2018

As residents of Southwest Florida, we enjoy a vibrant, growing community of people who hail from all across the country.

Amidst the sea of transplants and snowbirds who have relocated to the Paradise Coast, you will occasionally encounter one of the native Floridians of Collier County – someone who called Naples their home long before the community developed into a tropical haven for retirees and tourists.

Deeply Rooted in Naples

Meet Beatrice, a retired Florida native who has spent her entire life in Southwest Florida. Her family has been cultivating the land as subsistence farmers since the late 1800s!

In the late 1950s, her husband Bob took the risk of expanding the family vegetable farm to an entrepreneurial venture; and they were the first people to commercially farm citrus in Collier County.

As Beatrice and Bob developed their business and started their family during the 1960s, they were always cognizant about saving money consistently and carefully prioritizing their spending needs.

They also knew that the need to diversify their assets and develop multiple streams of income was paramount and could be necessary for the survival of their business. Farming is a risky industry, with the potential for huge fluctuations in income from year to year. One powerful storm could destroy a large swath of the crop, so Beatrice and Bob were always preparing for the worst.

While Bob handled the business decisions and operations of the family farm, Beatrice was hard at work raising their children and instilling the values of hard work, perseverance, love of family and faith within the next generation.

Of course, once their children were old enough to work, Bob introduced them to the challenging yet fulfilling profession of farming.

Bridge to the Next Generation

As Bob continued to succeed in his entrepreneurial pursuits and the family continued to build on their farming tradition throughout the 1980s and 1990s, he and Beatrice were adamant about leaving a lasting legacy – both financial and intangible – that would be preserved for posterity during the new millennium.

Our CAS team began working with Bob and Beatrice in the early 2000s. Although they had a great track record of saving and a clear vision of their goals, they knew very little about investing. Their financial records were totally disorganized, with stacks of papers and statements stashed around their home – making it difficult for them to see their full financial picture and nearly impossible for their children to piece together.

We helped them to open trusts, educational savings and other investment accounts for themselves and their children, organize and simplify their financial documentation, and facilitate consistent communication about money between their family members.

Fortunately, they were able to establish these sound financial practices before a heart-wrenching transition began to unfold.

A few years later, Bob’s health and mental capacity began to decline as he battled Alzheimer’s disease. Beatrice was devastated. Not only was her beloved starting to deteriorate, but she also found herself in the immensely difficult position of managing the farm.

Although she had never managed the business aspect of the family farm, she was forced to step up and make more of the decisions – much to the surprise of their children, who were unaware of their father’s struggle during the early stages of his Alzheimer’s.

Fortunately, Beatrice and Bob had dedicated several years to developing a strong succession plan and system of family communications. In addition to annual family meetings with myself and the CAS team, Beatrice organized monthly meetings with a psychologist to help the family come to terms with the emotional trauma and communication difficulties associated with their father’s dementia.

Without this foundation, Bob’s illness could have seriously jeopardized the family’s financial security – and their ability to carry on the farming legacy.

They continued these meetings for more than five years, with Beatrice and Bob sharing their financial knowledge, farming insight and wisdom with the whole family. If not for their advance planning, clear goals and time commitment, the children may not have been able to build upon their lifetime of progress.

Bob passed away peacefully in 2010 with the peace of mind that their children would continue to serve as good stewards of their land and their wealth. The next generation has certainly stepped up to continue the tradition, with three of their four children working as independent farmers in Collier and Lee counties.

However, Beatrice and her children were not finished with their work.

The Tradition Lives On

Beatrice’s four children have blessed her with 12 grandchildren and two great-grandchildren; and in the same way she instilled her values and knowledge within her children, the whole family is eager to follow her example of pursuing education, hard work, and always maintaining open communication.

Beatrice and her children are providing the grandchildren with the opportunities and support to lead successful lives – regardless of which profession they decide to pursue. They have established and funded 529 education savings plans, Roth IRAs and other investment accounts.

Above all, the whole family is continuing the tradition of family meetings – providing the youngest generation with effective channels of communication, comprehensive financial education and sage guidance, so they may remain good stewards of their legacy.

Note: The case study presented is based on the story of a real CAS client, but the names have been changed to protect anonymity.

Map Out Your Retirement Plan to Prevent Costly Mistakes

Kim Ciccarelli Kantor, CFP®, CAP® | Naples Daily News |

Kim Ciccarelli Kantor, CFP®, CAP® | Naples Daily News |

March 2018

Throughout your lifetime, you worked hard to save for your golden years. As you climbed the ladder of success, you likely accumulated several sources of deferred income to sustain your desired retirement lifestyle.

The most common forms of retirement savings plans are IRAs and defined contribution plans – 401(k)s, 403(b)s, etc.

While these plans are designed for effective retirement savings, often times these assets are scattered across numerous custodians from multiple employers. It may seem tempting to consolidate all your accounts for the sake of convenience.

However, before you merge your retirement accounts, you should map out the full picture of your qualified plans to avoid negating any of your benefits. Simply merging all of these accounts might eliminate the potential for any efficiencies that could be achieved through proper planning for lifetime distributions and legacy considerations.

Flowcharts serve as an especially effective tool for mapping out your full financial picture – empowering you to simplify your financial life in a way that prevents costly fees and accentuates the potential for tax savings.

An organized, well-designed flowchart allows you to delve into the nuts and bolts of each specific IRA or retirement program.

Figure 1. A sample financial planning flowchart for a hypothetical client scenario (Click the image to view full size).

Two of the most critical areas of your retirement plan to address are:

Distributions (lifestyle considerations): Qualified plans require you to take certain distributions once you or your beneficiaries hit a certain age (e.g. RMDs at age 70 ½ and older). Failing to adhere to the particular regulations and timelines associated with each plan can result in costly penalties and fees.

These programs add an additional layer of consideration in comparison to other assets, due to the income tax consequences that result from distributions and the fact that ownership may not transfer during your lifetime. You can make the most of any tax-deferred opportunities by executing a well-thought-out financial plan.

Beneficiaries (legacy considerations): Ensuring you have up-to-date beneficiaries listed that reflect your wishes may be more complex than you think. The most effective means for protecting your IRA and other qualified assets for your heirs is to understand what your custodian agreement will and won’t allow for at the time of death, as well as maintaining a time-stamped, up-to-date beneficiary designation form in your files.

If your beneficiary forms are not in good order, you may forfeit control of where your assets will end up after your death. In contrast, accurate beneficiary forms enhance the potential for your IRAs and other retirement programs to provide steady income for your heirs in the event of your passing.

In comparison to 401(k)s and 403(b)s, IRAs provide you with more flexibility when distributing your assets to beneficiaries: a lump-sum payment, consolidation into a qualified trust, merging or segregating various IRAs, use of disclaimers to pass wealth to contingent beneficiaries, and so on.

While you have discretion in incorporating some of these various approaches during your lifetime, most of these arrangements need to be in place prior to your death – or within a pre-defined period after your death – in order to take effect.

Pensions and deferred compensation plans generally have more restrictive clauses and stipulations for beneficiaries, which can vary widely depending on the administrator of the plan.

Lastly, you should review your entire retirement savings plan every 2-3 years. By doing so, you can address any ambiguity you may feel about your plan and identify new opportunities.

By mapping out your full financial picture and regularly updating your plan to reflect current circumstances, you will be well-positioned to protect and optimize your assets throughout retirement and impart a lasting legacy to future generations.

Unleash the Power of Education – Your Guide to 529 Plans

By Steven T. Merkel, CFP®, ChFC®

In an increasingly competitive and high-skilled job market, a college education is almost a necessity for young people who are jumpstarting their careers. Many employers are demanding a college-educated workforce, and the rise of technology and automation is steadily replacing millions of blue-collar jobs.

Higher education serves as the key that unlocks the door to success and upward mobility, but the opportunities afforded by a college degree come at a cost. College tuition and fees have skyrocketed over the past 40 years, increasing at nearly twice the rate as medical care (see figure 1).

Although public and private university expenses have risen at a comparable rate, the raw increase in costs for private institutions has been far more drastic (tuition and fees at private universities have gone up by more than $19,000 annually – see figure 2).

By steadily saving throughout your lifetime for this investment in your child and grandchildren, you can position them for future success in their career and help to alleviate the burden of student loan debt that could otherwise loom in their future.

Although there are many ways to save, 529 college savings plans are the most popular and effective vehicle for unleashing the power of education in your child or grandchild’s life.

Let’s take a closer look at how 529 plans work, the benefits and limitations of these accounts, and how the new tax law has impacted 529 plans.

Figure 1. The cost of college tuition and fees has increased by more than 1,000% during the 35-year period of 1968-2013 – far outpacing the rate of increase in healthcare, housing and other commodities.

Figure 2. For private universities in the U.S., the average cost of tuition and fees for the 2017-2018 academic year is $34,740. For public colleges and university, tuition and fees in 2017 dollars have more than tripled since 1987.

A 529 college savings plan is a tax-advantaged account that is specifically designed for future education expenses. When you establish a 529 plan, you designate a single beneficiary (typically a child or grandchild) who is the intended recipient of the savings.

The funds in this account may be utilized on behalf of the student at any college, university, trade school, or post-secondary institution that is recognized by the Department of Education (when in doubt, check with the school or institution regarding their eligibility).

As the custodian, you have control over the account. The beneficiary of the plan can be updated at any time, and the funds from one 529 plan may be rolled over to another 529 plan without penalty.

In terms of asset allocation, you have the ability to choose from a range of mutual fund and exchange-traded fund (ETF) portfolios based on your risk tolerance and savings target. Consult with your advisor for more details on which 529 investment strategy is best suited for your needs.

Every state in the U.S. sponsors some form of a 529 savings plan. More than 30 states provide you with tax benefits when you contribute funds to the account (typically in the form of claiming a deduction on your state income taxes).

Most states also exempt you from paying state taxes on the earnings of the 529 plan when you make withdrawals for qualified education expenses. The specifics of these plans can vary significantly state-by-state (see figure 3).

For all 529 plans, you do not pay any federal income taxes on earnings within your account as long as the withdrawals go towards qualified education expenses (see figure 4).

TIP: When making withdrawals from the 529 plan, you should maintain records of all qualified education expenses you have incurred. In the unlikely event that you are audited, the IRS may request documentation.

Figure 3. 529 plans are sponsored at the state level and are subject to different tax benefits. Some states offer a generous deduction on state income taxes, while others offer tax benefits upon withdrawal of funds for qualified education expenses.

Figure 4. If withdrawals from your 529 plan are spent on qualified higher education expenses, the earnings in the account are not subject to federal income tax (and are typically exempt from state income tax as well).

TIP: Under the new tax law, states have been granted the ability to classify tuition and fees for private K-12 schools – up to $10,000 – as qualified education expenses (check your home state’s 529 rules).

529 Plan Rules

As with most tax-advantaged investment accounts, 529 college savings plans are subject to legal restrictions:

Annual gift tax exclusion – Another advantage of 529 plans is the potential to apply contributions towards your gift tax exemption for the year. While leveraging this tax benefit is a great perk, there may be significant gift tax consequences if you contribute more than $15,000 per year individual limit ($30,000 for married couples) to a particular beneficiary.

We encourage you to be mindful of any other expenses you have applied to the gift tax exemption and to adjust your 529 contributions each year so that you fall below the $15,000 GST threshold ($30,000 for married couples).

Exception: Most 529 plans allow you to make a one-time, lump-sum contribution of up to $75,000 ($150,000 for married couples) to the account – as long as you do not gift any additional money to the account beneficiary over the course of the next five years. In essence, you can deposit five years’ worth of contributions at one time instead of contributing $15,000 annually.

Note: Additional contribution limits may apply to your account based on the regulations in place for your state’s plan.

Non-qualified withdrawals – Although you are technically allowed to take withdrawals from the 529 plan for expenses other than the qualified items listed in Figure 4, the earnings portion of these distributions are subject to 10% withdrawal penalty. In short, taking non-qualified withdrawals negate the tax benefits of the account.

Some examples of expenses that are classified as non-qualified include transportation costs, health insurance (even university-sponsored coverage) and student loan repayments.

Changes under the New Tax Law

The Tax Cuts and Jobs Act of 2017 had a direct impact on two key areas of consideration for 529 plans.

First, states have been granted the ability to classify tuition and fees for private and religious K-12 schools – up to $10,000 – as qualified education expenses. Most states have not yet codified this new rule into their respective 529 plans, but the notion of tax-efficient savings for primary education is certainly encouraging for those who have children and grandchildren enrolled in private schools.

Secondly, you now have the ability to roll over funds from a traditional 529 account to a 529 ABLE account. ABLE accounts are specifically designed to enhance quality of life for Americans with disabilities. This new law does not impact your ability to roll over funds from one 529 plan to another 529 plan.

In contrast, the following areas have not been impacted by the tax reform legislation:

- Coverdell Education Savings Accounts

- American Opportunity Tax Credit (AOTC)

- Student Loan Deductions

- Exemption of Tuition Fee Waivers from Taxable Income

Investing in the Next Generation

A 529 plan is an outstanding vehicle for preparing your children and grandchildren to pursue successful careers, as well as mitigating the massive debt burden they could accrue during their collegiate experience.

To further sweeten the pot, 529 plans also carry significant tax advantages for you – serving as an excellent tool for gifting funds to future generations.

Figure 5. The upsides to leveraging 529 plans as an education savings tool are wide-reaching.

Time and time again, our CAS team has witnessed the success of 529 plans in unleashing the power of education for future generations. Contact your advisor to discover more about how we can work together to provide a bright future for posterity while capitalizing on opportunities for tax efficiencies within your investment portfolio.

Sources

Figure 1 – Bureau of Labor Statistics, 2013 Consumer Price Index (CPI)

Figure 2 – College Board, 2017 Annual Survey of Colleges

Figure 3 – Saving for College, 2017: How much is your state’s 529 plan tax deduction really worth?

Liz Joins CAS

Our CAS team is pleased to announce a new addition to our growing, family-focused firm: Liz Koplitz!

Our CAS team is pleased to announce a new addition to our growing, family-focused firm: Liz Koplitz!

As an Operations Specialist at our Naples office, Liz will be instrumental in assisting our advisory team with Trust and Estate Coordination for our clients.

Prior to joining CAS, Liz spent 13 years working with seniors and people with disabilities to help them enhance their quality of life.

Before moving to Naples from New York, she served as the director for worldwide Information Technology and Development organizations at major entertainment and advertising companies. Liz holds a Bachelor’s degree in Organizational Management and IT Management, and she is also a Certified Senior Advisor and a Paralegal.

“Liz brings an abundance of professional experience and legal knowledge to our CAS team,” said Susan Hansen, Director of Administration. “Her distinctive skill set and strong work ethic will further enhance our firm’s ability to deliver trust and estate services to our client families.”

In her free time, Liz enjoys quilting and traveling with her husband. She is an active volunteer at St. John the Evangelist Church as both a second grade teacher and a Eucharistic Minister for the homebound.

Liz Koplitz is not registered with FSC Securities Corporation or Ciccarelli Advisory Services, Inc.

FULL WEBINAR: The Journey of a Lifetime

View Part II of our 2018 CAS Webinar Series below!

Develop a stronger understanding of the legal and financial “nuts and bolts” of estate planning.

CAS panelists: Judy G. Alexander-Wasley, MBA, CFP®, and Samantha Webster.

Guest panelist: Jason P. Torres, Esq. (Torres Law Office, P.C.).

Opportunities Abroad

By Jasen Gilbert, CFP®

By Jasen Gilbert, CFP®

The strong performance of the S&P 500 and the Dow Jones Industrial Average in 2017 was an encouraging sign for investors. While the above-average returns of U.S.-based investments receive a lot of attention in financial news outlets, international equity markets often fly under the radar.

As our team evaluated performance benchmarks both at home and abroad, we observed that the surge in U.S. equity markets mirrored a bullish trend that is happening across the globe. The scorecard is in: International markets – and especially emerging markets – actually outpaced the S&P 500 in 2017 (see figure 1).

The big question: Is the recent boom in international equity markets a fluke, or is it a sign of a greater long-term trend?

Figure 1. A comparison of 2017 market performance for three indices indicates that international markets outperformed U.S. benchmarks. Emerging markets led the way with a 33% return.

The Global Economic Reset

As with U.S. markets, international equity markets are cyclical by nature. After several years of lackluster performance, earnings in foreign markets are beginning to show the promise of recovery and growth (see figure 2a – the red line provides context for average annual returns).

We also observed that – despite modest growth in the U.S. – much of the global economy had been experiencing a recession since 2015, with a marked decline in global GDP growth and annual returns that were far below average (see figure 2b).

Figure 2a. Similar to U.S. markets, international equity valuation is subject to cyclical fluctuations over time.

Figure 2b. The drop in global GDP in 2015-2016 was almost as severe as the Great Recession of 2008-2009.

In addition to the cyclical ebb and flow of equity value, various additional economic and geopolitical factors suggest that a sustained upward trend in international markets could be on the horizon. The underlying fundamentals that drive market growth are strong, which could give way to a phenomenon known as the Global Economic Reset. We see the potential opportunity for pent-up consumer demand – coupled with significant improvements to the balance sheets of global corporations – to be translated into growth.

First, we have monitored the earnings per share growth of the All Countries World Index (excluding U.S. markets) over the past five years. Earnings have finally begun to recover after several years of negative growth, and the projections for 2018 are quite optimistic by comparison (see Figure 3). When coupled with the corresponding trends in GDP growth shown in Figure 2b, the outlook for international investing appears to be promising.

Figure 3.

By expanding our vantage point to examine the past 35 years, we observe that annual GDP growth from 1981-2008 (the “pre-crisis” time period) averaged 7%. In comparison, annual GDP growth from 2008-2016 has been about 5% on average. We anticipate that this metric may move closer to the 7% equilibrium over the long term – indicating that several years of above-average returns may arise within the near future.

Figure 4. The post-recession GDP growth of nations outside the U.S. has lagged behind the average annual growth rate of 7% from 1981-2008.

In addition to the economic indicators shown thus far, geopolitical factors have also created a scenario that could be ripe for strong international investment performance. When citizens are dissatisfied with the state of their nation’s economy – particularly in the case of a prolonged recession – democratic elections tend to favor candidates that propose pro-growth policies.

Alternatively, the current government leadership that is seeking re-election will make an effort to respond to the pleas of their business owners and workers so they can retain power. The results of upcoming elections and other political developments across the EU and Asia could have a profound impact on the growth outlook of the global economy.

Last by not least: Global corporations have made significant strides in improving their balance sheets. Whereas the ACWI debt-to-equity ratio for corporations ballooned to more than 32% in the early 2000s, a massive amount of debt has been paid off in the lead-up to the Global Economic Reset. The current debt-to-equity ratio is now about 23% – meaning that global corporations have much more capital to invest in the production of goods, delivery of services and labor (see figure 5).

Figure 5. Global corporations have made significant progress in reducing the amount of debt on their balance sheets, opening the door to more capital investment.

The synergy of these economic and political factors have created a “perfect storm” with the potential for strong international investment performance over the next few years. As a result of this trend, you could be well-served to include non-U.S. investments as a component of your diversified portfolio.

Balance in All Things

In addition to building a diversified investment portfolio for you, our CAS team works with our custodian partners to ensure that your international holdings are being rebalanced based on market trends and outlook in the global sector. Rebalancing involves a regular evaluation of how to best represent different equity classes in your portfolio.

In our evaluation, we consider a wide range of factors – two of which are national/regional performance trends and performance by industry. To illustrate this, let’s take a closer look at emerging markets in particular.

In figure 6, we observe that the international investing landscape has changed drastically since the late 1980s. As an example, Malaysia represented a large cross-section of the emerging markets universe in 1988; today, Malaysia is no longer a major player. China, Korea and Taiwan have emerged as the leading emerging markets, whereas many of the Latin American economies have fallen from prevalence.

Clearly, international markets are subject to the same steady, constant changes as U.S. markets, and the long-term effect of these fluctuations can lead to dramatic changes over the course of 30 years.

Figure 6. The emerging markets landscape has shifted dramatically over the past three decades, with Southeast Asia gaining prominence and Latin America/Malaysia receding.

The microcosm of emerging markets provides us with insights that can be applied broadly to the big picture of your financial plan. The need for diversification and regular rebalancing cannot be understated. By recognizing change and emerging opportunities over time and incorporating an appropriate balance of international markets within your portfolio, our team will work with you to capitalize on promising investing opportunities at home and abroad.

Contact your advisor to learn more about how CAS leverages international investments as part of your comprehensive financial plan.

FULL WEBINAR: Don’t Take a Chance on Your Retirement

View Part I of our 2018 CAS Webinar Series below!

Discover how to avoid common financial planning mistakes,

prepare for rising health care costs, and live a purposeful life during retirement.

CAS panelists: Jill Ciccarelli Rapps, CFP®, and Lynn A. Ferraina.

Guest panelists: Lisa Gruenloh (Blue Zones Project) and Annalee Kruger (Care Right, Inc.).

Planning For Market Uncertainty in Retirement

For investors, 2017 proved to be a rewarding year. The S&P 500 index rose by more than 20 percent, and the Dow Jones Industrial Average surged past both the 20,000 and 25,000 thresholds in a single year.

The trend of strong market returns has continued throughout January. The bull market that began in March 2009 continues to push forward, despite ongoing speculation from financial professionals that equity markets could be overvalued.

The real question is: How long will the market continue to rise and when will equity markets reach their peak? No one can provide a definitive answer, as market forces and fluctuations in value are largely beyond our control.

Cycling through History

Although historical performance is limited in its predictive ability, past performance does provide us with significant context for understanding big-picture trends. Recent history illustrates that a strong, sustained bull market often precedes a correction bear market, as inflated equity markets return to a more stable valuation and investor confidence begins to wane.

The decade-long bull market of the 1990s began to reverse course in 2000 in the wake of the “dot-com” bubble burst and the emergence of several major accounting scandals (in particular, Enron and Arthur Andersen). The once-burgeoning technology industry was especially hard-hit, with the NASDAQ losing 39% of value in 2000 (followed by losses of 21% and 31% in 2001 and 2002, respectively). The Dow also decreased by more than 27 percent during this three-year window.

Equity markets began to bounce back in late 2002, ushering in a new bull market that was sustained through late 2007. At this point, the sub-prime mortgage crisis (among other factors) led to the most drastic correction market since the Great Depression. All three major indices lost more than 50% of their value in 17 months (between October 2007 and March 2009).

Although we have knowledge of market cycles, we cannot say with certainty what the future holds. For this reason, it is critical for you to be prepared for the possibility of a bear market – especially if you are approaching retirement or are currently living on retirement investment assets today.

Figure 1. Performance of the S&P 500 index, Jan 1998 through Jan 2018.

Navigate Uncertainty with Preparation and Prudence

Above all, the most effective way to prepare for uncertainty in equity markets is to plan well in advance for your needs and priorities during retirement. To develop the “stepping stones” for future retirement success, we recommend that clients and their family members begin to work through the planning process with an advisor at least 8-10 years prior to their desired retirement date.

In our experience, the most effective retirement plans share two main characteristics: (1) a conservative draw rate and (2) a realistic, long-term approach to budgeting. With these provisions in place, you can build a strong, sustainable foundation for your financial success throughout retirement.

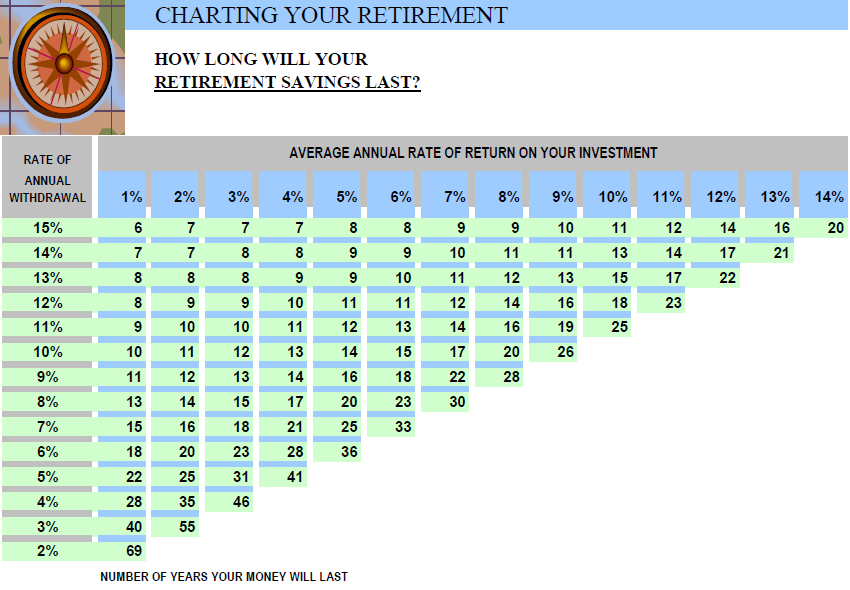

1. Be conservative when selecting your withdrawal rate. After working hard and accumulating assets throughout your lifetime, you will finally enter the asset distribution phase of life during retirement. As you begin to take distributions from your IRAs, 401(k)s and other investment accounts, you should exercise prudence when selecting your rate of withdrawal.

Your ideal withdrawal rate will vary based on your desired lifestyle (expenses) and your available asset base (income). That being said, we have generally seen great long-term success with a conservative draw rate of 4-5 percent.

When you begin to exceed 5 percent – especially once you enter the 7-9 percent range – it is likely that your withdrawal rate is not sustainable for the duration of your retirement. A high withdrawal rate – especially early in retirement – could cause your asset base to deteriorate at an alarming pace. As a result, you may find it difficult to meet expenses in your later years (especially with rising health care costs and uncertain market conditions).

Figure 2. Conservative draw rates can extend the lifespan of your retirement savings, regardless of fluctuations in the market.

2. Be realistic when developing your retirement budget. A detailed and well-thought-out budget for your retirement lifestyle is the key to determining your ideal withdrawal rate. Once you appreciate the full extent of your short-term spending priorities and long-term expenses throughout retirement, you can compare that figure to your asset base to determine the best withdrawal rate for your situation.

Apart from selecting a withdrawal rate that is too high, the biggest mistake you can make in retirement is to underestimate your expenses up front. When a retiree fails to plan for the inevitable costs that loom in their future, he or she will often take additional withdrawals beyond their predetermined distribution – which, in turn, threatens the long-term viability of their retirement savings.

Because budgeting is so crucial for promoting a sustainable retirement lifestyle, it is in your best interest to regularly consult with a financial expert to prevent overlooking key considerations and making costly mistakes.

As the current bull market enters its ninth year, we must not be lulled into a sense of false optimism or complacency. Our knowledge of market trends suggests that a bear market looms on the horizon; it is a matter of when, not if. Although the constant flux of market forces is beyond our control, you do have control over your expense budgeting and retirement income distributions.

While the specifics of your plan are dependent on your personal circumstances, the correct course of action when planning for your retirement lifestyle is preparation and prudence. With adequate foresight and consistent guidance from your advisory team, you can feel confident that your draw rates and spending habits will be sustainable throughout your golden years – regardless of the uncertainty that exists in the market.

Claim Your YES in 2018!

Jill Ciccarelli Rapps | èBella Magazine | January 2018

As we ring in the New Year, many of us reflect on our long list of new or old intentions and goals for the upcoming year. What if you were to throw away that list and consider just one thing that would make you the happiest – something that will really give you a YES year!

What is stopping you from making 2018 your best year yet? As you’ve probably seen throughout your own life, even the best-laid plans are bound to encounter numerous roadblocks. In particular, we’ve observed three major trends that hinder a person’s ability to achieve their YES:

Fear. Fear is a natural human response that tends to arise when we feel that we don’t have control; that we may fail; that we may be letting others down by doing something for ourselves.

The Fix: Accept that these feelings you have are completely normal, but that your fear must never define you. Make a conscious effort to re-focus your thoughts towards the feelings of accomplishment and joy you will experience when you persevere to claim your YES.

Time. Time is perhaps our scarcest resource. Our inclination is to organize all of our time around the dreaded to-do list or schedule. While this approach is effective in managing many tasks, we often feel as though our highly structured lives result in major constraints on our freedom, on our ability to fully experience the limited time we have.

The Fix: Every week, set aside some “me” time to claim your YES. Don’t look at your watch or your to-do list, disconnect from your phone, and hone in on the commitment you made to yourself. Breathe. Relax. Then, with a renewed dedication to that one underlying goal for 2018, consider how you can best structure your time going forward to ensure that your YES will come to fruition.

Money. Your money is a means to an end; the end is your happiness and fulfillment. Saving money is an important virtue, but many of us feel reluctant to spend money: some feel the need to hoard their assets, others may feel averse to “wasting” money on extravagant experiences or luxury items.

The Fix: Whereas saving is the key to long-term financial wellness, spending may be the key to claiming your YES. When you synchronize your spending with your deepest aspirations, your money can begin to achieve a grander purpose – and the true power of your financial plan becomes evident!

So how do you overcome these obstacles to claim your YES? Let’s take a look at Linda.

How Linda Claimed her YES

Linda had a difficult year in 2017. After turning 72 in February, she lost her husband of 46 years, John, in March after a long battle with a rare heart condition.

Linda had always loved traveling throughout Europe and was especially fond of her annual two-week excursion to Italy with John. However, since he passed away, she hasn’t felt comfortable traveling alone. In addition, her only son and her three teenaged grandchildren live in California and rarely have the opportunity to visit Southwest Florida. Linda felt isolated.

At her annual financial review, Linda shared her predicament with her advisor, who shared a curious idea to overcome her loneliness:

“Have you ever considered taking your grandchildren one at a time on the trip of their lifetime?” the advisor asked. “What if, after each of your grandchildren graduates from high school, you let them select any destination in Europe they would like to travel? You will have quality time with them, instill your passion for travel, and give them new perspectives and unforgettable experiences that will be meaningful to them throughout their lifetimes.”

Linda was ecstatic about the idea at first and went home feeling invigorated about her possible future travels. However, throughout the next week, she began to worry about money. Could she really afford three separate vacations in five years? How would these travel excursions impact her grandchildren’s inheritance? Would she need to make significant sacrifices in order to make it happen?

Wait a minute! Linda thought. I can either give them my money when I die, or I can use my money with them while I live. I have a perfect opportunity to enjoy Europe again with three very special travel partners. I can do it – I will do it!

That positive self-talk – overcoming the obstacles – was the turning point for Linda. In summer 2018, Linda will be traversing the mountains of Switzerland with her eldest grandson, and she is eager to explore new territory in 2019 as she and her granddaughter plan their trip to Czechia.

With Linda’s success story in mind, circle back to that one goal or action that will make 2018 your best year yet. Ponder how energized and happy you will feel when you fulfill that promise to yourself, how you will take the obstacles in stride, and how you will go forth with confidence and strength to make it happen!