Economic Update – Second Quarter 2014

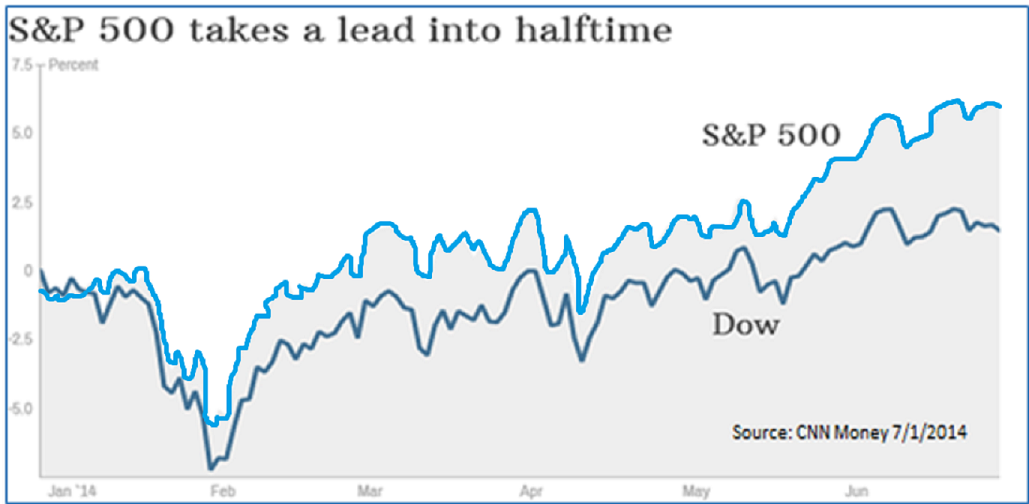

The year’s first half for equities can be summed up in simple terms: confusing and unpredictable markets produced gains. As of June 30, the S&P 500 had already logged 22 record highs this year alone, ending the first half up 6% while the Dow Jones Industrial Average (DJIA) increased by 1.5%. Both of these indexes hit new highs in the 2nd quarter while the NASDAQ Composite index rose by 5.5%, reaching a 14-year highpoint. Interestingly, 2014 has produced the biggest halftime lead by the S&P 500 over the DJIA since 2009 and the seventh-biggest since 1929, according to Bespoke Investment Group.

Bespoke also shared that in eight of the 10 years with the most underperformance, the DJIA has gone on to outperform the S&P 500 during the second half of the year. If this pattern holds, then the Dow might make up some of that lost ground. (Source: Barron’s, June, 2014)

Investors started 2014 with several serious concerns that were enough to make them nervous. How would the S&P 500 Index follow up 2013’s 30%+ gain (including dividends)? Would the market correct because the bull was getting tired, or would there be profit-taking? Would the slow improvement in the U.S. economy send bond prices lower, or would we see the Federal Reserve shift to higher interest rates? All of these fears made investors nervous.

Would the market correct because the bull was getting tired, or would there be profit-taking? Would the slow improvement in the U.S. economy send bond prices lower, or would we see the Federal Reserve shift to higher interest rates? All of these fears made investors nervous.

So far in 2014, the bond market has also fared well—in fact, better than most had expected. The yield on the U.S. Treasury ten-year note, which moves inversely to its price, fell to 2.51% from 2.76% at the end of the first quarter.

Unfortunately, many investors are having a hard time enjoying these increases, as concerns about lofty prices make it difficult to decide whether to keep funds in cash or stay invested. The forces driving the stock market to new highs and helping parts of the bond market to remain near record low yields don’t show immediate signs of changing.

What are the forces driving the rallies in both stocks and bonds? Many economists credit the aggressive efforts by the world’s major central banks to flood financial markets with new money in an effort to keep sluggish economies continually moving forward.

U.S. stocks have been supported by expectations that the U.S. economy, while still sluggish, will grow fast enough to keep corporate profits expanding. However, many investors no longer feel comfortable with that outlook, and have begun focusing more on what can go wrong with their portfolios than on where they can make money.

The current stock market rally has outlasted the historical average of other Bull Markets with higher returns. In contrast, the preceding Bear Market was much steeper and longer than average, and the gains from the period—from the beginning of the Bear Market to the end of this Bull Market—are currently near the median and below the average. This confusion can be why many investors are proceeding with great caution. (Source: Fidelity)

There is “still a bit of a fear-factor” among investors, said Thomas Huber, Manager of the T. Rowe Price Dividend Growth Fund. “Everyone is looking for what’s going to be the big crack in the markets.” (Source: Wall Street Journal, July 1, 2014)

While many investors are concerned about how markets will respond when the Fed raises interest rates in the future, there are also concerns building in the opposite direction regarding the estimate in the growth of our economy. The Commerce Department’s third and final estimate of the Gross Domestic Product (GDP) for the first quarter of 2014 continued the downward spiral of the first two estimates—from +0.1% to -1.0%, and now down to -2.9%. This was the largest drop recorded since the end of World War II that wasn’t part of a recession.

Many economists believe that the extent of the first quarter decline is so substantial that it makes it unlikely that we will reach a 2% increase, even if the next three quarters are significant. (Source: Bob LeClair’s Finance, June 28, 2014)

Early in the year, stocks ran into problems and investors blamed the harsh winter weather in large parts of the country. Several early indicators led to speculation that the economy was weakening, but in the 2nd quarter the market rebounded, sparked by thoughts that better growth was leading winter into spring. So far, those thoughts have proved to be accurate: the U.S. economy has improved, although there are still concerns over how strong the rebound will be.

A recent GDP report offered some positive data, including:

- Existing-home sales climbed 4.9%, the strongest gain in three years.

- New-home sales jumped 18.6% in May (the largest gain in more than 20 years) to an annual rate of 540,000 units, a six-year high. The median price for a new home also increased almost 7% from last year.

- The Conference Board’s confidence index improved to 85.2 in June. That was its highest reading since 2008, as many consumers were more optimistic about jobs and future conditions. (Source: Bob LeClair’s Finance, June 2014)

Will we be able to hold onto these gains and add enough through the end of the year to at least have a positive GDP for 2014? Let’s hope so. Slow growth could reduce corporate profits, which would be bad news for stocks and could lead to higher-than-expected default rates on junk bonds.

PRICE–TO–EARNINGS RATIO

Price-to-earnings (P/E) ratios have risen over the last two years, as improving investor confidence helped drive market gains. Some are focused on the current valuations which are slightly above the long-term average, 17.1 versus 15.1. The higher the P/E, the more likely the stock market is overpriced. Although most stock indices are at an all-time high, the market valuation is nowhere near its 2001 peak. (Source: Fidelity.com)

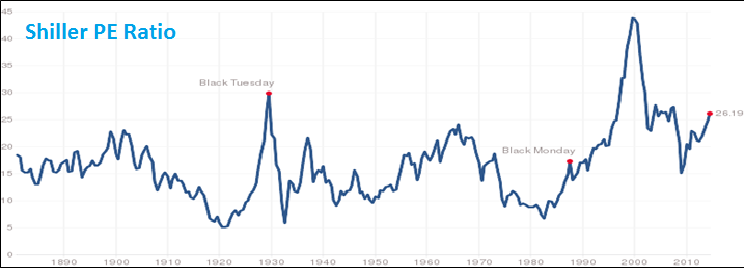

Even with a gain in the first half of 2014, bears exist. Nobel Prize-winning professor Robert Shiller notes that currently the market looked more expensive on a cyclically adjusted price/earnings basis only three other times in the past 130 years—1929, 2000 and 2007. The Shiller P/E ratio for the S&P 500 is based on average inflation-adjusted earnings from the previous 10 years. Despite this statistic in today’s low interest rate environment, Shiller is not telling investors to sell all of their holdings and to retreat to a bunker. He just thinks it might be time to be cautious and lighten up.

STOCK BUYBACKS

Many investors do not realize that one of the stock market’s biggest drivers today is stock buybacks. Companies buying back their own shares represent the single biggest category of stock buyers today, according to a study by Jeffery Kleintop, Chief Market Strategist at LPL Financial. (Source: Wall Street Journal, June 30, 2014)

Stock buybacks are also a source of controversy. Some economists say they allow companies to provide artificial support for stock prices by increasing demand for shares. Also, if a company reduces its number of shares, simple math shows that the earnings per share will rise even if the total earnings go nowhere. Most professional money managers look primarily at earnings per share, so buybacks can improve a company’s apparent earnings performance, even if overall earnings aren’t rising at all. Executives may use buybacks to manipulate share prices, helping them hit earnings targets, receive bonuses, and other benefits.

According to Mr. Kleintop, half of the first quarter’s S&P 500 per-share earnings gains came from declining share count, not from increases in actual earnings. (Source: Wall Street Journal, June 30th)

That doesn’t mean all buybacks are misguided, he added. In some cases, buybacks are better than dividends as a way to return money to shareholders because investors pay taxes on dividends and don’t pay taxes on buybacks unless they sell their shares.

GLOBAL

Financial markets worldwide are getting a boost from recent upbeat economic data out of China that is improving the outlook for global growth. China has increased its manufacturing activity and many economists believe that its appetite for raw materials will continue.

Many markets were rattled earlier this year by worries that China’s slowing growth would lead to a hard landing. However, the Chinese government has taken various measures to build investor confidence, including credit easing, more spending on highways, and business tax breaks.

After a massive credit boom in recent years, China continued to struggle to balance the competing objectives of tapering down its excessive credit expansion, preventing financial instability, and maintaining a fast pace of growth. Foreign capital inflows have risen and become more short-term in nature, increasing China’s vulnerability to shifts in global capital flows. (Source: Fidelity)

The U.K. and Germany remain the primary drivers of the European Economic Expansion, but there have now been indicators that other European economies have improved significantly, suggesting that Europe’s cyclical upturn continues to become more broad-based.

INTEREST RATES

Central bankers around the world debate whether very low interest rates, adopted in many economies since the 2008 financial crisis to spur stronger recoveries, are actually feeding market bubbles that could burst and potentially cause new financial turmoil. In June, Mario Draghi, President of the European Central Bank (ECB), made a bold move by cutting the main lending rate from 0.25% to a record low 0.15%. This pushed the deposit rate from zero to a minus 0.1%, effectively charging banks to park funds at the central bank. Following that move, Mr. Draghi said, “Are we finished? The answer is no. If need be, within our mandate, we aren’t finished here.” (Source: Barrons, June 2014)

The Fed has held short-term interest rates near zero since late 2008 and is winding down its bond-buying program. Recently, Janet Yellen, Chairperson of The Federal Reserve, assured investors and the public that the Fed won’t raise interest rates abruptly simply because some markets may look a bit volatile. The Fed has taken pains to reassure investors that interest rates will remain low even as the economic recovery picks up. (Source: Wall Street Journal, July 3, 2014)

Most Fed officials have indicated they expect to start raising interest rates in 2015, but the final decision will depend on whether the economy continues to strengthen as they forecast. The Fed has also stated that when it actually does increase rates, it will do so gradually and short‑term interest rates are unlikely to rise as high as they have in previous recoveries.

Many investors think that the rise in interest rates could happen sooner than the Fed’s estimate and the pace of increases could be more rapid than currently expected.

Historically, low interest rates and strong profitability have allowed U.S. corporations to reduce interest expense, improve their balance sheets, and accumulate liquid assets. Companies have used high cash balances to return capital to shareholders as both dividends and share buybacks, maintaining relatively high yield even though equity prices have continued to rise.

INFLATION

Inflation finally nudged above the 2% level that the Fed says is its long-term target. Compared with a year ago, the Consumer Price Index (CPI) is up 2.1% (not including food or energy). Although that might make the Fed happy, it sent a tremor of worry through analysts, investors, and economists.

Ongoing weak wage growth has continued to eliminate inflationary pressures in many developed economies. Weaker economic outlooks may help bring down inflation in some emerging markets’ economies over time. However, the rapid rise in agricultural prices could create inflationary pressures in many emerging economies, where food represents a higher proportion of consumer expenses. (Source: Fidelity)

UNEMPLOYMENT

On Wednesday, July 2, a report on the U.S. labor market was better than expected in that 281,000 private-sector jobs were created in June compared with an estimated increase of 210,000.

Although this is certainly good news, many investors say that stocks will need continued evidence of an improving economy to sustain the move higher. (Source: Wall Street Journal, July 3, 2014)

CONCLUSION

Equities have provided a nice return for the first half of 2014, so now what should an investor do? Your answer could depend upon your “worry level.” Some believe that stocks will benefit from robust earnings and low interest rates, while many other financial professionals are spending sleepless nights focusing on downward equity outlooks. The Federal Reserve has been a key factor in why equity markets have done well since 2009, but they have already started paring back their bond purchase programs and they will need to raise interest rates eventually.

Several money managers are suggesting that the five-year-plus bull market may be getting long in the tooth, but few are selling the bulk of their portfolios and leaving the room. Those money managers who sided with caution so far in 2014 have underperformed the indexes; however, even the great Confucius once said “the cautious seldom err.” Money managers that sometimes hold large cash positions don’t always move in sync with peers or benchmark indexes. Approaching market tops, they may become increasingly cautious, while peers remain fully invested. Thus, it is common for such money managers to trail peers when stocks are moving higher like they did in the first half of this year.

Several money managers are referring to the current period as the “new neutral.” Although U.S. stock indexes are pushing through fresh records and valuations have passed pre-financial crisis levels, some analysts believe markets aren’t overvalued yet.

“Sure, the S&P 500’s valuations look high on historical standards, but it’s really about ultra-low yields,” Bill Gross, chief investment officer at Pimco, told CNBC recently, citing Pimco’s “new neutral” mantra that the neutral federal funds rate will be lower for longer. “Based upon our assumption that this new neutral stays low, they’re not as bubbly as some would suggest,” Gross said.

“If fed funds going forward stops at 2% instead of 4%, which is historical, then [the Dow Jones Industrial Average, or DJIA] at 17,000 and high yield spreads at 350 basis points over Treasurys are attractive and are less bubbly than some would imagine,” he said.

In a blog post on July 2, Gross said that the “new neutral” means “all financial assets might logically be repriced relative to historical experience.”

Gross also noted that while the S&P 500’s 10-year cyclically adjusted P/E ratio, or cost adjusted P/E (CAPE), typically has predictive value of whether shares are overvalued, the “new neutral” indicates the CAPE’s historical median valuation of 17 times earnings may need to be adjusted to around 20-22 times. “That would mean the S&P 500’s current CAPE of 25 times isn’t terribly bubbly.”(Source: CNBC.com, July, 2014)

With the stock market setting new highs, investors face unusually tough choices. An examination of historical valuations points to proceeding with caution in the stock market. Normally during these times bonds would provide a safe harbor. Sadly, with interest rates still near historic lows, bonds might not provide the same portfolio protection as in years past and, potentially even worse, bond prices will decline when interest rates rise.

Fed Chairperson Janet Yellen warned investors on July 2 that, “Falling corporate bond spreads and volatility indicators are signs that investors may not fully appreciate the risk of future losses.” She continued her prepared remarks for a speech at the International Monetary Fund by also sharing, “that said, I do see pockets of increased risk-taking across the financial system.”

It’s not easy to structure a portfolio in the face of these risks, but investors still have to make some decisions. Perhaps the best advice is to continue to focus on your personal situation and timelines. Consider these three important questions:

- What is a realistic time horizon for my personal situation?

- What is a realistic return expectation for my portfolio?

- What is my risk tolerance?

Your answers to these questions will help us recommend what type of investment vehicles you should consider, which investments to avoid and how long to hold each of your investment categories before making major adjustments. For example, if you will need more cash flow from your investments over the next few years, you might consider different choices relative to someone who has a ten- to fifteen-year time horizon.

We are continually reviewing economic, tax and investment issues and drawing on that knowledge to offer direction and strategies to our clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.

On a final note, remember, one of the major causes of a stock market decline may not be investment performance—sometimes it’s investor behavior.

A good financial advisor can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the “emotions” out of investing for our clients. We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

P.S. During this year’s big Treasury rally, the question has been, “Who’s buying all those bonds?” The answer is the Federal Reserve. During the six months ended in May, the Fed bought 73% of all new Treasurys, notes Strategas Research Partners’ Daniel Clifton. That’s the largest percentage since the start of quantitative easing.

The reason isn’t greater demand, but reduced supply. With the budget deficit falling, the amount of bonds issued has declined faster than the Fed’s taper, or reduction in bond buying. That leaves a limited supply of bonds for others to buy, according to Clifton. Perhaps that’s why bonds have held up in the first half of 2014.