Financial Education

Our advisors share their insights and experience on a wide range of financial topics.

Annuities and Retirement Planning

You may have heard that IRAs and employer-sponsored plans (e.g., 401(k)s) are the best ways to invest for retirement. That’s true for many people, but what if you’ve maxed out your contributions to those accounts and want to save more? An annuity may be a good investment to look into.

Get the lay of the land

An annuity is a tax-deferred insurance contract. The details on how it works vary, but here’s the general idea. You invest your money (either a lump sum or a series of contributions) with a life insurance company that sells annuities (the annuity issuer). The period when you are funding the annuity is known as the accumulation phase. In exchange for your investment, the annuity issuer promises to make payments to you or a named beneficiary at some point in the future. The period when you are receiving payments from the annuity is known as the distribution phase.

Chances are, you’ll start receiving payments after you retire. Annuities may be subject to certain charges and expenses, including mortality charges, surrender charges, administrative fees, and other charges.

Understand your payout options

Understanding your annuity payout options is very important. Keep in mind that payments are based on the claims-paying ability of the issuer. You want to be sure that the payments you receive will meet your income needs during retirement. Here are some of the most common payout options:

- You surrender the annuity and receive a lump-sum payment of all of the money you have accumulated.

- You receive payments from the annuity over a specific number of years, typically between 5 and 20. If you die before this “period certain” is up, your beneficiary will receive the remaining payments.

- You receive payments from the annuity for your entire lifetime. You can’t outlive the payments (no matter how long you live), but there will typically be no survivor payments after you die.

- You combine a lifetime annuity with a period certain annuity. This means that you receive payments for the longer of your lifetime or the time period chosen. Again, if you die before the period certain is up, your beneficiary will receive the remaining payments.

- You elect a joint and survivor annuity so that payments last for the combined life of you and another person, usually your spouse. When one of you dies, the survivor receives payments for the rest of his or her life.

When you surrender the annuity for a lump sum, your tax bill on the investment earnings will be due all in one year. The other options on this list provide you with a guaranteed stream of income (subject to the claims-paying ability of the issuer). They’re known as annuitization options because you’ve elected to spread payments over a period of years.

Part of each payment is a return of your principal investment. The other part is taxable investment earnings. You typically receive payments at regular intervals throughout the year (usually monthly, but sometimes quarterly or yearly). The amount of each payment depends on the amount of your principal investment, the particular type of annuity, your selected payout option, the length of the payout period, and your age if payments are to be made over your lifetime.

Consider the pros and cons

An annuity can often be a great addition to your retirement portfolio. Here are some reasons to consider investing in an annuity:

- Your investment earnings are tax deferred as long as they remain in the annuity. You don’t pay income tax on those earnings until they are paid out to you.

- An annuity may be free from the claims of your creditors in some states.

- If you die with an annuity, the annuity’s death benefit will pass to your beneficiary without having to go through probate.

- Your annuity can be a reliable source of retirement income, and you have some freedom to decide how you’ll receive that income.

- You don’t have to meet income tests or other criteria to invest in an annuity.

- You’re not subject to an annual contribution limit, unlike IRAs and employer-sponsored plans. You can contribute as much or as little as you like in any given year.

- You’re not required to start taking distributions from an annuity at age 70½ (the required minimum distribution age for IRAs and employer-sponsored plans). You can typically postpone payments until you need the income.

But annuities aren’t for everyone. Here are some potential drawbacks:

- Contributions to nonqualified annuities are made with after-tax dollars and are not tax deductible.

- Once you’ve elected to annuitize payments, you usually can’t change them, but there are some exceptions.

- You can take your money from an annuity before you start receiving payments, but your annuity issuer may impose a surrender charge if you withdraw your money within a certain number of years (e.g., seven) after your original investment.

- You may have to pay other costs when you invest in an annuity (e.g., annual fees, investment management fees, insurance expenses).

- You may be subject to a 10 percent federal penalty tax (in addition to any regular income tax) if you withdraw earnings from an annuity before age 59½, unless you meet one of the exceptions to this rule.

- Investment gains are taxed at ordinary income tax rates, not at the lower capital gains rate.

Choose the right type of annuity

If you think that an annuity is right for you, your next step is to decide which type of annuity. Overwhelmed by all of the annuity products on the market today? Don’t be. In fact, most annuities fit into a small handful of categories. Your choices basically revolve around two key questions.

First, how soon would you like annuity payments to begin? That probably depends on how close you are to retiring. If you’re near retirement or already retired, an immediate annuity may be your best bet. This type of annuity starts making payments to you shortly after you buy the annuity, typically within a year or less. But what if you’re younger, and retirement is still a long-term goal? Then you’re probably better off with a deferred annuity. As the name suggests, this type of annuity lets you postpone payments until a later time, even if that’s many years down the road.

Second, how would you like your money invested? With a fixed annuity, the annuity issuer determines an interest rate to credit to your investment account. An immediate fixed annuity guarantees a particular rate, and your payment amount never varies. A deferred fixed annuity guarantees your rate for a certain number of years; your rate then fluctuates from year to year as market interest rates change. A variable annuity, whether immediate or deferred, gives you more control and the chance to earn a better rate of return (although with a greater potential for gain comes a greater potential for loss of principal). You select your own investments from the subaccounts that the annuity issuer offers. Your payment amount will vary based on how your investments perform.

Note: Variable annuities are long-term investments suitable for retirement funding and are subject to market fluctuations and investment risk including the possibility of loss of principal. Variable annuities contain fees and charges including, but not limited to mortality and expense risk charges, sales and surrender (early withdrawal) charges, administrative fees and charges for optional benefits and riders.

Variable annuities are sold by prospectus. You should consider the investment objectives, risk, charges and expenses carefully before investing. The prospectus, which contains this and other information about the variable annuity, can be obtained from the insurance company issuing the variable annuity or from your financial professional. You should read the prospectus carefully before you invest.

Shop around

It pays to shop around for the right annuity. In fact, doing a little homework could save you hundreds of dollars a year or more. Why? Rates of return and costs can vary widely between different annuities. You’ll also want to shop around for a reputable, financially sound annuity issuer. There are firms that make a business of rating insurance companies based on their financial strength, investment performance, and other factors. Consider checking out these ratings.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Additional securities and investment advisory services offered through FSC Securities Corporation, Member FINRA/SIPC and a registered investment adviser. 9601 Tamiami Trail N., Naples, FL 34108, 239-262-6577

This message may contain confidential information and is intended for use only by the addressee(s) named on this transmission. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Saving for Retirement

Although most of us recognize the importance of sound retirement planning, few of us embrace the nitty-gritty work involved. With thousands of investment possibilities, complex rules governing retirement plans, and so on, most people don’t even know where to begin. Here are some suggestions to help you get started.

Although most of us recognize the importance of sound retirement planning, few of us embrace the nitty-gritty work involved. With thousands of investment possibilities, complex rules governing retirement plans, and so on, most people don’t even know where to begin. Here are some suggestions to help you get started.

Determine your retirement income needs

Some experts suggest that you need anywhere from 60% to 90% of your current income to enable you to maintain your current standard of living in retirement. But this is only a general guideline. To determine your specific needs, you may want to estimate your annual retirement expenses.

Use your current expenses as a starting point, but note that your expenses may change dramatically by the time you retire. If you’re nearing retirement, the gap between your current expenses and your retirement expenses may be small. If retirement is many years away, the gap may be significant, and projecting your future expenses may be more difficult.

Remember to take inflation into account. The average annual rate of inflation over the past 20 years has been approximately 2.3%. (Source: Calculated from consumer price index (CPI-U) data published by the U.S. Department of Labor in January 2015.) And keep in mind that your annual expenses may fluctuate throughout retirement.

For instance, if you own a home and are paying a mortgage, your expenses will drop if the mortgage is paid off by the time you retire. Other expenses, such as health-related expenses, may increase in your later retirement years. A realistic estimate of your expenses will tell you about how much annual income you’ll need to live comfortably.

Calculate the gap

Once you have estimated your retirement income needs, take stock of your estimated future assets and income. These may come from Social Security, a retirement plan at work, a part-time job, and other sources. If estimates show that your future assets and income will fall short of what you need, the rest will have to come from additional personal retirement savings.

Figure out how much you’ll need to save

By the time you retire, you’ll need a nest egg that will provide you with enough income to fill the gap left by your other income sources. But exactly how much is enough? The following questions may help you find the answer:

- At what age do you plan to retire? The younger you retire, the longer your retirement will be, and the more money you’ll need to carry you through it.

- What kind of lifestyle do you hope to maintain during your retirement years?

- What is your life expectancy? The longer you live, the more years of retirement you’ll have to fund.

- What rate of growth can you expect from your savings now and during retirement? Be conservative when projecting rates of return.

- Do you expect to dip into your principal? If so, you may deplete your savings faster than if you just live off investment earnings. Build in a cushion to guard against these risks.

Build your retirement fund: Save, save, save

When you know roughly how much money you’ll need, your next goal is to save that amount. First, you’ll have to map out a savings plan that works for you. Assume a conservative rate of return (which will depend on your risk tolerance), and then determine approximately how much you’ll need to save every year between now and your retirement to reach your goal.

The next step is to put your savings plan into action. It’s never too early to get started (ideally, begin saving in your 20s). To the extent possible, you may want to arrange to have certain amounts taken directly from your paycheck and automatically invested in accounts of your choice (e.g., 401(k) plans, payroll deduction savings). This arrangement reduces the risk of impulsive or unwise spending that will threaten your savings plan. If possible, save more than you think you’ll need to provide a cushion.

Use the right savings tools

Employer-sponsored retirement plans like 401(k)s and 403(b)s are powerful savings tools. Your contributions come out of your salary as pretax contributions (reducing your current taxable income) and any investment earnings grow tax deferred until withdrawn. Some 401(k), 403(b), and 457(b) plans also allow employees to make after-tax “Roth” contributions. There’s no up-front tax advantage, but qualified distributions are entirely free from federal income taxes. In addition, employer-sponsored plans often offer matching contributions, and may be your best option when it comes to saving for retirement.

IRAs also feature tax-deferred growth of earnings. If you are eligible, traditional IRAs may enable you to lower your current taxable income through deductible contributions. Withdrawals, however, are taxable as ordinary income (except to the extent you’ve made nondeductible contributions).

Roth IRAs don’t permit tax-deductible contributions but allow you to make completely tax-free withdrawals under certain conditions. With both types, you can typically choose from a wide range of investments to fund your IRA.

Annuities are generally funded with after-tax dollars, but their earnings grow tax deferred (you pay tax on the portion of distributions that represents earnings). There is also no annual limit on contributions to an annuity. However, withdrawals may be subject to surrender charges.

Note: Taxable distributions from retirement plans, IRAs, and annuities prior to age 59½ may be subject to an additional 10% penalty tax unless an exception applies.

Investment advisory services offered through Ciccarelli Advisory Services, Inc., a registered investment adviser independent of FSC Securities Corporation. Additional securities and investment advisory services offered through FSC Securities Corporation, Member FINRA / SIPC and a registered investment adviser. 9601 Tamiami Trail N., Naples, FL 34108, 239-262-6577

This message may contain confidential information and is intended for use only by the addressee(s) named on this transmission. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Women and Retirement

Women face special challenges when planning for retirement. Because their careers are often interrupted to care for children or elderly parents, women may spend less time in the workforce and earn less money than men in the same age group. As a result, their retirement plan balances, Social Security benefits, and pension benefits are often lower. In addition to earning less, women generally live longer than men, and they may face having to stretch limited retirement savings and benefits over many years.

To meet these financial challenges, you’ll need to make retirement planning a priority.

Begin saving now

To help improve your chances of achieving a financially comfortable retirement, start with a realistic assessment of how much you’ll need to save. If the figure is substantial, don’t be discouraged–the most important thing is to begin saving now. Although it’s never too late to save for retirement, the sooner you start, the more time your investments have to potentially grow.

The chart below shows how just $2,000 invested annually at a 6% rate of return might grow over time:

Note: This is a hypothetical example, and does not reflect the performance of any specific investment.

Save as much as you can–you have many options

If your employer offers a retirement savings plan, such as a 401(k) or a 403(b), join it as soon as possible and contribute as much as you can. It’s easy to save because your contributions are deducted directly from your pay, and some employers will even match a portion of what you contribute. If your employer offers a pension plan, find out how many years you’ll need to work for the company before you’re vested in, or own, your pension benefits.

Women struggling to balance work and family sometimes shortchange their retirement savings by leaving their jobs before they become vested in their pension benefits. Keep in mind, too, that because your pension benefits will be based on your earnings and on your years of service, the longer you stay with one employer, the higher your pension is likely to be.

Most employer-sponsored plans allow you to choose from several investment options (typically mutual funds). If you have many years to invest or you’re trying to make up for lost time, you may want to consider growth-oriented investments such as stocks and stock funds. Historically, stocks have outperformed bonds and short-term instruments over the long term, although past performance is no guarantee of future results. However, along with potentially higher returns, stocks carry more risk than less volatile investments.

A good way to get detailed information about a mutual fund you’re considering is to read the fund’s prospectus, which can be obtained from the fund company. It includes information about the fund’s objectives, expenses, risks, and past returns. A financial professional can also help you evaluate your retirement plan options.

Save for retirement–no matter what

Even if you’re staying at home to raise your family, you can–and should–continue to save for retirement. If you’re married and file your income taxes jointly, and otherwise qualify, you may open and contribute to a traditional or Roth IRA as long as your spouse has enough earned income to cover the contributions. Both types of IRAs allow you to make contributions of up to $5,500 in 2016 (unchanged from 2015), or, if less, 100% of taxable compensation. If you’re age 50 or older, you’re allowed to contribute even more—up to $6,500 in 2016 (unchanged from 2015).

Plan for income in retirement

Do you worry about outliving your retirement income? Unfortunately, that’s a realistic concern for many women. At age 65, women can expect to live, on average, an additional 20.5 years. In addition, many women will live into their 90s. This means that women should generally plan for a long retirement that will last at least 20 to 30 years.

Women should also consider the possibility of spending some of those years alone. According to recent statistics, 35% of older women are widowed, 14% are divorced, and almost half of all women age 75 and older live alone. For married women, the loss of a spouse can mean a significant decrease in retirement income from Social Security or pensions.

So what can you do to help ensure you’ll have enough income to last throughout retirement? Here are some tips:

- Estimate how much income you’ll need. Use your current expenses as a starting point, but note that your expenses may change by the time you retire.

- Find out how much you can expect to receive from Social Security, pension plans, and other sources. What benefits will you receive should you become widowed or divorced?

- Set a retirement savings goal that you can work toward, and keep track of your progress.

- Save regularly, save as much as you can, and then look for ways to save more–dedicate a portion of every raise, bonus, cash gift, or tax refund to your retirement savings.

- Consider how you can help protect yourself and your family from potentially substantial long-term care expenses. By planning ahead, you could help preserve your choices for care and may avoid becoming a burden on your family.

What’s your excuse for not planning for retirement?

I’m too busy to plan

Perhaps you’re so wrapped up in balancing your responsibilities that you haven’t given retirement planning much thought. That’s understandable, but if you don’t put retirement planning at the top of your to-do list, you risk shortchanging yourself later on. Staying focused on your goal of saving for a comfortable retirement is difficult, but if you put yourself first it could pay off in the end.

My husband takes care of our finances

Married or not, it’s critical for women to take an active role in planning for retirement. Otherwise, you may be forced to make important financial decisions quickly during a period of crisis. Unfortunately, decisions that are not well thought through often prove costly later. Preparing for retirement with your spouse could help ensure that you’re both provided for, and pave the way to a comfortable retirement.

I’ll save more once my children are through college

Many well-intentioned parents put their own retirement savings on hold while they save for their children’s college education. But if you do so, you’re potentially sacrificing your own financial well-being. Your children have many options when it comes to financing college–loans, grants, and scholarships, for example–but there’s no such thing as a retirement loan! Why not set a good example for your children by getting your own finances in order before contributing to their college fund?

I don’t know enough about investing

Commit to spending just a few minutes a day learning the basics of investing, to help you become knowledgeable. And remember, you don’t have to do it by yourself–a financial professional will be happy to work with you to set retirement goals and help you choose appropriate investments.

Sources: NCHS Data Brief, Number 178, December 2014; U.S. Department of Health and Human Services Administration on Aging, A Profile of Older Americans: 2014; United States Census, 2012 Survey of Business Owners (most current data available)

This message may contain confidential information and is intended for use only by the addressee(s) named on this transmission. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Preserving Your Digital Estate

In recent years, a new category of assets has appeared on the scene, which can be more complicated to pass on at someone’s death than stocks, bonds and cash. The list includes such valuable property as digital domain names, social media accounts, websites and blogs that you manage, and pretty much anything stored on the cloud.

In addition, if you were to die tomorrow, would your heirs know the passcodes to access your iPad or smartphone? Or, for that matter, your email account or the Amazon.com or iTunes shopping accounts you’ve set up? Would they know how to shut down your Facebook account, or would it live on after your death?

A service called Everplans has created a listing of these and other digital assets that you might consider in your estate plan, and recommends that you share your logins and passwords with a digital executor or heirs. If the account or asset has value (airline miles or hotel rewards programs, domain names) these should be transferred to specific heirs—and you can include these bequests in your will. Other assets should probably be shut down or discontinued, which means your digital executor should probably be a detail-oriented person with some technical familiarity.

The site also provides a guide to how to shut down accounts; click on “F,” select “Facebook,” and you’re taken to a site (https://www.everplans.com/articles/how-to-close-a-facebook-account-when-someone-dies) which tells you how to deactivate or delete the account. Note that each option requires the digital executor to be able to log into the site first; otherwise that person would have to submit your birth and death certificates and proof of authority under local law that he/she is your lawful representative. (The executor can also “memorialize” your account, which means freezing it from outside participation.)

The point here is that even if you know who’s would get your house and retirement assets if you were hit by a bus tomorrow, you could still be leaving a mess to your heirs unless you clean up your digital assets as well.

Sources: https://www.everplans.com/articles/a-helpful-overview-of-all-your-digital-property-and-digital-assets

https://www.everplans.com/articles/how-to-close-online-accounts-and-services-when-someone-dies

https://www.everplans.com/articles/digital-cheat-sheet-how-to-create-a-digital-estate-plan

Estate Tax Complexities

Years ago, the way to most efficiently save on estate taxes was to set up credit shelter trusts that would pour assets from one spouse to another when death occurred, so that both spouses would get the maximum estate tax exemption. In those simpler days, people who didn’t have to pay estate taxes didn’t have to file an estate tax return.

Today, we live in a very different world. No longer is a credit shelter trust necessary; the surviving spouse gets to keep the unused portion of the deceased spouse’s estate tax exemption regardless of who owns which assets at the time of death. And with the exemption up to $5.43 million per spouse, you would think that fewer people would have to file estate tax returns.

This last assumption would be wrong. In order to claim the portable exemption of the deceased spouse, the estate has to file Estate Tax Form 706 on behalf of the survivor. This form can be complicated; it requires the executor to report the value of the assets that don’t need to be reported for tax purposes, and to subtract that amount from the exemption—in order to calculate the exemption amount that the survivor can keep and use when he or she dies and passes on assets to heirs. So you still have to do an estate valuation.

If you know for sure that your future estate won’t exceed $5.43 million indexed for inflation, then there is no need to file an estate tax return. But when people factor in the (hopefully) appreciating value of their house, in addition to their retirement assets over the years they expect to live, a surprising number of people should opt to file the tax form.

There’s one other complication: although the surviving spouse’s exemption will keep rising with inflation, the portable amount stays fixed until it’s eventually used.

And one more: people who die with assets in their name get a step-up in cost basis on their investments—which basically means that the capital gains taxes that would otherwise be owed when those investments are sold will go away. So although it no longer matters, from an estate tax perspective, who owns which assets, it is beneficial for the deceased spouse to own assets that have a low cost basis—things like a home purchased many years ago, or stocks acquired before a large runup in value, or shares of a small business that started with zero value. But beware transfers on a spouse’s deathbed; if the deceased dies less than a year after the transfer, the tax code treats it as if the transfer were never made.

What? You expected the government to simplify your estate taxes?

Sources: http://www.bna.com/portability-regulations-offer-b12884910119/

http://www.forbes.com/sites/lewissaret/2014/01/07/estate-tax-portability-computing-the-dsue-amount/#ab866a57f1bc

Although the information has been gathered from sources believed to be reliable, it cannot be guaranteed. Federal tax laws are complex and subject to change. This information is not intended to be a substitute for specific individualized tax or legal advice. FSC Securities Corp. does not offer tax or legal advice. As with all matters of a tax or legal nature, you should consult with your tax or legal counsel for advice.

Perspective on Financial Security

Chances are, you know that it takes steady savings to accumulate wealth. A recent article in Business Insider actually calculated how much you’d have to invest each day in order to become a millionaire.

Suppose your investments earn an average 7% yearly return, and you want to have $1 million by the age of 65. At age 20, you’d have to invest just $9 a day to achieve your goal—which really makes you rethink the cost of a cappuccino grande and a bagel at Starbucks every morning (typically over $10). If you start at age 25, then 12 dollars a day would do the trick. At age 30, your required daily investment goes up to $18, and it stays manageable even at age 35: $27 a day.

Of course, the longer you wait, the more you’re going to have to save. At age 55, your required investment has risen to $189 a day. If you’ve waited that long, let’s hope you have an enormous income to help you catch up.

Source: http://www.businessinsider.com/save-this-much-to-become-a-millionaire-by-age-65-2016-2

There’s Still Time to Contribute to an IRA for 2015

There’s still time to make a regular IRA contribution for 2015! You have until your tax return due date (not including extensions) to contribute up to $5,500 for 2015 ($6,500 if you were age 50 by December 31, 2015). For most taxpayers, the contribution deadline for 2015 is April 18, 2016 (April 19, 2016, if you live in Maine or Massachusetts).

You can contribute to a traditional IRA, a Roth IRA, or both, as long as your total contributions don’t exceed the annual limit (or, if less, 100% of your earned income). You may also be able to contribute to an IRA for your spouse for 2015, even if your spouse didn’t have any 2015 income.

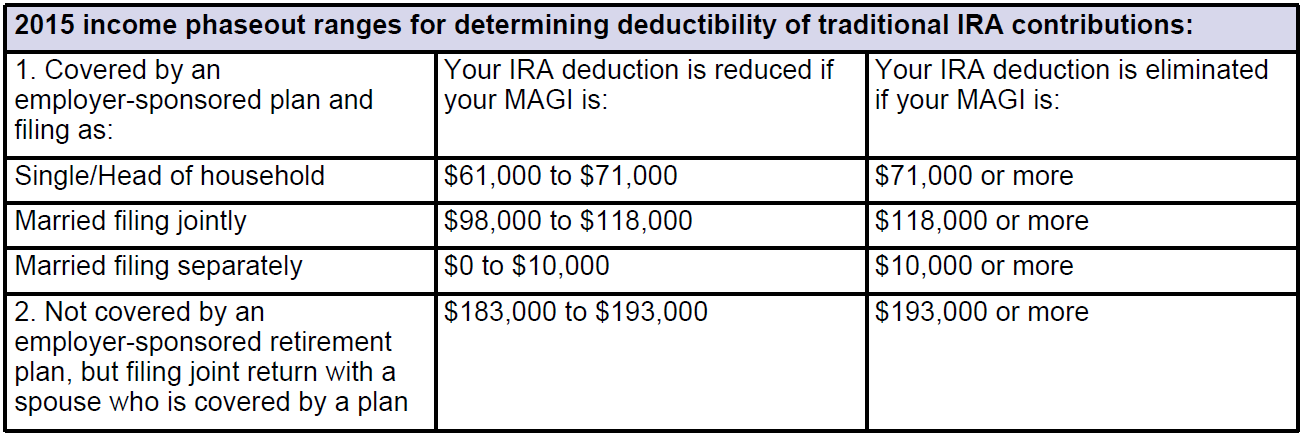

Traditional IRA

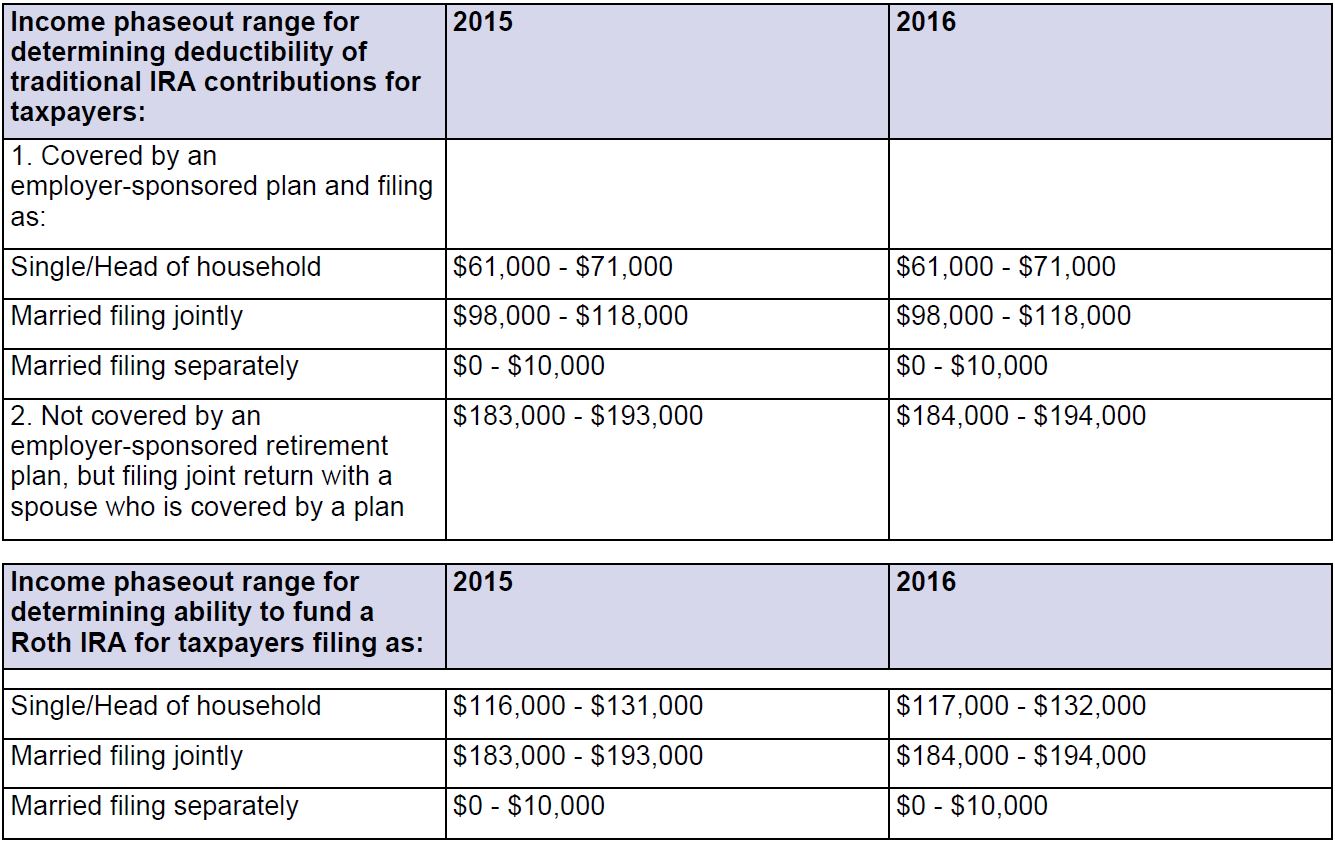

You can contribute to a traditional IRA for 2015 if you had taxable compensation and you were not age 70½ by December 31, 2015. However, if you or your spouse was covered by an employer-sponsored retirement plan in 2015, then your ability to deduct your contributions may be limited or eliminated depending on your filing status and your modified adjusted gross income (MAGI) (see table below). Even if you can’t deduct your traditional IRA contribution, you can always make nondeductible (after-tax) contributions to a traditional IRA, regardless of your income level. However, in most cases, if you’re eligible, you’ll be better off contributing to a Roth IRA instead of making nondeductible contributions to a traditional IRA.

Roth IRA

Roth IRA

You can contribute to a Roth IRA if your MAGI is within certain dollar limits (even if you’re 70½ or older). For 2015, if you file your federal tax return as single or head of household, you can make a full Roth contribution if your income is $116,000 or less. Your maximum contribution is phased out if your income is between $116,000 and $131,000, and you can’t contribute at all if your income is $131,000 or more. Similarly, if you’re married and file a joint federal tax return, you can make a full Roth contribution if your income is $183,000 or less. Your contribution is phased out if your income is between $183,000 and $193,000, and you can’t contribute at all if your income is $193,000 or more. And if you’re married filing separately, your contribution phases out with any income over $0, and you can’t contribute at all if your income is $10,000 or more.

Even if you can’t make an annual contribution to a Roth IRA because of the income limits, there’s an easy workaround. If you haven’t yet reached age 70½, you can simply make a nondeductible contribution to a traditional IRA, and then immediately convert that traditional IRA to a Roth IRA. Keep in mind, however, that you’ll need to aggregate all traditional IRAs and SEP/SIMPLE IRAs you own–other than IRAs you’ve inherited–when you calculate the taxable portion of your conversion. (This is sometimes called a “back-door” Roth IRA.)

Finally, keep in mind that if you make a contribution to a Roth IRA for 2015–no matter how small–by your tax return due date, and this is your first Roth IRA contribution, your five-year holding period for identifying qualified distributions from all your Roth IRAs (other than inherited accounts) will start on January 1, 2015.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The

information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

New Legislation Makes Many Tax Provisions Permanent

The Protecting Americans from Tax Hikes (PATH) Act of 2015

The Protecting Americans from Tax Hikes (PATH) Act of 2015

In one of its final actions for calendar year 2015, Congress passed the Consolidated Appropriations Act, 2016, a massive spending bill that will keep the federal government funded for fiscal year 2016. Signed into law on December 18, 2015, the legislation includes the Protecting Americans from Tax Hikes (PATH) Act of 2015 (Division Q of the Consolidated Appropriations Act), which addresses a host of popular but temporary tax provisions–commonly referred to as “tax extenders”–that had expired at the end of 2014, making many of them permanent. Some of the major provisions addressed are listed below.

Individuals

- American Opportunity Tax Credit

The American Opportunity Tax Credit (a modified version of the original Hope Credit) and the credit rules–including maximum credit amount, number of years of education covered, income phaseout ranges, and refundability provisions–are made permanent. - Child tax credit

The lower $3,000 earned income threshold for determining the refundable portion of the tax credit is made permanent (if the credit exceeds tax liability, an amount equal to 15% of earned income over $3,000 may be refunded). - Credit for nonbusiness energy property

The credit is extended for two additional years (through 2016); lifetime cap of $500 remains. - Deduction for classroom expenses paid by educators

The $250 above-the-line deduction is made permanent–the rules that applied in 2014 are retroactively extended for 2015; starting in 2016, the limit will be indexed for inflation, and qualifying professional development expenses will be considered eligible expenses for purposes of the deduction. - Deduction for qualified higher-education expenses

The above-the-line deduction, worth up to $4,000, is reinstated for 2015 and extended through 2016. - Deduction for state and local general sales taxes

Individuals who itemize deductions on Schedule A of IRS Form 1040 can elect to deduct state and local general sales taxes in lieu of the deduction for state and local income taxes–this is made permanent. - Discharge of qualified personal residence debt

The exclusion from gross income of the discharge of debt associated with a qualified principal residence is reinstated for 2015 and extended through 2016. - Earned income tax credit

The increased credit percentage for families with three or more qualifying children and the increased threshold phaseout range for married couples filing joint returns are made permanent. - Employer-provided mass transit benefits

The monthly exclusion for employer-provided transit pass and vanpool benefits will be permanently set to the same level as the exclusion for employer-provided parking (applies retroactively to 2015, increasing the exclusion from $130 to $250 monthly). - Mortgage insurance premiums

The provision allowing premiums paid for qualified mortgage insurance to be treated as deductible qualified residence interest on Schedule A of IRS Form 1040 (subject to phaseout based on income) is extended for two additional years, through 2016. - Qualified charitable distributions (QCDs)

The provision allowing individuals age 70½ or older to make qualified charitable distributions (QCDs) from their IRAs, and exclude the distribution from gross income (up to $100,000 in a year), is made permanent. - Qualified conservation contributions of capital gain real property

Special rules for qualified conservation contributions of capital gain real property are made permanent; new rules for qualified contributions by certain Alaska Native Corporations are added for years after 2015.

Businesses

- Bonus depreciation

Additional 50% bonus depreciation is reinstated for 2015 and extended through 2019; the bonus percentage is reduced to 40% in 2018 and 30% in 2019 for most property types. - Exclusion of gain on qualified small business stock

The 100% exclusion of capital gain from sale or exchange of qualified small business stock held for more than 5 years is made permanent; it applies to alternative minimum tax as well as regular income tax. - IRC Section 179 expensing

Increased dollar amounts ($500,000/$2,000,000) associated with Section 179 expensing are made permanent and indexed for inflation after 2015; $250,000 limit on qualified real property eliminated after 2015. - Research credit

The research tax credit is made permanent, with new provisions effective in tax years beginning after 2015 that will provide additional benefits to some small businesses. - Work Opportunity Tax Credit

The tax credit is extended through 2019 and expanded (after 2015) to apply to employers who hire qualified long-term unemployment recipients.

Other changes

In addition to the tax extender provisions, the Consolidated Appropriations Act contains multiple other tax provisions, including:

- The Act delays imposition of the excise tax on high-cost employer-sponsored health coverage (the so-called “Cadillac tax”) for two years; the tax, originally scheduled to take effect after 2017, will now be effective for tax years beginning after December 31, 2019.

- The Act eliminates the requirement that ABLE accounts (tax-favored savings vehicles intended to benefit disabled individuals) be established only in the ABLE account owner’s state of residence.

- Rules relating to 529 plans are modified for tax years after 2014, including expansion of the definition of qualified expenses to include the purchase of a computer, peripheral equipment, computer software, and Internet access if used primarily by the beneficiary while enrolled at an eligible education institution.

- The Act permits funds to be rolled over to a SIMPLE IRA from employer-sponsored retirement plans and traditional IRAs once a participant has participated in the SIMPLE IRA for a two-year period (effective for rollover contributions made after December 18, 2015).

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

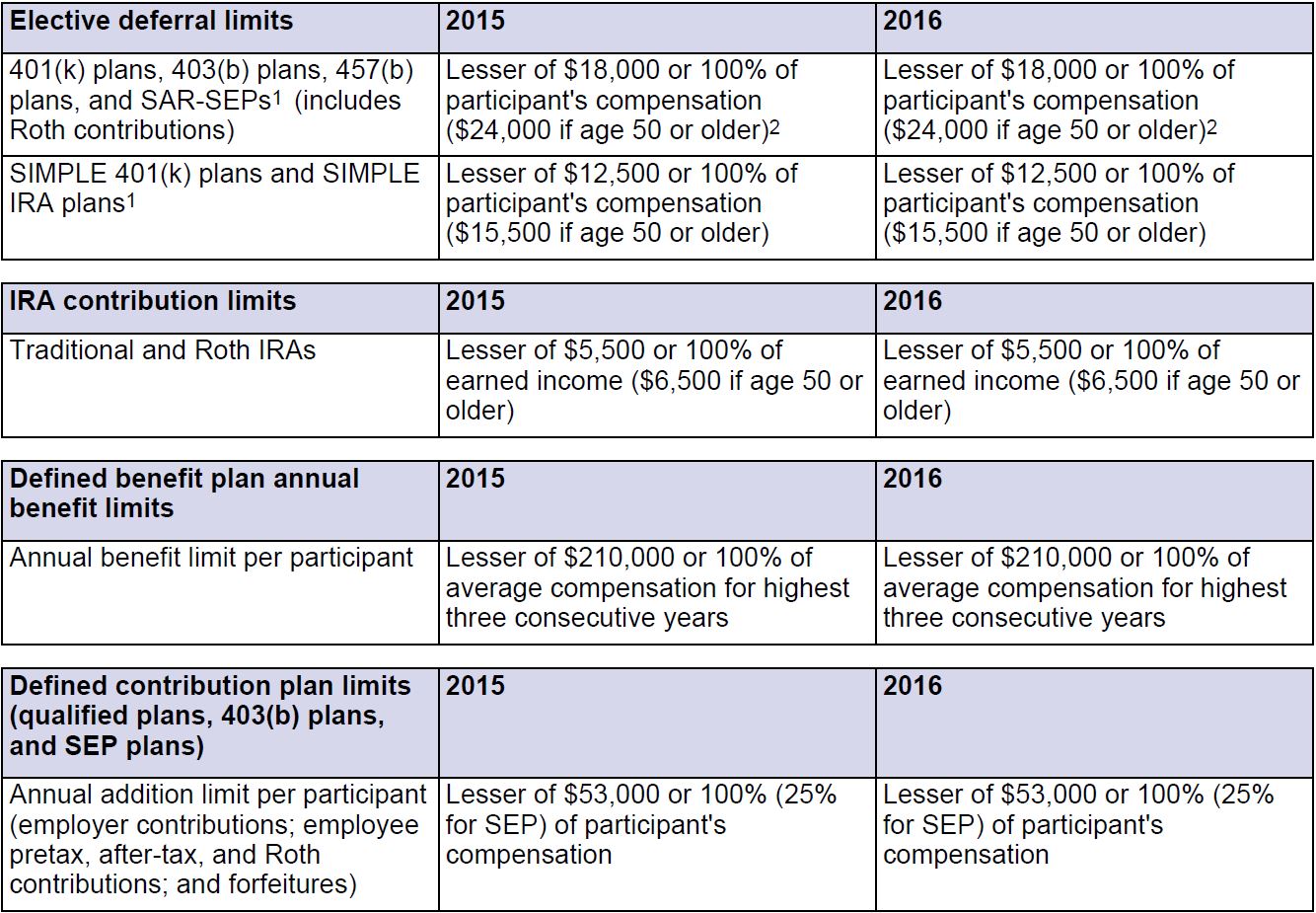

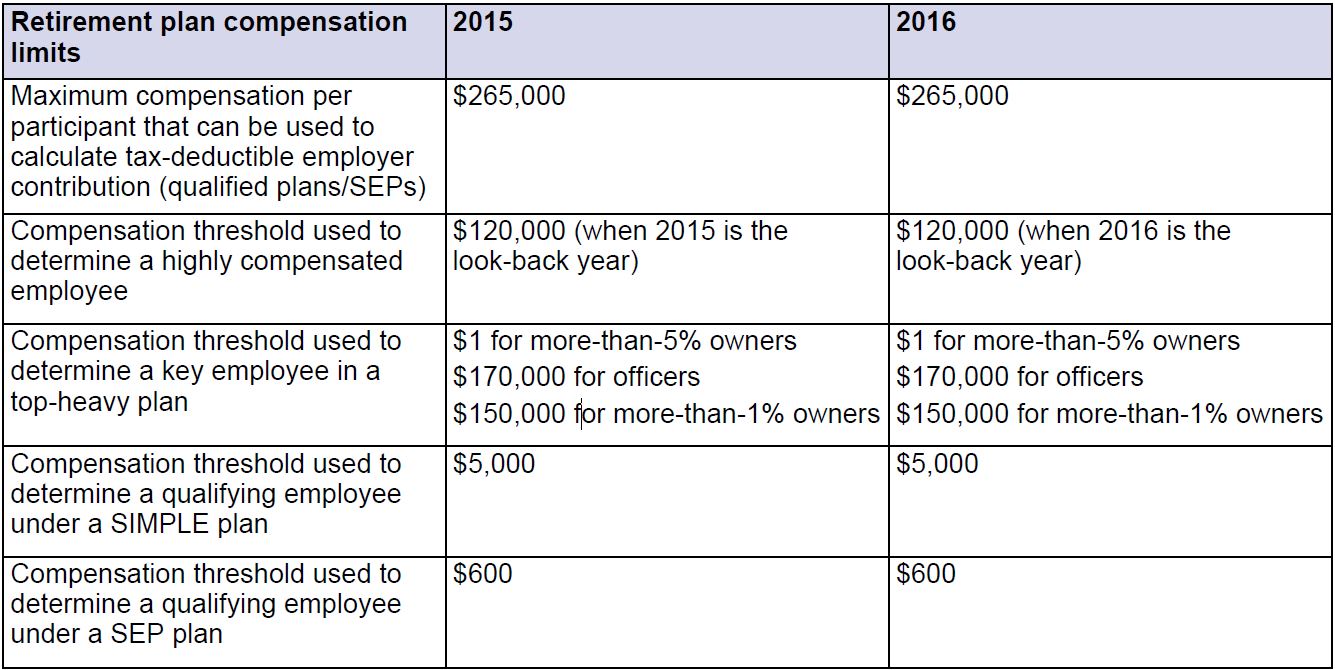

Retirement Planning Key Numbers

Certain retirement plan and IRA limits are indexed for inflation each year, but only a few of the limits eligible for a cost-of-living adjustment (COLA) have increased for 2016. Some of the key numbers for 2016 are listed below, with the corresponding limit for 2015. (The source for these 2016 numbers is IRS Information Release IR-2015-118.)

1 Must aggregate employee deferrals to all 401(k), 403(b), SAR-SEP, and SIMPLE plans of all employers; 457(b) contributions are not aggregated. For SAR-SEPs, the percentage limit is 25% of compensation reduced by elective deferrals (effectively a 20% maximum contribution).

2 Special catch-up limits may also apply to 403(b) and 457(b) plan participants.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Five Questions and Answers About New Social Security Claiming Rules

When Congress unexpectedly eliminated two Social Security claiming strategies as part of the Bipartisan Budget Act of 2015, retirement planning got a little more complicated for people who expected to use those strategies to boost their retirement income. Here are some questions and answers that could help if you are wondering how the new rules might affect you.

When Congress unexpectedly eliminated two Social Security claiming strategies as part of the Bipartisan Budget Act of 2015, retirement planning got a little more complicated for people who expected to use those strategies to boost their retirement income. Here are some questions and answers that could help if you are wondering how the new rules might affect you.

What’s Changing?

The provision of the budget bill called “Closure of Unintended Loopholes” primarily addresses two Social Security claiming strategies that have become increasingly popular over the last several years. These two strategies, known as “file and suspend” and “restricted application for a spousal benefit,” have often been used to increase cumulative Social Security income for married couples. The budget bill has eliminated those strategies for most future retirees, but you may still have time to take advantage of them, depending on your age.

File and Suspend

Under the old rules, an individual who had reached full retirement age could file for retired worker benefits in order to allow a spouse or dependent child to file for a spousal or dependent benefit. The individual could then suspend the retired worker benefit in order to accrue delayed retirement credits and claim an increased worker benefit at a later date, up to age 70. For some couples and families, this strategy increased their total lifetime combined benefit.

Under the new rules, effective for suspension requests submitted on or after April 30, 2016 (or later if the Social Security Administration provides additional guidance), the worker can file and suspend and accrue delayed retirement credits, but no one can collect benefits on the worker’s earnings record during the suspension period, effectively ending the file-and-suspend strategy for couples and families. The new rules also mean that a worker who files and suspends can no longer request a lump-sum payment in lieu of receiving delayed retirement credits for the period during which benefits were suspended. (This previously available option was helpful to someone who faced a change of circumstances, such as a serious illness.)

Restricted Application

Under the old rules, a married individual who had reached full retirement age could file a “restricted application” for spousal benefits after the other spouse had filed for retired worker benefits. This allowed the individual to collect spousal benefits while delaying filing for his or her own benefit, in order to accrue delayed retirement credits.

Under the new rules, an individual born in 1954 or later who files a benefit application will be deemed to have filed for both worker and spousal benefits, and will receive whichever benefit is higher. He or she will no longer be able to file only for spousal benefits.

The Bottom Line

A limited window still exists to take advantage of these two claiming strategies. If you are currently at least age 66 or will be by April 30, 2016, you may be able to use the file-and-suspend strategy to allow your eligible spouse or dependent child to file for benefits, while also increasing your future benefit. To file a restricted application and claim only spousal benefits at age 66, you must be at least age 62 by the end of December 2015. At the time you file, your spouse must have already claimed Social Security retirement benefits or filed and suspended benefits before the effective date of the new rules.

Why Did Congress Act Now?

Both the file-and-suspend and the restricted application strategies were made possible by the Senior Citizens Freedom to Work Act of 2000. Part of this Act’s original intent was to enable individuals to change their minds in the event they determined that they wanted to work longer but were already receiving Social Security retirement benefits. However, this opened up some claiming strategies, that while legal, went beyond the original intent of the legislation. Congress used the budget bill to close these loopholes in order to save money and slightly reduce the long-range actuarial deficit faced by the Social Security trust funds.

What if You’re Already Using One of These Strategies?

If you are already using the file-and-suspend or the restricted application strategy, you will not be affected by the new rules. You have already met the age requirements.

How Are Benefits for Surviving Spouses Affected?

Rules affecting surviving spouses have not changed. If you are eligible for both a survivor benefit and a retirement benefit based on your own earnings record, you can still opt to receive one benefit first, then switch to the other higher benefit later.

What Planning Opportunities Still Exist?

Even if you can no longer take advantage of the file-and-suspend and restricted application strategies, you may still benefit from considering your Social Security filing options. The age when you begin receiving Social Security benefits can significantly affect your retirement income and income that is available to your survivors.

Basic options for claiming Social Security remain unchanged. Currently, the earliest age at which you can receive Social Security retirement benefits is 62, but if you choose to take benefits before your full retirement age (66 to 67, depending on the year you were born), your benefit will be permanently reduced by as much as 30%. On the other hand, if you delay receiving Social Security benefits past your full retirement age, you’ll receive delayed retirement credits, which will increase your benefit by 8% for each year you delay, up to age 70.

Determining when to file for Social Security benefits is one of the biggest financial decisions you’ll need to make as you approach retirement. There’s no “one-size-fits-all” answer–it’s an individual decision that must be based on many factors, including other sources of retirement income, whether you plan to continue working, how many years you expect to spend in retirement, and your income tax situation. It’s especially complicated when you’re married because you and your spouse will need to plan together, taking into account the Social Security benefits you each may be entitled to, including survivor benefits.

Although some claiming options are going away, plenty of planning opportunities remain, and you may benefit from taking the time to make an informed decision about when to file for Social Security.