Financial Education

Our advisors share their insights and experience on a wide range of financial topics.

IRA and Retirement Plan Limits for 2015

Forbes Lists Naples, FL at Top of Best Cities for Future Job Growth

Economic Growth has now returned to the Sunshine State… Naples, FL was recently ranked as the #1 city in the United States for job growth over the next three years. Austin, Texas finished second and two other Florida cities also ranked in the Top 10 (Cape Coral and Port St. Lucie). Expected Naples job growth is projected to be about 4.1% annually over the next three years- primarily in the healthcare, retail, leisure, and hospitality sectors.

Economic Growth has now returned to the Sunshine State… Naples, FL was recently ranked as the #1 city in the United States for job growth over the next three years. Austin, Texas finished second and two other Florida cities also ranked in the Top 10 (Cape Coral and Port St. Lucie). Expected Naples job growth is projected to be about 4.1% annually over the next three years- primarily in the healthcare, retail, leisure, and hospitality sectors.

According to a recent article published on www.Forbes.com, Florida added retail jobs at the fastest rate of any state in 2013 and Naples was the top ranked market in Florida. The study was conducted by Moody’s Analytics where they looked at the 200 largest metro areas in the country and their projected growth rates through the year 2016.

When the financial/real estate crisis hit the country back in 2007-2008, home prices in Florida nosedived, foreclosures and short-sales climbed, and unemployment skyrocketed to 11.4% across the state of Florida. Naples unemployment peaked at 12.2% in January 2010, it has since dropped to 5.4% in June of 2014. A majority of the growth is attributed to stock market gains which is fueling spending on construction, tourism, and consumer goods in the area.

Other cities that made the Top 10 list included the Texas cities of Dallas, Houston, San Antonio, and McAllen- along with Greeley, CO and Raleigh, NC. All are expected to have annual job growth of at least 3.5%.1

1“Naples, Austin Head List of Best Cities for Job Growth”, www.Forbes.com, by Kurt Badenhausen, July 23, 2014

Listed entities are not affiliated with FSC Securities Corporation.

Use Your Annuity to Pay for Long-Term Care Insurance

The cost of long-term care can quickly deplete your savings and affect the quality of life for you and your family. Long-term care insurance allows you to share that cost with an insurance company. But premiums for long-term care insurance can be expensive, and cash or income to cover those premiums may not be readily available. One option is to exchange your annuity contract for a long-term care insurance policy.

Section 1035 exchange

Generally, withdrawals from a nonqualified deferred annuity (premiums paid with after-tax dollars) are considered to come first from earnings, then from your investment (premiums paid) in the contract. The earnings portion of the withdrawal is treated as income to the annuity owner, subject to ordinary income taxes. IRC Section 1035 allows you to exchange one annuity for another without any immediate tax consequences, as long as certain requirements are met. However, prior to 2010, an annuity couldn’t be exchanged for a long-term care insurance policy on a tax-free basis. But the Pension Protection Act (PPA) changed that and, as of January 1, 2010, both life insurance and annuities may be exchanged, tax free, for qualified long-term care insurance.

Generally, to be considered a tax-free exchange rather than a taxable surrender, you cannot receive the annuity proceeds directly–the proceeds from the annuity must be paid directly to the long-term care insurance company. Also, Section 1035 applies only if both the annuity contract and the long-term care insurance policy are owned by the same person or persons.

Conditions for tax-free exchange

In order for the transfer of the annuity to the long-term care insurance policy to be treated as a tax-free exchange, certain conditions must be met:

- The annuity must be nonqualified, meaning it cannot be part of an employer-sponsored retirement plan. For example, a tax-sheltered annuity or an annuity used to fund an IRA would not qualify for tax-free exchange treatment.

- The long-term care insurance policy must meet the requirements of the Health Insurance Portability and Accountability Act (HIPPA) and IRS criteria. Generally, the long-term care insurance policy must provide coverage only for qualified long-term care services; it must be guaranteed renewable; it cannot have a cash surrender value; refunds or dividends can only be used to reduce future premiums; and policy benefits cannot pay for expenses covered by Medicare (except where Medicare is a secondary payee).

- The exchange must be made directly from the annuity issuer to the long-term care insurance company. You will not receive tax-free treatment if you withdraw funds from the annuity directly, then use them to pay the long-term care insurance premium.

Presuming these criteria are met, exchanging an annuity for a long-term care policy can be done in one of two ways: a full transfer of the entire cash surrender value of the annuity in exchange for the long-term care insurance policy; or partial exchanges of the annuity’s cash value for the long-term care policy. Not all insurance companies allow long-term care policies to be funded with a single, lump-sum payment, so the more common approach may be to pay long-term care insurance premiums through several partial exchanges from the annuity.

Potential tax advantages

Exchanging your nonqualified deferred annuity for a long-term care insurance policy may have several tax-related advantages. You can use annuity earnings to pay for long-term care insurance without paying income tax on those earnings. This allows you to use otherwise taxable annuity earnings in a more tax-efficient manner.

According to the IRS, Section 1035 exchanges from a nonqualified annuity to pay for tax-qualified long-term care insurance are pro-rated based on the comparative percentages of principal and earnings in the annuity. For example, say you have a nonqualified annuity worth $100,000, which includes your premium of $50,000, plus earnings worth $50,000, and you haven’t taken any previous withdrawals. You direct the annuity issuer to send $2,500 to the long-term care insurance carrier as a partial exchange to pay for insurance premiums. Your annuity cash value is reduced by $2,500, but half of that amount ($1,250) comes from earnings. As a result, not only have you withdrawn annuity earnings ($1,250) without paying taxes on them, but you have further reduced the taxable portion of your annuity by $1,250. By withdrawing earnings from your annuity to pay for long-term care insurance, you could reduce the taxable portion of your annuity, which can be important if you surrender the annuity later.

Another advantage relates to the long-term care insurance policy. Generally, a qualified long-term care insurance policy is treated as an accident and health insurance contract, and the benefits are typically treated as tax free, subject to certain limits. In this way, you may be able to use tax-free annuity earnings to pay for tax-free long-term care benefits.

Other possible benefits

Generally, IRC Section 1035 allows tax-free exchanges in the following circumstances:

•An annuity contract for an annuity contract

•A life insurance policy for an annuity contract

•An endowment contract for an annuity contract

•A life insurance policy for a life insurance contract

•A life insurance policy for an endowment contract

•An endowment policy for an endowment contract (with special requirements)

•A life insurance policy, endowment contract, annuity, or qualified long-term care policy for a qualified long-term care contract

Aside from the favorable tax treatment, there may be other benefits as well.

- Using an annuity to pay for long-term care insurance may lessen the need to tap other savings or income to pay for premiums.

- You may still use any remaining cash surrender value of the annuity for other income needs or expenses.

- Exchanging the annuity for long-term care insurance may better meet your current needs, financial situation, and preferences.

Some potential disadvantages

There are also some potential disadvantages to exchanging an annuity for long-term care insurance.

- Annuity surrender charges might be incurred on the exchange of the annuity, thus reducing the annuity’s value.

- Reducing the annuity’s value to pay for long-term care insurance premiums may reduce your ability to use the annuity to provide income needed in the future.

- Some nonqualified deferred annuities might not be eligible for a partial Section 1035 exchange because the annuity contracts may not allow annuity payments to be made to other than the annuity owner (e.g., annuity payments cannot be assigned to another payee).

- If you exchange the annuity for a long-term care insurance policy, your survivors won’t have the annuity’s cash value for income or savings that otherwise would have been available at your death.

- Generally, premiums for qualified long-term care insurance are deductible as qualified medical expenses subject to certain restrictions. The tax savings of using a tax-free Section 1035 exchange needs to be compared to available federal or state income tax deductions for long-term care insurance premiums. Depending on your situation, it might be more beneficial to deduct premiums and include annuity earnings as taxable income.

Frequently asked questions

If I am the sole owner of the annuity, can I exchange it for a long-term care insurance policy jointly owned by my spouse and me?

Generally, no, because the owners of both the annuity and the long-term care insurance policy must be the same. However, you may be able to change the ownership of your annuity to include your spouse. While changing ownership of an annuity is generally treated as a taxable event to the extent of gain (earnings) in the annuity, ownership changes between spouses are typically tax free, but be sure to consult your tax or financial professional before making ownership changes to your annuity.

I’m receiving payments from a non-qualified immediate annuity. Can I exchange these payments for long-term care insurance?

You may be able to assign the payments directly to the long-term care insurance company as a 1035 exchange, but the annuity payee must be the long-term care insurance company–if you’re listed as the payee, payments will not receive tax-free treatment. Also, be aware that if long-term care insurance premiums increase, the annuity payments may not be sufficient to cover the cost of the long-term care insurance premiums. Also, if the annuity payment exceeds the insurance premium, you may be able to split the annuity payment, where an amount equal to the insurance premium is sent to the long-term care insurance company and the balance of the annuity payment is sent to you, but this would be at the discretion of the annuity issuer.

Can I use more than one annuity to pay for long-term care insurance?

Generally, yes, because funds from one or more non-qualified annuities can be exchanged for a long-term care insurance policy.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

The 2014 Social Security Trustees Report: What Does the Future Hold?

On July 28, The Boards of Trustees for Medicare also issued their 2014 annual report on the current and future financial health of the Medicare program. The financial projections in their report indicate that even though the trust fund that finances Medicare’s hospital insurance coverage will remain solvent until 2030 (four years beyond last year’s projection), steps need to be taken to address Medicare’s financial challenges. To read this report, visit www.cms.gov.

Every year, the Trustees of the Social Security Trust Funds release a report to Congress on the current financial condition and projected financial outlook of the program. This year’s report, released on July 28, contains valuable information about the health of Social Security that may help you understand how your Social Security benefits might be affected.

What are the Social Security Trust Funds?

The Social Security program consists of two parts. Retired workers, their families, and survivors of workers receive monthly benefits under the Old-Age and Survivors Insurance (OASI) program; disabled workers and their families receive monthly benefits under the Disability Insurance (DI) program. The combined programs are referred to as OASDI. Each program has a financial account (a trust fund) that holds the Social Security payroll taxes that are collected to pay Social Security benefits. Other income (reimbursements from the General Fund of the Treasury and income tax revenue from benefit taxation) is also deposited in these accounts. Money that is not needed in the current year to pay benefits and administrative costs is invested (by law) in special Treasury bonds that are guaranteed by the U.S. government and earn interest. As a result, the Social Security Trust Funds have built up reserves that can be used to cover benefit obligations if payroll tax income is insufficient to pay full benefits.

What are some highlights from this year’s report?

This year’s Trustees report projects that the OASI Trust Fund and the DI Trust Fund will have sufficient reserves to pay full benefits on a timely basis until 2034 and 2016, respectively. The combined trust fund reserves (OASDI) are still increasing and will continue to do so through 2019. Beginning in 2020, annual costs will exceed total income, and the U.S. Treasury will need to redeem trust fund asset reserves. The combined trust fund reserves will be depleted in 2033 if Congress does not act before then. This is the same year projected in last year’s report.

Once the combined trust fund reserves are depleted, payroll tax revenue alone should still be sufficient to pay about 77% of scheduled benefits. This means that 20 years from now, if no changes are made, beneficiaries may receive a benefit that is about 23% less than expected.

However, because the DI Trust Fund reserve is projected to be depleted in two years, legislative action is needed as soon as possible. Once the reserve is depleted, income to the fund will be sufficient to pay only 81% of DI benefits.

You can view the 2014 OASDI Trustees Report at www.ssa.gov.

Why is Social Security facing financial challenges?

Fewer workers are paying into the system, so payroll tax income is decreasing. When there are fewer payroll taxes coming into the system each year than benefits paid out, trust fund reserve assets have to be spent to make up the difference. The strain on the trust funds is worsening as large numbers of baby boomers reach retirement age and Americans live longer.

What is being done to address the financial challenges Social Security faces?

For years, the Trustees have been urging Congress to address the financial challenges in the near future, so that solutions will be less drastic and may be implemented gradually, lessening the impact on the public. As the conclusion to this year’s report states, “The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust to them. Implementing changes soon would allow more generations to share in the needed revenue increases or reductions in scheduled benefits. Social Security will play a critical role in the lives of 59 million beneficiaries and 165 million covered workers and their families in 2014. With informed discussion, creative thinking, and timely legislative action, Social Security can continue to protect future generations.”

Action needs to be taken very soon to address the DI program’s reserve depletion. According to this year’s report, in the short term, lawmakers may reallocate the payroll tax rate between OASI and DI (as they did in 1994). However, this may only serve to delay DI and OASI reforms. Members of Congress and the President support longer-term efforts to reform Social Security, but progress on the issue has been slow.

Some long-term reform proposals on the table are:

- Raising the current Social Security payroll tax rate (according to this year’s report, an immediate and permanent payroll tax increase of 2.83 percentage points would be necessary to address the revenue shortfall)

- Raising the ceiling on wages currently subject to Social Security payroll taxes ($117,000 in 2014)

- Raising the full retirement age beyond the currently scheduled age of 67 (for anyone born in 1960 or later)

- Reducing future benefits, especially for wealthier beneficiaries

- Changing the benefit formula that is used to calculate benefits

- Changing how the annual cost-of-living adjustment for benefits is calculated

What can you do in the meantime?

The financial outlook for Social Security depends on a number of demographic and economic assumptions that can change over time, so any action that might be taken and who might be affected are still unclear. But no matter what the future holds for Social Security, your financial future is still in your hands.

- Follow the news to learn about new developments or proposed legislation to reform Social Security

- Understand your own benefits, and what you’ll receive from Social Security based on current law

- Consider various income scenarios when planning for retirement

- Focus on saving as much for retirement as possible

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014

A View of Healthcare from Around the World

The United States health-care system has been impacted by the Affordable Care Act (ACA). But how does delivery of health care in the United States compare to that of other nations? And where does the United States rank with respect to the cost of health care per capita and as a percentage of gross domestic product?

The United States health-care system has been impacted by the Affordable Care Act (ACA). But how does delivery of health care in the United States compare to that of other nations? And where does the United States rank with respect to the cost of health care per capita and as a percentage of gross domestic product?

Types of health-care systems

While each country has its own system of health care, most health-care systems generally fall within the parameters of one of four models, with the health-care system of the United States consisting of aspects of each of these models.

The Beveridge Model.Countries such as the United Kingdom, Finland, Denmark, Spain, and Sweden generally follow this model, named after social reformer William Beveridge. Health care is deemed to be a right for each citizen and is provided by the government and financed primarily through taxes. Hospitals and clinics may be government owned, and medical staff, including doctors, may be government employees. Medical providers are paid by the government, which generally dictates treatments provided and the cost for services.

The Bismarck Model.The Bismarck Model requires that all citizens have health insurance. Health care is provided by private doctors and hospitals whose fees and charges are paid for by insurance. The insurance programs are nonprofit entities and must accept all applicants, including those with pre-existing medical conditions. Insurance is funded through employer and employee payroll taxes. Countries that use a form of the Bismarck Model include Germany, France, Belgium, the Netherlands, Japan, and Switzerland.

The National Health Insurance (NHI). Combining aspects of both the Beveridge and Bismarck Models, the NHI Model is used in several countries, with the most prominent being Canada. Health care is provided through private providers who are paid by government-run insurance. Citizens pay into the government insurance program primarily through taxes. As the sole payor, the government directly influences the cost of medical care and the services covered.

The Out-of-Pocket Model. Used by the majority of countries, including China, this model provides little or no government health care. Instead, those who can afford care get it and those who cannot pay for care generally do not receive care.

The United States Model.The United States incorporates all of these systems to varying degrees. Medicare is akin to the NHI Model; servicemembers and veterans receive health care similar to the Beveridge Model; and the ACA can be described as a type of Bismarck plan, although health insurers are typically for-profit entities.

Comparing the cost of health care*

The following information compares health-care expenditures of several countries as a percentage of gross domestic product as well as per capita.

*Information derived from The World Bank Health, Nutrition, and Population Data and Statistics (www.datatopics.worldbank.org)

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

Chart: Ten-Year History of U.S. Average Gasoline Prices

Gas prices fluctuated widely in 2008, peaking at a high of $4.11 during the second week of July, then plummeting to $1.81 by the first week of December. Since 2008, gasoline prices have generally been on an upswing, but have leveled off during the past three years, as this chart shows. According to the U.S. Energy Information Administration (EIA), average gasoline prices are even expected to decline slightly in 2015, although projections are far from certain.

Gas prices fluctuated widely in 2008, peaking at a high of $4.11 during the second week of July, then plummeting to $1.81 by the first week of December. Since 2008, gasoline prices have generally been on an upswing, but have leveled off during the past three years, as this chart shows. According to the U.S. Energy Information Administration (EIA), average gasoline prices are even expected to decline slightly in 2015, although projections are far from certain.

Sources: Short-Term Energy Outlook, May 6, 2014, U.S. Energy Information Administration, www.eia.gov; Chart data is from the EIA’s Weekly U.S. Regular Conventional Retail Gasoline Prices (chart shows average dollars per gallon as of the second week of May of each year).

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

Gas Prices: Why are you paying more at the pump?

Have you ever stood at the pump wondering why you’re paying so much to fill up your vehicle? The answer is … complicated. According to the U.S. Energy Information Administration (EIA), many factors contribute to the cost of a gallon of gasoline, including the price of crude oil (which accounts for the majority of the cost), refining costs and profits, taxes, and distribution and marketing expenses.

Have you ever stood at the pump wondering why you’re paying so much to fill up your vehicle? The answer is … complicated. According to the U.S. Energy Information Administration (EIA), many factors contribute to the cost of a gallon of gasoline, including the price of crude oil (which accounts for the majority of the cost), refining costs and profits, taxes, and distribution and marketing expenses.

The price of crude oil is dependent on global supply levels relative to demand, and can be influenced by political events in major oil-producing countries, supply disruptions (which often result from hurricanes and storms in supply zones), and market speculation. Supply and demand is also one of the reasons that U.S. gas prices tend to fluctuate seasonally, with prices generally rising in the spring and remaining higher in early summer. But refining costs also play a role. Prices tend to rise as refineries shift from winter to summer gasoline blends in order to meet federal and state environmental guidelines. Gasoline must be blended with other ingredients to reduce emissions, and costlier ingredients are used in the summer blend.

How much you pay for gasoline also depends on where the pump is located and who owns it. For example, prices are generally highest on the West Coast due to higher state taxes and transportation costs from distant refineries. But no matter where you live, you know that prices also vary locally from one station to the next. Why? Generally it’s because the cost of doing business for an individual station owner varies. The price the station pays for gasoline, the station’s location and volume of business, and whether it must match or beat prices from local competitors all contribute to how much you pay for a gallon of gas.

What’s the outlook for the future? The EIA expects the average price of gasoline to fall in 2015 to $3.39 per gallon. Despite the increasing demand from emerging economies, U.S. crude oil reserves and production are expected to increase, and U.S. demand is expected to decrease as vehicles become more fuel efficient.

Sources: “Factors Affecting Gasoline Prices” and “Short-Term Energy Outlook”, May 6, 2014, www.eia.gov

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

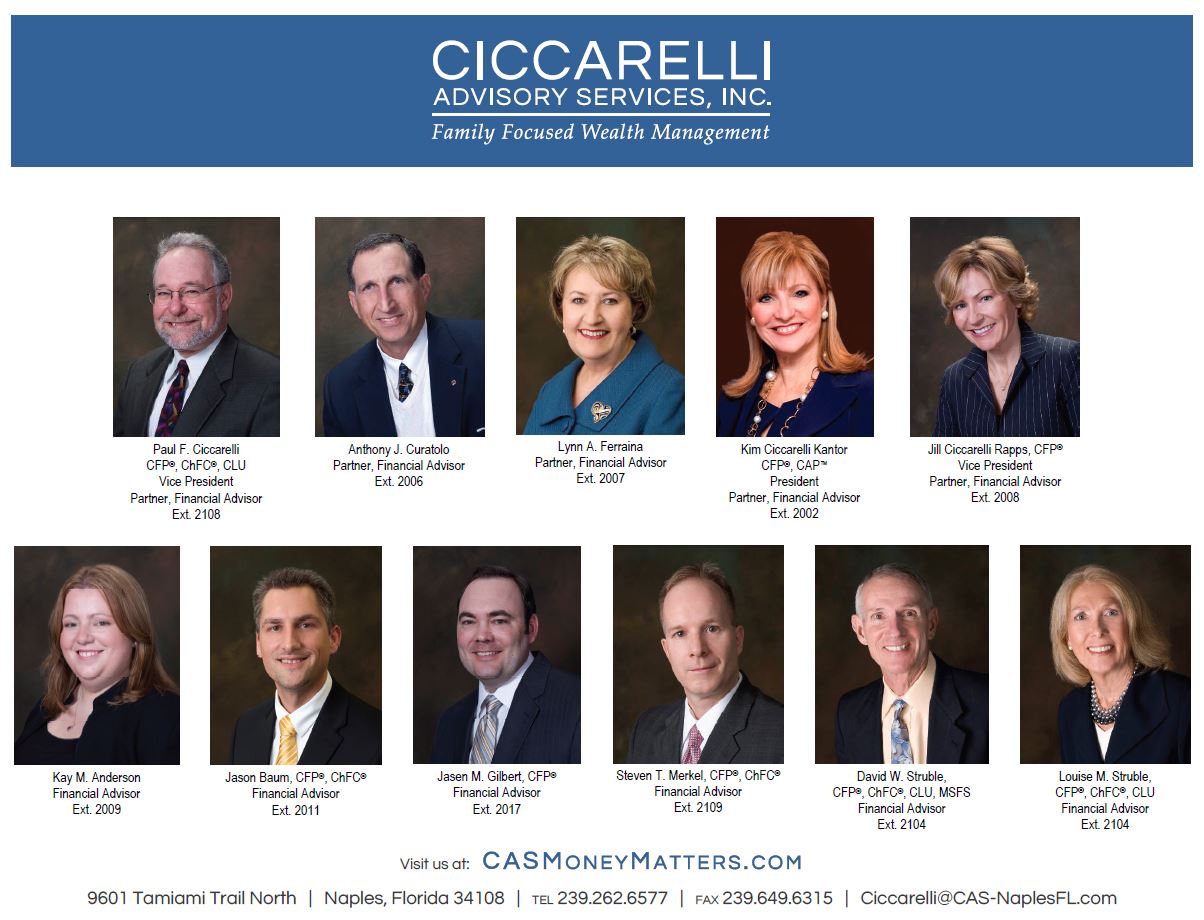

Updated Naples Staff Directory

Here’s a look at the people that make our Naples office run. The picture is a snippet of some of our staff. To see them all, click on the link below the photo and download it if you like.

Preparing a Strategic Plan

by Anthony J. Curatolo

by Anthony J. Curatolo

Two years ago I began working with noted psychologist Dr. Bill Beckwith who specializes in memory management for individuals affected with mild memory loss and dementia. During the course of our collaboration, I became aware of how a decline in memory such as mild cognitive impairment or Alzheimer disease affects not only the forgetful person but also the family as a whole.

Try to imagine the impact on family members when, what took a few minutes and little thought, such as reconciling your checking account, now takes hours and can possibly be riddled with numerous errors. If the decline becomes severe, think of what stress it would be if your parent, husband, wife or sibling did not recognize you. If would be a truly sad and empty experience.

Memory loss may come on suddenly, as in the case of a head injury, stroke, medication side effects, etc., or it may come on gradually and progressively as in the case of Alzheimer’s disease. The good news about slow onset memory loss changes is that you can be proactive in maintaining your quality of life. Just as in managing finances, managing memory loss early may improve outcome.

Through Dr. Beckwith, I learned that dementia can be misdiagnosed or made worse by loss of hearing, severe depression, medication side effects, or sleep apnea. The key is to identify a baseline and monitor short term memory just as you do blood pressure or blood sugars. To date, there are no medical or vitamin cures to prevent dementia, but one can slow the process with exercise, a healthy diet and social activities. In fact, Medicare covers memory evaluation through approved providers.

It is important to distinguish the difference between natural aging and progressive memory loss. For example, it’s normal to forget your keys or where you park your car, but it’s not normal to forget that you own a car.

How does the caretaker cope with a loved one‘s progressive memory loss? How does one better cope with a progressive chronic disease? Dr. Beckwith recommends the solution to managing your memory is to know how your memory works and then create a strategic plan for your future, rather than waiting until the memory loss is serious and detrimental. Realize that your daily calendar is your best tool. It allows you to control not only what you have to do but also what you love to do. Remember the one minute rule “anything given less than one minute of thought will fade from your memory” to quote Dr. Beckwith.

How does this relate to financial planning? It’s advised to develop a documented plan for a good life, no matter what circumstances may present themselves along the way. We suggest a Plan for a Lifetime report to assist you and your loved ones in helping you maintain a good life. This report should include:

- Account numbers of all investments and their values, along with company phone numbers and possible online credentials

- List of how assets are titled and taxed

- List of all insurance contracts inforce, along with company phone numbers

- Identify who the beneficiaries are

- Identify who will manage the assets if you are unable

- Identify who will be the executor and do they know the responsibilities that come with the position

- Identify who will be your care provider, if necessary

- List of trusted advisors (accountant, attorney, etc.) and their contact information

- Funeral and legacy arrangements

- Best friend or spiritual advisor

This report should also include a flow chart mapping how money is to be distributed to loved ones and a budget for your surviving spouse so there is continuity in their lifestyle.

A methodical and thoroughly thought out plan ensures your money is passed to family members as you desire. This flow chart is particularly important when divorce, step-children and or ex-spouses are involved.

Money has a habit of evaporating with poor communications, especially when health issues or second marriage families play into the scenario. The wall we must overcome is the “Code of Secrecy” which is more common than not. Unfortunately, many families do not share money behavior patterns among members, which can lead to chaos and confusion during a period of crisis. What is critically important is working with a trusted financial advisory team to develop a transparent and strategic document so that those who survive you are well aware of the financial and legacy plan you have worked to put in place. Engaging a loved one in your financial management responsibilities and on the building of this life-long plan is an important aspect of the process.

Don’t ignore this process. Involve members of your family; most importantly your spouse. Talk with your advisor and review all documents and plans. Have your accountant and attorney engaged in the process and have all trusted advisors on the same page in regards to major decision making issues.

Dementia /Alzheimer’s are more feared than death. Losing your memory does not mean that you must lose your best friends and family members. Communication and transparency are paramount to reducing anxiety, family disappointments and legal fees in the face of an uncertain future.

It is a good idea to constantly build and communicate to all trusted parties. You may even consider making a short video of your life to include your best lessons to pass along to the next generation and in which you can share your philosophy of financial and wealth management.

Begin preparing your Strategic Plan for a Lifetime today, while you have the capability. Should there ever be a period of crisis and you do not have the ability to perform or make the decisions you do today, you may find that this plan will be of great value to you and your loved ones.

Shutdown? Default? Consequences?

It’s possible that you’ve heard a news report or two about the government shutdown that started October 1, and now a dispute over raising the U.S. debt ceiling and possibly defaulting on the government’s debt obligations as soon as October 17. The question for an increasingly nervous investing public is: how will this affect the U.S. economy and (not to be too selfish here) my retirement portfolio?

Interestingly, it is starting to look like the government shutdown, if it runs for weeks instead of months, might have almost no effect on the economy at all. Why? The economic impact that had economists worried was the loss of income suffered by tens of thousands of federal employees. But the Defense Department has continued paying all of its civilian personnel, simply by declaring all of them “essential employees.” Not only were the leaders of the House of Representatives not inclined to argue; they have quietly passed legislation that would give back-pay to all federal workers who have been furloughed, just as soon as the stalemate ends. The Senate and the President are likely to go along, giving the country the worst of all worlds: paying most government employees for staying home and not providing a wide variety of services to the public.

Ironically, the way the politics are working, one can almost guarantee that there will be some kind of a stock market selloff before the shutdown ends. For the Republican leaders in the House, there is little cost to holding their ground so long as there is not a public outcry and loss of voter confidence. One of the sources of that pain would be a big drop on Wall Street. Indeed, if you listen closely to the speeches by President Obama and the Democratic leadership, you hear dire warnings that the of a market drop as a result of the shutdown–which is their way of focusing the public’s attention on who to blame when it happens.

What is interesting about that is that the markets often deliver corrections after long, accelerating uptrends like what we have experienced in the U.S. since March of 2009, and with the 20+% returns that Wall Street has delivered so far this year. It wouldn’t have surprised anyone to see some kind of a quick downturn this Fall regardless of whether the government was operating at full capacity or at a standstill. A week of small leaks in stock prices could lead to something larger as people realize they are sitting on nice gains and have no idea what Congress will or won’t do next. The last time the government was shut down, stocks dropped 20%, the Republican leadership realized it wasn’t winning any popularity contests and the stalemate ended. We’ve seen this script before.

A more consequential issue is the debt ceiling. Congress must raise the total amount that the U.S. government can borrow (by selling Treasury bonds) to pay its various obligations, including, of course, interest on its current Treasury bonds. Contrary to popular belief, raising the debt ceiling does not increase the federal debt; that debt exists whether or not Congress authorizes additional borrowing.

Failure to authorize the government to pay its legal obligations would create a self-induced fiscal crisis–ironic for a country whose representatives claim that they never want to become another Greece, and then talk about voluntarily defaulting on the nation’s debt obligations, which even Greece has avoided.

One recent article suggested that a default on Treasuries would ripple through the global economy, among other things, causing anxious investors to demand higher interest rates and dramatically raising U.S. borrowing costs. That, in turn, would raise rates on mortgages, credit cards and student loans, pushing the U.S. toward or into recession and putting pressure on the stock market. One report suggests that if the U.S. misses just one interest payment, the downward impact on stock prices would be greater than the Lehman Brothers bankruptcy. In THAT aftermath, the stock market lost half its value.

Bigger picture, a default would undermine the role of the U.S. in the world economy.

The irony of the debt ceiling debate is that the gap between government spending and tax revenues has been closing rapidly on its own. In July, the Congressional Budget Office reported that the deficit had fallen by 37.6%, the result of tax increases and sequester-related cuts in spending. As a percentage of America’s GDP, the deficit has fallen from more than 10% at the end of 2009 to somewhere around of 4% currently. Last June, the government actually posted a surplus of $117 billion, paying down the overall deficit, and the Congressional Budget Office has projected that September will also bring government surpluses.

Most observers seem to think that all of this will get worked out. After all, what rational person–in Congress or elsewhere–wants to self-impose these problems when we have plenty of economic challenges already? The stock market’s calm trading days tell us that investors expect a compromise on the government shutdown in the near future. It may take a sharp day of selling to prod Congress off the dime. Foreign investors are still lending to the U.S. government at astonishingly low interest rates (despite modest increases over the past week), which tells us they aren’t worried about a default.

The last time we went through this, the stock market plunges proved to be buying opportunities for investors. One of the great things about uncertainty and volatility is that it causes investments to periodically go on sale, and creates such anxiety that only disciplined investors are able to take advantage. There’s no reason to think this isn’t more of the same.

Sources:

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/10/06/maybe-the-government-shutdown-wont-clobber-the-economy-after-all/

http://www.cbsnews.com/8301-505123_162-57606253/debt-ceiling-understanding-whats-at-stake/

http://krugman.blogs.nytimes.com/2013/08/13/what-people-dont-know-about-the-deficit/

http://www.moneynews.com/newswidget/default-Catastrophe-lehman-demise/2013/10/07/id/529564?promo_code=125A8-1&utm_source=125A8Moneynews_Home&utm_medium=nmwidget&utm_campaign=widgetphase1