Planning For Market Uncertainty in Retirement

For investors, 2017 proved to be a rewarding year. The S&P 500 index rose by more than 20 percent, and the Dow Jones Industrial Average surged past both the 20,000 and 25,000 thresholds in a single year.

The trend of strong market returns has continued throughout January. The bull market that began in March 2009 continues to push forward, despite ongoing speculation from financial professionals that equity markets could be overvalued.

The real question is: How long will the market continue to rise and when will equity markets reach their peak? No one can provide a definitive answer, as market forces and fluctuations in value are largely beyond our control.

Cycling through History

Although historical performance is limited in its predictive ability, past performance does provide us with significant context for understanding big-picture trends. Recent history illustrates that a strong, sustained bull market often precedes a correction bear market, as inflated equity markets return to a more stable valuation and investor confidence begins to wane.

The decade-long bull market of the 1990s began to reverse course in 2000 in the wake of the “dot-com” bubble burst and the emergence of several major accounting scandals (in particular, Enron and Arthur Andersen). The once-burgeoning technology industry was especially hard-hit, with the NASDAQ losing 39% of value in 2000 (followed by losses of 21% and 31% in 2001 and 2002, respectively). The Dow also decreased by more than 27 percent during this three-year window.

Equity markets began to bounce back in late 2002, ushering in a new bull market that was sustained through late 2007. At this point, the sub-prime mortgage crisis (among other factors) led to the most drastic correction market since the Great Depression. All three major indices lost more than 50% of their value in 17 months (between October 2007 and March 2009).

Although we have knowledge of market cycles, we cannot say with certainty what the future holds. For this reason, it is critical for you to be prepared for the possibility of a bear market – especially if you are approaching retirement or are currently living on retirement investment assets today.

Figure 1. Performance of the S&P 500 index, Jan 1998 through Jan 2018.

Navigate Uncertainty with Preparation and Prudence

Above all, the most effective way to prepare for uncertainty in equity markets is to plan well in advance for your needs and priorities during retirement. To develop the “stepping stones” for future retirement success, we recommend that clients and their family members begin to work through the planning process with an advisor at least 8-10 years prior to their desired retirement date.

In our experience, the most effective retirement plans share two main characteristics: (1) a conservative draw rate and (2) a realistic, long-term approach to budgeting. With these provisions in place, you can build a strong, sustainable foundation for your financial success throughout retirement.

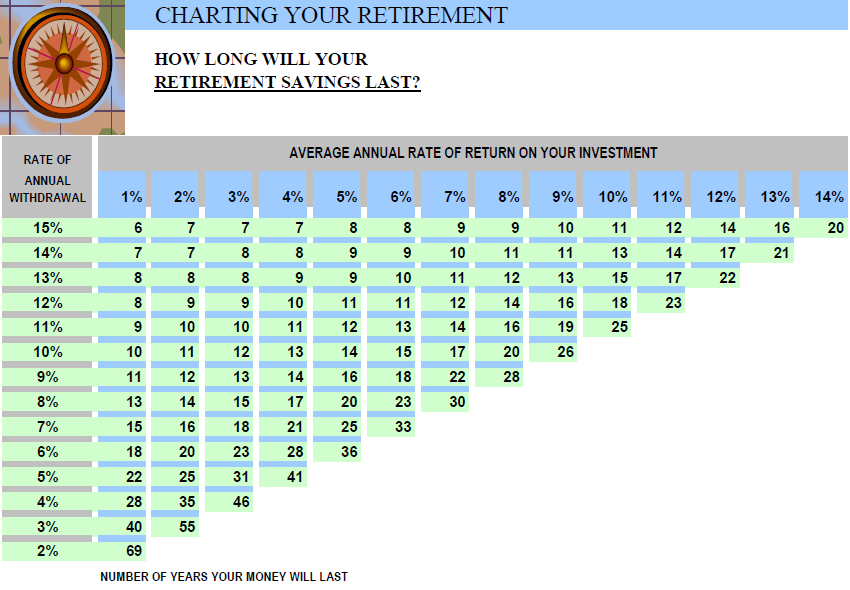

1. Be conservative when selecting your withdrawal rate. After working hard and accumulating assets throughout your lifetime, you will finally enter the asset distribution phase of life during retirement. As you begin to take distributions from your IRAs, 401(k)s and other investment accounts, you should exercise prudence when selecting your rate of withdrawal.

Your ideal withdrawal rate will vary based on your desired lifestyle (expenses) and your available asset base (income). That being said, we have generally seen great long-term success with a conservative draw rate of 4-5 percent.

When you begin to exceed 5 percent – especially once you enter the 7-9 percent range – it is likely that your withdrawal rate is not sustainable for the duration of your retirement. A high withdrawal rate – especially early in retirement – could cause your asset base to deteriorate at an alarming pace. As a result, you may find it difficult to meet expenses in your later years (especially with rising health care costs and uncertain market conditions).

Figure 2. Conservative draw rates can extend the lifespan of your retirement savings, regardless of fluctuations in the market.

2. Be realistic when developing your retirement budget. A detailed and well-thought-out budget for your retirement lifestyle is the key to determining your ideal withdrawal rate. Once you appreciate the full extent of your short-term spending priorities and long-term expenses throughout retirement, you can compare that figure to your asset base to determine the best withdrawal rate for your situation.

Apart from selecting a withdrawal rate that is too high, the biggest mistake you can make in retirement is to underestimate your expenses up front. When a retiree fails to plan for the inevitable costs that loom in their future, he or she will often take additional withdrawals beyond their predetermined distribution – which, in turn, threatens the long-term viability of their retirement savings.

Because budgeting is so crucial for promoting a sustainable retirement lifestyle, it is in your best interest to regularly consult with a financial expert to prevent overlooking key considerations and making costly mistakes.

As the current bull market enters its ninth year, we must not be lulled into a sense of false optimism or complacency. Our knowledge of market trends suggests that a bear market looms on the horizon; it is a matter of when, not if. Although the constant flux of market forces is beyond our control, you do have control over your expense budgeting and retirement income distributions.

While the specifics of your plan are dependent on your personal circumstances, the correct course of action when planning for your retirement lifestyle is preparation and prudence. With adequate foresight and consistent guidance from your advisory team, you can feel confident that your draw rates and spending habits will be sustainable throughout your golden years – regardless of the uncertainty that exists in the market.