Financial Education

Our advisors share their insights and experience on a wide range of financial topics.

Will Our Children Be Better Off in Retirement than We Are?

By Raymond F. Ciccarelli

By Raymond F. Ciccarelli

When we take a look at the landscape of our work histories over the years, we find that many working people in the 60s, 70s and 80s have worked for one company for most of their lives.

In many cases, they could count on a defined-benefit plan, a pension plan that provided a guaranteed income stream, or at least a lump-sum payment upon retirement. At that time, there was no concern about the solvency of Social Security as a dependable income source in retirement.

When we compare that situation to the current financial circumstances facing our children and grandchildren, what is the likelihood that the younger generations will work for the same company for 25 or 30 years? Almost zero!

If Social Security still exists, the benefits will most likely be reduced and insufficient for covering retirement income needs. The likelihood of having a defined-benefit plan through an employer is virtually non-existent today.

As parents and grandparents, it is vital for us to spend time with our children to help them recognize the value of saving from an early age. If they are not disciplined in making consistent contributions to their retirement savings plans, then their chances of achieving financial security in retirement are quite low.

Given the shifting retirement landscape, the need to make the most of 401(k) plans and other retirement accounts has never been more critical. While most younger people have access to a 401(k) plan through their employer, many providers spend little to no time explaining the benefits of the plan, how to participate in the plan, and how and where to invest the contributions.

When our children begin their careers, the top priority should be ensuring that they are fully participating in the company’s retirement plan (if one is offered).

If they do have the ability to make contributions to a 401(k) plan, help them to see the benefit of consistently saving at least 5% of their income into the program and investing their asset in a growth-oriented financial strategy. We suggest setting aside 5% of their annual income, as that amount typically will not significantly hamper their cash flow.

Since participating in a 401(k) plan will result in an automatic payroll deduction, your children and grandchildren will not feel as though they are missing out on money as they progress in their career. Additionally, some employers offer a 401(k) match based on a certain percentage of income (typically 2-5%). In these instances, someone who contributes to their 401(k) each pay period will effectively be earning more money than their colleagues who do not participate.

A good goal for progressively building a strong asset base for retirement is to increase contribution rates by 1% each year (especially if their income steadily increases throughout their career).

Retirement savings plans come in a variety of configurations depending on the type of employer. While most private businesses have embraced the traditional 401(k) plan as the gold standard for retirement savings, some public-sector jobs – especially education – offer different programs.

For example, teachers or administrators who are employed by the state may participate in a tax-sheltered annuity. In some cases, employees of colleges and universities have access to a 403(b) retirement plan.

Regardless of the specific details of these employer-sponsored plans, the key to building a comfortable nest egg for retirement is contributing early and frequently. Your goal as a parent and grandparent should be to work with the next generation to understand the benefits that are available to them and get them started in a steady accumulation account.

If no retirement savings plans are offered through their place of employment, you need to focus on the value of contributing to either a Roth IRA or traditional IRA account. Again, the most imperative steps to promote your children and grandchildren’s future success is to help establish the account for them and have them transfer funds from their checking account to the IRA each month. Our team of advisors is more than happy to evaluate which type of IRA would be most beneficial for them.

If we fail to teach our children and grandchildren the long-term benefits of putting away dollars on a regular basis, then they are unlikely to attain the financial freedom that can result from properly designing and executing a strategic retirement plan.

On the flip side, a well-thought-out savings plan that is implemented throughout the duration of their careers will position them to be even better off in retirement than we are.

Baby Boomers are Redefining Retirement

By Lynn A. Ferraina

By Lynn A. Ferraina

How do you picture your retirement? Whether it’s more time with the grandkids, downsizing into a new home or buying into a continuing-care retirement community, or simply being free from debt and the demands of a full-time job, we all have our own unique vision of how to make the most of our golden years.

That being said, a dream without a plan is simply a wish; and the need for retirement planning has never been more critical than it is today.

The reality of retirement has undergone quite a radical transformation in recent times. As more and more Baby Boomers approach retirement age, they are finding that their circumstances are considerably different than those of their parents.

The tradition of lifelong commitment to one employer and earning your “gold watch retirement” is no longer the norm. Whereas long-time employees counted on a pension plan for the duration of their lifetime, today’s retirees depend on other sources of income. Concerns over the long-term viability of Medicare and Social Security have grown, and most retirees today understand that these services alone will not meet their needs in retirement.

Above all, Baby Boomers tend to pursue healthier, more active lifestyles and have access to more advanced medical technology than previous generations – empowering them to live longer than any other cohort in history.

Each of these factors requires careful consideration and detailed planning as you approach your retirement. With proper foresight and dedication, many of our clients have successfully adapted to the evolving landscape and are pursuing their dream retirement lifestyle on their own terms.

Here are three key areas where Baby Boomers are redefining retirement:

Baby Boomers are living longer than previous generations. While the U.S. population has doubled since 1950, the number of Americans aged 65 or older has quadrupled. The Census Bureau reported that 20% of U.S. residents are projected to be senior citizens by 2030, compared to 13% in 2010.

The time span for your retirement could be more than 20 years longer than that of your parents! Believe it or not, some people will spend as much time in retirement as they did in their careers. A 2018 report by Social Security Administration forecasts that 25% of Americans who reach age 65 will live until age 90.

Living longer is a beautiful thing, but it also presents new challenges. Most strikingly, Baby Boomers will have to stretch their personal assets much further to sustain their desired lifestyle. For this reason, creating and monitoring a detailed budget is essential.

Understanding the distinction between growth-oriented and income-generating investment strategies is also a key to successful cash flow planning during your retirement years.

Given the extended time horizon of retirement – and the desire for an active lifestyle – a growing number of Baby Boomers are taking up part-time jobs. Many retirees have found that a part-time job is a welcome addition to their retirement.

Whether out of boredom or necessity, millions of Baby Boomers are keeping their minds occupied, pursuing new fields that they find interesting and rewarding, and generating some extra income to preserve their financial stability.

Most Baby Boomers are no longer counting on pension plans, which have gradually become a thing of the past. Most private-sector retirees (and those who are self-employed) will not receive a monthly pension check to cover their living expenses; instead, they will rely on 401(k)s, IRAs and other personal assets they have amassed.

After employers started to move away from traditional pension plans in the 1970s, many employees have been diligent in contributing to other accounts; however, many workers have not contributed enough. Those who neglected to save adequate funds could run into dire financial straits during retirement. Seeking professional advice many years prior to retirement – during the accumulation phase – has become increasingly vital.

The restructuring of retirement income also requires a more advanced understanding of tax laws. As employees contributed to a traditional IRA or 401(k) plans, they received a deduction in taxable income; but when they start to withdraw income from retirement plans, the withdrawn amount becomes taxable as ordinary income for that year.

Planning for the impact of taxation on your nest egg has never been more integral to your financial success.

Retirees are grappling with the uncertain future of Medicare and Social Security, and many are realizing that these programs are not sufficient for a comfortable retirement.

The number one mistake we see with retired clients is failing to prepare for the skyrocketing cost of health care. Even though Medicare and Medicare supplements provide superior coverage, a Boston College study found that the average American household spends $197,000 in out-of-pocket health care costs during their retirement (not including services covered by Medicare or nursing home care).

The solvency of Medicare has also come into question over the past decade. The 2018 Medicare Trustees report indicates that the Medicare Part A trust fund is projected to be depleted by 2026. The shortfall could be corrected by a 0.82% increase in combined Medicare payroll taxes or an immediate 17% reduction in Medicare expenses – neither of which seem likely to occur in the foreseeable future.

To make matters worse, the long-term-care insurance market is not what it once was. Premiums have become unaffordable for many retired individuals and couples.

As a result, more seniors are realizing they may have to self-insure for long-term care costs with their own assets or buy into a continuing-care retirement community (where you are able to “lock in” your health care costs by purchasing an all-inclusive bundle that lasts a lifetime).

Social Security was designed to be supplemental income for retirement; however, many Americans are questioning whether this support system will remain effective and sustainable in the future.

The $2.89 trillion Social Security trust fund is being depleted for the first time since 1982, which is especially problematic when considering the rapidly increasing number of retired people. Today, there are 2.8 workers for every 1 Social Security beneficiary; the Social Security Trustees Report projects that there will be 2.2 workers for every beneficiary by 2035.

In addition, Social Security cost-of-living adjustments (COLAs) have failed to keep up with the true cost of living. According to The Senior Citizens League, Social Security benefits have lost 34% of their buying power between 2000 and 2018. During that timeframe, COLAs increased the average Social Security benefit by 46% (from $816 to $1,193), while average expenditures for retirees increased by 96%.

Long story short: it is a mistake to rely only on Medicare and Social Security to meet your health care and cash flow needs during retirement. Although the benefits will not dry up overnight, the long-term viability of the programs is questionable. Thus, creating a savings initiative that exclusively addresses your long-term care costs may be the best option for reducing risk and uncertainty in your future.

The changing paradigm of retirement is not only impacting Baby Boomers; it is also redefining how to plan for retirement and live life to the fullest for all generations – including Gen X and Millennials.

Creating the retirement of your dreams requires proper advance planning. That being said, it is never too late to seek advice and develop an organized, simplified plan for your future. We always welcome the opportunity to meet you and your family to help you through the process!

Preserving Your Family Legacy – Part I

How to Properly Designate and Update Beneficiaries

By Kay Anderson, CFP®

Having an up-to-date will and legal documents is an essential part of your legacy plan; however, these documents alone may not be enough to ensure that your assets are transferred to future generations in a manner that is consistent with your wishes.

Whenever you open a new account, you should ask yourself, “What will happen to this account if I pass away?”. In some cases, you may find the default option to be surprising.

Name that Beneficiary!

For retirement accounts, insurance policies and annuities, you always have the ability to specifically designate who will receive these assets in the event of your death.

Most custodians allow you to elect multiple primary and contingent beneficiaries, and you can often select what percentage of the assets are to be passed on to each beneficiary. These elections will override the provisions of your will.

Failing to appoint beneficiaries can be a costly mistake. If no beneficiaries are named, the custodian that houses your assets will follow their default rules to determine how your money is handled upon your death. Some will default to a surviving spouse, while others may follow the instructions of the account holder’s will and estate plan or simply name your estate as beneficiary. Why leave it up to a custodian to determine how to handle your legacy?

Naming a single beneficiary on an account could also lead to unwelcome consequences. For instance, if your account lists only your spouse as the primary beneficiary but has no contingents, what would happen if you both were to die in an accident? The process will depend on how the death occurs and who is deemed to pass first.

As an example, if your spouse is deemed to die after you, then the assets will flow according to their will and probate. In cases where you are in a first marriage and both spouses have same beneficiary wishes, this could work out fine; but what if that is not the case? It is important to consider your family dynamics and to ensure that your legacy wishes are specifically detailed.

Once you have established an account and listed your desired beneficiaries, you must not “set it and forget it.” Rather, you should review your elections on all accounts every 2-3 years and immediately following any significant life event, whether it be family-related or financial.

Accounts with up-to-date beneficiary designations can also provide you with an added benefit: simplifying the probate process. Although probate is a necessary component of estate settlement, it can be an expensive and time-intensive ordeal.

By selecting beneficiaries for your accounts in advance, these assets can bypass the probate process. In contrast, any holdings that are settled through your will (or lack a specific designation) are subject to the probate process.

Two other key factors to contemplate for your financial accounts are (1) establishing POD/TOD provisions and (2) understanding the difference between per capita and per stirpes beneficiaries.

A payable-on-death (POD) designation can be added to a bank account or CD to allow the money in that account to be inherited by a beneficiary immediately upon your death. The appointed person does not have control over these assets during your lifetime.

Similar to a POD, a transfer-on-death (TOD) designation serves the same purpose for an individually owned brokerage account or other investment that you wish to pass directly to a beneficiary. In both cases, taking this simple step will allow the accounts to bypass probate court.

Finally, when designating beneficiaries, you can stipulate either per capita or per stirpes as the path of succession for your assets. The distinction here is essential.

Per capita means that equal weighting is given to each surviving beneficiary. For example, if you have three children and one predeceases, then the inheritance that was granted to the deceased beneficiary will be evenly split between your two surviving children. If your deceased child had any descendants, they would not receive a share of the inheritance.

Per stirpes continues your inheritance along the family line. In the previous example where you have three children and one predeceases, the deceased beneficiary’s portion – 1/3 of the total inheritance – would be passed along and evenly split among that deceased child’s descendants (i.e. not split between your two surviving children).

Family Dynamics – Questions to Ponder

Every family situation is unique and often involves constant change – divorce/second marriages, new children and grandchildren, and much more.

For this reason, it is critical to regularly review and update your accounts to ensure that your vision for the succession of your assets is executed as desired.

Here is a list of considerations that can easily be overlooked as your family dynamics shift over time:

Spousal Considerations

If you are divorced, is your ex-spouse still listed as your primary beneficiary?

If your spouse is deceased, have you removed them as primary beneficiary? Have you designated a contingent beneficiary?

Considerations for Stepchildren and Adopted Children

Are you in a second marriage and have children from your prior marriage and/or new marriage?

Do you have stepchildren or adopted children?

What is your intent for the assets – keeping money within the blood line or including other family members?

Note: The legal nature of your relationship with a child/grandchild will drive how a beneficiary designation is viewed. Stating “my children, per stirpes” as your account beneficiaries, for example, would not include stepchildren unless this provision is formally adopted.

Additional Considerations

Do you have a child who is under 18, has a learning disability or other mental disorder, struggles with drug or alcohol issues, or simply cannot handle money?

What will they do with an influx of cash/assets without restrictions or guidance?

Have you considered establishing a special needs trust or guardianship to accommodate these circumstances?

Above all, it is essential to have proper documentation for all of your financial accounts and beneficiary designations. We recommend maintaining and organizing all of this information within one easy-to-access file, along with verified date stamps.

Our CAS team can facilitate this process on your behalf – compiling your account and beneficiary listings for your annual review and suggesting updates when appropriate. If it’s been a while since you have reviewed your accounts, we always welcome the opportunity to discuss your legacy plan.

Together, we can ensure that your beneficiary designations align with your current family circumstances and your vision for the future – empowering you to preserve wealth for generations to come.

The Royal Treatment?

By Carol Girvin

This weekend, the world will direct its collective gaze upon the United Kingdom to observe the joyous wedding of Prince Harry of Wales and Meghan Markle.

Notably, their wedding will mark the first time in British history that a U.S. citizen has married into the royal family.

Amidst the fanfare of their highly anticipated union, Ms. Markle will likely face some tax-related hassles behind the scenes. A recent article in the Wall Street Journal outlined some of the challenges that the princess-to-be could encounter as a result of her trans-Atlantic matrimony. Ms. Markel is not alone; many Americans who marry foreign nationals could experience a lifetime of harassment from the U.S. Internal Revenue Service.

The greatest impact on Ms. Markel will be the need to constantly report her financial activities to U.S. authorities. For example, suppose that Ms. Markel’s new grandmother-in-law, the Queen of England, lends her a tiara or diamond bracelet. She would be obligated to report this exchange to the IRS.

In addition, if she shares free rent for the residence at Kensington Palace, its value is reportable to the IRS. And if Harry and Meghan have a joint bank account or credit card with a balance that exceeds $10,000, the account has to be reported.

The penalties for improperly reporting her information to the IRS are severe, with the potential to consume as much as half of her account values.

That being said, it is possible that none of these regulations will significantly increase Ms. Markel’s tax bill. Assets that are held in trusts can be taxed at a rate of 37%, and many of the British royal family’s assets are organized in this fashion.

Photo Credit – The Wall Street Journal

The WSJ article also dives deeper into other odd provisions within the convoluted tangle of international financial requirements. For example, if a U.S. citizen works in Australia, Australian law requires that a person have a retirement account; however, U.S. tax law treats these accounts the same as offshore trusts, with very complex reporting rules.

Of course, Ms. Markle could simply opt out of U.S. citizenship, which thousands have done over the years. However, she would not receive U.K. citizenship for a potentially significant period of time (due to a long waiting period in England); so it appears she will have to adhere to U.S. tax rules for the foreseeable future.

As you watch the coverage of the wedding, keep your eyes peeled for the guys in plain dark suits and glasses. There’s a good chance they are the IRS agents – the unwelcome guests at the happy couples’ special day.

The Business of Family – Your Guide to Legacy Planning

By Kim Ciccarelli Kantor, CFP®, CAP®

By Kim Ciccarelli Kantor, CFP®, CAP®

When we hear the term estate planning, most people consider the “nuts and bolts” of your plan:

Estate documents (wills, powers of attorney, health care proxies);

Financial vehicles that can support your family and your community for years to come (various types of trusts, donor-advised funds, etc.).

While the tangible aspects of your estate plan are absolutely necessary to your family’s long-term financial success, your legacy plan encompasses more than just your investments and assets. When properly prepared and executed, the plan should serve as a blueprint to prepare your children and grandchildren to become good stewards of your wealth.

Unfortunately, many personal fortunes have been squandered more quickly than they were amassed as a result of poor family communication and inadequate planning.

All too often, the intangible component of legacy planning is overlooked and future generations are left without a guiding framework for how to best sustain and enhance family wealth.

Key Considerations for Family Founders

As the family matriarch or patriarch, a well-thought-out legacy plan affords you with a unique opportunity to guide your children and grandchildren in achieving long-term personal and financial success.

At the very core of the legacy planning process should be your family’s mission and deeply held values. A mission or values statement serves as a succinct, powerful means for articulating financial priorities and creating mutual understanding about how to align your money with your principles and purpose.

In order for your legacy plan to achieve its full potential, you must consistently communicate your family mission and story – including the core values and key lessons that were instrumental during your lifelong journey of building and sustaining your wealth.

Perhaps the most important consideration as the family patriarch/matriarch is how to prepare your children and grandchildren to inherit wealth and embrace a healthy perspective about money.

In our experience, families realize the greatest benefit when they move beyond a simple explanation what is given to heirs. Rather, the heart of your family discussions should focus on (1) why the assets are being passed forward and (2) your intentions for how the wealth should be utilized.

If you have neglected to lay out clear expectations during your lifetime, your children and grandchildren could misinterpret your wishes and use their inheritance in a manner that is not consistent with your family mission and values statement.

While some of your descendants may indeed view their inheritance as a legacy to be preserved and passed on to future generations, others may see the windfall as a means for immediate gratification and short-term indulgence.

With these considerations in mind, the question remains: As the family founder, what is the most effective way to convey my wishes for how my legacy plan ought to be carried out?

Based on our extensive work with client families, we have identified five vital components of most successful plans – known as the “capital” in the business of family. By fostering strong development in each of these crucial areas, your family members will gain clarity and insight into your distinctive vision for the future.

Figure 1. The five types of capital serve as the building blocks of the business of family, with each component playing a critical role in constructing a legacy for future generations.

Financial capital consists of the tangible assets you have accumulated during your lifetime – investments, business interests and possessions – as well as the future growth potential of these assets.

Sustaining family capital is best accomplished when you have clear, realistic expectations and a strategic approach to long-term growth. Through the family financial and legacy plan, your children and grandchildren should gain a mechanism for investing appropriately, conserving values and appreciating the end use for the wealth.

Human capital is expressed through the personal character development of individual family members. In order to serve as good stewards of your wealth, your descendants must value responsibility and productivity, as well as a desire to continuously learn and expand their skill set.

To successfully cultivate these traits, you must talk about the meaning of money as a family unit – sharing your values about spending, saving, sharing and investing. Assisting your children and grandchildren in developing these traits will empower them to pursue worthwhile ambitions during their life – in essence, utilizing their human capital in an impactful way.

Family capital involves the process of creating and reinforcing mutual understanding so that you can strengthen your existing familial ties into positive, productive relationships. Families learn to respect and trust each other through the open exchange of ideas, by mitigating past misunderstandings, and by listening to and learning from each other.

Mastering the ability to compromise is necessary, as well as striving to achieve a win/win outcome for all parties involved.

Societal capital manifests through community action and your family’s involvement in service and philanthropy. To be effective, societal capital must be expressed both in individual and collective family choices.

Depending on your circumstances, family foundations, donor-advised funds and charitable trusts are useful vehicles for carrying out your philanthropic goals (as may be reflected in your family mission statement).

Structural capital serves as the foundation required to hold the legacy plan together, to bridge the gap between generations in a concrete way.

The framework of your legacy plan – the business of family – is demonstrated through the development of the family mission and value statement, regular communication between family members, and decision-making procedures that promote accountability and boundaries for managing your money.

Successful family governance is best achieved through clearly written, living agreements among family members, with an eye towards perpetuating the family’s mission and values for posterity.

Figure 2. By gathering multiple generations for a family meeting, you can promote open communication between all parties and reinforce the desired mission and goals of your legacy plan.

By facilitating intergenerational communication about your family mission, values and purpose of the plan, our CAS team aims to help you build mutual understanding and cohesiveness among family members and prepare your heirs to leverage all five types of capital to their fullest potential – today, tomorrow, and for generations to come.

Discover how our team of experienced advisors go above and beyond the traditional, tangible financial planning role to simplify the transfer of your intangible wealth and values to your children and grandchildren.

Social Security Loopholes for Married Couples

By Josh Espinosa, CFP®, CIMA®

Most of us are familiar with the analogy of the “three-legged stool” of retirement income: (1) Social Security; (2) savings and investments; and (3) pension plans.

As the saying goes, your level of stability during retirement depends upon the combined strength of each of these three legs; and a lack of planning in one of these areas could knock out a key structural component of your financial security.

As private pensions have steadily been phased out by most employers, the remaining two legs – investments and Social Security – have become even more critical for sustaining your desired lifestyle throughout retirement.

While the reality of today’s retirement income “stool” may be more wobbly than in years past, a strategic approach to maximizing your Social Security income can compensate for the lack of a private pension plan.

Changes to the Rules

As a result of the Bipartisan Budget Act of 2015, two Social Security loopholes for married couples were closed or restricted. The legislation could impact couples who are approaching retirement age with respect to their flexibility in claiming individual and spousal benefits.

Loophole #1 – File & Restrict

Under the previous law, if you are eligible for benefits both as a retired worker and as a spouse (or divorced spouse) and are not yet full retirement age (66 years), you must apply for both individual and spousal benefits. You will receive the higher of the two benefits.

The loophole allowed some married individuals to start receiving spousal benefits at full retirement age while letting their own retirement benefit grow by delaying it.

The new law is known as “deemed filing.” By applying for one benefit, you are “deemed” to have also applied for the other. Deemed filing has now been extended to apply to those at full retirement age and beyond.

Who’s Affected: If you were born after January 1, 1954, and will be eligible for Social Security benefits both as a retired worker and as a spouse (or divorced spouse), then the new law applies to you.

Note: File and restrict is still available if you were born before 1/1/1954 and your spouse is receiving benefits.

Loophole #2 – File & Suspend

The earlier law allowed a worker at full retirement age or older to apply for retirement benefits and then voluntarily suspend payment of those retirement benefits; which allowed a spousal benefit to be paid to his or her spouse while the worker was not collecting retirement benefits.

The worker would then restart his or her retirement benefits later (for example, at age 70), with an increase for every month retirement benefits were suspended.

Under the new law, you can still voluntarily suspend benefit payments at your full retirement age in order to earn higher benefits for delaying. But during a voluntary suspension, other benefits payable on your record – such as benefits to your spouse – are also suspended.

Also, if you have suspended your benefits, you cannot continue receiving other benefits (such as spousal benefits) on another person’s record.

Who’s Affected: The new law applies to individuals who request a suspension on or after April 30, 2016, which was 180 days after the new law was enacted. In short, the file and suspend loophole is no longer available unless already doing it.

Case Study – Maximizing Social Security Benefits

Despite the recent regulations surrounding Social Security, you and your spouse can still take steps to make the most of your benefits during retirement. Let’s explore a situation where we helped one of our client families maximize the value of their Social Security benefits.

George (age 66) and Doris (age 65) are a married couple who retired and moved to Naples in 2015. George served as the chairman of a large packaging and coatings company, and Doris was a small business owner.

Prior to becoming a CAS planning client, Doris started claiming Social Security benefits at age 63. The couple has sufficient cash flow to meet their retirement lifestyle needs before accounting for their Social Security income.

Based on their situation, we recommended that George delays his Social Security benefits until he reaches age 70. Because they do not need the extra income at this time, waiting until age 70 allows the benefits to grow at a rate of approximately 8% annually (increasing his annual benefits from $2,687/year to $3,538/year.

Since Doris is already taking Social Security benefits, George can also claim half of Doris’ spousal benefit until age 70 (based on her full retirement amount).

When George reaches age 70, Doris will also be able to activate her spousal benefits based on his increased benefit. Because she started claiming benefits before reaching full retirement age, she will get the difference of her income and half of George’s spousal benefit minus the early retirement reduction.

Doris also benefits from an increased benefit should George pass away before her. In this case, she would qualify for widow benefits at George’s full amount.

Overall, this strategy will maximize their total combined benefits based on both their life expectancies.

Note: There is no “one-size-fits-all” approach to managing your Social Security income flow. Your unique circumstances will serve as the foundation for developing an appropriate strategy for you and your family.

In some instance, delaying retirement income is not the most suitable option (especially if you are considering an assisted-living housing situation, in which case current income could be a more important criterion for admission than net worth).

Our CAS team has had the opportunity to help hundreds of client families determine the best approach for claiming their Social Security benefits. Before making any final decisions about your Social Security income, we recommend speaking with your advisor to establish a sustainable cash flow plan that fulfills your needs throughout retirement.

1 Based on an individual with full retirement age of 66, comparing early filing at age 62 and receiving reduced benefits of 75% of primary insurance amount versus delayed filing at age 70 and receiving credits to increase benefits by 32% of primary insurance amount.

NOTE: THE CASE STUDY PRESENTED IS BASED ON THE STORY OF A REAL CAS CLIENT FAMILY, BUT THE NAMES HAVE BEEN CHANGED TO PROTECT ANONYMITY.

Unleash the Power of Education – Your Guide to 529 Plans

By Steven T. Merkel, CFP®, ChFC®

In an increasingly competitive and high-skilled job market, a college education is almost a necessity for young people who are jumpstarting their careers. Many employers are demanding a college-educated workforce, and the rise of technology and automation is steadily replacing millions of blue-collar jobs.

Higher education serves as the key that unlocks the door to success and upward mobility, but the opportunities afforded by a college degree come at a cost. College tuition and fees have skyrocketed over the past 40 years, increasing at nearly twice the rate as medical care (see figure 1).

Although public and private university expenses have risen at a comparable rate, the raw increase in costs for private institutions has been far more drastic (tuition and fees at private universities have gone up by more than $19,000 annually – see figure 2).

By steadily saving throughout your lifetime for this investment in your child and grandchildren, you can position them for future success in their career and help to alleviate the burden of student loan debt that could otherwise loom in their future.

Although there are many ways to save, 529 college savings plans are the most popular and effective vehicle for unleashing the power of education in your child or grandchild’s life.

Let’s take a closer look at how 529 plans work, the benefits and limitations of these accounts, and how the new tax law has impacted 529 plans.

Figure 1. The cost of college tuition and fees has increased by more than 1,000% during the 35-year period of 1968-2013 – far outpacing the rate of increase in healthcare, housing and other commodities.

Figure 2. For private universities in the U.S., the average cost of tuition and fees for the 2017-2018 academic year is $34,740. For public colleges and university, tuition and fees in 2017 dollars have more than tripled since 1987.

A 529 college savings plan is a tax-advantaged account that is specifically designed for future education expenses. When you establish a 529 plan, you designate a single beneficiary (typically a child or grandchild) who is the intended recipient of the savings.

The funds in this account may be utilized on behalf of the student at any college, university, trade school, or post-secondary institution that is recognized by the Department of Education (when in doubt, check with the school or institution regarding their eligibility).

As the custodian, you have control over the account. The beneficiary of the plan can be updated at any time, and the funds from one 529 plan may be rolled over to another 529 plan without penalty.

In terms of asset allocation, you have the ability to choose from a range of mutual fund and exchange-traded fund (ETF) portfolios based on your risk tolerance and savings target. Consult with your advisor for more details on which 529 investment strategy is best suited for your needs.

Every state in the U.S. sponsors some form of a 529 savings plan. More than 30 states provide you with tax benefits when you contribute funds to the account (typically in the form of claiming a deduction on your state income taxes).

Most states also exempt you from paying state taxes on the earnings of the 529 plan when you make withdrawals for qualified education expenses. The specifics of these plans can vary significantly state-by-state (see figure 3).

For all 529 plans, you do not pay any federal income taxes on earnings within your account as long as the withdrawals go towards qualified education expenses (see figure 4).

TIP: When making withdrawals from the 529 plan, you should maintain records of all qualified education expenses you have incurred. In the unlikely event that you are audited, the IRS may request documentation.

Figure 3. 529 plans are sponsored at the state level and are subject to different tax benefits. Some states offer a generous deduction on state income taxes, while others offer tax benefits upon withdrawal of funds for qualified education expenses.

Figure 4. If withdrawals from your 529 plan are spent on qualified higher education expenses, the earnings in the account are not subject to federal income tax (and are typically exempt from state income tax as well).

TIP: Under the new tax law, states have been granted the ability to classify tuition and fees for private K-12 schools – up to $10,000 – as qualified education expenses (check your home state’s 529 rules).

529 Plan Rules

As with most tax-advantaged investment accounts, 529 college savings plans are subject to legal restrictions:

Annual gift tax exclusion – Another advantage of 529 plans is the potential to apply contributions towards your gift tax exemption for the year. While leveraging this tax benefit is a great perk, there may be significant gift tax consequences if you contribute more than $15,000 per year individual limit ($30,000 for married couples) to a particular beneficiary.

We encourage you to be mindful of any other expenses you have applied to the gift tax exemption and to adjust your 529 contributions each year so that you fall below the $15,000 GST threshold ($30,000 for married couples).

Exception: Most 529 plans allow you to make a one-time, lump-sum contribution of up to $75,000 ($150,000 for married couples) to the account – as long as you do not gift any additional money to the account beneficiary over the course of the next five years. In essence, you can deposit five years’ worth of contributions at one time instead of contributing $15,000 annually.

Note: Additional contribution limits may apply to your account based on the regulations in place for your state’s plan.

Non-qualified withdrawals – Although you are technically allowed to take withdrawals from the 529 plan for expenses other than the qualified items listed in Figure 4, the earnings portion of these distributions are subject to 10% withdrawal penalty. In short, taking non-qualified withdrawals negate the tax benefits of the account.

Some examples of expenses that are classified as non-qualified include transportation costs, health insurance (even university-sponsored coverage) and student loan repayments.

Changes under the New Tax Law

The Tax Cuts and Jobs Act of 2017 had a direct impact on two key areas of consideration for 529 plans.

First, states have been granted the ability to classify tuition and fees for private and religious K-12 schools – up to $10,000 – as qualified education expenses. Most states have not yet codified this new rule into their respective 529 plans, but the notion of tax-efficient savings for primary education is certainly encouraging for those who have children and grandchildren enrolled in private schools.

Secondly, you now have the ability to roll over funds from a traditional 529 account to a 529 ABLE account. ABLE accounts are specifically designed to enhance quality of life for Americans with disabilities. This new law does not impact your ability to roll over funds from one 529 plan to another 529 plan.

In contrast, the following areas have not been impacted by the tax reform legislation:

- Coverdell Education Savings Accounts

- American Opportunity Tax Credit (AOTC)

- Student Loan Deductions

- Exemption of Tuition Fee Waivers from Taxable Income

Investing in the Next Generation

A 529 plan is an outstanding vehicle for preparing your children and grandchildren to pursue successful careers, as well as mitigating the massive debt burden they could accrue during their collegiate experience.

To further sweeten the pot, 529 plans also carry significant tax advantages for you – serving as an excellent tool for gifting funds to future generations.

Figure 5. The upsides to leveraging 529 plans as an education savings tool are wide-reaching.

Time and time again, our CAS team has witnessed the success of 529 plans in unleashing the power of education for future generations. Contact your advisor to discover more about how we can work together to provide a bright future for posterity while capitalizing on opportunities for tax efficiencies within your investment portfolio.

Sources

Figure 1 – Bureau of Labor Statistics, 2013 Consumer Price Index (CPI)

Figure 2 – College Board, 2017 Annual Survey of Colleges

Figure 3 – Saving for College, 2017: How much is your state’s 529 plan tax deduction really worth?

Opportunities Abroad

By Jasen Gilbert, CFP®

By Jasen Gilbert, CFP®

The strong performance of the S&P 500 and the Dow Jones Industrial Average in 2017 was an encouraging sign for investors. While the above-average returns of U.S.-based investments receive a lot of attention in financial news outlets, international equity markets often fly under the radar.

As our team evaluated performance benchmarks both at home and abroad, we observed that the surge in U.S. equity markets mirrored a bullish trend that is happening across the globe. The scorecard is in: International markets – and especially emerging markets – actually outpaced the S&P 500 in 2017 (see figure 1).

The big question: Is the recent boom in international equity markets a fluke, or is it a sign of a greater long-term trend?

Figure 1. A comparison of 2017 market performance for three indices indicates that international markets outperformed U.S. benchmarks. Emerging markets led the way with a 33% return.

The Global Economic Reset

As with U.S. markets, international equity markets are cyclical by nature. After several years of lackluster performance, earnings in foreign markets are beginning to show the promise of recovery and growth (see figure 2a – the red line provides context for average annual returns).

We also observed that – despite modest growth in the U.S. – much of the global economy had been experiencing a recession since 2015, with a marked decline in global GDP growth and annual returns that were far below average (see figure 2b).

Figure 2a. Similar to U.S. markets, international equity valuation is subject to cyclical fluctuations over time.

Figure 2b. The drop in global GDP in 2015-2016 was almost as severe as the Great Recession of 2008-2009.

In addition to the cyclical ebb and flow of equity value, various additional economic and geopolitical factors suggest that a sustained upward trend in international markets could be on the horizon. The underlying fundamentals that drive market growth are strong, which could give way to a phenomenon known as the Global Economic Reset. We see the potential opportunity for pent-up consumer demand – coupled with significant improvements to the balance sheets of global corporations – to be translated into growth.

First, we have monitored the earnings per share growth of the All Countries World Index (excluding U.S. markets) over the past five years. Earnings have finally begun to recover after several years of negative growth, and the projections for 2018 are quite optimistic by comparison (see Figure 3). When coupled with the corresponding trends in GDP growth shown in Figure 2b, the outlook for international investing appears to be promising.

Figure 3.

By expanding our vantage point to examine the past 35 years, we observe that annual GDP growth from 1981-2008 (the “pre-crisis” time period) averaged 7%. In comparison, annual GDP growth from 2008-2016 has been about 5% on average. We anticipate that this metric may move closer to the 7% equilibrium over the long term – indicating that several years of above-average returns may arise within the near future.

Figure 4. The post-recession GDP growth of nations outside the U.S. has lagged behind the average annual growth rate of 7% from 1981-2008.

In addition to the economic indicators shown thus far, geopolitical factors have also created a scenario that could be ripe for strong international investment performance. When citizens are dissatisfied with the state of their nation’s economy – particularly in the case of a prolonged recession – democratic elections tend to favor candidates that propose pro-growth policies.

Alternatively, the current government leadership that is seeking re-election will make an effort to respond to the pleas of their business owners and workers so they can retain power. The results of upcoming elections and other political developments across the EU and Asia could have a profound impact on the growth outlook of the global economy.

Last by not least: Global corporations have made significant strides in improving their balance sheets. Whereas the ACWI debt-to-equity ratio for corporations ballooned to more than 32% in the early 2000s, a massive amount of debt has been paid off in the lead-up to the Global Economic Reset. The current debt-to-equity ratio is now about 23% – meaning that global corporations have much more capital to invest in the production of goods, delivery of services and labor (see figure 5).

Figure 5. Global corporations have made significant progress in reducing the amount of debt on their balance sheets, opening the door to more capital investment.

The synergy of these economic and political factors have created a “perfect storm” with the potential for strong international investment performance over the next few years. As a result of this trend, you could be well-served to include non-U.S. investments as a component of your diversified portfolio.

Balance in All Things

In addition to building a diversified investment portfolio for you, our CAS team works with our custodian partners to ensure that your international holdings are being rebalanced based on market trends and outlook in the global sector. Rebalancing involves a regular evaluation of how to best represent different equity classes in your portfolio.

In our evaluation, we consider a wide range of factors – two of which are national/regional performance trends and performance by industry. To illustrate this, let’s take a closer look at emerging markets in particular.

In figure 6, we observe that the international investing landscape has changed drastically since the late 1980s. As an example, Malaysia represented a large cross-section of the emerging markets universe in 1988; today, Malaysia is no longer a major player. China, Korea and Taiwan have emerged as the leading emerging markets, whereas many of the Latin American economies have fallen from prevalence.

Clearly, international markets are subject to the same steady, constant changes as U.S. markets, and the long-term effect of these fluctuations can lead to dramatic changes over the course of 30 years.

Figure 6. The emerging markets landscape has shifted dramatically over the past three decades, with Southeast Asia gaining prominence and Latin America/Malaysia receding.

The microcosm of emerging markets provides us with insights that can be applied broadly to the big picture of your financial plan. The need for diversification and regular rebalancing cannot be understated. By recognizing change and emerging opportunities over time and incorporating an appropriate balance of international markets within your portfolio, our team will work with you to capitalize on promising investing opportunities at home and abroad.

Contact your advisor to learn more about how CAS leverages international investments as part of your comprehensive financial plan.

Planning For Market Uncertainty in Retirement

For investors, 2017 proved to be a rewarding year. The S&P 500 index rose by more than 20 percent, and the Dow Jones Industrial Average surged past both the 20,000 and 25,000 thresholds in a single year.

The trend of strong market returns has continued throughout January. The bull market that began in March 2009 continues to push forward, despite ongoing speculation from financial professionals that equity markets could be overvalued.

The real question is: How long will the market continue to rise and when will equity markets reach their peak? No one can provide a definitive answer, as market forces and fluctuations in value are largely beyond our control.

Cycling through History

Although historical performance is limited in its predictive ability, past performance does provide us with significant context for understanding big-picture trends. Recent history illustrates that a strong, sustained bull market often precedes a correction bear market, as inflated equity markets return to a more stable valuation and investor confidence begins to wane.

The decade-long bull market of the 1990s began to reverse course in 2000 in the wake of the “dot-com” bubble burst and the emergence of several major accounting scandals (in particular, Enron and Arthur Andersen). The once-burgeoning technology industry was especially hard-hit, with the NASDAQ losing 39% of value in 2000 (followed by losses of 21% and 31% in 2001 and 2002, respectively). The Dow also decreased by more than 27 percent during this three-year window.

Equity markets began to bounce back in late 2002, ushering in a new bull market that was sustained through late 2007. At this point, the sub-prime mortgage crisis (among other factors) led to the most drastic correction market since the Great Depression. All three major indices lost more than 50% of their value in 17 months (between October 2007 and March 2009).

Although we have knowledge of market cycles, we cannot say with certainty what the future holds. For this reason, it is critical for you to be prepared for the possibility of a bear market – especially if you are approaching retirement or are currently living on retirement investment assets today.

Figure 1. Performance of the S&P 500 index, Jan 1998 through Jan 2018.

Navigate Uncertainty with Preparation and Prudence

Above all, the most effective way to prepare for uncertainty in equity markets is to plan well in advance for your needs and priorities during retirement. To develop the “stepping stones” for future retirement success, we recommend that clients and their family members begin to work through the planning process with an advisor at least 8-10 years prior to their desired retirement date.

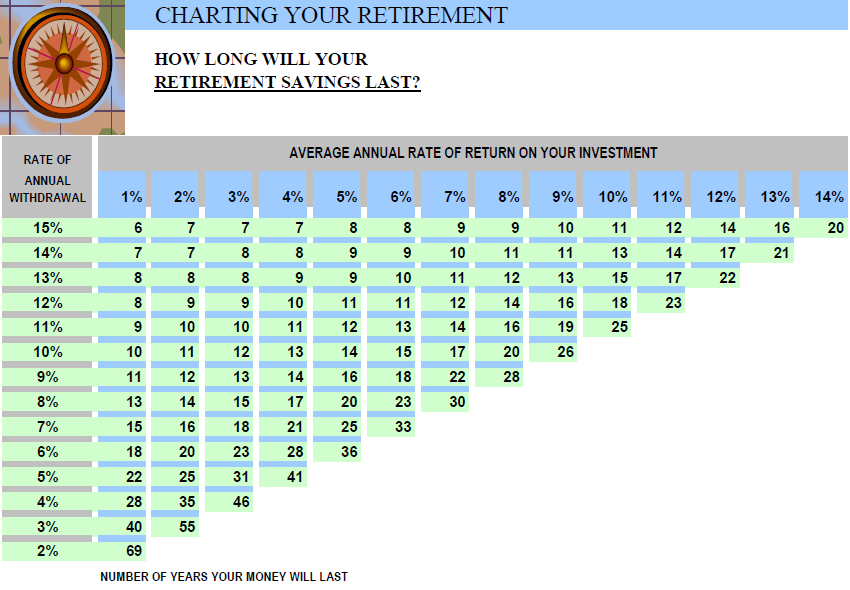

In our experience, the most effective retirement plans share two main characteristics: (1) a conservative draw rate and (2) a realistic, long-term approach to budgeting. With these provisions in place, you can build a strong, sustainable foundation for your financial success throughout retirement.

1. Be conservative when selecting your withdrawal rate. After working hard and accumulating assets throughout your lifetime, you will finally enter the asset distribution phase of life during retirement. As you begin to take distributions from your IRAs, 401(k)s and other investment accounts, you should exercise prudence when selecting your rate of withdrawal.

Your ideal withdrawal rate will vary based on your desired lifestyle (expenses) and your available asset base (income). That being said, we have generally seen great long-term success with a conservative draw rate of 4-5 percent.

When you begin to exceed 5 percent – especially once you enter the 7-9 percent range – it is likely that your withdrawal rate is not sustainable for the duration of your retirement. A high withdrawal rate – especially early in retirement – could cause your asset base to deteriorate at an alarming pace. As a result, you may find it difficult to meet expenses in your later years (especially with rising health care costs and uncertain market conditions).

Figure 2. Conservative draw rates can extend the lifespan of your retirement savings, regardless of fluctuations in the market.

2. Be realistic when developing your retirement budget. A detailed and well-thought-out budget for your retirement lifestyle is the key to determining your ideal withdrawal rate. Once you appreciate the full extent of your short-term spending priorities and long-term expenses throughout retirement, you can compare that figure to your asset base to determine the best withdrawal rate for your situation.

Apart from selecting a withdrawal rate that is too high, the biggest mistake you can make in retirement is to underestimate your expenses up front. When a retiree fails to plan for the inevitable costs that loom in their future, he or she will often take additional withdrawals beyond their predetermined distribution – which, in turn, threatens the long-term viability of their retirement savings.

Because budgeting is so crucial for promoting a sustainable retirement lifestyle, it is in your best interest to regularly consult with a financial expert to prevent overlooking key considerations and making costly mistakes.

As the current bull market enters its ninth year, we must not be lulled into a sense of false optimism or complacency. Our knowledge of market trends suggests that a bear market looms on the horizon; it is a matter of when, not if. Although the constant flux of market forces is beyond our control, you do have control over your expense budgeting and retirement income distributions.

While the specifics of your plan are dependent on your personal circumstances, the correct course of action when planning for your retirement lifestyle is preparation and prudence. With adequate foresight and consistent guidance from your advisory team, you can feel confident that your draw rates and spending habits will be sustainable throughout your golden years – regardless of the uncertainty that exists in the market.

Don’t Take the Bait!

Online commerce and communications have become ubiquitous in the lives of millions of Americans. Whether it’s online banking, shopping or social media, the Internet plays an integral role of our society.

Unfortunately, opportunistic hackers and scam artists are often quite tech-savvy, and they are actively attempting to swindle people and sow chaos on your computer or mobile device. Every year, especially during the peak of the holiday shopping season, we observe an uptick in a particular type of online fraud: phishing.

Most phishing emails or text messages share one primary goal: getting you to click on a link or open an attachment. If you receive a suspicious email, the most important thing to remember is DO NOT CLICK on anything in the email! By clicking on the content, you are potentially unleashing a barrage of malware and viruses that could harm your computer or mobile device.

Releasing the malware may be the end goal of some phishing scams, but others go a step further to hijack your personal information for financial exploitation. For example, you may be directed to a fake website prompting you to enter your log-in credentials for a financial institution or to input other confidential information.

Although it is almost inevitable that you will receive a fraudulent email or text message, many of these scams possess several recognizable characteristics. By understanding the signs of a phishing message and remaining vigilant when opening your emails, you can significantly decrease the likelihood of “taking the bait” from a phishing scam.

Telltale Signs of Phishing

♦ The email starts with “Dear Customer” or another generic greeting.

♦ The email is written in broken English or contains an excessive amount of grammatical errors.

♦ Hover your curser over the sender’s name to reveal the sender’s real email address. If the real email address does not match the email address displayed, it is likely a scam.

♦ Do a Google search for the sender’s email address/phone number or the email subject line, followed by the phrase “phishing” or “scam”. Take a look at the first few results to see if the email has been previously identified as malicious.

If the email possesses any of these characteristics, delete it immediately.

Confirm Your Order?

The fake “order confirmation” email is especially prevalent during the holidays. You may receive an email that appears to be from an online retailer, asking you to confirm your purchase. The hacker’s goal when sending an order confirmation phishing email is for you to “review your order” by either clicking on a link or opening the email’s attachment.

Of all the various scams, these emails are perhaps the most enticing. If you did not order anything from the retailer in question, you may be tempted to click or open to see what was ordered. On the other hand, if you had recently purchased from the online retailer, you may assume it was for your legitimate purchase and click on the link or attachment.

If you have an account with the supposed sender, log in to your account and check your order history. If no purchases are listed, the email is a scam. If you do not have an account with the supposed sender, it is almost certainly a scam.

While it is likely that an unexpected order confirmation email is the work of a phishing scam artist, it is also possible that someone has hacked into one of your online retail accounts and made fraudulent purchases. Just in case, monitor your credit card and bank transactions for fraudulent transactions. If detected, report it to the financial institution as soon as possible.

This holiday season, be vigilant when handling suspicious emails or text messages. By following the guidelines in this article and remaining aware of the signs of phishing emails, you can protect yourself and your devices from falling prey to the malicious attempts of online scam artists.