Economic Update – Third Quarter 2014

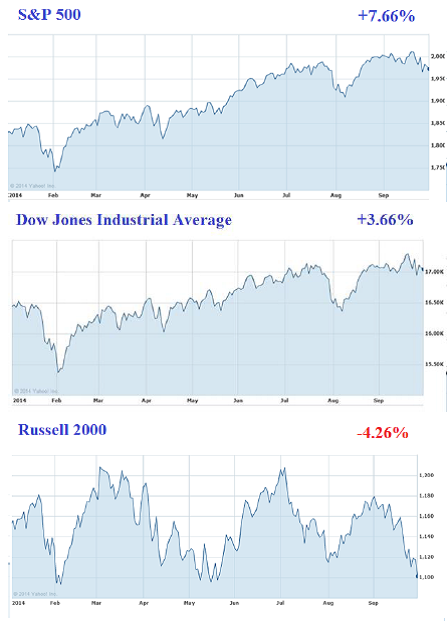

The third quarter of 2014 was very interesting. The overall results for many investors were positive, but while several diverse pockets of the market enjoyed gains, other stocks struggled. The S&P 500 and the DJIA (both of which track larger established companies) continued to outperform small stocks and foreign shares. Through Sept 30, 2014 the S&P 500 was up 7.66% and the DJIA was up 3.66%. By comparison, the Russell 2000 Index (which tracks small stocks) is down 4.26% for 2014. (Source: Wall Street Journal)

pockets of the market enjoyed gains, other stocks struggled. The S&P 500 and the DJIA (both of which track larger established companies) continued to outperform small stocks and foreign shares. Through Sept 30, 2014 the S&P 500 was up 7.66% and the DJIA was up 3.66%. By comparison, the Russell 2000 Index (which tracks small stocks) is down 4.26% for 2014. (Source: Wall Street Journal)

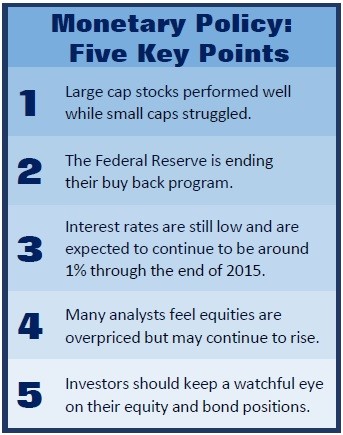

Many analysts feel that several U.S. big stocks are still more attractively priced than smaller stocks and that this trend could continue. “Small stocks are victims of their own success,” according to Jack Ablin, Chief Investment officer of BMO Private Bank. “They made a huge move last year and entered into this year overvalued. While there are great small company stocks, small caps in general need to take a back seat to their larger competitors until valuations come back into alignment.” In fact, some portfolio managers are fearful that the small cap underperformance has just begun. (Source: Wall Street Journal 9/29/2014)

Although caution still remains the top priority for most investors, many analysts feel that the bull could stay in charge for the rest of this year and possibly longer. Barron’s surveyed 10 top analysts in September and surprisingly, all of them felt that the upward trend would continue. While several analysts toned down their optimism because of the market’s gains, they still feel that we have not reached the market’s ultimate peak. They feel that rising corporate profits will continue to lead to increases in large cap stock prices. Having said this, they still caution investors about political tensions and interest rates. (Source: Barron’s 9/8/2014)

In a recent Interview, Dirk Hofschire, Senior Vice President of Asset Allocation Research at Fidelity Investments, said, “We continue to have a favorable global backdrop for asset prices. It’s been a Goldilocks environment where things are not too fast, not too slow, not too warm, not too cold. The U.S. economy has still been making progress, jobs are being created, unemployment is coming down and many leading indicators still point up.” (Source: Fidelity.com)

Investors are still keeping a watchful eye on the Fed—its bond buying program is set to end in October and many investors expect the Fed to raise interest rates sometime next year.

Recently, volatility has returned to the market and investors are noticing a “see-saw” effect between the bears (who are convinced stock prices will fall) and the bulls (who rush in during market swings to selectively add to their equity positions). Who is right? Only time will tell!

MONETARY POLICY

Many investors are watching the Federal Reserve very closely and with good reason. The Fed’s September bond purchases were only $15 Billion and in October they are moving towards their pledge to end the Quantitative Easing program of buying bonds. This is leaving many analysts concerned about the upward movement of interest rates. The Fed’s key interest rate target has been pinned at virtually zero since December 2008 (the depth of the financial crisis).

This is not the first time that the Federal Reserve has taken a “whatever it takes” approach to supporting monetary policy. Thirty-five years ago on October 6, 1979,  the Federal Reserve, led by Paul Volker, made a revolutionary change in how it handled monetary policy. Faced with double-digit inflation rates, the central bank responded by raising interest rates to 20%. Although this caused other aftershocks, this extreme policy would go on to tame inflation rates. (Source: Barrons 10/6/2014)

the Federal Reserve, led by Paul Volker, made a revolutionary change in how it handled monetary policy. Faced with double-digit inflation rates, the central bank responded by raising interest rates to 20%. Although this caused other aftershocks, this extreme policy would go on to tame inflation rates. (Source: Barrons 10/6/2014)

Monetary policy has had a key impact on the world’s major economies. Investors are rightly concerned about how effective monetary policy can be given the fact that central bankers have cut rates just about as much as they can.

According to Matthew Coffina at Morningstar research, “interest rates have been one of the biggest surprises of the year. Going into 2014, most pundits expected a steady rise in interest rates as the Federal Reserve winds down its purchases of long-term bonds and moves closer to raising short-term rates. Instead, the yield on the 10-year Treasury fell from 3% at the start of the year to a low of 2.34% in mid-August. The 10-year Treasury yield has since recovered to around 2.6%, but it remains below where many market observers had expected.”

Today, as the Fed prepares to wind down its extraordinary Quantitative Easing policy, interest rates are still close to zero. The consensus among analysts is that we are still about a year or so away from the Fed’s first interest rate hike, or tightening of the cycle. The Federal Reserve faces a delicate few months ahead amid internal debates over when to start raising interest rates and how to adjust its public guidance about its likely actions. The Fed and its current leader, Janet Yellen, have been clear in communicating that even when they get to that first tightening, they will probably go pretty slow in raising interest rates.

Many investors are still searching for safe, short-term debt. This demand intensified at the end of the quarter, pushing up bond prices and forcing down yields. The yield on the US Treasury bill on September 2nd reached a negative .01%. (Source: Wall Street Journal 9/24/2014)

During periods of market anxiety, Treasury Bonds can provide a safe harbor for many investors. So what should Bond investors do? Should they sit back and watch the data and refrain from taking any long term positions?

The entire bond market suffered when interest rates rose last year. If the Fed changes rates it could affect shorter dated bonds. Russ Koesterich, Chief Investment Strategist at Blackrock, warns to be careful with even two to five year Treasury bonds. (Source: Barron’s 9/1/2014)

While bonds are an important part of many financial plans, this is a good time to be very watchful of all income-oriented investments. Interest rates have remained at historically low levels for quite some time. Global rates continue to remain exceptionally low and that typically reduces the risk of a swift upward movement in U.S. interest rates.

Recent employment reports painted a brighter picture of the U.S. economy, but they also showed stagnant workers’ wages. Without rising incomes, the Fed seems to be less worried about inflation. That means that even though the jobless rate has hit a level at which the Fed might otherwise consider raising interest rates, it is no longer under the inflation gun when it comes to timing. (Source: Barron’s 10/6/2014)

It is anyone’s guess when the Fed will raise interest rates and by how much. On a positive note, Federal Reserve Chairperson Janet Yellen stated that she sees interest rates continuing around 1% until the end of 2015.

PRICE–TO–EARNINGS RATIO

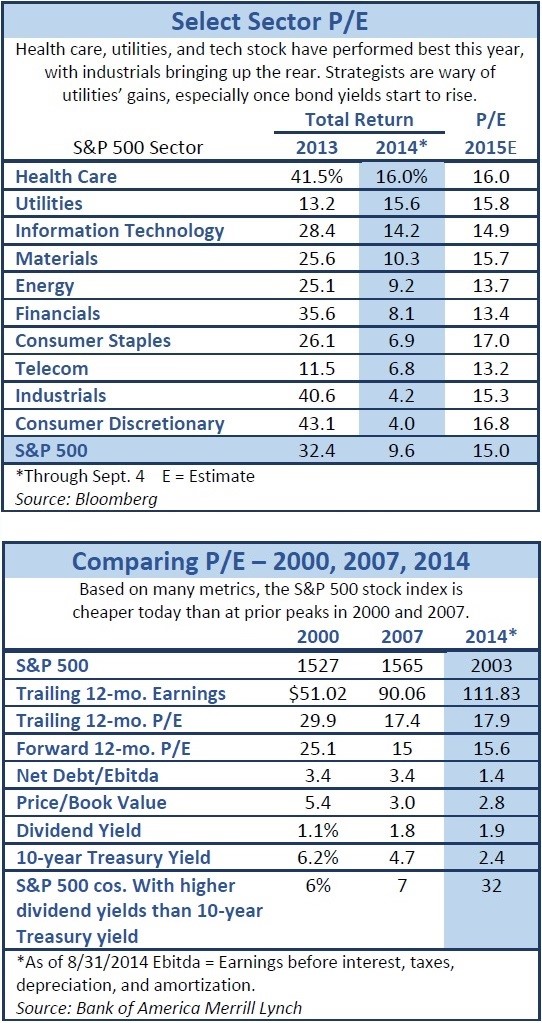

Price-to-earnings (P/E) ratios are still a key factor in the valuation of equities for many analysts. P/E is a valuation ratio of a company’s current share price (market value) compared to its per-share earnings. For example, if a company is currently trading at $40/share and earnings over the last 12 months were $2/share, the P/E ratio for the stock would be 20 ($40/$2). Generally a high P/E ratio means that investors are anticipating higher growth in the future.

According to a Barron’s survey in September, P/E ratios were one of the main criteria used by 10 top analysts to measure equity valuations. They felt that with macroeconomic data improving and profitability broadening out, a case could be made that the market’s P/E ratios were extended but not outrageous. They viewed U.S. stocks as neither cheap nor expensive, considering the low level of interest rates. “Stocks offer less compelling value than a few years ago,” says Savita Subramanian, head of U.S. Equity and Quantitative Strategy at Bank of America Merrill Lynch. “But if anything, there’s an upside risk to my view.” (Source: Barron’s 9/1/2014)

Steven Auth, Chief Investment Officer of Federated Investors, is more bullish. “The U.S. economy is accelerating and so are earnings,” he said, adding that his market views have been right on for the past two years. (Source: Barron’s 9/1/2014)

However, John Campbell, a Harvard economist who collaborates with Robert Shiller (a Nobel laureate in economics who is also a noted P/E watcher) feels that based on today’s P/E measurements, stocks are overpriced. (Source: New York Times)

While the P/E ratio can be informative, you can see that not even the experts always agree on what it means. It is therefore important not to base a decision on this measure alone. When the denominator in this equation (earnings per share) shrinks, the actual numbers can change significantly.

STOCK BUYBACKS

Once again in the third quarter, corporate managements preferred to put their cash to work by purchasing their own stock. Reducing the number of outstanding shares raises the earnings per share. To the extent that corporate executives are compensated with stock, this can enhance their stakes. Many analysts presume that the decision to buy back stock is fueled by analyses that suggest that stock buybacks yield a better return than investments in expanding the businesses.

THE ECONOMY

Positive economic news during this quarter included the following:

- The U.S. labor market is improving at a faster rate, though gains remain slow enough to avoid provoking broad-based, late-cycle wage inflation. Year to date, the economy has added 1.6 million jobs—the 1.9% year-over-year increase in July was the fastest pace of growth since 2006.

(Source: Bureau of Labor Statistics)

- Core consumer inflation has slowed to 1.9% year over year. (Source: Fidelity.com)

- Personal consumption is still growing at a relatively modest 4% (nominal) year-over-year pace. (Source: Bureau of Economic Analysis, Haver Analytics)

In addition to this good news, of course, there were still some concerning factors. The main one was the housing sector, which remains in a soft patch, even though leading indicators are showing signs of slow improvement. Sales activity remains at historically weak levels and prices have flattened over the past three months. Construction starts and permit issuance remain at low levels, though they rose in July and remain in an upward trend. (Source: Core-Logic, Haver Analytics)

Although mortgage credit remains relatively tight during this quarter, banks reported the broadest rise in more than 20 years in their willingness to make residential loans during the second quarter.

GLOBAL OUTLOOK

Although differences vary wildly across the globe, overall economic developments outside the U.S. appear to be moving slowly and carefully.

Eurozone growth has idled due to GDP reductions in their two largest economies—Germany and France. However, analysts believe this might be a mid-cycle slowdown instead of the start of a new recession. Bank lending standards have eased up across the board and the European Central Bank has indicated a desire to help beyond the monetary stimulus plans already announced. The rate of growth is likely to remain low, with about 60% of the region’s economies experiencing expansion in their leading economic indicators during the past six months, down from 90% at the start of 2014.

Japan’s outlook remains ambiguous. Due to April’s tax hike, they recently underwent a worse-than-anticipated 19% annualized contraction in second quarter consumer spending. With the tax hike over, consumption should stay stable. Economic indicators have improved, but they still remain below the levels seen before the tax increase.

China, on the other hand, continues to benefit from their second quarter stimulus. However, leading indicators are exposing the diminishing returns that these policy decisions can provide and any return to expansive growth remains questionable. China’s property sector has been persistently plagued by falling housing prices and rising inventories and continues to be the largest near-term risk for economic and financial stability.

Across other developed markets, conditions vary drastically. Countries such as Indonesia and India seem to have benefited from the global stabilization after the interest rate shudder in 2013. Elections of perceived reformers have also seemed to add optimism back into their respective economies. Other emerging markets, such as Brazil, have been hindered by recessionary conditions. The weak global situation and diminishing commodity prices continue to challenge many developing countries. However, this significant variation among the world’s economies is still pushing the global business cycle into a slow upward trend.

INFLATION

The rate of inflation is something that is always monitored by the Fed and investment professionals. As mentioned earlier, inflation appears to be under control. However, it is important to remember that this number (which excludes food and energy) rose at its fastest pace in 15 months. (Source: Barron’s 6/23/2014)

Currently inflation isn’t high enough to cause much damage to the stock market, says Ned Davis of Ned Davis Research. He notes that since 1925, the S&P 500 has dropped 5% a year on average, when the inflation rate has exceeded the S&P500’s yield by more than 2.1 percentage points. While May’s 2.1% inflation rate was higher than the S&P 500’s 1.9% dividend yield, it’s in a range where shares have historically produced positive returns. (Source: Barron’s 6/23/2014)

Many investors are also concerned that inflation might start to decrease dramatically and actually cause a very unusual dilemma: deflation. This has already taken hold in many different European countries. The European Central Bank cut interest rates significantly and stimulated bank lending—moves that were specifically aimed at reversing this trend before other countries might encounter this problem. (Source: Wall Street Journal 6/6/2014)

CONCLUSION

Volatility seems to have returned to the equity markets and past 4th Quarters have seen their share of market swings. Analysts are focused on earnings, the Fed, the economy and stock valuations. However, individual investors still have to look at their own situations first. It is important to be cautious, but it is just as important to determine your own personal risk or “worry” level. That’s where we can help.

Now is good time to ask yourself:

- Has my risk tolerance changed?

- What are my investment cash flow needs for the next few years?

- What is a realistic return expectation for my portfolio?

Your answers to these questions will govern how we recommend investment vehicles for you to consider. We can help you determine which investments to avoid and how long to hold each of your investment categories before making major adjustments. For example, if your cash flow needs have changed for the next few years, you might consider different investments than someone who has limited to no cash flow needs.

We continually review economic, tax and investment issues and draw on that knowledge to offer direction and strategies to our clients.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings and

- continuing education for our team on the issues that affect our clients.

A good financial advisor team can help make your journey easier. Our goal is to understand our clients’ needs and then try to create a plan to address those needs. We continually monitor your portfolio. While we cannot control financial markets or interest rates, we keep a watchful eye on them. No one can predict the future with complete accuracy, so we keep the lines of communication open with our clients. Our primary objective is to take the emotions out of investing for our clients. We can discuss your specific situation at your next review meeting, or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial matters.

P.S. Under normal conditions, Fed tightening wouldn’t be too much of a worry. Since 1983, the Standard & Poor’s 500 Index has averaged a 4.4% gain during the 6 months before a hike and another 7.7% during the six months following it, according to Strategic Research Partners. The only problem: These aren’t normal times!