2013 Year-End Tax Report

Year-End Tax Moves for 2013

One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current on ever-changing tax reduction strategies. This special report covers the details of many year-end tax strategies for 2013. Remember—every situation is different and not all strategies will be appropriate for you. Please discuss all tax strategies with your tax preparer prior to making any final decisions.

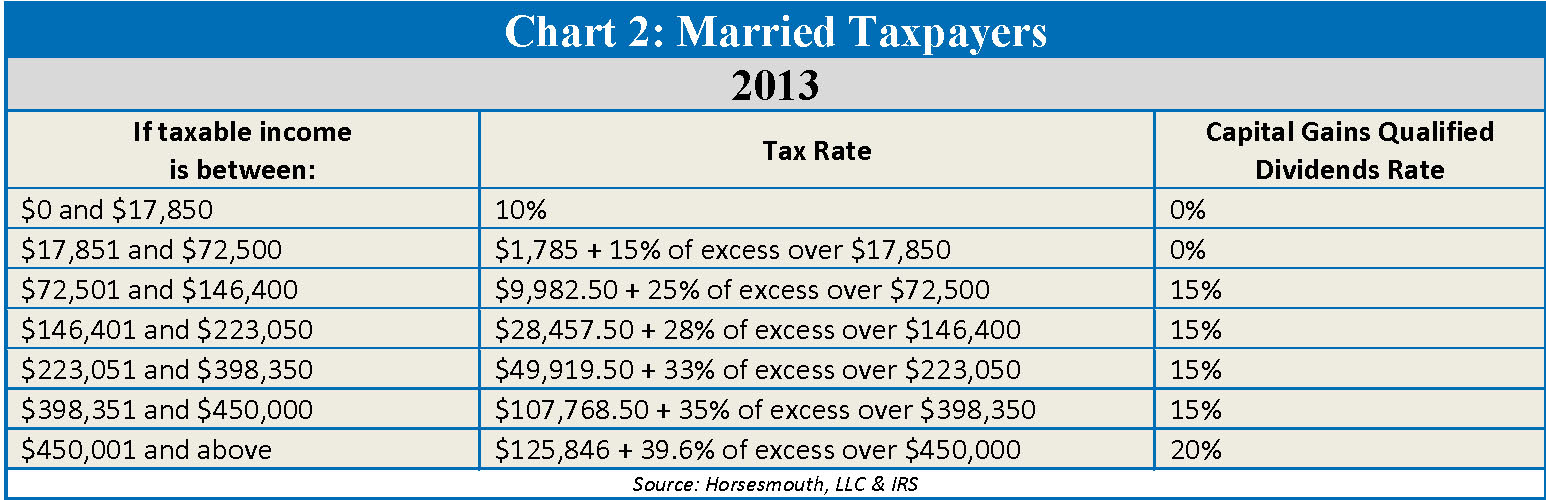

Income Tax Rates for

Income Tax Law Changes

Thanks to the American Taxpayer Relief Act of 2012 (ATRA), taxes rose sharply in 2013. The top marginal ordinary income tax rate for all taxpayers increased from 35% in 2012 to 39.6% in 2013. Additionally, the top marginal capital gains tax rate on long-term capital gains and qualified dividends increased from 15% in 2012 to 20% in 2013.

Medicare Tax

There are two major changes to the Medicare tax. The first is an additional 0.9% Medicare tax on wages and other earned income (such as self-employment income) exceeding certain thresholds. The other more expansive change is a 3.8% Medicare surtax on “net investment income” for wealthy taxpayers. The 3.8% Medicare surtax is on top of ordinary income and capital gains taxes, meaning long-term capital gains and qualified dividends may be subject to taxes as high as 23.8%, while short-term capital gains and other investment income (such as interest income) could be taxed as high as 43.4%!

The Medicare surtax is imposed only on “net investment income” and only to the extent that total “Modified Adjusted Gross Income” (“MAGI”) exceeds $200,000 for single individuals and $250,000 for taxpayers filing joint returns. The chart below shows which types of income are subject to this new Medicare tax.

For those of you who will be subject to this new Medicare surtax, some of the strategies that we can consider will take time to implement. Now is a good time to review your situation. For example, you might:

- Consider investing in tax-advantaged vehicles such as: tax-exempt bonds, qualified retirement accounts, qualified annuities, or cash value life insurance policies (assuming that the cost of acquisition and maintenance does not exceed the tax savings).

- Convert passive real estate activities to active interests.

- Marry someone who has large capital loss carry-forwards, or currently has large net operating losses (NOLs).

For specific ideas, please call our office or bring this up at your next review.

Capital Gains and Losses

Looking at your investment portfolio can reveal a number of different tax saving opportunities. Start by reviewing the various sales you have realized so far this year on stocks, bonds, and other investments. Then review what’s left and determine whether these investments have an unrealized gain or loss. (Unrealized means you still own the investment and haven’t yet sold it, versus realized, which means you’ve actually sold the investment.)

Know your basis. In order to determine if you have unrealized gains or losses, you must know the tax basis of your investments, which is usually the cost of the investment when you bought it. However, it gets trickier with investments that allow you to reinvest your dividends and/or capital gain distributions. We will help you calculate your cost basis.

Consider loss harvesting. If your capital gains are larger than your losses, you might want to do some “loss harvesting.” This means selling certain investments that will generate a loss. You can use an unlimited amount of capital losses to offset capital gains. However, you are limited to only $3,000 of net capital losses that can offset other income, such as wages, interest and dividends. Any remaining unused capital losses can be carried forward into future years indefinitely.

Be aware of the “wash sale” rule. If you sell an investment at a loss and then buy it right back, the IRS disallows the deduction. The “wash sale” rule says you have to wait at least 30 days before buying back the same security in order to be able to claim the original loss as a deduction. However, while you cannot immediately buy a substantially identical security to replace the one you sold, you can buy a similar security—perhaps a different stock in the same sector. This strategy allows you to maintain your general market position while utilizing a tax break.

Sell worthless investments. If you own an investment that you believe is worthless, ask your tax preparer if you can sell it to someone other than a related party for a minimal amount, say $1, to show that it is, in fact, worthless. The IRS often disallows a loss of 100% because they will usually argue that the investment has to have at least some value.

Always double check brokerage firm reports. If you sold a stock in 2013, the brokerage firm reports the basis on an IRS Form 1099-B in January 2014. Unfortunately, there were a number of problems implementing the new reporting rules last year, so we suggest you double-check these numbers to make sure that the basis is calculated correctly and does not result in a higher amount of tax than you need to pay.

Zero Percent Tax on Long-term Capital Gains

You may qualify for a 0% capital gains tax rate for some or all of your long-term capital gains realized in 2013. The strategy is to calculate how much long-term capital gain you would need to recognize to take advantage of this tax break.

The 0% long-term capital gains tax rate has been permanently extended for taxpayers who end up in the 10% or 15% ordinary income tax brackets, which is up to $36,250 for single filers and $72,500 for joint filers. If your taxable income goes above this threshold, then any excess long-term capital gains will be taxed at a 15% capital gains tax rate and/or 20% capital gains tax rate, depending on how high your taxable income is for the year. (NOTE: The 0%, 15% and 20% long-term capital gains tax rates only apply to “capital assets” (such as marketable securities) held longer than one year. Anything held one year or less is considered “short-term capital gains” and is taxed at ordinary income tax rates.)

If you are eligible for the 0% capital gains tax rate, it might be appropriate to sell some appreciated stocks to take advantage of it. Sell just enough so your gain pushes your income to the top of the 15% tax bracket, then buy new shares in the same company. You do not have to comply with the “wash sale” and wait 30 days. With “gains harvesting,” you can actually sell the stock and buy it back in the same day. Of course, there will be transaction costs such as commissions and other brokerage fees. At the end of the day you will have the same number of shares, but with a higher cost basis. Please remember, you must also review your state income tax rules to determine whether or not these gains will be tax-free at the state level.

If you’re ineligible for the 0% capital gains tax rate, but you have adult children in the 0% bracket, consider gifting appreciated stock to them. Your adult children will pay a lot less in capital gains tax than if you sold the stock yourself and gifted the cash to them.

Taxation of Social Security Income

Social Security income may be taxable, depending on the amount and type of other income a taxpayer receives. If a taxpayer only receives Social Security income, this income is generally not taxable (and it is possible that the taxpayer might not even need to file a federal income tax return).

If a taxpayer receives other income in addition to Social Security income, and one-half the Social Security benefits plus the other income exceeds a “base amount,” then up to 85% of the Social Security income could be taxable. The “base amount” is $25,000 for single filers, $32,000 for married taxpayers filing a joint return. A complicated formula is necessary to determine the amount of Social Security income that is subject to income tax. (We suggest using the worksheet in IRS Publication 915 to make this determination.)

Finally, please note that Social Security income is included in the calculation of “Modified Adjusted Gross Income” (“MAGI”) for purposes of calculating the 3.8% Medicare surtax on “net investment income” (as discussed earlier). Therefore, taxpayers having significant net investment income will have more reason to defer Social Security benefits.

Kiddie Tax

When you make gifts to minors, pay close attention to the “kiddie tax.” This tax was tightened up a few years ago, so in more cases investment income earned by minors will be taxed at their parents’ highest marginal tax rate. Generally, the kiddie tax kicks in when a child’s investment income exceeds $2,000 for the year and the child was under age 19 (or under 24 if a full-time college student). It doesn’t matter if the parents claim the child as a dependent. (Details about the kiddie tax can be found in IRS Publication 17, IRS Publication 929 and in the instructions to IRS Form 8615, which are available for free at www.irs.gov.)

Itemized Deductions & Exemptions

Taxpayers are entitled to take either a standard deduction or itemize their deductions on IRS Form 1040, Schedule A. Itemized deductions include, but are not limited to, mortgage interest, certain types of taxes, charitable contributions and medical expenses. Unfortunately, itemized deductions are subject to several limitations. For example, starting in 2013 medical expenses are now deductible only to the extent that they exceed 10% of AGI in any given year. (The deductible was only 7.5% of AGI in 2012, which represents an increase of the deductible by 33% in only one year!) If you or your spouse are over 65, the deduction limit will stay at 7.5% until December 31, 2016.

Many taxpayers don’t have enough itemized deductions to reduce their taxes more than if they take the standard deduction. If you find you miss the threshold by only a small amount per year, it may be best to “bunch” your deductions every other year, taking a standard deduction in the alternate years. The standard deduction for 2013 is $6,100 for singles, $6,100 for married persons filing separate returns, and $12,200 for married couples filing jointly. However, for 2014, it is $6,200 for singles, $6,200 for married persons filing separate returns, and $12,400 for married couples filing jointly.

Confirm that you are taking all available dependent exemptions. It might be best to support your parents to make them dependents. Providing more than one-half of the support of a parent qualifies for the $3,950-per-dependent exemption and the ability to deduct medical, dental and educational expenses incurred for the parent or parents.

Miscellaneous Year-End Tax Reduction Strategies

Prepare a tax projection for 2013 and possibly 2014 to determine which tax bracket you are in. Then make use of the following strategies if they apply to your situation.

- If your itemized deductions/standard deduction and personal/dependency exemptions are greater than your gross income, you will have negative taxable income, with a $0 income tax liability. (This is often the case with seniors who receive tax-free Social Security income.) Thus, it may be prudent to increase your income from negative taxable income to zero taxable income (still zero tax!).

– One way to do this is to do a partial Roth IRA conversion (see later discussion).

– Another option would be to postpone some deductible expenses to 2014, which will increase your taxable income.

- If you are itemizing your deductions in 2013, you may want to consider accelerating some of these deductions before the end of this year (assuming that you have a taxable income this year). You can make your January 2014 mortgage payment in December 2013, maximize your payments of state or sales taxes (for example, by buying big ticket items in December), prepay state income taxes, or pay all your property taxes in 2013 rather than deferring them to 2014.

– Remember the credit card rule: a deductible expense is deducted in the year it is charged against your credit card regardless of the year in which you pay the credit card bill. So, you can still charge a deductible expense in 2013, deduct it on your 2013 tax return and not have to pay for it until 2014. Please remember that interest expense paid on personal debt, which most interest on credit cards is, is not deductible even if you itemize.

It is important to note that some itemized deductions (such as state income taxes, real estate taxes and miscellaneous itemized deductions) are not allowed when computing the “Alternative Minimum Tax” (“AMT”). If you are subject to the AMT, it is often best to delay payment on the disallowed deductions and push them off until 2014 or later tax years (when AMT is no longer an issue). It is always possible you might be able to use the deductions next year. We suggest that you talk with your tax preparer about AMT prior to using any deduction and exemption strategies we have mentioned.

Paying taxes is bad enough. Paying a penalty is even worse. If you face an estimated tax shortfall for 2013, have the extra tax withheld on an IRA distribution. Withheld taxes are treated as if you paid them evenly to the IRS throughout the year. This can make up for any previous underpayments, which could save you penalties.

If you turned age 70½ during 2013, you must take a “required minimum distribution” (“RMD”) from your traditional IRAs and/or qualified retirement plans (such as a 401(k) plan) on or before April 1, 2014. If you do not take out the entire amount of your first RMD by April 1, 2014, you will be faced with a 50% penalty on the amount that you failed to take out. Also, keep in mind that once you start taking RMDs, you will need to take them until you die. Failure to take out the entire RMD in any given year will result in a 50% penalty on the difference between the RMD and the amount you actually took out. (NOTE: If your first RMD is due by April 1, 2014, you will be responsible for taking out two RMDs in 2014. This will often put you in a higher tax bracket in 2014. Therefore, if you need to take out your first RMD by April 1, 2014, you may want to take your first RMD out on or before 12/31/2013.)

Charitable Giving

This is a great time of the year to clean out your garage and give your items to charity. However, please remember that you can only write off these donations to a charitable organization if you itemize your deductions. Sometimes the donations can be difficult to value. You can find estimated values for your donated clothing at http://turbotax.intuit.com/personal-taxes/itsdeductible/.

Send cash donations to your favorite charity by December 31, 2013, and be sure to hold on to your cancelled check or credit card receipt as proof of your donation. If you contribute $250 or more, you also need a written acknowledgement from the charity.

If you plan to make a significant gift to charity this year, consider gifting appreciated stocks or other investments that you have owned for more than one year. Doing so boosts the savings on your tax returns. Your charitable contribution deduction is the fair market value of the securities on the date of the gift, not the amount you paid for the asset, and therefore you avoid having to pay taxes on the profit!

Do not donate investments that have lost value. It is best to sell the asset with the loss first and then donate the proceeds, allowing you to take both the charitable contribution deduction and the capital loss.

Up through December 31, 2013, taxpayers age 70½ and older can transfer up to $100,000 directly from their IRA over to a charity, satisfying all or part of the required minimum distribution (RMD) with this IRA-to-charity maneuver.

Retirement Plans

In 2013, the maximum 401(k) and 403(b) contribution is $17,500 (plus a $5,500 catch-up contribution for those 50 or older by the end of the year). If you are self-employed, you have other retirement savings options. We can review these alternatives with you at your next appointment.

You can also contribute to a traditional IRA and/or Roth IRA for the 2013 tax year all the way up to April 15, 2014. The maximum traditional/Roth IRA contribution is $5,500 with a catch-up provision of $1,000. The traditional IRA deduction phases out depending on your MAGI and whether you or your spouse is covered by a workplace retirement plan. Depending upon your income level, you may be eligible to contribute to a Roth IRA. To determine your best decision, call our office or ask us at your next review.

Roth IRA Conversions

Some IRA owners are considering converting part or all of their traditional IRAs to a Roth IRA. This is never a simple and easy decision. Roth IRA conversions can be helpful, but they can also create immediate tax consequences and can bring additional rules and potential penalties. It is best to run the numbers and calculate the most appropriate strategy for your situation. Call us if you want to review your options.

Step-Up in Basis Rules

If someone gifts you an appreciated asset while he/she is alive, then your basis is the same as the basis of the donor (not the current fair market value). However, if you inherit certain appreciated assets, you receive a step-up in basis to the fair market value as of the date of the decedent’s death. This new cost basis is often much greater than the original basis that the decedent had in this investment. (Some investments, such as tax-deferred accounts like traditional IRAs, do not receive a step-up in basis.)

So, if you’re the one doing the gifting, how do you determine which asset is the best one to give?

- High-basis assets or cash are usually best, especially if you’re in poor health.

- Low-basis assets (properties with big gains) usually aren’t good gifts because gifted assets don’t usually receive a step-up in basis, so the recipient’s basis will be the same as your basis. The recipient will owe capital gains taxes on all the appreciation since you first bought the asset when they decide to sell. Holding such an asset in your estate until you die allows it to pass by way of inheritance, which grants the recipient a step-up in basis.

- Appreciated assets can be much better than cash if you are worried about the recipient spending the money instead of investing it. There are also other ways to reduce the chance that the recipient will sell the assets and spend the proceeds, such as giving through a trust, partnership or other vehicle.

- Appreciated assets can also be a good idea when the recipient is in the 0% capital gains tax bracket.

Estate and Gift Tax Opportunities

In 2013, each taxpayer can pass up to $5,250,000 (minus prior taxable gifts) to children and/or other beneficiaries without having to pay gift and/or estate taxes. Any transfers in excess of the $5,250,000 exemption amount are subject to a flat 40% tax rate. Each $1 of the gift tax exemption you use during lifetime reduces your estate tax exemption by $1. (NOTE: The $5,250,000 exemption amount is for federal gift and estate taxes only. Depending on which state you live in, there could be state gift, estate and/or inheritance taxes imposed.)

Many people believe that with the estate tax exemption set at over $5,000,000 per person, they don’t need to worry about shrewd, tax-wise ways to give wealth. However, these people might want to rethink their strategy. Congress can change the law (and has changed the law in the past), and your wealth could grow faster than expected, thereby subjecting you to estate tax. Nevertheless, before you gift something away, you need to consider the income tax effects of making a particular gift. Giving away the wrong asset can cost your family some unnecessary taxes.

Make use of the annual gift tax exclusion. You may gift up to $14,000 tax-free to each person in 2013. These “annual exclusion gifts” do not reduce your lifetime gift tax exemption. (NOTE: The annual exclusion gift is doubled to $28,000 per recipient for joint gifts made by married couples or when one spouse consents to a gift made by the other spouse.)

Help someone with medical or education expenses. There are opportunities to give unlimited tax-free gifts when you pay the provider of the services directly. The medical expenses must meet the definition of deductible medical expenses. Qualified education expenses are tuition, books, fees, and related expenses but not room and board. You can find the detail qualifications in IRS Publications 950; and the instructions for IRS Form 709 at www.irs.gov.

Don’t give loss property. When you give loss property, the recipient’s basis is the current fair market value. It may be better for you to sell the property and deduct the loss on your tax return, and then you can give the cash proceeds.

Review state gift tax rules. Make sure that any strategies you use also apply to your state. In fact, some taxpayers actually move to another state and establish residency in that state before selling or gifting any property.

Contribute to a 529 plan on behalf of a beneficiary. This qualifies for the annual gift-tax exclusion. Withdrawals (including earnings) used for qualified education expenses (tuition, books and computers) are income tax free. The tax law even allows you to give the equivalent of five years’ worth of contributions up front with no gift-tax consequences. Non-qualifying distribution earnings are taxable and subject to a 10% tax penalty.

Consider the beneficiary’s situation before making a sizable gift. Keep in mind that these gifts may actually backfire tax-wise in some cases. For example, a gift might make a student ineligible for college financial aid, or the earnings from the gift might trigger tax on a senior recipient’s Social Security benefits.

Make gifts to trusts. These gifts often qualify for the annual exclusion ($14,000 in 2013) if the gift is direct and immediate. A gift that meets all the requirements removes the property from your estate. The annual exclusion gift can be contributed for each beneficiary of a trust. We are happy to review the details with your estate planning attorney.

Consider discounted gifts. These are gifts in which the value of the property for tax purposes is less than the current value of the property, usually because there are some restrictions or defects that reduce the value to the beneficiary. Discounted gifts can be made to trusts or other vehicles. Discounted values are often 20% or more.

A gift that exceeds the annual exclusion gift either reduces your lifetime gift/estate tax exemption or it is subject to current gift tax. If you make a taxable gift, the IRS requires a gift tax return to be filed so it can track the reduction in your lifetime gift/estate tax exemption and also track any lifetime gift taxes you might pay. You should consider filing a gift tax return even when one isn’t required in order to hold the IRS to the three-year statute of limitations (there is no statute of limitations when no return is filed, so the IRS can come back years or decades later, argue that the property was undervalued, and impose a lot of penalties and interest on you or your estate). The gift tax return is IRS Form 709 which is available with instructions for free at www.irs.gov.

Conclusion

Are you having trouble keeping up with changes in the tax laws? In April 2011, IRS commissioner Shaulmen reported that there have been about 3,500 tax law changes since the year 2000. Remember, it was Albert Einstein that said, “The hardest thing in the world to understand is the income tax.” He said that way before it became a whopping 25-volume edition with over 70,320 pages.

Here are some numbers directly from the IRS; the average taxpayer who files an IRS Form 1040 needs about 23 hours to prepare the return. America spends more than 7.6 billion hours and over $193 billion each year just to figure out what taxes we owe—more than the hours used to build every car, van, truck and airplane manufactured in America.

One of our primary goals is to keep clients aware of tax law changes and updates. This report is not a substitute for using a tax professional. Please note that many states do not follow the same rules and computations as the federal income tax rules. Make sure you check with your tax preparer to see what tax rates and rules apply for your particular state.

There are many other additional tax reduction strategies that will vary depending on your financial picture. We encourage all of our clients and prospects to come in so that we can review your particular situation and hopefully take advantage of those tax rules that apply to you. We look forward to seeing you soon.